Das Webinar beginnt in Kürze - WKO

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Das Webinar beginnt in Kürze...

PERSPEKTIVEN DER BRASILIANISCHEN WIRTSCHAFT KLAUS HOFSTADLER Wirtschaftsdelegierter AußenwirtschaftsCenter São Paulo 06.10.2020

WAS ERWARTET SIE?

SITUATION

ÖSTERREICHISCHER

EXPORTEURE UND

INVESTOREN IN

BRASILIEN Q&A SESSION

VORSTELLUNG DER KEYNOTE:

WEBINAR-REIHE PERSPECTIVES OF

THE BRAZILIAN

“EXPERT FORUM ECONOMY AND ITS

BRAZIL” MAIN SECTORS

3

Webinar-Reihe

EXPERT FORUM Brazil

1

exklusiv und kostenlos

für Mitglieder der WKÖ

4

EXPERT FORUM Brazil: Webinare im Oktober 2020

14.10.2020 Sicherheit & Verteidigung

Manfred Hauser, Geschäftsführer, Frequentis Brasilien

21.10.2020 Gesundheit und Life Sciences

Roberto Latini, CEO Latinigroup

28.10.2020 Öl- und Gassektor

Ronaldo Martins, Geschäftsführer Fa. ENSOTEC & Ex-Petrobras-Einkaufsmanager

5

EXPERT FORUM Brazil: Webinare im November und

Dezember

04.11.2020 Gründung und (Krisen-) Management von Niederlassungen in Brasilien

11.11.2020 Eisenbahnsektor

18.11.2020 Abfallwirtschaft, Wasserversorgung und Abwasser

25.11.2020 Dienstleistungsexporte nach Brasilien

02.12.2020 Bergbausektor

09.12.2020 Warenexport nach Brasilien: Finanzierung und Steuern

6

EXPERT FORUM Brazil: Webinare im Jänner, Februar und

März 2021

13.01.2021 Export und Registrierung von Wein und Nahrungsmitteln

20.01.2021 Brasiliens Startup-Ökosystem / FinTech Cluster São Paulo

27.01.2021 Erneuerbare Energiewirtschaft

24.02.2021 Automobilindustrie

03.03.2021 Geschäftskultur & Etikette in Brasilien

10.03.2021 Land- und Forstwirtschaft

17.03.2021 Maschinenexporte nach Brasilien und Normen

24.03.2021 Incoming-Tourismus aus Brasilien

7

Situation

österreichischer

2 Exporteure und

Investoren in Brasilien

8

COVID-Situation in Brasilien

• offiziell 146.352 Todesopfer COVID-Todesopfer, nach Zeitpunkt der Registrierung

(Stand: 04/10) Quelle: brasilianisches Gesundheitsministerium covid.saude.gov.br

• Homeoffice bzw.

Schichtarbeit in Büros

• „Normalität“ in Einzelhandel,

Gastronomie

• Reisebeschränkungen für

Brasilianer

• Reisen nach Brasilien wieder

möglich

9Österreichische Exporte nach Brasilien (in Mio EUR)

Quellen: Statistik Austria, The Economist

1061

1000

950

900 833

850

800

750

700

650

600

550

500

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

10207 197

194,4

Österreichische 200

190

179,4

176,8

Exporte nach 180

170

Brasilien (in Mio EUR) 160

150

Quelle: Statistik Austria

140 129,1

130

120

Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020

EUR-BRL Wechselkurs

in letzten 6 Quartalen

Quelle: EZB

25. Februar: erster

bestätigter COVID-

19-Fall in Brasilien

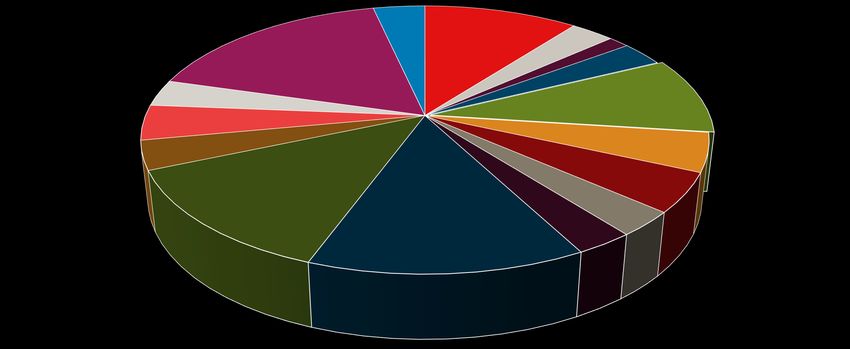

11Österreichische Exporte nach Brasilien breit gefächert

(Gesamt im 1 HJ: 326 Mio EUR)

Rest (Rohstoffe, Getränke; 34,0 Fertigwaren (Möbel, Waffen und Munition;

Tierfutter, etc.); 11,4 Kunststoffwaren etc.); 4,6

9,7

Pharma-Produkte; 55,5

Luftfahrtzulieferungen; Messgeräte (inkl.

