HARNESSING THE POWERS OF BLOCKCHAIN AND ITS ASSISTIVE TECHNOLOGIES - http

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

1

HARNESSING THE POWERS OF BLOCKCHAIN

AND ITS ASSISTIVE TECHNOLOGIES

Case Studies in Renewable Energies, Publishing, Voting Sys-

tems, Notaries and Supply Chain Management

MSc Thesis

International Master of Management of IT

Author

Wassim BENDELLA

Anr: 287853

Supervisor 1

Prof. Dr. Anne-Françoise RUTKOWSKI

Supervisor 2

Prof. Dr. Antonin RICARD

01.06.2017

2

Den Haag, Netherlands

3 ABSTRACT Firms are both concerned and excited by the business implications arising from block- chain technology. They have begun to educate themselves and are now exploring how blockchain could be used to bring new services to market and enhance operational capa- bilities. In this study, we present 5 use cases and seek to explain how blockchain can impact various industries, among which publishing, energy, voting, notaries and supply chain management. We present a view of where blockchain stands and what future ac- tions are needed to fully understand and exploit this exponential technology. By using data from 354 startups using blockchain, we paint a view of the current landscape in this field, and expose lines of thought that have the potential of overcoming the adoption ob- stacles on the blockchain journey.

4

ACKNOWLEDGMENTS

Writing this thesis has been both a demanding and rewarding project. It hasn’t always

been easy juggling a full-time internship, a part-time writing job on cryptocurrency, and

long nights after work dedicated to this thesis. It did require endurance and self-motiva-

tion, but it has been a journey with very good learnings, and finalizing this work makes

it even more significant.

First and foremost, I would like to thank my parents for their sacrifices, patience and

faith in me, as well as my family and loved ones for their continuous and priceless sup-

port.

I would also like to thank my competent supervisors A.F. Rutkowski and A. Ricard

for their understanding of my particular situation, their expert advice and their precious

feedback.

I would like to thank the 6 startup founders that, despite their busy schedules, took the

time to inspire me and share their expertise: Leanne Kemp, Larry Temlock, Alex Tran

Qui, Daniele Levi, David Ruescas, and Oleksii Konashevych. I wish you all the best for

the rest of your adventure.

Finally, I want to thank all the classmates, colleagues and friends met during these

years in France, Finland and The Netherlands. With special thanks to the IMMIT 9 cohort

and the 40% Team who made my university time so memorable that I can now reminisce

it with a big grin.

Sincerely,

Den Haag,

June the 1st, 2017

Wassim Bendella

5

TABLE OF CONTENTS

Abstract ............................................................................................................................. 3

Acknowledgments ............................................................................................................. 4

Table of Contents .............................................................................................................. 5

List of Figures ................................................................................................................... 7

List of Tables..................................................................................................................... 8

1 INTRODUCTION ................................................................................................... 9

1.1 Research Background ..................................................................................... 9

1.2 Research Motivation .................................................................................... 10

1.3 Research Questions ...................................................................................... 11

1.4 Research Structure........................................................................................ 11

2 LITERATURE REVIEW ...................................................................................... 12

2.1 Bitcoin: The Promise of Independence from Banks .................................... 12

2.2 Blockchain Goes Beyond Cryptocurrencies ................................................ 14

2.3 An Explanation of Blockchain Terminology ............................................... 15

2.4 The Trust Trade-Off: Different Flavors of Blockchain Architectures ......... 17

2.4.1 Permissioned and Permissionless Blockchains ................................ 17

2.4.2 Public and Private Blockchains ....................................................... 18

2.4.3 Generic and Specific Blockchains ................................................... 19

2.5 A Peek into How Blockchain Works ........................................................... 21

2.6 The Advent of Smart Contracts .................................................................... 23

2.7 Decentralized Autonomous Organizations................................................... 25

2.8 Putting Theory into Practice......................................................................... 26

2.9 The Value Net Framework ........................................................................... 27

3 METHODOLOGY ................................................................................................ 29

3.1 Research Design ........................................................................................... 29

3.1.1 Qualitative Methodology ................................................................. 29

3.1.2 Case Study Methodology ................................................................. 30

3.1.3 Sample Selection .............................................................................. 31

3.2 Data Scraping for Quantitative Data ............................................................ 32

3.3 Interviewing Blockchain Actors................................................................... 33

6

4 RESEARCH FINDINGS ....................................................................................... 36

4.1 The Business Field of Blockchain................................................................ 36

4.2 Use Cases of Blockchain Technology.......................................................... 41

4.2.1 Renewable Energies: The Sun Exchange ........................................ 41

4.2.2 Publishing: Katalysis ....................................................................... 43

4.2.3 Electronic Voting Systems: e-Vox and nVotes ............................... 47

4.2.4 Notaries: Stampery .......................................................................... 51

4.2.5 Supply Chains: Everledger .............................................................. 53

4.3 Key Findings ................................................................................................ 55

5 DISCUSSION ........................................................................................................ 65

5.1 Towards More Sustainable Protocols........................................................... 65

5.2 Overcoming the Scalability Challenge......................................................... 66

5.3 Transacting Privately on a Blockchain ........................................................ 67

5.4 Blockchain and Cybersecurity ..................................................................... 68

5.5 Potential Impacts on the Labor Market ........................................................ 69

5.6 Regulating Blockchain Transactions............................................................ 70

5.7 New Blockchain Based Business Models .................................................... 73

6 CONCLUSION ..................................................................................................... 75

References ....................................................................................................................... 76

Appendix ......................................................................................................................... 84

7 LIST OF FIGURES Figure 1 The Logical Components of Blockchain (Betz, 2016)................................. 17 Figure 2 Different Flavors of Blockchain (Betz, 2016).............................................. 19 Figure 3 How One Block Is Built and Validated (Schneider et al., 2016) ................. 21 Figure 4 Overview of a Blockchain Transaction Process (Betz, 2016)...................... 21 Figure 5 The Process of Reaching Consensus (Schneider et al., 2016) ..................... 22 Figure 6 The Execution of a Smart Contract (Morabito, 2017) ................................. 24 Figure 7: The Value Net Framework ........................................................................... 28 Figure 8: Number of Blockchain-Related Startups Created Since 2009 ..................... 36 Figure 9: A Map of Blockchain-Related Startups Per Country ................................... 37 Figure 10: A Map of Blockchain-Related Startups Per City ......................................... 38 Figure 11: A Visualization of the Adoption of Blockchain Per Industry ...................... 39 Figure 12: VFN of a Blockchain Solar Company ......................................................... 58 Figure 13: VFN of a Blockchain Publication Manager ................................................. 59 Figure 14: VFN of Blockchain Voting System Provider............................................... 60 Figure 15: VFN of a Blockchain Virtual Notary ........................................................... 61 Figure 16: VNF of a Blockchain Provenance Company ............................................... 62

