France : towards a universal pension system - Fiscal sustainability and social systems Challenges and policy options for the next decades ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

France : towards

a universal

pension system

Berlin 22 June 2018

Fiscal sustainability and social systems

Challenges and policy options for the next decades

An overview

THE FRENCH PENSION SYSTEM

2

2

SINCE 1993, MAJOR PENSION REFORMS HAVE BEEN CARRIED OUT.

SIGNIFICANT EFFORT HAS BEEN MADE TO IMPROVE THE FINANCIAL

SITUATION

• 1993 (the « Balladur » reform) : review of the pension calculation

formula (25/40 years) and price indexation

• 2001 : creation of a Pensions Reserve Fund (FRR - Fonds de Réserve

pour les Retraites)

• 2003 (the « Fillon » reform) : extension of period of insurance

required for a full-rate pension; long-career-based early retirement

scheme

• 2008 (special regimes’ reform) : gradual convergence with existing

general regime (retirement age, period of insurance, contribution

rates, indexation, bonuses and penalties, etc.)

• 2010 (the « Woerth » reform) : increase of minimum retirement

age from 60 to 62 years, full-rate retirement age from 65 to 67 years

• 2014 (the « Touraine » reform) : extension of period of insurance

required for a full-rate pension (period of insurance required : 43 years

for those born from 1973) ; retirement from arduous work scheme

(« arduous work risk prevention account”, now called “job risk

prevention account”, includes an opportunity for workers to retire up

to two years before the minimum retirement age or individual training 3

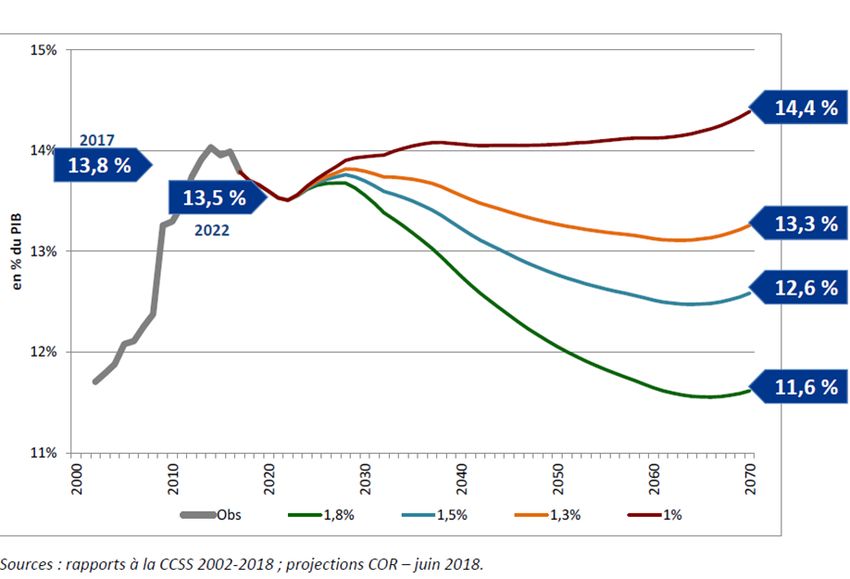

A FINANCIAL POSITION THAT IS CLOSE TO BALANCE

RELATIVELY POSITIVE PROSPECTS

Pension system’s financial balance (%

of GDP)

Pension system’s

financial balance (→)

2017 : 0 % of GDP

2022 : - 0,2 % of GDP

2040 : +0,3 to -1% of GDP

(1,8 to 1,0 % productivity)

2070 : +1,1 to -1,5 % of

GDP (c.a.)

Public pension spending (%

of GDP)

Public pension spending

(↘)

2017 : 13,8 % of GDP

2022 : 13,5 % of GDP

2040 : 12,8 to 14,1 % of GDP

(c.a.)

2070 : 11,6 to 14,4% of GDP

(c.a.)

4THE AVERAGE EFFECTIVE RETIREMENT AGE HAS INCREASED

OVER RECENT YEARS (STARTED FROM A LOW BASE)

Impact on labour market

due to the effect of past

Average effective age of retirement pension reforms :

(by gender) • Increase in older workers

employment rate

• Continued increase even

post-crisis

• Marked increase in the 55-

59 group

• Generations born between

1951 and 1955 :

percentage of retirees at 61

years has decreased from

73 % to 34 %.