10,5 medizin. Geräte); 9,6

Chemische Erzeugnisse;

Fahrzeuge; 13,8

30,3

Motoren ; 11,4 bearbeitete Waren

(Feuerfeststoffe, Papier,

Aluminium, etc.); 15,2

Elektrische Maschinen

(vor allem

Wechselrichter); 42,1 Eisen und Stahl; 15,4

Maschinen und Anlagen; Metallwaren (Beschläge, Nickellegierungen;

43,6 Werkzeuge, etc.); 9,2 9,7

Quelle: Statistik Austria, in Mio EUR 12Österreichische Importe aus Brasilien im 1. Halbjahr 2020

(Gesamt 111,8 Mio EUR)

Rest (Schuhe, etc.)

4%

Nahrungsmittel

Maschinenbauerzeugnis (Früchte, Fruchtsäfte,

se und Fahrzeuge Fleisch, Kaffee, etc.)

21%

30%

Bearbeitete Waren

(Eisen, Stahl, Metalle,

Metallwaren, Papier, Rohstoffe (Eisenerz,

etc.) Feuerfeststoffe,

18% Zellstoff, etc.)

17%

Chemische Erzeugnisse

10%

Quelle: Statistik Austria, EUR, 1 HJ 2020 13Investitionen

• Österreich Brasilien Direktinvestitionen

(Bestand, in Mio EUR, Quelle: OeNB)

• 200 österreichische Niederlassungen in Brasilien

3 500

(2015: 250 Niederlassungen) 3 000

• österreichischer FDI-Bestand stabil, wichtiger 2 500

2 000

Arbeitgeber 1 500

• Brasilien Österreich 1 000

• Österreich traditionell wichtiger Standort für

500

0

Steueroptimierung brasilianischer Konzerne, 2017 2018 2019

Doppelbesteuerungsabkommen FDI Österreich in Brasilien FDI Brasilien in Österreich

14Keynote by Alessandra

Ribeiro, Tendências

3 Consultoria Integrada:

PERSPECTIVES OF THE

BRAZILIAN ECONOMY AND

ITS MAIN SECTORS

15Perspectives of the Brazilian

Economy and its Main Sector

October 2020 | Alessandra Ribeiro

Powered byIntroduction 2

▪ The adverse effects of the pandemic for the Brazilian Economy in the 2º. quarter were

in line with the average contraction (considering developed and emerging economies)

▪ The fiscal and monetary stimuli have been essential to limit the negative effects

▪ The uncertainty is still high considering: a) the Emergency aids´end and its economic

impacts and b) the attempts to create a permanent social program given the complex

fiscal situation

▪ Despite the adverse effects of the pandemic, there are important advances in the

microeconomic agenda: Sanitation, Gas Law and Banking System Agenda

Powered byEconomic impacts – 2º. Quarter GDP 3

2o. quarter GDP (y/y)

5% 3,2%

0%

-5% -2,9%

-5,3%

-10% -7,7% -7,9% -8,5%

-9,0% -9,1%

-9,9% In general lines, the most affected

-11,3%-11,4%

-15% Average - countries by the pandemic show

12,5% the worse results

-16,3%

-17,3%-17,7%

-20% -18,9%-18,9%

-21,7%-22,1%

-25% -23,9%

-30%

Estados Unidos

Alemanha

Indonésia

Polônia

França

China

Russia

México

Índia

Coreia do Sul

Japão

Suécia

Itália

Espanha

Brasil

Portugal

África do Sul

Reino Unido

Holanda

Powered by

Source: BloombergRecovery Format 4

Permanent effects of the pandemic and an environment of political- fiscal

tension should shape the recovery format

THEORETICAL MODEL OF RESUMPTION

C

B

A

t-1 t t+ t++ t++

Powered by

Elaboration: Tendências.Main sectors - recovery 5

The recovery trend has been heterogeneous among sectors

Comparison to its pre-

pandemic level

▪ Retail sales: 5.3%

above

▪ Industrial production:

6.0% below

▪ Services: 12.5%

below

Powered by

Elaboration: Tendências.GDP 6

GDP was upward revised given the strong effects of the government stimuli

this year. Caution increased in relation to next year.