8 LIST OF TABLES Table 1 The Blockchain Technology Stack, adapted from (Pon, 2015) ................... 16 Table 2 Trade-Offs Between Permissioned and Permissionless Architectures ........ 18 Table 3 Examples of Different Blockchain Architectures ........................................ 20 Table 4 A Bitcoin Analogy to Understand DAOs..................................................... 25 Table 5 A List of Interviewees from Various Industries ........................................... 33 Table 6: The Interview Process .................................................................................. 34 Table 7 Interview Guide ............................................................................................ 34 Table 8: Top 8 Countries in Blockchain Innovation .................................................. 37 Table 9: Top 8 Cities in Blockchain Innovation ........................................................ 38 Table 10: Top 8 Industries Adopting Blockchain ........................................................ 40 Table 11: The Value-Adding Aspects of Blockchain .................................................. 55 Table 12: New Blockchain-Powered Business Models ............................................... 57 Table 13: Challenges on The Blockchain Journey ....................................................... 62

9

1 INTRODUCTION

1.1 Research Background

In 1991, the World Wide Web was introduced and it disrupted every aspect of our lives

in an unprecedented manner. More than thirty years later, our society is still continuously

transforming powered by this technology. Now with the advent of the Internet of Things,

it is more than ever the nervous system of our smart, connected world.

Within this ecosystem, many applications have become valuable by capturing data

from users and storing it in centralized private databases. This is the model behind Google

and Facebook, for example. The aggregation of value on top at the application layer is

referred to as the “thin protocols and fat applications” model (Monégro, 2016).

Enters blockchain technology, which many argue is “the biggest thing since the Inter-

net” (Torpey, 2016). Rather than most of the value being concentrated at the application

layer, it is distributed at the protocol layer. This reverse relationship that unlocks data and

openly shares it is referred to as the “fat protocols and thin applications” model.

Since the Economist’s 2015 famous cover featuring blockchain, this technology has

spread like wildfire and triggered many new players to peek an interest in this novel field.

Much has been written in the press on its development and it has attracted massive interest

from governments, companies and academia altogether.

In the last few years, many financial institutions have realized the depth of blockchain

capabilities and applications, which can span from moving money to securely recording

transactions. In Seattle, Microsoft and R3, a consortium of the world’s biggest banks,

signed a strategic partnership to accelerate the use of distributed ledger technologies and

agree on standards for their future adoption. In fact, blockchain can bring more speed,

transparency and security to financial transactions compared to how these are carried out

nowadays (Kharpal, 2016). The technology could cut costs by up to $20 billion annually

by 2022, according to Santander (Rennick & Veitch, 2015). Besides the financial sector,

Goldman Sachs even notes that blockchain has the potential to change “everything”

(Boroujerdi & Wolf, 2015).

The military industry is one of the many sectors that is embracing this technology. The

U.S. Defense Advanced Research Projects Agency, known as DARPA, is currently ap-

plying blockchain to counter the ubiquitous corporate and governmental hacks. As a dis-

tributed indelible ledger that detects tampering, blockchain is used to secure highly sen-

sitive data and could be involved in more military applications in the future from nuclear

weapons to military satellites (Wong, 2016).

In Russia, the National Settlement Depository, which is the central securities deposi-

tory, has successfully developed and tested a voting mechanism based on blockchain for10 shareholder meetings, for increased security and transparency (Prisco, 2016). More and more governments are looking to incorporate this technology, such as Georgia that al- ready recorded more than 100,000 land titles on a blockchain in partnership with BitFury (Smerkis, 2017). Given these much promising capabilities, no wonder investments in blockchain startups are at an all-time high. Investors have already poured $550M in 2016 from dis- closed funding alone, which brings the total investment over the past four years to $1.53B (CB Insights, 2017). Proofs-of-concept are being developed, pilots launched and some of these foundational technologies even moved from the lab to early production. For Jeremy Gardner, chairman of the board at the Blockchain Education Network, blockchain “is going to make the financial world, and beyond (remittance, provenance, ownership), achieve a level of unbelievable transparency and auditability that has never occurred in human history” (Lachance, 2016). 1.2 Research Motivation I personally was involved with blockchain for the first time when I was looking for alter- native solutions to transfer money abroad without having to pay for expensive fees. I discovered it was possible to make money transfers through the Bitcoin protocol, and it enabled me to dramatically reduce my remittance costs and to send and receive money internationally even faster than traditional wire transfers. I instantly recognized the power of blockchain and couldn’t resist watching numerous conferences and reading hundreds of articles on this much promising topic. Later, I encountered a new service that was offering me to invest in solar energy and earn regular income out of it through blockchain technology. I hopped on the opportunity and funded along with hundreds of other people from all around the world a solar project in Africa. This naturally made me ask myself about what else could be achieved with blockchain, and where can it be applied to produce value. This question started to be addressed 3 years ago from various angles. Each month, new blockchain startups are cre- ated and there is currently every indication that these figures will continue to grow (CB Insights, 2017). Despite the amount of research on blockchain applications, much of the discussion around its day-to-day applications remain abstract. The center of interest for academia has been on the potential of decentralizing markets and empowering users, but the capa- bilities of blockchain are subtler than that straight-forward portrayal.

11

1.3 Research Questions

In 2016, a systematic mapping study explored the existing studies related to blockchain

technology to identify possible research gaps. It highlighted that most of current research

is conducted in the Bitcoin environment, which is only one application of blockchain.

The authors recommended that new research needs to be carried out to increase

knowledge outside cryptocurrencies. “It is necessary to conduct research on the possibil-

ities of using blockchain in other environments, because it can reveal and produce better

models and possibilities for doing transactions in different industries” (Yli-Huumo, Ko,

Choi, Park, & Smolander, 2016).

