Majors forecasts: EUR/USD to peak relatively soon as Fed could turn "hawkish"

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

13 January 2021

Majors forecasts: EUR/USD

to peak relatively soon as

Fed could turn “hawkish”

Andreas Steno Larsen | Jan von Gerich

We see EURUSD peaking in the first half of 2021 as the USD yield curve is

still alive. The Fed could be tempted to “taper” formally already this year

and a hike in 2022 is clearly not out of the question. The ECB will remain

accommodative.

Highlights:

• Strong growth and inflation already during H1-2021

• EUR/USD could peak around 1.25-1.27 already during the first half of this year

• The USD curve has more steepening potential, while the potential is very modest

in the EUR curve

• The Fed is not as dovish as anticipated and a taper process could be launched

already this summer

Global: A growth “ketchup eect” and (headline) inflation upcoming

The manufacturing sector has already started to perform as a result of lagged eects of 2020 stimulus and

low interest rates. If we assume that we are only 4-6 weeks from the seasonal peak in the Covid 19 spread,

paired with a successful vaccine roll-out (news are increasingly upbeat), we will argue that most restrictions

on the service economy will be gone by mid-April or thereabout and momentum towards fewer restrictions

could already begin during March.

e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-

soon-as-fed-could-turn-hawkish

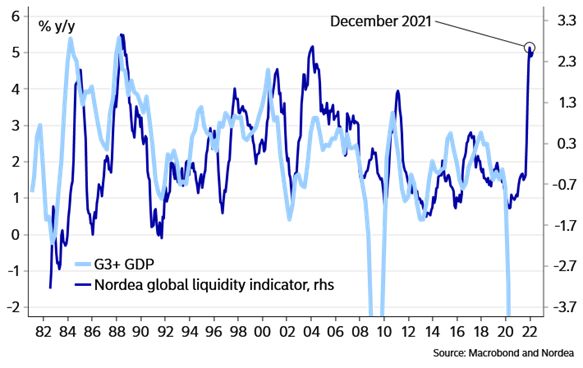

Chart 1. Super strong nominal growth this year as a lagged eect om stimulus from 2020 This could lead to a benign economic scenario for the first half of this year with a strong re-opening momentum in the service economy paired with a continued momentum in the interest rate sensitive manufacturing sector. This could lead to a solid nominal growth pace in 2021 and we also see a possible inflation pressure (mostly in the US) following it. Usually, long bond yields tend to pick-up when nominal GDP growth is strong, but the USD curve should be (clearly) most sensitive to this storyline. EUR/USD could consequently peak during the first half of this year because of a wider USD-EUR interest rates spread. e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-soon-as-fed-could-turn-hawkish

Chart 2. Inflation pressure upcoming in the US? FX: EURUSD to peak in the first half of 2021 We have warned in recent quarters about the risk of a much weaker USD alongside the rebound in the global economy that would follow after the malaise in Q2-2020. The story has unfolded broadly speaking with a weakening USD against EUR, EM and Scandis as we had anticipated. The consensus surrounding further USD weakness is now striking and most, if not all, expect the USD to weaken further. There are sound arguments behind such a view, most notably the massive double deficit of the United States, but it also seems as if everyone is already positioned for the USD weakness, which could mean that the story is already mostly baked in to market prices. In 2017/2018, EUR/USD rose towards 1.25 before reversing lower because of the US once again outpacing the Euro area on growth and interest rates. We are starting to see the contours of a similar develop in to the second half of 2021. A too strong EUR will turn into a slight headache for European exports, while the US looks ripe for a solid economical comeback meanwhile. We accordingly adjust our forecast to reflect this, and expect a peak in EURUSD during first half of 2021 around the 1.25-1.27 area before a reversal longer alongside higher spreads between USD and EUR interest rates. e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-soon-as-fed-could-turn-hawkish

Chart 3. Could 2020/2021 turn into a mirror image of 2017/2018 in EURUSD? Emerging markets countries have been on the receiving end of inflows after the Biden election victory and due to positive vaccine news. We expect continued EM performance during the first half of this year, while we also find that high-beta currencies such as Scandi FX, NZD and AUD will continue to perform against both EUR and USD until a reversal of the USD trend occurs alongside higher USD interest rates. GBP remains a tricky case and it is not carved in stone that GBP strengthens on the heels of a semi-lukewarm Brexit deal. Trade in goods was secured on tari free terms, but trade will not be frictionless and the whole service sector is still left partly in the dark. We see risks of a disappointing Q1 for GBP but do also acknowledge that GBP looks cheap in a historical perspective. e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-soon-as-fed-could-turn-hawkish

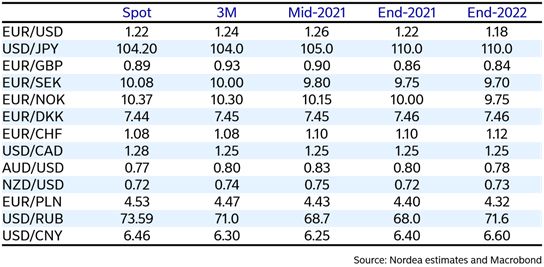

Chart 4. Which currencies gain from vaccine news? We adjust SEK and NOK forecasts in a positive direction, while we expect EUR/USD to peak around 1.25-1.27 during the first half of 2021. The forecasts are presented below. Table: New FX forecasts e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-soon-as-fed-could-turn-hawkish

