Märkte und Wandelanleihen in 2021 - "Quo vadis?" - Lazard ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Märkte und Wandelanleihen in 2021 – „Quo vadis?“

28. Januar 2021, um 15.00 Uhr

Werner Krämer, CEFA

Geschäftsführer & Economic Analyst bei

LAM Deutschland

Arnaud Brillois

Managing Director, Portfolio Manager/Analyst

LAM LLC (New York)

Bitte nehmen Sie zur Kenntnis, dass die folgende Präsentation aufgezeichnet wird.

Informationen und Meinungen, die im Folgenden diskutiert werden, stellen keine Anlageberatung dar. Jegliche erwähnte Wertpapiere

müssen nicht zwangsläufig von Lazard Asset Management gehalten noch als Kaufempfehlung oder Kundenwerbung verstanden

werden. Alle geäußerten Meinungen sind unverbindlich.

_______________________________________________________________

Please note today’s presentation is being recorded.

Please note, the information and opinions discussed today do not constitute investment advice. Any securities mentioned are not

necessarily held by Lazard Asset Management, and should not be considered a recommendation or solicitation to buy or sell those

MC33854 securities. All opinions expressed are subject to change.

Märkte und Wandelanleihen in 2021 – „Quo vadis?“ Werner Krämer, Geschäftsführer & Economic Analyst 28. Januar 2021

Makro-Ausblick

Vier Dekaden fallende Renditen

Seit 1981 fallen die Renditen von (sicheren) Staatsanleihen und

haben in 2020 historische All-Zeit-Tiefs erreicht.

Quelle: Refinitiv Datastream, Stand 22.01.2021

4 Lazard Asset Management

Renditen von Euroland Staatsanleihen unattraktiv

Bei Euroland-Staatsanleihen finden sich kaum noch Renditen

oberhalb der Null.

Quelle: Refinitiv Datastream, Stand 22.01.2021

5 Lazard Asset ManagementEWU ein gemeinsamer Risikoraum?

Die Märkte haben mittlerweile eingepreist, dass es bei den

Staatsanleihen der Eurozone kein länderspezifisches Creditrisiko

mehr gibt, dass man differenzieren könnte.

Quelle: Refinitiv Datastream, Stand 22.01.2021

6 Lazard Asset ManagementEnge Credit-Spreads

Auch die Renditen von Unternehmensanleihen notieren nahe der

historischen Tiefs, unter dem Vorkrisenniveau.

Quelle: Refinitiv Datastream, Stand 22.01.2021

7 Lazard Asset ManagementZinsanlagen in der Eurozone

▪ Staatsanleihenrenditen niedrig oder negativ

▪ Zinsstrukturkurven flach

▪ Credit-Spreads eng

▪ Schwieriges aktives Management von € Portfolios ohne

Risikopuffer

Die Anleger suchen nach Alternativen

8 Lazard Asset ManagementHyperexpansive Geldpolitik

Wichtiger Einflussfaktor für die Negativzinsen und die Eliminierung

eingepreister Risiken sind die Zentralbanken mit ihrer

hyperexpansiven Geldpolitik und massiven Wertpapierkäufen. Dies

treibt die Assetpreise, fast unabhängig von der Realwirtschaft.

Quelle: Refinitiv Datastream, Stand 22. Januar 2021

9 Lazard Asset ManagementWas kann den geldpolitischen Supercycle

stoppen?

Solange keine Inflation auftritt, können Geld- und Fiskalpolitik hyperexpansiv

bleiben. Sollte die Inflation aber auch außerhalb der Assetpreise zurückkehren,

steht uns ein harter Test der Unabhängigkeit der Zentralbanken bevor.

