Liquidity Landscape November 10, 2020 - Liquidnet

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Liquidity

Landscape

November 10, 2020

Disclaimer

This document is confidential between you and Liquidnet and should not be disclosed to anyone else without Liquidnet’s prior permission. It is published

only for Liquidnet Members, customers, and anyone who has been sent this document directly from Liquidnet. This document is not investment advice or

intended as a recommendation to buy or sell any instrument covered with it. Although the statements within this document are believed to be correct,

they have not been verified by the author and should not be relied upon when considering the merits of any particular investment. A recipient should

consider their own financial situation, investment objectives and seek independent advice, where appropriate, before making any investment. This

document does not and is not intended to constitute legal advice. It is provided on a non-reliance basis and all recipients should seek their own independent

legal advice in relation to the matters discussed in this document. All presented data may be subject to slight variations. All data and figures are Liquidnet

internal data unless stated otherwise.

1

Liquidity Landscape: Post Covid-19 Brexit With the end of the transition period fast approaching and the continued uncertainty regarding the outcome of negotiations, regulators on both sides of the channel continue to look for pragmatic solutions to mitigate any negative effects resulting from a hard Brexit. Both the FCA and ESMA have issued statements on limiting the impact of the Share Trading Obligation. While the UK intend to allow trading to continue as it does today by extending Temporary Transitional Power (TTP) to March 2022,1 ESMA instead are restricting the impact of the STO to ISIN and currency only.2 However, despite the regulators’ efforts to reduce any immediate impact, the industry needs to be aware and prepared for changes that could be in play 1 January 2021. OTC Trade Reporting Following the end of the transition period, trading venues established in the UK will, with effect from 1 January 2021, no longer be considered EU trading venues. Consequently, transactions concluded on UK trading venues would be considered OTC-transactions and subject to the post-trade transparency requirements (Articles 20 and 21 of MiFIR).3 While UK trading venues have been positively assessed as third-country venues provided that they meet all relevant criteria,4 UK SI will not. Trades conducted on UK SI together with OTC activity will now need to be trade reported by both parties, and as such, EU investment firms will need to make public transactions concluded OTC with UK counterparties via an APA established in the EU. There are a number of issues in relation to this; firstly, that any type of reporting by an EU firm does not impact the use of waivers; secondly, there needs to be alignment of the deferral regime to increase harmonisation of reporting and finally ISINs need to be in scope under the DTO (Derivatives Trading Obligation). Share Trading Obligation (STO) In the short term the STO looks to be resolved, but in reality, the issue has merely been kicked down the road. While the UK intend to use the TTP to mitigate any market disruption, they also state clearly that they reject ESMA’s proposal to reduce the scope of the STO to ISIN and currency.5 The UK approach of allowing open markets between trading venues globally is likely to lead to a response from the EU Commission next year when they revisit MiFID II in Q4 2021, given concerns of a liquidity drain to the UK in a similar manner to the outcome of Swiss Equivalence negotiations. 1 https://www.fca.org.uk/brexit/onshoring-temporary-transitional-power-ttp/previous-ttp-updates 2 https://www.esma.europa.eu/sites/default/files/library/esma70-155- 7782_statement_brexit_share_trading_obligation_q42020.pdf 3 https://www.esma.europa.eu/sites/default/files/library/esma70-155- 10962_statement_brexit_mifid_remaining_issues_2020_q4.pdf 4 https://www.esma.europa.eu/press-news/esma-news/esma-adds-uk-venues-opinions-third-country-trading- venues-1 5 https://www.esma.europa.eu/sites/default/files/library/esma70-155- 7782_statement_brexit_share_trading_obligation_q42020.pdf 2

As it stands currently, EU asset managers will still be able to trade dual listed stocks on the LSE in

GBP under the new scope of ISIN plus currency, however dealing in EU instruments traded in

euro will need to be executed on EU venues. Looking at the list of dual listed stocks which

appear to have meaningful activity (>5% of the total shares traded across both lines), out of 36

dual listed stocks starting with an EU27 ISIN, seven names have their main pool of liquidity in the

UK reducing the scope of the EU STO to only two names: Bank of Cyprus and Greencoat

Renewables, both of which are traded in Euros in the UK. This will remain one to watch given that

the FCA also notes its intention to keep its approach under review. In particular, the FCA have

highlighted discussions with market participants on whether or not to keep the current MiFID II

transparency calibrations if equivalence is not achieved.