The purpose of this study is to move beyond the theoretical to the practical, by explor-

ing a range of specific real-world applications in various industries including publishing,

energy, notaries, and voting systems. Therefore, we defined four research questions to

guide us throughout this thesis:

• RQ1: How is the current landscape of blockchain startups?

• RQ2: How can blockchain add value?

• RQ3: To what extent can blockchain impact current business models?

• RQ4: What challenges is blockchain adoption facing?

1.4 Research Structure

The rest of the study is organized as follows. In the following section, we will introduce

the concept of cryptocurrencies and lay out how it led to the development of different

types blockchain, and display a high-level technical overview of how the technology

works. Along the way, we will also present its assistive technologies: smart contracts and

decentralized autonomous organizations. In Section 3, we describe the applied research

methodology and the process of interviewing our selected sample. Section 4 presents the

results of our quantitative analysis and interviews. Finally, we answer the research ques-

tions stated previously in the last section, and conclude the study with our views on the

future of blockchain technology and its applications.12 2 LITERATURE REVIEW 2.1 Bitcoin: The Promise of Independence from Banks From barters to bytes, financial exchanges have evolved with civilization. Just a few cen- turies ago, mankind paid and bartered goods with slabs of meat and baskets of berries. In the digital age, we now have the convenience of virtual payments and a plethora of mobile payment options that allow us the freedom to pay for goods almost anywhere. For most of our modern history, most national currencies were directly linked to gold at a specified fixed rate. In 1971, the United States abandoned this “gold standard” and given the dollar’s role as an international reserve currency, the global monetary system became a fiat-currency one. Such currencies are only based on faith in the economy, but are not backed by gold (Davies, 2010). While the digital revolution has made money become more virtual and less physical than ever, it also gave birth to attempts to return to gold-backed currency, by representing gold digitally. The first attempt ever for creating a digital currency has been led by the American mathematician David Chaum in 1990 (Chaum, Fiat, & Naor, 1990). By using cryptographic protocols, he created the Cyber Buck and developed its use for Internet micropayments through his company DigiCash BV. Between 1998 and 2005, Nick Szabo created a cryptocurrency named Bit Gold (Szabo, 2005). Many argue it has heavily contributed to the intellectual foundation of the Bitcoin, because of their similarities in the use of digital signatures, public and private keys, and timestamping processes (O’Leary, 2015). However, neither one of these two experiments ever reached the mainstream level. Citizens weren’t as concerned back then about privacy issues, the underlying foundations of these currencies were vulnerable to cyber-attacks, and digital currencies even suffered from government censorship that slowed down their growth (DeMartino, 2016). Years passed until the 31st of October 2008. Satoshi Nakamoto –which is a pseudo- nym- published an article titled “Bitcoin: A Peer-to-Peer Electronic Cash System”, in which is presented an open source protocol of distributed computations that enable trust- worthy exchanges of data without the need of third parties (Nakamoto, 2008). Bitcoin was born right in the financial crisis of 2008. This specific context of fragile monetary system and mistrust in banks presented Bitcoin as an alternative solution to the centrali- zation of financial institutions. In an increasingly complex and globalized world, billions of international transactions are carried out daily. These transactions are recorded in an isolated and closed ledger, and we hence require middlemen to facilitate and clear them. Banks, governments, account- ants, and notaries are examples of these middlemen. Bitcoin is revolutionary because it

13 enables a collective bookkeeping via the Internet, that is not in control of any central party nor closed to the public. Indeed, Bitcoin is the first currency that is resistant to government censorship, without any point of failure. Thanks to cryptography, its entire system is distributed and thus im- possible to pinpoint and shut down. This distributed ledger is called the blockchain, in which each single transaction is logged in terms of date, time, participants and amount. On the network, each node owns a full copy of the blockchain, and transactions are veri- fied by Bitcoin miners who maintain the ledger (Antonopoulos, 2014). The nodes agree automatically and continuously on the transactions on the network. If anyone attempts to corrupt a transaction, the nodes will not arrive at consensus and there- fore, they will refuse to incorporate the flagged transaction in the blockchain. In other words, every transaction is public, and thousands of nodes unanimously agree on each transaction’s attributes, as if a notary is present for each one of these. Everyone has access to a single, shared source of truth, hence the trust revolution it entails (Tapscott & Tapscott, 2016). A Bitcoin is divisible in 100,000,000 units, and one unit is referred to as one Satoshi (1 Satoshi = 0.00000001 BTC). Each one of these units is both individually identifiable and programmable. Users can assign properties to each unit, and they can program it represent a multitude of elements such as a euro cent, a kWh of energy, a title of owner- ship or a share in a company. This aspect of Bitcoin enables what is referred to as “com- pliancy upfront”, in the sense that Bitcoin can comply with a predetermined governance before the transaction occurs (van der Hoek, 2016). For example, a unit can be pro- grammed to be used during at a certain period, or for specific uses only such as with certified vendors. This has the potential to significantly decrease bureaucracy and make organizations more efficient and productive. In other words, “Bitcoin is programmable money. When you have programmable money, the possibilities are truly endless. We can take many of the basic concepts of the current system that depend on legal contracts, and we can convert these into algorithmic contracts, into mathematical transactions that can be enforced on the Bitcoin network” (Antonopoulos, 2016). “Bitcoin represents a fundamental transformation of money. An invention that changes the oldest technology we have in civilization. It changes it radically and disruptively by changing the fundamental architecture into one where every participant is equal. Where transaction has no state or context other than obeying the consensus rules of the network that no one controls.” Users have absolute control over their money through digital sig- natures, as no entity can seize their assets nor freeze them. “Bitcoin is a system of money that is simultaneously, absolutely transnational and borderless. We’ve never had a system of money like that” (Antonopoulos, 2016).

14

2.2 Blockchain Goes Beyond Cryptocurrencies

In our digital world, data flow from one place to another in high volumes. To verify the

authenticity and accuracy of this information, we rely on trusted intermediaries. We take

the word of such authorities on a regular basis in our daily lives, in both mundane inter-

actions and important decisions. Trust is at the core of transactions because the partici-

pants are embedded in a social relationship (Mayer, Davis, & Schoorman, 1995), charac-

terized by its degree of uncertainty (Kollock, 1994). The aforementioned intermediaries

can provide such trust, and hence make transact different parties that don’t necessarily

trust each other, but have trust in the intermediary. Banks or credit card companies are

examples of intermediaries. When a financial transaction is in progress, intermediaries

confirm the identities of both parties, and check if the sender's balance has sufficient funds

before processing the payment and updating the bank ledger. This chain of services that

allow strangers to conduct business comes at variable costs (Beck, Czepluch, Lollike, &

Malone, 2016).