Quelle: Refinitiv Datastream, Stand 22. Januar 2021

10 Lazard Asset ManagementWoher könnte Inflation kommen?

▪ Geldmengenexpansion

▪ Staatsverschuldung

▪ Politisierung der Zentralbank

▪ Rohstoffpreise

▪ Rückgestaute Nachfrage

▪ Sinkendes Angebot (Dauerlockdown)

▪ Mehr (teurer) Staat

▪ Überregulierung

▪ De-Globalisierung

▪ Monopolisierung/Oligopole

▪ Klimawandelkosten

Inflationierungskräfte werden stärker

Quelle: Refinitiv Datastream, Stand 22. Januar 2021

11 Lazard Asset ManagementKonsequenz - Flucht in die Sachwerte

Die Aktienmärkte sind in starker Verfassung und dem „TINA“-

Argument ist nicht wirklich zu widersprechen, aber relativ zur

eigenen Historie sind sie hoch bewertet.

Quelle: Refinitiv Datastream, Stand 22. Januar 2021

12 Lazard Asset ManagementWelche Assetklassen?

▪ Skandi Fixed Income (Safe Assets)

▪ Global Fixed Income (Safe Assets)

▪ Emerging Markets Debt (Spread)

▪ Global Convertibles (Safer Risk Assets)

▪ Global Quality Equity (Safer Risk Assets)

▪ Emerging Markets / Asian Equities (antizyklisch)

Will man als Anleger noch eine Chance auf Erträge

haben, muss man besondere Risiken nehmen:

Währungen, Aktien, Optionen (Konvexität), Illiquidität,

Komplexität.

13 Lazard Asset ManagementConvertible Bond Market Update Arnaud Brillois, Managing Director, Portfolio Manager/Analyst 28. Januar 2021

Lazard Convertible Global | PC H EUR

Recent performances

CONVEXITY

Convexity is a specific feature of convertible bonds

This differentiates them from a simple diversification through bonds and equities

We tend to favour bonds with equity exposure between 20% and 65% as this is where we have observed convexity at its the greatest

Total YTD 140

2020 PERFORMANCE1 Performance

130

Lazard Convertible Global PC H EUR, net of fees

+32.72% 120

(Hedged in EUR)

110

Refinitiv/Thomson Reuters Convertible Global Focus

hedged Index +21.49%

100

(Hedged in EUR)

2019/12/31 = 100

Excess Return versus Benchmark +1123 bps 90

80

MSCI ACWI nd

+12.52%

(Hedged in EUR)

70

Dec- Jan- Feb- Mar- Apr- May- Jun- Jul- Aug- Sep- Oct- Nov- Dec-

19 20 20 20 20 20 20 20 20 20 20 20 20

ICE BofA Global High Yield Index (Hedged in EUR) +4.78% Lazard Convertible Global PC H EUR

Thomson Reuters Convertible Global Focus H EUR

MSCI ACWI H EUR

ICE BofA Global High Yield H EUR

(1) Performance period from 31 December 2019 to 31 December 2020.

Past performance does not guarantee future performance. Performances vary. Performances are net-of-fee (excluding possible buying fees charged

by the distributor), but are gross of fees and taxes applicable to an average retail client (with Belgian residence). Performances of less than one year

are disclosed for information only. The return may increase or decrease as a result of currency fluctuations.

Source: Lazard, Bloomberg, MSCI, Refintiv/Thomson Reuters, ICE

15 Lazard Asset ManagementLazard Convertible Global | PC EUR

Recent performances

CONVEXITY

Convexity is a specific feature of convertible bonds

This differentiates them from a simple diversification through bonds and equities

We tend to favour bonds with equity exposure between 20% and 65% as this is where we have observed convexity at its the greatest

Total 140

2020 PERFORMANCE1 Performance

130

Lazard Convertible Global PC EUR, net of fees

+26.18% 120

(in EUR)

110

Refinitiv/Thomson Reuters Convertible Global Focus

Index +15.04%

100

(in EUR)

2019/12/31 = 100

Excess Return versus Benchmark +1114 bps 90

80

MSCI ACWI nd

+6.65%

(in EUR)

70

Dec- Jan- Feb- Mar- Apr- May- Jun- Jul- Aug- Sep- Oct- Nov- Dec-

19 20 20 20 20 20 20 20 20 20 20 20 20

ICE BofA Global High Yield Index (in EUR) -0.89% Lazard Convertible Global PC EUR

Thomson Reuters Convertible Global Focus

MSCI ACWI

ICE BofA Global High Yield Index

(1) Performance period from 31 December 2019 to 31 December 2020.