Exhibit 1: Dual listed EU stocks most likely impacted by EU/UK STO only

EuropeP UKPerc EU % UK %

ISIN Europe UK SWISS TotalVol Names

erc 2020 2020 2019 2019

AT0000641352 1,363,852 100,561 1,464,413 93% 7% 1 1 CA IMMOBILIEN ANLAGEN AG

AT0000652011 14,046,943 1,685,139 15,732,082 89% 11% 1 1 ERSTE GROUP BANK AG

AT0000743059 7,792,625 2,927,078 10,719,703 73% 27% 1 1 OMV AG

AT0000831706 2,805,819 1,178,780 3,984,599 70% 30% 1 1 WIENERBERGER AG

AT0000APOST4 797,796 85,027 882,823 90% 10% 1 1 OESTERREICHISCHE POST AG

BE0003826436 2,243,697 236,996 2,480,693 90% 10% 1 1 TELENET GROUP HOLDING NV

DE000TUAG000 28,641,957 15,511,482 44,153,439 65% 35% 48% 52% TUI AG-DI

ES0171996087 15,883,628 1,651,299 17,534,927 91% 9% 1 1 GRIFOLS SA

ES0177542018 319,411,547 521,772,488 841,184,035 38% 62% 28% 72% INTL CONSOLIDATED AIRLINE-DI

FI0009005987 13,583,518 1,180,915 14,764,433 92% 8% 1 1 UPM-KYMMENE OYJ

FI0009013403 8,717,981 889,249 9,607,230 91% 9% 1 1 KONE OYJ-B

FI4000153309 605,813 521,864 1,127,677 54% 46% 1 1 FARON PHARMACEUTICALS OY

FR0000045072 74,075,316 14,275,958 88,351,274 84% 16% 1 1 CREDIT AGRICOLE SA

FR0000120271 78,755,127 28,942,962 3,920,603 107,698,089 73% 27% 1 1 TOTAL SE

FR0000121972 10,863,903 1,379,233 12,243,136 89% 11% 1 1 SCHNEIDER ELECTRIC SE

FR0000125007 20,256,012 2,142,094 22,500 22,398,106 90% 10% 1 1 COMPAGNIE DE SAINT GOBAIN

FR0010397232 71,910,083 25,172,180 97,082,263 74% 26% 1 1 NOVACYT

IE0000020408 7,883 7,376 15,259 52% 48% 1 1 ABBEY PLC

IE0000669501 4,216,569 326,999 4,543,568 93% 7% 1 1 GLANBIA PLC

IE0001827041 18,053,210 9,267,378 27,320,588 66% 34% 58% 42% CRH PLC

IE0004906560 2,018,672 239,941 2,258,613 89% 11% 88% 12% KERRY GROUP PLC-A

IE0004927939 4,030,097 598,687 4,628,784 87% 13% 86% 14% KINGSPAN GROUP PLC

IE0007214426 430,398 26,353 456,751 94% 6% 1 1 CPL RESOURCES PLC

IE00B1RR8406 7,373,844 3,714,713 11,088,557 66% 34% 62% 38% SMURFIT KAPPA GROUP PLC

IE00B66B5T26 4,332,351 49,959,839 54,292,190 8% 92% 1 1 PROVIDENCE RESOURCES PLC

IE00BD1RP616 53,289,376 5,569,226 58,858,602 91% 9% 1 1 BANK OF IRELAND GROUP PLC

IE00BD5B1Y92 343,247 486,226 829,473 41% 59% 1 1 BANK OF CYPRUS HOLDINGS PLC

IE00BD6JX574 14,754,117 2,137,108 16,891,225 87% 13% 1 1 GLENVEAGH PROPERTIES PLC

IE00BF0MZF04 4,827,418 57,202,429 62,029,847 8% 92% 15% 85% ORMONDE MINING PLC

IE00BF2NR112 9,176,328 63,157,380 72,333,708 13% 87% 42% 58% GREENCOAT RENEWABLES PLC

IE00BWB8X525 473,304 128,278 601,582 79% 21% 90% 10% PERMANENT TSB GROUP HOLDINGS

IE00BWT6H894 1,300,164 2,879,292 4,179,456 31% 69% 35% 65% FLUTTER ENTERTAINMENT PLC

IE00BWY4ZF18 24,225,002 3,221,656 27,446,658 88% 12% 71% 29% CAIRN HOMES PLC

IE00BXC8D038 1,114,891 881,579 1,996,470 56% 44% 42% 56% APPLEGREEN PLC

IE00BYTBXV33 18,991,357 14,068,567 33,059,924 57% 43% 57% 43% RYANAIR HOLDINGS PLC

NL0012650360 70,272 489,539 559,811 13% 87% 1 1 RHI MAGNESITA NV

Delegation

In addition to the STO, ESMA is also looking at delegation rules as part of its review of the AIF and

UCITS framework.6 This could impact delegate dealing capacity by requiring this to be licensed

in Europe. ESMA has requested legal clarification from the EU Commission in relation extent of

delegation including a list of core or critical functions that must always be performed internally

and may not be delegated to third parties. However, this remains at a theoretical stage for now

given the letter from ESMA to the European Commission has no legal basis. It highlights the

remaining concerns regarding the outcome of the Brexit negotiations, and ESMA could respond

rapidly if they deem it necessary to prevent liquidity draining from Europe.

6 https://www.esma.europa.eu/sites/default/files/library/esma34-32-551_esma_letter_on_aifmd_review.pdf