Fed: A hike in 2022 and a tapering process launched in summer 2021 The Fed is not as dovish as anticipated by many and there are already signs of a forthcoming discussion on the QE pace. It will be interesting to see how the Fed tackles this discussion since a “taper-tantrum” needs to be avoided. Various indicators hint of >2% PCE core price prints during the spring of 2021, which will likely lead the markets to test the Fed AIT regime, since the Fed has not truly launched an AIT-regime in our view. The first step for the Fed is to get rid of the promise to buy at a minimum pace in the QE program and introduce flexibility along the lines that the ECB has done in the PEPP program. Several FOMC members have hinted that they need to re-assess policy as soon as inflation has printed above 2% for some months in a row and even the über-dovish member Kashkari has explicitly written that he would support a hike with 12 consecutive prints of 2% or more in core inflation. Currently no one is willing to talk about the possibility of a rate hike already in 2022 from the Fed, but we find it likely that markets will at least chase the story in to the summer of 2021 since the combo of high growth and increased inflation during Q2, will push the Fed to debate the current policy mix. We add a rate hike from the Fed around mid-2022 to our forecast profile and find that the Fed will start a formal tapering of asset purchases around summer 2021. Chart 5. No one’s willing to bet on a Fed rate hike yet ECB bond purchases to continue for longer but at a slower pace The ECB delivered another sizable easing package in December, including a EUR 500bn expansion in the Pandemic Emergency Purchase Programme (PEPP) and an extension in its duration to at least the end of March 2022. We see a good chance that this was the last major expansion and extension in the e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-soon-as-fed-could-turn-hawkish

programme. After all, the ECB has linked the programme to the coronavirus crisis phase, and we think it will be hard to argue that the crisis phase is still ongoing in early 2022. The end of net PEPP purchases does not mean the end of net purchases altogether. The Asset Purchase Programme (APP) also continues at a monthly volume of EUR 20bn, and we expect the ECB to move at least some of the flexibility of the PEPP into the APP later this year, when it concludes its strategy review. The ECB could then continue net asset purchases also beyond March 2022, but the focus will shift back to the APP. Purchases will likely be sizable still in the first half of this year, when bond issuance needs are large, but the peak pace of the purchases is likely already behind and the pace will gradually fall. The falling pace of purchases will reflect the proceeding economic recovery but also a compromise between the more dovish and hawkish members of the Governing Council, with the latter group actively reminding that the PEPP needs to be only a temporary tool. Since the ECB has not set any purchase pace targets for the PEPP, it can allow the pace to fall relatively silently without having to make an explicit decision at a monetary policy meeting. This could make the ECB’s exit strategy somewhat easier. The ECB as already taken a more flexible approach to its purchases. Rather than buying a specific amount of bonds every month, the central bank will purchase flexibly according to market conditions and with a view to preventing a tightening of financing conditions that is inconsistent with countering the downward impact of the pandemic on the projected path of inflation. Preserving a tightening of financing conditions is probably a relative concept, meaning the ECB would tolerate a gradual rise in longer bond yields, if they reflected a rebounding economy and higher inflation expectations. We do not expect the ECB’s policy to be on autopilot going forward. While no bigger decisions are probably needed in the first meetings of the year, the terms of the Targeted Longer-Term Refinancing Operations (TLTROs) will probably be eased further later this year, while the tiering multiplier could be raised. Further, the ECB’s strategy review will be an important exercise, which should be concluded during the second half of this year. We do not expect the ECB to cut its deposit rate further. e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-soon-as-fed-could-turn-hawkish

Chart 6: Peak bond purchases already behind Rates: US curve steepness to peak later this year The notable economic recovery we expect to materialize later this year still leaves plenty of steepening potential on yields curves, especially in the US, where the recovery is likely to be stronger and the Fed quicker to make changes to its policies compared to the ECB. We expect the Fed to hike rates already in 2022, and curves normally start to flatten clearly before the first rate hike. As a result, we expect the US curve to reach its peak steepness later this year and start to flatten next year. We do not think the markets will be quick to price in any rapid or long-term Fed hiking cycle, and questions about how high rates the economy can handle will probably increase, as longer rates continue to climb. As a result, we do not see the US 10-year yield climb above 2% next year either, even if the Fed starts to raise rates. In the Euro area, any monetary policy normalization will be much farther away than in the US. The ECB will continue its net bond purchases throughout our forecast horizon, but the pace of the purchases will likely gradually recede and the ECB will tolerate slightly higher bond yields, as long the rise takes place gradually and reflects and an improving economic and inflation outlook. We expect the German 10-year yield to climb to zero by the end of next year, which still looks very depressed in a historical context. e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-soon-as-fed-could-turn-hawkish

Chart 7. German yields not followed US ones higher lately Our new forecasts for German benchmark yields e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-soon-as-fed-could-turn-hawkish

Our new forecasts for US benchmark yields Andreas Steno Larsen Jan von Gerich Chief Global FX/FI Strategist Chief Analyst andreas.steno.larsen@nordea.com jan.vongerich@nordea.com +45 55 46 72 29 +358 9 5300 5191 e-markets.nordea.com/article/62773/majors-forecasts-eur-usd-to-peak-relatively-soon-as-fed-could-turn-hawkish

You can also read