Past performance does not guarantee future performance. Performances vary. Performances are net-of-fee (excluding possible buying fees charged

by the distributor), but are gross of fees and taxes applicable to an average retail client (with Belgian residence). Performances of less than one year

are disclosed for information only. The return may increase or decrease as a result of currency fluctuations.

Source: Lazard, Bloomberg, MSCI, Refintiv/Thomson Reuters, ICE

16 Lazard Asset ManagementAn Active Management

Of the Various Performance Drivers

140 EQUITY RISK 3,50 MODIFIED DURATION 5,00%

130 70,00% Switch to

3,00 higher modified

120 duration 4,00%

110 60,00% 2,50

100 3,00%

50,00% 2,00

90

1,50 2,00%

80 Re-risking 40,00%

70 De-risking 1,00

60 1,00%

30,00% 0,50

50

40 20,00% - 0,00%

Apr-20

Dec-19

Dec-20

Aug-19

Nov-19

Mar-20

Aug-20

Nov-20

Jul-20

Jul-19

May-20

Jan-20

Jun-19

Jun-20

Oct-19

Feb-20

Oct-20

Sep-19

Sep-20

Modified Duration LCG (LHS) Modified Duration Index (LHS)

MSCI ACWI (LHS) Delta LCG (RHS) Delta Benchmark (RHS)

US 10 year yield (RHS)

EXAMPLE OF SECTOR EXPOSURE ACTIVE MANAGEMENT RECENT TIMELINE: KEY EVENTS

10,0% Reduction Luxury July 2019: Switch to overweight modified duration

Exposure

8,0% Q4 2020: Profit taking on technology

Jan 2020: Discovery of Covid-19. Reduction Luxury sector

6,0%

Profit Taking Feb 2020: Reduction Delta

Switch to Technology

4,0% Underweight March 2020: Underweight delta then overweight after 16th of March

Technology

2,0% Re-exposure April 2020: Increase exposure technology

May 2020: Increase exposure consumer discretionary

0,0%

Sep Okt Nov Dez Jan Feb Mrz Apr Mai Jun Jul Aug Sep Okt Nov Dez June 2020: Increase exposure IG credit in recovery sector (Airlines and

-2,0%

19 19 19 19 20 20 20 20 20 20 20 20 20 20 20 20 Energy)

Information Technology (relative delta vs benchmark) Jul/Aug 20: Targeted take profit in some technology issuers

Consumer Discretionary (relative delta vs benchmark) Sep/Oct 20: Continued build in recovery sectors

As of 31 December 2020. Source: Lazard, Refinitiv/Thomson Reuters, Bloomberg

The portfolio positioning shown on this page is for illustrative purposes only and may change at any time in the investment team’s discretion.

17 Lazard Asset ManagementGlobal Convertible Bond Dynamics

A Market Dominated By US Convertible Bonds

GLOBAL MARKET SIZE BY REGION* GLOBAL MARKET SIZE BY BOND CURRENCY

Japan, 2,8% SGD; 1%

Asia ex-Japan, GBP; 1% CHF; 1%

10,6% HKD; 2%

JPY; 4%

EUR; 20%

Europe,

17,5%

US,

69,1%

USD; 70%

GLOBAL MARKET SIZE BY SECTOR

30%

▪ Technology companies have always been active issuers of 25%

convertible bonds 20%

15%

▪ Sectors impacted by COVID-19 have been active issuers

in 2020. 10%

5%

▪ Strong presence of growth and mid-cap companies (≈60%

0%

of the market)

▪ ≈65% of convertible bond issuers only issue convertible

bonds (versus other security types)