3

Post Covid Capital Market Recovery Package

As a result of the pandemic, the MiFID II review has been significantly reduced in scope, with the

bulk of industry concerns being pushed into Q4 2021. The elements that will be included in the

Capital Markets Recovery package proposed by the European Commission in July 2020 is slowly

working its way into the legislate.

Timeline

Parliament review of Translation of Immediate publication

Presidency proposal proposals in four expected in November

and amendments to languages

MiFID II currently

underway

Product governance

• Product governance requirements on more complex products should no longer apply to

non-complex bonds where they are marketed or distributed on an execution-only basis

• Eligible counterparties are also deemed to have sufficient knowledge on financial

instruments and can be exempt from product governance requirements. The exemption

only applies to financial instruments exclusively marketed and distributed to eligible

counterparties

Cost and charges disclosures

• Services provided to eligible counterparties and professional clients should be exempt

from cost and charges disclosure requirement

• The exemption does not apply to services of investment advice and portfolio

management

Cost benefit analysis

• Exemption for professional investors from cost benefit analysis in case of switching

financial instrument but possibility for professional investors to opt-in

Best execution reports

• To facilitate the communication between investment firms and their clients, investment

information should be provided electronically and no longer on paper

• Retail clients should however be able to request the continued provision of information

on paper

Service reports

• Reports deemed unhelpful in extreme volatile markets given their high frequency

• Professional clients often react to those service reports by not reading them at best or

by rushing into investment decisions rather than continuing with a long-term strategy

• Eligible counterparties should be exempt from receiving such reports while professional

clients should have the possibility to opt-in

4

Other topics reviewed by Europe

• Reversing Research Unbundling for

o SMEs along with expanding the definition of small and mid-cap issuers to issuers with

a market capitalization threshold of up to EUR 10 billion over a 12-month period

• Fixed income research: Proposal considers if fixed income research is received without

impacting the spread, it can be exempt from MiFID II research rules.

Longer-term change

Despite the immediate focus on Brexit and the MiFID II Review, market participants should focus

on the longer-term direction of policy. Europe has re-launched Capital Markets Union in support

the recovery of SMEs and the real economy post-Covid. Although MiFID II improved liquidity for

large caps, it is the regulators view that secondary markets have failed to improve liquidity for

SMEs. Given these companies are now at a greater risk due to increased levels of debt incurred

and the recent fall in economic activity, EU policy makers are looking to stimulate re-equitisation

of SMEs. To achieve this, they plan to significantly reduce red-tape in terms of listing

requirements, improve research exposure and look at alternative means of bolstering

secondary market activity. The latest discussions include a new paper by the AMF based on the

introduction of a new auction model for SMEs,7 this will be another area to watch going forward,

as well as the outcome of future relations between the EU and the UK. While regulators on both

sides of the channel are searching for pragmatic solutions, ultimately what they are able to

implement will all come down to politics.

