The Rising Interest Rate Environment of 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Rising Interest Rate Environment of 2022

By Rajesh Chainani (RC), Senior Vice-President PMA Financial Network MAY 10, 2022

WHAT A DIFFERENCE A YEAR MAKES

Last year (on 5/6/2021) short-term treasury rates (rates 12 months or less) were about as close to zero

percent as one can get (with the one-month rate trading at a negative yield of -0.003%), and there was zero

anticipation of a Federal Open Market Committee (FOMC) decision to raise interest rates.

Just one year later, the FOMC have become inflation fighters and in their decision to raise rates for the

second time in 2022, they elected to raise the Fed Funds rate by 50 basis points to 0.75% to 1.00%. This

was the most aggressive move made by the Fed since 2000.1

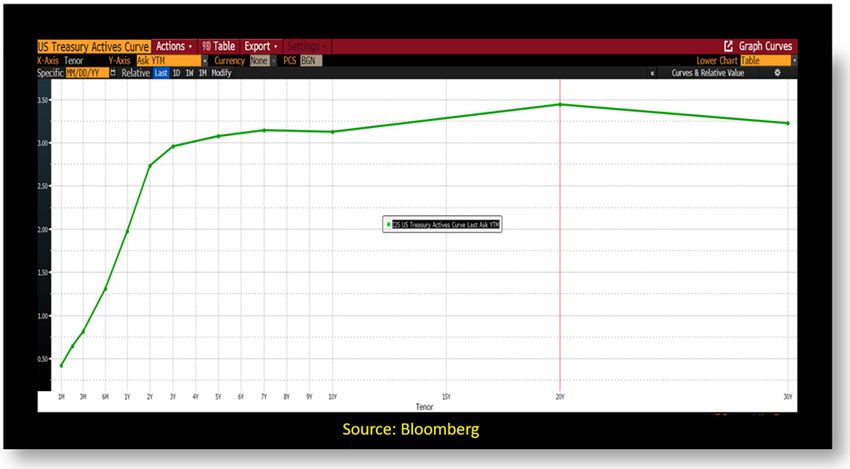

As Figure 1 clearly shows, short-term rates have significantly increased due to both the Fed decisions and

what the market now expects the Fed to continue to do moving forward (Figure 2). The 12-month Treasury

Bill (T-Bill) is now trading at 1.97% (as of 5/6/2022) compared to 0.04% last year.

FIGURE 1- DIFFERENCE IN YIELDS (UP TO 1 YEAR) 5/6/2021 COMPARED TO 5/6/2022

Source: Bloomberg

THE RISING INTEREST RATE ENVIRONMENT OF 2022 CONT.

FIGURE 2- FED FUNDS FUTURES AS OF 5/6/2022

Source: Bloomberg

EXPECTATIONS MOVING FORWARD

Based on current Fed Funds Futures, the expectation is the Fed will increase rates at the following meetings:

6/15/2022-50 basis points (0.50%)

7/27/2022-50 basis points (0.50%)

9/21/22- 25 or 50 basis points (0.25% or 0.50%)

11/2/22- 25 basis points (0.25%)

12/14/22- 25 basis points (0.25)

The following must be stressed as we review these expectations- Things can change rapidly from one day

to the next.

THE RISING INTEREST RATE ENVIRONMENT OF 2022 CONT.

THOUGHTS DURING THIS SHIFT TO A RISING INTEREST RATE ENVIRONMENT.

If we are discussing mortgage rates, the time to lock in that fixed rate may have past for most (but not all).

Mortgage rates for a traditional 30-year mortgage are currently in the 5% to 6% range (depending on many

factors rates can be even higher), which is the highest since 2009.2 With inflation continuing to be a major

focus of the Fed, these levels may rise even higher. In my opinion, this could be an interesting area for

the Fed to monitor as it attempts a “soft landing” (controlled slowdown of the economy without the risk

of a recession).

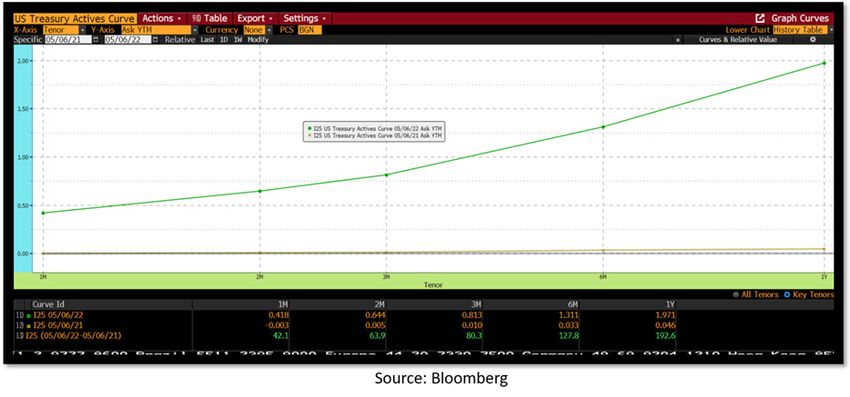

Investing strategies also need to be reevaluated as things continue to change. Figure 3 shows the current

Treasury curve from 1 month to 30 years. While the yield curve has steepened significantly from 1 month to

3 years, it is relatively flat (very little pick-up in yields) from 3 to 20 years.