As of 31 December 2020

Source: BofA Merrill Lynch Global Research, Jefferies

*Region of the underlying equity

18 Lazard Asset ManagementGlobal Convertible Bond Dynamics

New Issue Trends

TOTAL NEW ISSUANCES (USD) AVG. SIZE OF NEW ISSUES AVG. INITIAL PREMIUM AVERAGE COUPON

2020 2019 2018 2020 2019 2018 2020 2019 2018 2020 2019 2018

$158.6bn $85.0bn $84.6bn $539mil $436mil $355mil 33.5% 29.9% 28.8% 1.82% 2.44% 1.87%

New Issuance (in USD mm) Net Supply (New Issue – Redemptions)

180.000 200.000

160.000 150.000

140.000 100.000

120.000 50.000

100.000

0

80.000

-50.000

60.000

40.000 -100.000

20.000 -150.000

0 -200.000

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

1999

2004

1998

2000

2001

2002

2003

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

US Europe Asia Japan Issuance Redemptions Net

New Issue Sectors (in USD mm) Use of Proceeds* (2020)

50.000 CapEx Others

45.000 6% 6%

40.000

35.000

30.000 M&A

25.000

5%

20.000

15.000 Refi

10.000 22% GCP

5.000 61%

0

2019 2020

As of 31 December 2020

Source: BofA Global Research

* M&A: Mergers and Acquisitions. GCP: General Corporate Purposes. CapEx: Capital Expenditures

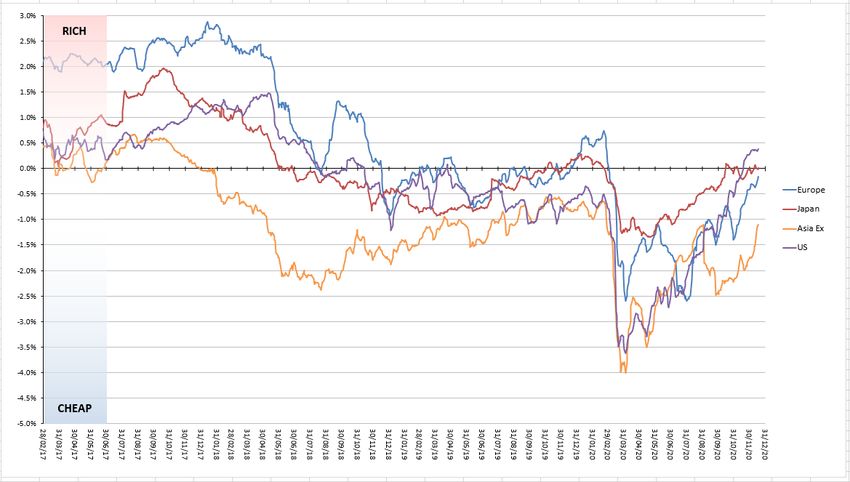

19 Lazard Asset ManagementGlobal Convertible Bonds Valuations

Still undervalued

▪ It is possible to compare the theoretical price (fair value) of a convertible bond to its traded price

▪ This can allow you to asses the cheapness or richness of the convertible bond market

▪ Since March, the convertible bond market reached a record cheapness

FAIR VALUE TRACKER OF GLOBAL CONVERTIBLE BONDS

Sources: Jefferies. As of 18 December 2020.

The opinion expressed above is as of date of this presentation and may change.

20 Lazard Asset ManagementOutlook

Equity exposure: An active management at the subsector level

2020 TYPE OF ISSUER* LARGEST RECOVERY ISSUERS CHANGE VERSUS 2019

10.000

9.000

Others

10% 8.000

7.000

Recovery

6.000

38,08%

5.000

4.000

Lockdown

3.000

winners, 51,55%

2.000

1.000

0

*Recovery: Cons. Disc., Financials, Industrials,Transportation,, Energy

Lockdown winners: Technology, Health Care, Telecom, Media

Others: Utilities, Materials, Cons. Stp.