From their nature of middlemen, these institutions are subject to disintermediation

(Seppälä, 2016). Enters blockchain technology, which promises to create cheaper, simpler

and more efficient systems by eliminating these intermediaries.

“The heart of blockchain’s potential lies in the unique properties of a dis-

tributed ledger and how it can improve transparency, security, and effi-

ciency. Historically, organizations used databases as central data reposi-

tories to support transaction processing and computation. Control of the

database rested with its owner, who managed access and updates, limiting

transparency, scalability, and the ability for outsiders to ensure records

were not manipulated. A distributed database was practically impossible

because of technology limitations. But advances in software, communica-

tions, and encryption now allow for a distributed database spanning or-

ganizations.” (Schneider, Blostein, Lee, Kent, & Boroujerdi, 2016)

Many times compared with centralized database technology, blockchain is distinguish-

able for three main aspects:

• Security: Blockchain is an indelible ledger secured by heavy-duty encryption. It

guarantees that consensus will not be reached for non-legitimate transactions,

and thus, these won’t be registered on the distributed ledger. The fact that each

block is linked to the previous one in a tamper-proof chain makes it practically

impossible for anyone to corrupt this ledger. If one wants to do so, the whole

history of the ledger needs to be rewritten, and this will require computing power

so huge it would make it financially unworthy (Mougayar, 2016).15

• Transparency: A blockchain consists of multiple nodes that maintain the data-

base running in a distributed manner. These nodes check the integrity of trans-

actions and record them on the blockchain when they are valid. As such, data

must be consistent between nodes for them to reach a consensus and consider a

transaction to be valid. Anyone can view these recorded transactions at any time

because they reside on the distributed network, as each node holds a copy of the

database (Pilkington, 2015).

• Efficiency: “Conceptually, maintaining multiple copies of a database with

blockchain would not appear to be more efficient than a single, centralized data-

base. But in most real-world examples, multiple parties already maintain dupli-

cate databases containing information about the same transactions. Furthermore,

in many cases, the data pertaining to the same transaction is in conflict – result-

ing in the need for costly, time-consuming reconciliation procedures between

organizations. Employing a distributed database system like blockchain across

organizations can substantially reduce the need for manual reconciliation, thus

driving considerable savings across organizations” (Schneider et al., 2016).

As a decentralized ledger, blockchain enables value transactions of different natures.

Whether it is money, assets, titles of ownerships or messages, value can be shared and

stored in a reliable way by using high-grade cryptographic methods (Kiviat, 2015). Since

these value transfers can be verified by anyone without needing a trusted intermediary to

guarantee the authenticity of records, blockchain is described as a “trustless technology”.

Freeing transactions and their auditability from a central authority sheds light on the dis-

ruptive potential of blockchain (Lemieux, 2016). Therefore, a significant proportion of

our economy could move to a decentralized architecture of ownership and trust. While

the single source of truth enabled by blockchain is in the hands of everyone, the commu-

nity can freely use and maintain it. As long as at least a single node is working, the infor-

mation contained in the blockchain is safe (Watanabe et al., 2015).

2.3 An Explanation of Blockchain Terminology

The concept of blockchain traces back to the publication in 2008 of a paper detailing the

Bitcoin protocol by Satoshi Nakamoto. This paper combined techniques and ideas dating

back to decades ago into one functional system allowing its users to freely transfer and

receive money (Nakamoto, 2008). The specific word “blockchain” is not written in this

paper as such, but the idea of blocks of data linked together in a growing chain is clearly

developed. Nakamoto used the words “blocks” and “chain” separately to describe the

Bitcoin cryptocurrency system, and throughout the years, the common parlance merged

the two into a single word: “blockchain” (Brito & Castillo, 2013).16

If we follow this etymology, blockchain would refer to a protocol layer. Up until 2015,

the Bitcoin protocol was the only practical application of the decentralized data structure

popularized by Nakamoto. This explains why it was constituting the entire technology

stack of blockchain, until new companies started focusing on other layers of the stack. As

such, Ethereum proposed an open-source virtual machine on top of the protocol layer,

and Monax an open-source smart contract platform to build applications on. Therefore,

the stack quickly became fragmented, and the terminology of blockchain enlarged to en-

compass a variety of different structures. These different layers of the stack are outlined

in the table below, along with some examples.

Table 1 The Blockchain Technology Stack, adapted from (Pon, 2015)

Layer Example

Application layer Everledger

Platform layer The Monax platform

Processing layer Ethereum Virtual Machine (EVM)

Data/Protocol layer The Bitcoin blockchain

Network layer Filament Tap

Hardware layer BitFury mining chips

The phenomenon of distributed ledgers progressed carried out by the hype around this

innovation in the media and within the corporate sphere. Quickly enough, just like big

data or cloud computing in recent years, blockchain became a buzzword encompassing

various elements. The present research uses the term blockchain broadly, referring to the

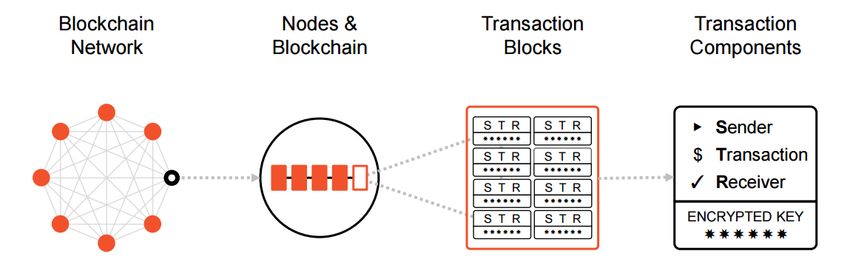

entire technology stack presented above. To understand how this technology works, it is

necessary to understand its logical components as represented in the figure below.

• The blockchain network: Members, or nodes, communicate over a peer-to-

peer, private or public network.

• The nodes and the chain of blocks: All members, within their node, hold the

entire network-validated transaction history.