Global Liquidity

Despite lockdown measures being lifted progressively over the summer and governments

making every attempt to re-start their respective economies, Top of Book Liquidity8 has not

returned to pre Covid levels for the UK Top 100 and EU STOXX 600 trading respectively 32% and

30% lower than the January average, whereas Australia and Japan is now higher than pre Covid

levels. There has been little change in US TOB liquidity.

Global Top of Book Liquidity

Exhibit 2: Top of Book Liquidity

Top of Book Liquidity Top of Book Liquidity % Change October

(median number October (median average vs January

Index of shares) number of shares) average

US Top 500 429 431 0%

Hong Kong All 100,834 93,088 -7%

Australia Top 200 16,995 26,271 54%

Japan Top 225 6,861 4,387 36%

UK Top 100 2,237 1,521 -32%

STOXX 600 1,440 998 -30%

Source: Liquidnet Investment Analytics

7 https://arxiv.org/abs/2010.02827

8 As represented by the median number of shares at the top of the book proxied against the January average

5

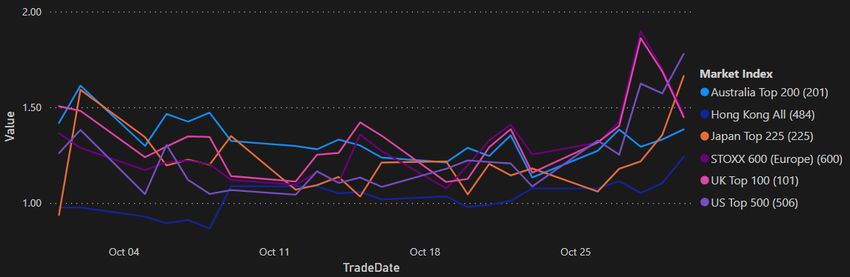

Exhibit 3: Top of Book Liquidity represented by the median number of shares proxied against January average (split by market) Source: Liquidnet Investment Analytics – Date range from January 2 to October 30 Liquidity levels have remained relatively stable in Japan and Hong Kong even at the height of the pandemic due to the proportion of lit market activity. Within this high proportion of lit activity there are local differences such as the lack of HFT in Hong Kong versus the comparative higher proportion of HFT in Australia which impacted liquidity provision. One potential reason for the low Liquidity levels in the UK/Europe compared to other markets is due to the high proportion of US and APAC retail activity which is taking place. Continued lack of liquidity across UK and Europe markets will force buy-side traders to review when, where and how to trade to ensure best execution for their end investors. In a recent market structure survey, asset managers are already adjusting their trading hours with the bulk of the activity now taking place from the US Open to the European close to guarantee maximum liquidity access. Exhibit 4: Top of Book Liquidity represented by the median number of shares proxied against January average Source: Liquidnet Investment Analytics – Date range from January 2 to October 30 Global Volumes Global volumes are significantly lower than March levels but remain around 20-30% higher than the January average except for Australia which has experienced heightened volatility and volumes 62% higher than the January average. 6