GDP (YoY)

QUARTERLY

7,5%

10,0%

PERFORMANCE

6,1%

5,8%

8,0% 5,1%

4,0%

4,0%

6,0%

▪ Worst moment in the

3,2%

3,0%

2,7%

2,9%

2,4%

2,1%

1,9%

4,0%

1,3%

1,3%

2nd quarter.

1,1%

0,5%

2,0%

▪ Recovery will be

0,0%

more evident from

-0,1%

-2,0%

the 3th and 4th

-4,0%

-3,3%

-3,5%

-6,0% quarter on.

2020-5,6%

-8,0% ▪ Subsequent growth

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2021

2022

2023

2024

will be very gradual.

Powered by

Source: Brazilian Institute of Geography and Statistics. Elaboration and projections: Tendências.GDP 2017 2018 2019 2020

7

2021

Consumption and investments should GDP 1,3% 1,3% 1,1% -5,6% 2,9%

suffer the most this year Agricultural 14,2% 1,4% 1,3% 1,2% 0,3%

Industry -0,5% 0,5% 0,5% -5,6% 3,7%

Services 0,8% 1,5% 1,2% -5,9% 2,8%

Caution factors

2017 2018 2019 2020 2021

GDP 1,3% 1,3% 1,1% -5,6% 3,4%

▪ High level of economic uncertainty.

▪ Low growth of the main partner Household 2,0% 2,1% 1,8% -6,6% 3,0%

countries.

Government -0,7% 0,4% -0,4% -2,8% 1,6%

▪ Financial conditions of families and

GFCF -2,6% 3,9% 2,2% -7,0% 5,3%

small companies.

Exports 4,9% 4,0% -2,5% 1,2% 2,7%

Imports 6,7% 8,3% 1,1% -7,6% 5,0%

Powered by

Source: Brazilian Institute of Geography and Statistics. Elaboration and projections: Tendências.Labor Market 8

The fall in civilian labor force limits the increase

in the unemployment rate

Occupation 2018 2019 2020 2021

EAP/WAP 62,5% 62,7% 61,8% 62,8%

Occupation (growth %) 1,4% 2,0% -7,2% 5,5%

Unemployment rate (%) 12,3% 11,9% 13,9% 15,7%

Income 2018 2019 2020 2021

Real income (growth %) 1,5% 0,4% 4,7% -2,7%

Real wage mass (growth %) 3,0% 2,5% -2,6% 1,5%

Powered by

Source: Brazilian Institute of Geography and Statistics. Elaboration and projections: Tendências. EAP: Economically Active

Population. WAP: Working Age Population.Total income 9

Short-term perspectives

The positive impact of government transfers is expected to more than

compensate the fall in the labor income. However, the hangover effect of

Emergency Aid should be reflected in substantial total mass´fall in 21.

Total Income

2020 4,5

TRILHÕES

4,2

4,3

+4.5%

4,0

4,0

4,0

3,9

4,1

3,9

3,9

3,8

3,8

3,9

2021 3,7 3,6

3,4

3,5

-4.2%

3,2

3,3

3,1

2,9

2,7

2,5

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Source: IBGE. The total income is an estimate by Tendências and considers the data on labor income (IBGE); transfers from Bolsa Família Powered by

(Ministry of Citizenship); Social Security benefits (Ministry of Economy); and other sources of income (IBGE and Ministry of Economy).Consumer inflation (IPCA) 10

Inflation well-behaved despite some pressures

▪ Weak economic activity leads to reduced inflation for 2020 and 2021.

▪ Commodities and depreciated currency are putting some pressures

in items such as food

14%

10,7%

IPCA

12%

10%

7,6%

6,5%

6,4%

6,3%

8%

5,9%

5,9%

5,9%

5,8%

5,7%

4,5%

4,3%

6% 4,3%

3,7%

3,3%

3,2%

3,1%

3,0%

3,0%

2,9%

4%

1,9%

2%

0%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

Powered by

Source: Brazilian Institute of Geography and Statistics. Elaboration and projections: Tendências.Interest Rate 11