• The transaction blocks: Transactions are aggregated and stored as linked

blocks over time.

• The transaction components: Each transaction is logged in terms of date, time,

participants and amount. A hash is generated from these unique attributes.17

Figure 1 The Logical Components of Blockchain (Betz, 2016)

2.4 The Trust Trade-Off: Different Flavors of Blockchain Architec-

tures

2.4.1 Permissioned and Permissionless Blockchains

So far, we mainly focused on the permissionless architecture because it is at the core of

the blockchain philosophy. Nakamoto envisioned a system in which distributed ledgers

are open to anyone, shortcutting the need of a permission-access delivered by a third party

Anyone can become a participant in the network. Even though these participants don’t

know each other, they don’t have to trust each other to be able to transact securely. In

fact, trust emanates from cryptography and mathematical incentives, rather than from a

central authority.

However, if a network’s participants are all know and can trust each other, is it neces-

sary to gulp the significant computing power needed to create trust from code? Permis-

sioned blockchains fill this gap. By leveraging the fact that trust is inherent to the system,

this type of architecture provides participants with access permissions to take part in the

network, and therefore saves great amounts of electricity, which can be quite significant

when aggregated. “By only allowing trusted members to participate in the blockchain, the

operation of the network can be made faster, more flexible and most importantly, much

more efficient — but at the cost of reduced security, immutability and censorship-re-

sistance” (Swanson, 2015).

While consensus algorithms are constantly being developed to reduce the energy ap-

petite of permissionless ledgers, for the time being, organizations must choose between

the two architectures. Opting for one inevitably leads to abandoning some properties in

favor of some others, which is both a strategic choice and a philosophical one. These

trade-offs are presented in the table below (Mattila, 2016).18

Table 2 Trade-Offs Between Permissioned and Permissionless Architectures

Dimensions Permissioned Permissionless

Fast ☑

Energy-efficient ☑

Easy to scale ☑

Censorship-resistant ☑

Tamper-proof ☑

The decentralization and censorship-resistant aspects of permissionless blockchains are

what aligned it remarkably with political movements post-crisis of 2008. The presence of

an access control layer in permissioned blockchains sweeps away the initial spirit of the

technology. Indeed, permissioned blockchains aren’t “looking to overthrow the political

system, or remove the need for established financial institutions. Instead, they leverage

some of the other core elements of blockchain architecture […] to create efficiencies,

reduce cost, and open opportunities for new data-driven business models” (Allaby, 2016).

On the level of the individual user transacting on a permissionless blockchain, paying

an inexpensive fee to benefit from blockchain’s features is a painful act. But for an or-

ganization that needs to make thousands of transactions a day, the overall cost is signifi-

cant, especially that the heavy computations that enable the network to process transac-

tions are redundant ones. Therefore, permissionless blockchains are less performant than

permissioned ones that allow transparence within the decision-making consortium only.

In permissioned blockchains, “authority and trust created outside of the networks en-

sures that participants trust what is committed to the ledger, while almost all the logistical

issues (cost, speed, throughput and contract sophistication ceilings) with creating trust

artificially disappear. The managing body can ensure data access so that only participants

that are party to a transaction can see sensitive details, a feature deemed rather important

according to modern enterprise security standards” (Allaby, 2016). This led Goldman

Sachs to predict the domination of permissioned blockchains in most commercial appli-

cations, especially in capital markets (Schneider et al., 2016).

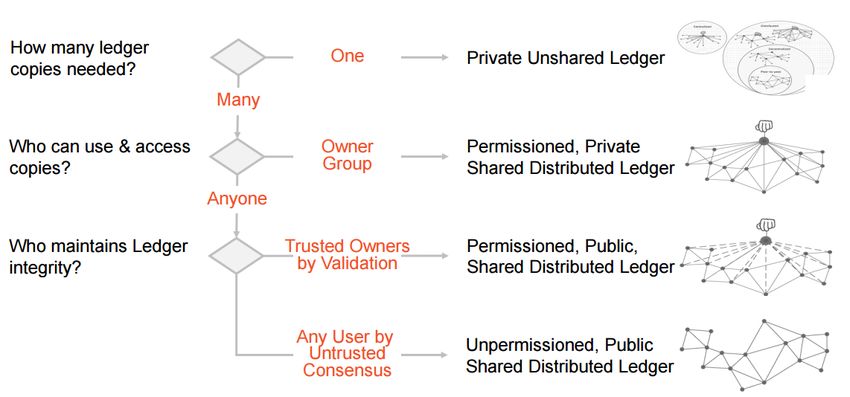

2.4.2 Public and Private Blockchains

Blockchains can also be categorized by their centralization level in a spectrum spanning

from public blockchains to private ones. Since each type has unique benefits and limits,

as for permissioned and permissionless blockchains, opting for one architecture means

making a trade-off and giving up on some capabilities, in order to benefit from some other

ones. Let us define three types on this centralization spectrum (Betz, 2016).19

• Public blockchains are blockchains that anyone can read and write in. Partici-

pation in the consensus process, which is the process by which transactions are

validated and added to the chain of blocks, is also open to anyone. These block-

chains are generally considered to be “fully decentralized”, and are therefore

extremely secure and transparent.

• Consortium blockchains are ones in which controlling nodes are predefined.

To illustrate this concept, let’s imagine that 15 art galleries gathered and formed

a consortium blockchain. Each node of this blockchain represents a single art

gallery, and for a block to be validated, at least 10 out of the 15 art galleries must

agree on it. Either anyone is given read-access to the blockchain transactions, or

access to these is restricted to the art galleries. This type of blockchain is “par-

tially decentralized”.

• Private blockchains are blockchains for which a central owner holds the per-

missions of writing and editing the ledger. This aspect makes them particularly

attractive to large companies. As for the read-permissions, they are either open

to anyone when public auditability is required, or reserved to a list of trusted

owners when it is not necessary to disclose transactions. These blockchains pro-

cess transactions at a faster rate and lower costs.