FIGURE 3- CURRENT TREASURY YIELD CURVE

Source: Bloomberg

For most local governments (school or municipal entities), investing to 20 years is not a typical practice

and not one that is recommended by this article. The important (and most common) question from most is

“Should we stay liquid to “ride the increases” or lock in some aggressive rates and take advantage of what

is available now?”

THE RISING INTEREST RATE ENVIRONMENT OF 2022 CONT.

There are many factors to consider including (but not limited to)

The fixed rates that are available now.

The liquid rates that are also available.

How quickly could the liquid rates rise with the Fed moves.

It is important to note that the Treasury rates available as of 5/6/2022 are “anticipating” the Fed’s next

moves. They are more of a leading indicator of where rates are potentially heading. If expectations change,

so will the levels available. The markets are dynamic, not static.

Liquid rates on the other hand, typically lag the Fed movements by about 1-2 months (depending on many

individual factors such as the average length of portfolio, etc.). Per a recent Forbes Advisor article,

“Yields on banking products like certificates of deposit (CDs) and high-yield savings accounts tend to show

a delayed reaction to increases in the federal funds rate. Eventually, the annual percentage yield (APY) on

these products will rise after the Fed hikes rates, but the gains lag the interest rate increases by weeks, if not

months.” (Smith, 2022).

Hence waiting for the increase to kick in could cost your organization more (in lost interest earning) than

taking the available fixed rate available at that moment, depending on the factors that were noted earlier.

Here is an example of a break-even analysis of how rapidly liquid rates will have to increase to

outperform a six-month Treasury Bill available on 5/5/2022:

Fixed Investment

Principal Net Rate Settlement Maturity Term Interest Earnings

$1,000,000.00 1.25% 05/05/22 11/03/22 182 $6,232.88

Liquid Investment

Principal Avg Liquid Rate Settlement Maturity Term Interest Earnings

$1,000,000.00 0.75% 05/05/22 06/16/22 42 $863.01

$1,000,863.01 1.25% 06/16/22 07/28/22 42 $1,439.60

$1,002,302.61 1.75% 07/28/22 09/22/22 56 $2,691.11

$1,004,993.73 2.00% 09/22/22 11/03/22 42 $2,312.86

Total 182 $7,306.59

Liquid rates will need to increase immediately (which is not typical based on historic performance of liquid

rates) with the anticipated Fed moves to the “lower band” of the Fed Funds rate to outperform the six-

month fixed investment. And that is if the Fed does not change its outlook.

As the old saying goes, “A bird in hand is worth two in the bush.”

References:

1 Siegel, R., & Bhattaraj, A. (2022, May 4). Fed hikes rates by half a percentage point in fight against inflation.

The Washington Post. Retrieved from https://www.washingtonpost.com/us-policy/2022/05/04/fed-rate-

hike-inflation-may/

2 The Associated Press. US mortgage rates rise; 30-year at 5.27%, highest since 2009. (2022, May 3).

Retrieved from https://abcnews.go.com/US/wireStory/us-mortgage-rates-rise-30-year-527-

highest-84521792

Smith, K. A. (2022, March). How The Fed’s Interest Rate Hike Will Affect Savings Accounts. Forbes Advisor.

Retrieved from https://www.forbes.com/advisor/banking/fed-rate-increase-savings-accounts/

Rajesh Chainani

Senior Vice President, Director

PMA Financial Network, LLC

717-519-5922

rchainani@pmanetwork.com

Securities, public finance services and institutional brokerage services are offered through PMA Securities, LLC. PMA Securities, LLC is a

broker-dealer and municipal advisor registered with the SEC and MSRB, and is a member of FINRA and SIPC. PMA Asset Management, LLC,

an SEC registered investment adviser, provides investment advisory services to local government investment pools. All other products and

services are provided by PMA Financial Network, LLC. PMA Financial Network, LLC, PMA Securities, LLC and PMA Asset Management, LLC

(collectively “PMA”) are under common ownership.

Securities and public finance services offered through PMA Securities, LLC are available in CA, CO, FL, IL, IN, IA, MI, MN, MO, NE, NY, OH,

OK, PA, SD, TX and WI. This document is not an offer of services available in any state other than those listed above, has been prepared for

informational and educational purposes and does not constitute a solicitation to purchase or sell securities, which may be done only after client

suitability is reviewed and determined. All investments mentioned herein may have varying levels of risk, and may not be suitable for every

investor. PMA and its employees do not offer tax or legal advice. Individuals and organizations should consult with their own tax and/or legal

advisors before making any tax or legal related investment decisions. Additional information is available upon request.

For more information visit www.pmanetwork.com

©2022 PMA Financial Network, LLC

You can also read