Average effective age of

retirement in 2016 : 61 y

and 10 m

• Women : 62 y and 1 m

• Men : 61 y and 6 m

Average effective age of

retirement (projection)5PENSIONERS’ HIGH STANDARD OF LIVING

Standard of living of 65 years + One of the lowest elderly

% average income of the population poverty

rates in the OECD

Total 65 à 74 ans 75 ans et plus

25,0

20,0

15,0

10,0

5,0

0,0

66 ans et plu s ( ↗) 6 6-75 ans 76 an s et plus

Source : OECD (2017), Pensions at a Glance, indicator Source : Eurostat (2016)

6.1. Note : poverty threshold at 60 % of median

household income

642 RÉGIMES

EXPECTED DE RETRAITES

YEARS EN 2018

IN RETIREMENT ARE RECORD HIGH

Life expectancy

France is indeed the OECD country

and effective age of labour market

with the longest average retirement

exit (2016)

espérance

Eséprance de viede

Expected vie résiduelle

years after

résiduelle à la sortie

labour

à la sortie du marché

market

du marché du

period, mainly due

27

du travail

travailexit

75

to early labour market exit (2016)

âge deAge ofdu

sortie labour

marchémarket exit

du travail (échelle de droite)

Average Expecte Expecte

effective d years d years

Normal

age of after at

pensiona

labour labour normal

ble age

market market pensiona

22 70 exit exit ble age

France 61,6 60,2 25,6 24,2

OCDE 63,9 64,4 20,3 20,8

Differen - 2,3 - 4,2 + 5,3 + 3,4

tial

17 65 German 65 63,2 21,1 19,3

y

Belgium 65 60,5 21,7 17,2

Italy 65 61,7 21,7 18,4

Swede 65 65,2 20,3 20,5

12 60

n

Source : OECD (2017), Pensions at a Glance

Source : OECD (2017), Pensions at a Glance Note : Normal pensionable age is shown for individuals

retiring in 2016 and assuming labour market entry at age

20

7A HIGH LEVEL OF INTRA-GENERATIONAL SOLIDARITY

• A mixed system : both a contributory system and a

non-contributory system

• Redistribution aspects of the french pension system

– Early retirement is possible for those with a disability, a long career, or a

history of arduous work

– Basic scheme and contributory minimum pensions

– Periods credited as periods of insurance (periods of cessation of work in the

case of sickness, maternity, disability, unemployment…)

– Pensions increase for raising children, reversion for surviving spouses and ex-

spouses

– 20% of pensions rights (employees and public employees) provided through

non-contributory schemes

• Significant redistributive effects

The minimum pension scheme and non-contributory benefits help achieve one of

the lowest elderly poverty rates in the OECD. First-tier pensions and instruments

for periods of unemployment and childcare generate substantial redistribution

– Income earning : a one-to-six ratio

– Retirement pensions : a one-to-four ratio (due to non-contributory benefits)

8THE SYSTEM REMAINS DEEPLY FRAGMENTED : 42 PENSION

SCHEMES (I)

Legacy of history and professional status rationale

:

42 mandatory retirement schemes

Source : HCRR

9THE SYSTEM REMAINS DEEPLY FRAGMENTED : 42 PENSION

SCHEMES (II)

• Unusually, in the private sector, the pension system has two

public mandatory tiers: a general defined benefit scheme

managed by Social Security (régime général) and a point system

managed by social partners (régimes complémentaires, notably

AGIRC-ARRCO), together representing about 70% of benefits paid

(financed on a pay-as-you go basis)

• The other 30% come from special regimes including those

covering civil servants

• Voluntary pensions play a limited role as many saving

instruments benefit from tax incentives and target long-term

savings

• The complexity of the pension system comes from the

duality of the mandatory system in the private sector and

also from the substantial differences in the treatment of

private-, public-sector workers and those covered by

special regimes

• Rules to compute contributory retirement pension and

non-contributory benefits differ across schemes 10A SYSTEM THAT CAN DISCOURAGE OCCUPATIONAL