Figure 2 Different Flavors of Blockchain (Betz, 2016)

2.4.3 Generic and Specific Blockchains

Another dimension by which blockchains might be characterized is whether they are

logic-optimized or transaction-optimized.20

Logic-optimized blockchains allow developers to store algorithms and run customized

logical processes. Ethereum and Monax are examples of such platforms, and are referred

to as “consensus engines” (Oudejans & Erkin, 2017). This is because they allow devel-

opers to convoke the distributed network nodes to reach consensus, which enables the

execution and running of the programs stored on them (Kuhlman, 2017). To fulfill this,

these blockchains provide business and governance logic for running smart contracts (i.e.

small scripts which are saved onto the blockchain).

On the other hand, transaction-optimized blockchains are a good fit for tracking assets

and transferring value. They don’t offer developers much freedom and creativity in their

use, but are the best suited for building transfer, clearing and settlement mechanisms. The

table below illustrates multiple blockchain architectures along with an example for each

one. Kuhlman (2017) expects these binary optimizations to develop into a wider range

over time.

Table 3 Examples of Different Blockchain Architectures

Logic-Optimized

Ethereum Tendermint

Permission-

Permissioned

less

Bitcoin Ripple

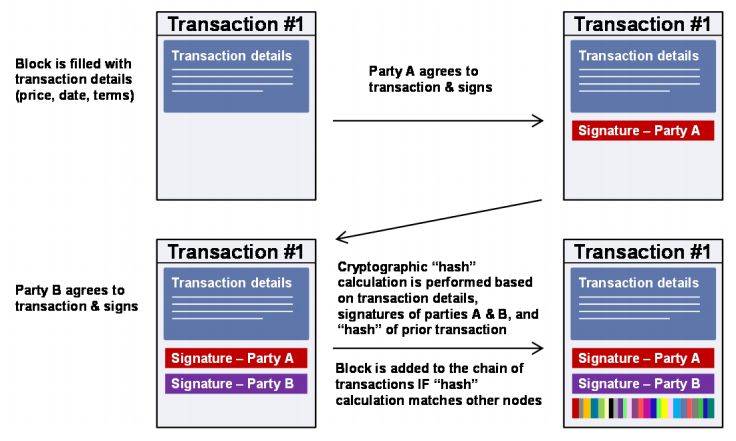

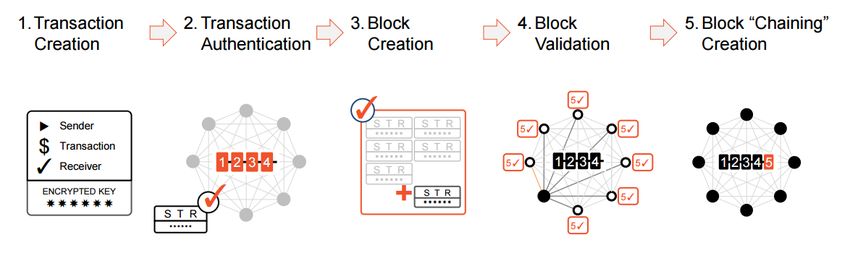

Transaction-Optimized21 2.5 A Peek into How Blockchain Works Figure 3 How One Block Is Built and Validated (Schneider et al., 2016) A transaction on the blockchain is composed of several pieces of information: the sender’s digital signature, the receiver’s digital signature, the transaction details, and a unique cryptographic hash. Transactions are gathered into “blocks”, which are in turn forming the “blockchain”. Figure 4 Overview of a Blockchain Transaction Process (Betz, 2016) 5 main steps constitute a transfer of value on the blockchain (Dorri, Kanhere, & Jurdak, 2016). These steps are illustrated in the figure above and outlined below.

22

1- The transaction definition: The sender creates and transmits a transaction to the

node. This transaction contains the receiver’s public address, the value of the trans-

action and a cryptographic digital signature to ensure the transaction is legitimate

and valid.

2- The transaction authentication: The network node receives and authenticates the

transaction. Valid transactions are then placed in a pending transaction cache.

3- The block creation: The block is updated on a node and broadcasted for network

validation.

4- The block validation: Some/all network nodes receive the new block and validate

it through algorithmic consensus frameworks.

5- The block chaining: Once all blocks are validated, the new block is chained to the

previous one and the new state of the ledger is replicated throughout to network.

These sequential steps can take about 3 to 10 seconds to finish. Compared to the tradi-

tional settlement mechanisms used by financial institutions, blockchain has a leading

speed advantage. Every 10 minutes, the heart of the blockchain ledger beats, at which

moment transactions are cleared and permanently saved in a new block chained to the

existing ones.

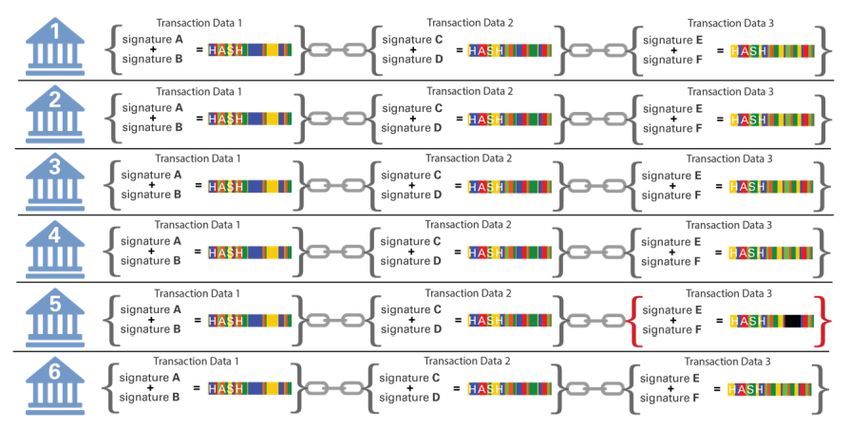

Figure 5 The Process of Reaching Consensus (Schneider et al., 2016)

In the figure above, “the blockchain ledger is replicated across multiple locations (we

show just six here for simplicity), and each maintains its own copy, which is separately

updated based on new transaction data. We show a sequence of three transactions. In the

first two transactions, data and signature information are properly validated by all six

nodes with matching hash values. However, for Transaction #3 at Location #5, the hash23

does not match the others, and will be corrected by the others via consensus” (Schneider

et al., 2016).

2.6 The Advent of Smart Contracts

Since 2015, smart contracts have been gaining popularity in the repertoire of technologies

brought by the blockchain. These are self-executing and self-maintaining contracts cap-

tured in code and housed on the blockchain at a particular address. They contain functions

that automatically performs the obligations the participating parties have agreed to

(Lewis, 2016). Smart contracts overlay the blockchain and can interact with other con-

tracts. They can make decisions autonomously and transact with various entities.