2019 2020

As of 31 December 2020

Source: BofA Merrill Lynch Global Research, Jefferies

*Region of the underlying equity

21 Lazard Asset ManagementOutlook

Equity exposure: An active management at the subsector level

▪ The convertible bond market today offer potential to obtain exposure to companies

at different stage of the recovery

▪ This allows efficient portfolio management and offers various drivers of returns

Direct Beneficiaries

- E-commerce

- TeleHealth,

First to Rebound - Cyber-security

- Semiconductors - Cloud

- Videogames

- Payment Processors

Recovery

- Airlines

- Cruises

- Events Companies

- Online Travel Agencies

- Energy

*As of 31 December 2020

The opinion expressed above is as of date of this presentation and may change.

Mention of these securities should not be considered a recommendation or solicitation to purchase or sell the securities. It should not be assumed that any

investment in these securities was, or will prove to be, profitable, or that the investment decisions we make in the future will be profitable or equal to the

investment performance of securities referenced herein. There is no assurance that any securities referenced herein are currently held in the portfolio or that

securities sold have not been repurchased. The securities mentioned may not represent the entire portfolio.

22 Lazard Asset ManagementLazard Global Convertibles

Current Positioning

EQUITY SENSITIVITY MODIFIED DURATION NUMBER OF CONVERTIBLES

Strategy Index Strategy Index Strategy Index

63.6% 57.6% 1.83 2.00 81 215

BREAKDOWN BY SECTOR (BY EQUITY SENSITIVITY) BREAKDOWN BY GEOGRAPHIC AREA (BY EQUITY SENSITIVITY)

25% 40% 37,9%

19,7% 35%

20% 18,5%

30%

15%

25%

10% 6,6% 6,2%

4,9% 20%

5% 2,6% 2,1% 14,4%

1,3% 0,3% 15%

0,0% 0,0% 1,3%

0% Banks 10% 8,0%

Discretionary

Materials

Energy

Insurance

Technology

Real estate

Industrials

Communication

Utilities

Health Care

Consumer Staples

Information

Consumer

5% 1,9% 1,3%

Services

0%

US Europe Asia ex Japan Others Japan

Lazard

Lazard Refinitiv/Thomson Reuters Convertible Global Focus (EUR)

Refinitiv/Thomson Reuters Convertible Global Focus (EUR)

BREAKDOWN BY CURRENCY (% NET ASSETS) BREAKDOWN BY PROFILE (% NET ASSETS)

70% 64,0% 80%

60% 68,0%

70%

50% 60%

40% 50%

27,5% 40%

30%

30%

20%

20% 14,3%

10% 5,5% 10% 5,6% 5,8% 6,2%

2,2% 0,8% 0,0% 0,0%

0% 0%

USD EUR JPY CHF GBP HKD Others Equity-Like Mixed Equity Mixed Bond Bond Cash

Lazard Refinitiv/Thomson Reuters Convertible Global Focus (EUR) Lazard Refinitv/Thomson Reuters Convertible Global Focus (EUR)

As of 31 December 2020

Allocations and security selection are subject to change.

Index data shown above is for the Refinitv/Thomson Reuters Convertible Global Focus (EUR) Index.

Source: Lazard, Refinitv/Thomson Reuters

23 Lazard Asset ManagementLazard Global Convertibles

Rating Distribution

COUPON YIELD BOND FLOOR DISTANCE TO AVERAGE CREDIT AVERAGE

BOND FLOOR SPREAD MATURITY

0.5% 93.1% 30.2% 260.0bps 3.6 years

DISTRIBUTION WITHOUT IN-HOUSE RATINGS1 DISTRIBUTION WITH IN-HOUSE RATINGS2,3

70%

60% 25%

50%

40%

… 20%

14%

12% 15%

10%

8% 10%

6%

4% 5%

2%

0% 0%

AAA

AA+

BBB

BB+

AA-

BB-

AA

A+

BB

B+

A-

B-

A

B

D

CCC-

CC

NR

CCC

Cash

CCC+

BBB+

BBB-

AAA

BBB

AA+

AA-

BB+

BB-

AA

BB

A+

B+

A-

B-

A

B

D

CC

CCC

Cash

CCC+

CCC-

BBB+

BBB-

Lazard Refinitiv/TR Convertible Global Focus Lazard Refinitiv/TR Convertible Global Focus