MOBILITY

A typical case: a nurse could A single

belong to five schemes during occupation

her career Five different

pension schemes

Nurse in a Nurse in a Self-employed Working in a

private clinic nurse medical humanita Régime général

public hospital rian association

Régime de base de

la CARPIMKO

Régime Régime

général de Régime de

général de la

la sécurité base de la

sécurité

Caisse CARPIMKO

sociale sociale ARRCO

Nationale de

Retraite des

Agents des Régime

Collectivités Régime complémentaire de

Locales ARRCO complément

ARRCO la CARPIMKO

aire de la

CARPIMKO

CNRACL

Source : HCRR

11A FUNDAMENTAL NEED FOR THE PENSION SYSTEM TO ADAPT

TO THE LABOUR MARKET

Information on people's

pension entitlements has

improved recently, but a

complexity issue

Generations born between

1949 et 1992, all mandatory

schemes combined (2017) :

o In average, individuals

belong to 3,1 pension

schemes

o 1/3 of individuals

belong to 4 pension

schemes

o 250 000 people belong

to 7 or more pension Source : GIP Union Retraite (inter-

schemes institutional information agency on

people's pension entitlements) 12COMPLEXITY IS DETRIMENTAL TO THE TRUST IN THE SYSTEM

• The French pension system faced various

challenges :

o The overall complexity feeds the impression that other

groups might be treated favourably.

o Risk of loss of confidence in the system and doubts

about the sustainability of the pension system

• A paradox :

o Reforms over the last decades have improved the

viability and continuity of the retirement pension system

o Pensioners’ standard of living has never been higher

o Distrust remains regarding the financial sustainability

and the level of pensions in the future

13Prospects

MOVING TOWARDS A UNIVERSAL PENSION

SYSTEM

14

14THE REFORM PROPOSAL

• Strong campaign commitment of the President of

the French Republic

• The reform proposal :

“Our project is not to change this or that parameter of our

pension system.

It is to restore trust, (...)

It is to clarify rules once for all, by installing a universal

system, fair, transparent and sustainable (...)

We will create a universal pension system where one euro

contributed offers the same pension rights, whatever the

period it was contributed, whatever the occupation or status

of the person who contributed.”

Emmanuel Macron, En Marche platform

15THE UNIVERSAL PENSION SYSTEM : CLARITY, FAIRNESS AND

SUSTAINABILITY

The principles of the systemic reform :

• From a professional status-based system to a universal system

(common to active people)

• All 42 mandatory pension schemes concerned

• Renewed contributory principle: pension will be calculated on

the basis of work-related earnings adjusted over the person's

entire career (compared to earnings reference based on the

average of the 25 best years in private sector or on the last six

months preceding retirement in public sector today)

• Renewed non-contributory principle: while preserving a high

level of intra-generational solidarity, the universal pension

system provides opportunities to review, update and align the

non-contributory instruments

• A common unit of account (points or notional accounts)

• « For every euro contributed to the pension system, the same

pension rights »

• A balanced pension system from the date of its coming into force;

16BEHIND THE UNIVERSAL PENSION SYSTEM,

A COHESIVE AND INTEGRATED VISION OF SOCIETY

A realistic but ambitious political project :

• Solidarity between active people, whatever their status, so

that trust is restored

• Common non contributory benefits, so that fairness is

guaranteed

• Modernisation of the social protection system so that it

encourages professional mobility

A political project with fiscal and technical implications

:

• A balanced system from the date of its coming into force,

• A review of contributory efforts

• A reform which will improve transparency and facilitate

management of the pension system (monitoring, correction

of deviations),

• An organisational transformation in the coming years

17Prospects

THE METHOD : REFORM EXPERIENCE,

REFORM EXPERIMENT

18

18HIGH COMMISSIONER FOR PENSION REFORM’S MANDATE

• Appointment of a High Commissioner for Pension

Reform,

Mr Jean-Paul Delevoye (September 2017)

High Commissioner in charge of the reform (with a team of

special advisers) :

o organise the dialogue with the main actors in the field of

pensions (including social partners)

o coordinate at the inter-ministerial level the preparation of the

pension reform and the drafting of legislative and regulatory

projects

o monitor their implementation

• Universal pension system under preparation in 2018

• Universal pension system Act expected to be voted on

in 2019

• Gradual introduction of the universal pension system

19Une méthode à confirmer – Un dialogue constructif, transparent et permanent

AN OPEN METHOD : A TRANSPARENT, CONTINUOUS AND

CONSTRUCTIVE DIALOGUE WITH SOCIAL PARTNERS AND CIVIL SOCIETY

Communication of the results of the public

participation

HCRR

CONCERTATION PARTICIPATION

SOCIAL PARTNERS FINDINGS CITIZENS

EXPECTATIONS

Results of the public

PROPOSALS participation

used to inform

parliamentarians

Parliamentarians involved

in citizens' workshops

INFORMATION

JOURNALISTS

INFORMATION

PARLIAMENTARIANS

20You can also read