Since smart contracts can reflect any kind of business logic which is data-driven, they

are programmed to run when a certain event happens or when a set of predefined condi-

tions are met. The automatic character of such contracts enables strangers to build trust

and transact without involving any third party. It is indeed the system itself -and not its

users- that guarantees the legitimacy of transactions (Tuesta et al., 2015). No legal support

is needed, only consensus reached by the blockchain nodes. For example, if a car accident

happens and if a predefined set of conditions are met, the insured driver can automatically

receive money from his/her car insurance firm.

The contract’s terms, information and dates are timestamped and stored forever on the

blockchain, thus providing an immutable proof of these contracts. “They will exist and

be executable as long as the whole network exists, and will only disappear if they were

programmed to self-destruct” (Tapscott & Tapscott, 2016).

At the time of writing, the most popular smart contract language is Solidity. It is a

high-level coding language that runs on the Ethereum Virtual Machine, suited both for

small as well as more complex programs. For contracts which check for conditions avail-

able on the blockchain, such a verification is automatic. However, if an external factor

needs to be checked and since smart contracts cannot access the outside network on their

own, a third party referred to as an “oracle” is needed (Silverberg, French, Ferenzy, &

Van Den Berg, 2016).

“Oracles are known in computer science for their ability to provide information from

outside a system which that system itself cannot acquire” (Klayman, 2016). These data

platforms collect information out of the reach of blockchains, to allow smart contracts to

decide whether the predefined conditions have been met or not.24

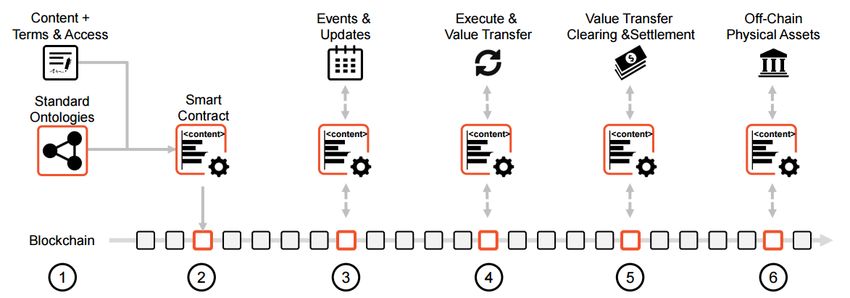

Figure 6 The Execution of a Smart Contract (Morabito, 2017)

The figure above presents different steps from the creation of a smart contract to its

execution and settlement. The 6 steps of this flowchart are as:

1- The counterparties establish obligations and settlement instructions;

2- A smart contract is created using interpretive languages (e.g. Solidity) and saved

in the distributed ledger;

3- An event triggers contract execution. An event could be anything data-driven such

as a transaction initiated, information received, a date met or a status change. New,

updated version of contract stored;

4- The business logic, that is the terms of the contract, checks which predefined con-

ditions are met to initiate the corresponding set of actions;

5- For digital assets “on the chain” such as cryptocurrencies, the accounts engaged by

the contract are settled automatically;

6- For assets “off the chain” such as a flat, accounts “off the chain” are inscribed

accordingly, and accounts on the blockchain are only modified once a third party

physically checks and guarantees the “off the chain” conditions are met.

The core difference between smart contracts and traditional scripts lies in the certainty of

results. When traditional scripts are running on a server, there is no guarantee they will

perform as intended, and deviations or inconsistencies can arise. Smart contracts, on the

contrary, live on the blockchain and have full visibility on the events happening on it.

This unique quality offers more certainty as to the results of their execution (Christidis &

Devetsikiotis, 2016).

Smart contracts can track logic-based events in real-time and take immediate action

following their predefined rules, thus eliminating human errors that could lead to costly

consequences. Instead of having multiple people in separate departments check a website

or call a data source for proof of performance (e.g., price, weather, location), the contract

itself is now able to automatically check that same proof of performance (Savelyev,

2017).25

“By removing the need for direct human involvement once a smart contract has been

deployed onto a distributed ledger, the computer program could make contractual rela-

tionships more efficient and economical with potentially fewer opportunities for error,

misunderstanding, delay or dispute” (Silverberg et al., 2016).

By building business logic in smart contracts, the participants in a transaction benefit

from more certainty and verifiability that leverage the increases in automation our world

is knowing. Indeed, coupling smart contracts with other technologies such as the Internet

of Things could be truly disruptive. Imagine a vending machine in a shopping mall. Its

embedded smart meters let the machine know exactly how much supplies it contains.

When some items reach a critical predefined limit, the machine automatically orders them

from a list of suppliers. It negotiates prices, pays for the order from its dedicated bank

accounts, and registers the transaction in its accounting book. It can fill tax reports at the

end of each year and even adjust prices of its products with the market. All autonomously

and with very limited human interaction.

2.7 Decentralized Autonomous Organizations

Decentralized autonomous organizations (DAOs) are organizations ruled by smart con-

tracts on the blockchain. DAOs can be for profit or nonprofit entities, which bylaws are

translated into scripts and which shareholders can take decisions are modify these scripts

if they gather a majority of votes (Tapscott & Tapscott, 2016).

This paradigm shift brings multiple advantages arising from transparency and immu-

table governance, which explains DAOs are sometimes referred to as “sharing govern-

ance” or “governance 2.0”. Each shareholder can make a proposal and submit to the com-

munity that will vote for it or reject it. Contracts can be enforced on the fly and thus, there

is no need for contacting all shareholders, processing huge amounts of paperwork. Eve-

rything is processed automatically on the blockchain (Buterin, 2014).

Once it published, no single shareholder can alter the code, as it is censor-free from

the characteristics inherited from the blockchain and open source for everyone to see.

These benefits however are not appropriate for all organizations, which is why some ar-

gue we are more likely to see the rise semi-DAOs, more suited to the unique needs of

each organization.

DAOs and traditional organizations share many of the same dimensions. To illustrate

this point, the table below presents an analogy between the characteristics of a traditional

organization and those of the Bitcoin blockchain, the first DAO to ever be created.