Exhibit 5: Global volumes

January Peak in October % change % change

average March average January in peak March

(in million (in million (in million average vs vs October

Index shares) shares) shares) October average

average

Australia 1.3 5.9 2.1 62% -64%

Hong Kong 4.4 13.3 5.5 25% -59%

Japan Top 225 1 3.1 1.3 30% -58%

STOXX 600 0.8 3.2 1 25% -69%

UK Top 100 1.9 7.1 2.2 16% -69%

US Top 500 1.2 3.6 1.6 33% -55%

Source: Liquidnet Investment Analytics

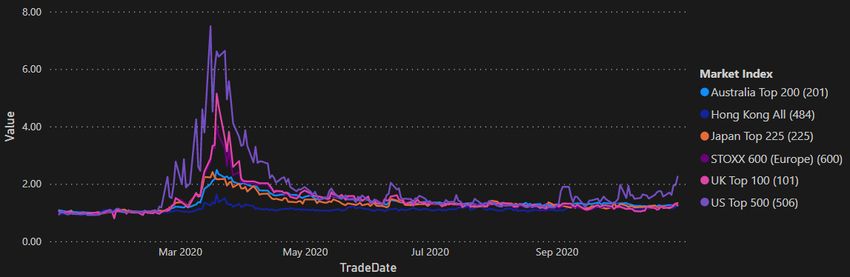

Exhibit 6: Global Volumes (split by Index) from January 2020

Source: Liquidnet Investment Analytics – Date range from January 2 to October 30

Overall volumes have been consistent for the last few months with the occasional spike due to

rebalances.

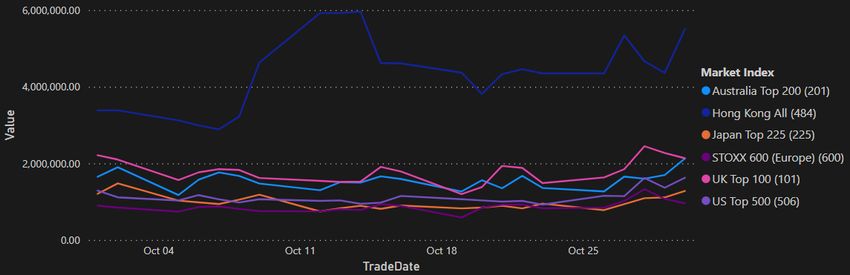

Exhibit 7: Global Volumes (split by Index) in October

Source: Liquidnet Investment Analytics – Date range from September 1 to October 30

7

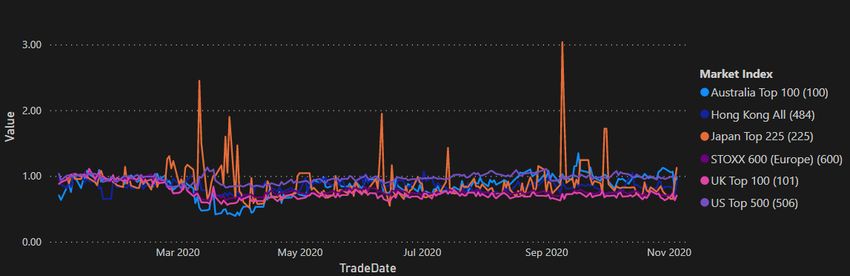

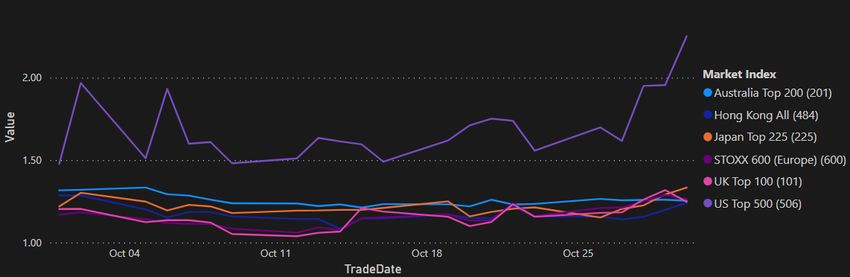

Over the last month volumes have stayed relatively steady with only a slight uptick towards the end of October as Covid-19 took hold in some European countries leading to talks of lockdown and new restrictions. Global Spreads Despite liquidity and volumes on track to recover from pre-Covid levels for most markets, spreads9 are still wider than in January in all markets indicating that it will take some time for the market to fully re-adjust from the pandemic and ongoing uncertainty regarding the re- introduction of restrictions globally. US Top 500 spreads widened recently, rising 147% from 4.01 on January 1 to 9.91 on October 30. Exhibit 8: Spreads proxied by January average (split by market) from January 2020 Source: Liquidnet Investment Analytics – Date range from January 2 to October 30 Although spreads have tightened since the peaks in March, Exhibit 9 shows how the spreads have increased in the last week of October. Exhibit 9: October spreads proxied by January average Source: Liquidnet Investment Analytics – Date range from October 1 to October 30 9 Normalised spreads to a factor of 1 (each stock is divided by the January average spread where 1 becomes a reference for what happened pre Covid) 8