Average rating Average rating Average rating Average rating

BBB- BBB BBB- BB+

As of 31 December 2020. The distribution shown on this page is for illustrative purposes only and may change at any time in the investment team’s discretion. Index data shown

above is for the Refinitv/Thomson Reuters Convertible Global Focus (EUR) Index.

1. Ratings methodology: When calculating the data shown on this slide, the investment team selected the second best issue rating or the second best issuer rating of those

published by the three main rating agencies (i.e., Fitch, Moody’s and S&P).

2. Shadow rating methodology: For issuers that are not rated by any of the three main rating agencies (i.e., Fitch, Moody’s and S&P), the data shown reflects shadow ratings

maintained by the investment team using the Bloomberg DRSK methodology combined with the investment team’s/Lazard’s proprietary in-house methodology.

3. There is no guarantee that the investment team’s ratings methodology will be equally or more predictive of credit quality than that of the ratings agencies.

Source: Lazard

24 Lazard Asset ManagementCurrent Outlook: Convertible Bond Team’s View on the Asset Class

Angle of analysis Driver Our View

Positive outlook for equities during the first half of the year, particularly for the companies still in

the recovery phase, who often present attractive valuations.

Equity Within the companies that benefitted from the lockdowns, such as e-commerce, cloud or internet

security, we focus on the companies that will be able to maintain high revenue growth momentum

and continue to surprise positively at the next two quarterly earnings releases.

Focus on high quality credit to keep stable and elevated portfolio bond floor. Select only

Macroeconomic analysis strongest balances sheets within US energy, global airlines and tourism related activity.

Credit

→ allows the portfolio to display strong convexity in a volatile equity market environment.

Interest Rates ▪ To stabilize around the current levels in the medium term.

▪ We expect the implied volatility to trend upwards as underlying markets are getting more

Volatility volatile.

▪ Will support valuations of convertible bonds through the value of their optionality.

▪ 2021 new issuance to continue at a high pace, in particular from Q2 as issuers will have to

Market analysis Primary

refinance.

▪ We expect steady inflows into the asset class as convertible bonds become particularly

Liquidity

relevant in volatile markets.

The opinions expressed above are as of the date of this presentation and subject to change.

25 Lazard Asset ManagementDisclaimer

Die in dieser Präsentation enthaltenen Informationen beruhen auf öffentlich zugänglichen

Quellen, die wir für zuverlässig halten. Eine Garantie für die Richtigkeit oder Vollständigkeit

der Angaben können wir nicht übernehmen, und keine Aussage in diesem Bericht ist als

solche Garantie zu verstehen. Alle Meinungsaussagen geben die aktuelle Einschätzung

des Verfassers/der Verfasser wieder und stellen nicht notwendigerweise die Meinung von

Lazard oder deren assoziierter Unternehmen dar.

Die in dieser Präsentation zum Ausdruck gebrachten Meinungen können sich ohne

vorherige Ankündigung ändern. Weder Lazard noch deren assoziierte Unternehmen

übernehmen irgendeine Art von Haftung für die Verwendung dieses Vortrages oder deren

Inhalt.

Weder diese Präsentation noch dessen Inhalt noch eine Kopie dieses Vortrages darf ohne

die vorherige ausdrückliche Erlaubnis von Lazard auf irgendeine Weise verändert oder an

Dritte verteilt oder übermittelt werden. Mit der Annahme dieser Veröffentlichung wird die

Zustimmung zur Einhaltung der o.g. Bestimmungen gegeben.

Lazard Asset Management (Deutschland) GmbH, Neue Mainzer Strasse 75, 60311

Frankfurt am Main.

Januar 2021

26 Lazard Asset ManagementYou can also read