Table 4 A Bitcoin Analogy to Understand DAOs26

Characteristics of a traditional organi- The Bitcoin example

zation

Costs Distributing 100% of revenues to miners

Revenues Small fee on transactions

Shareholders Bitcoin holders

Voting Voting power comprised in Bitcoin own-

ership

Product A payment service

Customers Anyone making a transaction

Employees Miners that secure and facilitate pay-

ments

Values Bitcoin code

2.8 Putting Theory into Practice

Even though the world is noticing frenetic innovation in the blockchain field, block-

chain remains a complex technology underestimated by the market. This is explained by

the fast that blockchain suffers from an important lack of understanding. The low level of

familiarity with the technology (Kashyap et al., 2016).

Blockchain can be considered disruptive in two fronts. On the one hand, it enables us

to build trust while shortcutting third parties, clear and settle trades faster than ever, and

transact in a secure and censorship-resistant manner. Blockchain technology invites us to

reassess our answer to value production and ownership. On the other hand, it offers or-

ganizations the unique possibility of streamlining their activities by shortcutting data syn-

chronization and concurrency control, and thus significantly gain in efficiency.

This double potentiality can be leveraged by many industry incumbents or new play-

ers, in a wide variety of different industries, to solve current problems or add value to

present activities. “Whether it is with completely novel solutions to interacting over the

Internet or with increased efficiencies in pre-existing industrial systems, there are benefits

to reap in all playing fields — and those who neglect to do so may just end up finding

themselves at a disadvantage.” (Zysman & Kenney, 2016).

3 design principles of blockchain have been identified. First, the decentralization char-

acteristic of blockchain enables the creation of value networks in which participants in-

teract and transact with each other without middlemen. Secondly, trust is an essential

principle as it guarantees the integrity of transaction data. Movements of value on the

blockchain are timestamped and recorded in a secure and immutable ledger. This provides

an indisputable mechanism to check the provenance and ownership of data. Furthermore,

the fact that blocks are chained together makes it impossible to alter. Finally, the design27

nature itself of blockchain provides resilience and irreversibility, because each node on

the work stores a complete copy of the distributed ledger (Tapscott & Tapscott, 2016).

From these design principles arise a plethora of benefits:

• Reduction in costs of overall transactions and IT infrastructure

• Irrevocable and tamper-resistant transactions

• Reduction in systemic risks (by eliminating credit and liquidity risks)

• Consensus in a variety of transactions

• Ability to store and define ownership of any tangible asset

• Increased accuracy of trade data and reduced settlement risk

• Near-instantaneous clearing and settlement

• Improved security and efficiency of transactions

• Enabling effective monitoring and auditing by participants, supervisors and reg-

ulators

2014-2015 were the “buzz years” in which blockchain got serious attention and invest-

ment from financial services and venture capital firms. Many consortiums were created

to accelerate adoption, innovation and the development of common standards to harness

all the theoretical benefits of blockchain. Therefore, we are now living critical years for

this technology that needs to demonstrate sustainable value and show adoption beyond

theory (Jimit, Aaditya, Archit, Ronak, & Ankur, 2016). The startups backed by investors

need to show results to justify the large sums of funding, and to solve scalability and

throughput issues to cross the chasm to mainstream adoption (Moore, 2014).

2.9 The Value Net Framework

In 1996, Adam Brandenburger and Barry Nalebuff developed a framework to identify the

key players in a given business. To make better strategic decisions, the interdependencies

between a company and four other types of participants in the network need to be out-

lined. These key players are:

• Customers: The people or organizations buying the company’s product or ser-

vice;

• Suppliers: These are the internal or external players that provide the company

with the necessary resources for it to produce its products or deliver its services;

• Competitors: The direct and indirect players sharing the company’s target mar-

ket by their similar offerings;

• Complementors: The players whose offerings complement the company’s. The

availability of both offerings creates positive synergies and augment the value

of each offering.28

Competitors

Suppliers nVotes Consumers

Complementors

Figure 7: The Value Net Framework

The Value Net Model is organized in two axes. The horizontal one represents a simplified

supply chain in which resources flow from the left, are transformed by the company in a

certain way to be delivered to consumers. The vertical axis represents competitors, which

are usually taken into consideration when defining a company’s strategy, as well as com-

plementors. The latter are usually overlooked at, even though they have the potential of

proposing growth opportunities from cooperation. The framework illustrates the symme-

tries between all players, and its authors recommend having the full picture in mind when

making strategic decisions.29

3 METHODOLOGY

3.1 Research Design

3.1.1 Qualitative Methodology

In its broadest sense, research is a systematic process aiming at improving the knowledge

of a particular topic (Merriam, 2009). We are engaging in this process in an attempt of

contributing to the knowledge base in the field of blockchain. The main motivation for

this thesis is to demystify this technology, and provide an overview of how it is currently

applied in various industries to create new ways of doing business and producing value.

Engaging in such a systematic inquiry about blockchain applications involves choosing

an appropriate study design that will enable us to answer our previously stated research

questions.

These motivations are best approached through a qualitative research design. For

Maanen (1979), qualitative research is “an umbrella term covering an array of interpretive

techniques which seek to describe, decode, translate, and otherwise come to terms with

the meaning, not the frequency, of certain more or less naturally occurring phenomena”.

Basically, qualitative researchers focus on how respondents interpret the world and how

their own perspective brings meaning to the object under investigation. Since blockchain

entrepreneurs and workers, with their wide variety of backgrounds, each have a different

understanding of the complex topic of blockchain, our epistemological perspective will

be interpretive and constructivist. This perspective will allow us to describe and interpret

the understandings of these players from various industries, to come up with context-

bound conclusions.

Merriam (2009) identified four main characteristics to the nature of qualitative re-

search. First, the focus is on meaning and understanding. As Patton (1985) explains, qual-

itative research is “an effort to understand situations in their uniqueness as part of a par-

ticular context and the interactions there.” The key concern is understanding blockchain’s

current and potential applications from the emic perspective, that is the participants’ view

on the topic.

The second characteristic is both an advantage and a disadvantage. By being the pri-

mary mean of data collection, the researcher is particularly fit to directly adapt his ques-

tions and be responsive to interviewees. However, the researcher must be aware of the

biases that might influence his reading and understanding of respondents. These biases

must be monitored in order to interpret data as neutrally as possible and free of influence.You can also read