Expectation is for

Selic to be maintained at 2.0% for almost 1 year

▪ The main channels of transmission of the

INTEREST RATE

pandemic on prices are disinflationary. End of period

18,00%

17,75%

▪ A further drop is less probable

14,25%

13,75%

13,75%

20%

13,25%

11,75%

11,25%

11,00%

10,75%

10,00%

▪ Selic is expected to rise again only at 15%

8,75%

7,25%

7,00%

6,50%

6,25%

6,25%

the end of 2021 considering

5,00%

10%

4,50%

3,00%

2,00%

responsible fiscal policy 5%

0%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

Powered by

Source: Brazilian central bank. Elaboration and projections: Tendências.Fiscal situation 12

Even considering the maintenance of the responsible fiscal rules

public debt shows a substantial increase

Public Debt (% GDP)

Powered by

Source: Brazilian central bank. Elaboration and projections: Tendências.Exchange Rate EXCHANGE RATE

End of period

13

5.35

5.25

R$ 6.0

▪ Local issues should limit the recovery of the

4.85

4.80

4.79

BRL, by preventing a further decline in risk R$ 5.0

4.03

3.90

3.87

premiums.

3.31

3.26

R$ 4.0

2.66

▪ Central Bank’s actions are important, but only

2.65

2.34

2.34

2.34

R$ 3.0

2.14

2.04

1.88

mitigate the global trajectory.

1.77

1.74

1.67

R$ 2.0

R$ 1.0

R$ 0.0

2004

2009

2010

2011

2012

2013

2018

2019

2020

2021

2022

2005

2006

2007

2008

2014

2015

2016

2017

2023

2024

▪ In real terms, exchange rates show a significant

depreciation, which reinforces the expectation of a

certain accommodation throughout the second

semester, although limited by domestic risks.

Powered by

Source: Bloomberg e Central Bank of Brazil. Elaboration and projections: Tendências.Sectorial Recovery Timeline | The 10 Largest Industrial Sectors 14

Petroleum Mining and Oil Paper and Machinery and Non-metallic

products and (weight: 11.8%) cellulose equipment minerals

biofuels (weight: 3.6%) (weight: 12.0%) (weight: 3.4%)

Maturation of major

(weight: 10.9%)

investments in Greater Asian In addition to low Gradual recovery of

Production recovery Vale's mining and demand and interest rates and the real estate

given the great new oil platforms. expansion of controlled inflation, market and

industrial idleness. productive capacity the positive outlook investments in

in Brazil. for agricultural infrastructure.

production benefits

the production of

machinery.

VERY FAST FAST

recovery recovery

Powered by

Source: Brazilian Institute of Geography and Statistics. Elaboration and projections: Tendências. Classification criteria

based on the accumulated variation between the level of industrial production in 2022 and the average 2017-19.Sectorial Recovery timeline | The 10 Largest Industrial Sectors 15

Food Other chemicals Metallurgy Rubber and Automotive

(weight: 15.3%) (weight: 5.6%) (weight: 5.2%) plastic products (weight: 9.3%)

(weight: 3.4%)

Sugar production High external Maintenance of Higher exports and

settles down and competition and economic Expansion of investments, amid

cattle slaughter absence of large uncertainties and China's production the gradual

continues at investments. high idle capacity in capacity and recovery of

reduced levels. several industrial weakening global domestic demand.

segments. demand.

SLOW VERY SLOW

recovery recovery

Powered by

Source: Brazilian Institute of Geography and Statistics. Elaboration and projections: Tendências. Classification criteria

based on the accumulated variation between the level of industrial production in 2022 and the average 2017-19.Conclusion 16

The Brazilian economy should resume its pre-pandemic GDP level in

2022

Baseline scenario

Strong recovery in the first moment and a

gradual pace in the next ones

The permanent effects of the

pandemic and uncertainties related to Positive Factors:

political/fiscal issue limit the Stimulative monetary policy, precautionary

recovery trend savings and advnaces in microeconomic

agenda

Caution Factors:

High level of uncertainty (fiscal issue), end of

emergency programs and effects for small

businessess/employment.

Powered byPowered by

Stellen Sie uns

Ihre Fragen!

Bitte über die Chatfunktion rechts stellen.

Q&A SESSIONKlaus Hofstadler

Wirtschaftsdelegierter

Österreichisches AußenwirtschaftsCenter São Paulo

Av. Dr. Cardoso de Melo, 1340 conj.71

04548-004 São Paulo

Brasilien

T +55 11 30 44 99 44

saopaulo@wko.at

wko.at/aussenwirtschaft/br

2You can also read