Spreads Across Market Cap A similar picture is emerging across Market Caps with all caps’ spreads still considerably wider than they were back in January. Exhibit 10: Normalised Spreads against January average (split by cap size) from January 2020 Source: Liquidnet Investment Analytics – Date range from January 2 to October 30 Mega Caps currently had the widest spreads on September 30 at 88% wider than the January average. Next are Large caps, which are 47% wider than the January average. Exhibit 11: Normalised Spreads against January average (split by cap size) from January 2020 Source: Liquidnet Investment Analytics – Date range from January 2 to October 30 Market Impact The cost of trading remains higher than January levels across all markets, however, the reason why the cost of trading has not recovered to pre-Covid levels vary from one market to another. Higher volumes and wider spreads in Australia appear directly responsible for maintaining the cost of trading 38% higher in October compared to January while for the UK and Europe, the lack of liquidity result in the cost of trading still being respectively 45% and 46% higher than January. Wider spreads in the US may be the cause of the rise in costs there. 9

Exhibit 12: Cost to Trade (split by market) year to date Source: Liquidnet Investment Analytics – Date range from January 2 to October 30 Exhibit 13: Cost to Trade (split by market) month to date Source: Liquidnet Investment Analytics – Date range from October 1 to October 30 10

Breakdown of European Liquidity Overall market volumes were significantly lower throughout the summer months at €33.8B in August and was at €40.9B in October, compared to €57.6B in June and €81B average recorded in March. Volumes are now more on par with January levels. Exhibit 14: EMEA Monthly Market Share 2018 to date Source: Bloomberg Market share remains stable - Lit continuous is 39%; Auctions 16%; Lit MTF 15%. Systematic Internaliser activity declined in the third quarter and is now at 20% of total volumes. Dark trading and Periodic Auctions remain static at approximately 8% and 3% of overall market volumes respectively. Systematic Internalisers SI Average Daily Principal Traded has now declined to €8.2B compared to the June’s peak at €13.8B coinciding with a decrease in the average execution size from €31k in June to €16.2K in October (see Exhibit 15). The constant decline in SI average execution size since April 2018 further evidence the reduction in available risk. 11

Exhibit 15: SI Average Daily Principal Traded by Month Source: Bloomberg Dark Trading Dark trading as a percentage of overall exchange traded activity increased from 7.8% in June to 10.3% in October (see Exhibit 16) and is now in line with pre-Covid levels although dark trading as a percentage of overall activity firmly remains at or below the 8% threshold (see Exhibit 14). Exhibit 16: Dark % of dark and lit volumes Source: Bloomberg 12

© 2020 Liquidnet Holdings, Inc. and its subsidiaries. Liquidnet, Inc. is a member of FINRA/SIPC. Liquidnet Europe Limited is authorised and regulated by the Financial Conduct Authority in the UK, is licensed by the Financial Sector Conduct Authority in South Africa, and is a member of the London Stock Exchange and a remote member of the Warsaw Stock Exchange and SIX Swiss Exchange. Liquidnet EU Limited is authorised and regulated by the Central Bank of Ireland and is a remote member of the Warsaw Stock Exchange. Liquidnet Canada Inc. is a member of the Investment Industry Regulatory Organization of Canada and a member of the Canadian Investor Protection Fund. Liquidnet Asia Limited is regulated by the Hong Kong Securities and Futures Commission for Type 1 and Type 7 regulated activities and is regulated by the Monetary Authority of Singapore as a Recognized Market Operator. Liquidnet Japan Inc. is regulated by the Financial Services Agency of Japan and is a member of JSDA/JIPF. Liquidnet Australia Pty Ltd. is registered with the Australian Securities and Investment Commission as an Australian Financial Services Licensee, AFSL number 312525, and is registered with the New Zealand Financial Markets Authority as a Financial Service Provider, FSP number FSP3781. Liquidnet Singapore Private Limited is regulated by the Monetary Authority of Singapore as a Capital Markets Services Licensee, CMSL number CMS 100757-1. 11/20

You can also read