Challenges and Learning Points in the Danish Pension System - Tela

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Challenges and Learning Points in the Danish Pension System Presentation at Tela-ETLA seminar on “Intergenerational risk-sharing – “from early age to old age” Musiikkitalo, Helsinki, February 8, 2018 Svend E. Hougaard Jensen, Ph.D. Professor, ECON, CBS Director, PeRCent, CBS Chairman, Scientific Council, Bruegel

Outline

- Suggested by the organizers…

• Brief description of the pension scheme:

– the most important pension schemes, retirement ages and typical

replacement rates, and the role of voluntary pensions.

• Description of the earnings-related system:

– The key decision makers (e.g. the role of social partners), pension

funds, benefit accrual, DB or DC.

• Financial sustainability:

– what would happen if future fund returns turn out to be much

lower than the historical returns? How would the system adjust?

• Questions to be answered:

– What is especially good about the Dutch/Danish pension

system?

– What are the main concerns with the system?

– What are the main topics in current pension policy debates?

Mercer Global Pension Index (2017)

Denmark vs. ROW

Index

Grade Value Countries Description

A first class and robust retirement income system that delivers good benefits, is

A > 80

sustainable and has a high level of integrity.

Denmark

B+ 75 - 80 Netherlands

Australia

Norway New Zealand A system that has a sound structure, with many good features, but has some areas

Finland Chile for improvement that differentiates it form a A-grade system.

B 65 - 75 Sweden Canada

Singapore Ireland

Switzerland

Germany

C+ 60 - 65 Colombia

UK A system that has some good features, but also major risks and/or shortcomings

France Brazil that should be addressed. Without these improvements, its efficacy and/or long-

US Austria term sustainability can be questioned.

C 50 - 60

Malaysia Italy

Poland

Indonesia Mexico

A system that has some desirable features, but also major weaknesses and/or

South Africa India

D 35 - 50 omissions that need to be addressed. Without these improvements, its efficacy and

Korea Japan

China Argentina sustainability are in doubt.

E < 35 A poor system that may be in early stages of development or non-existent.

Source: Mercer (2017)Mercer Global Pension Index (2017)

Denmark vs. ROW

Denmark

Year Rank Overall Index Value Adequacy Sustainability Integrity

2017 1 78.9 76.5 79.8 81.3

2016 1 80.5 75.8 85.3 81.4

2015 1 81.7 77.2 84.7 84.5

Finland

Year Rank Overall Index Value Adequacy Sustainability Integrity

2017 5 72.3 70.2 61.3 91.1

2016 4 72.9 70.6 62.2 91.5

2015 6 73.0 70.7 61.8 92.4

Netherlands

Year Rank Overall Index Value Adequacy Sustainability Integrity

2017 2 78.8 78.0 73.5 87.5

2016 2 80.1 78.2 77.0 87.7

2015 2 80.5 80.5 74.3 89.3•Basic design characteristics…

The Danish pension system

Three pillars

Private, individual saving

schemes:

• Flexible and voluntary

• Banks and insurance

companies

3rd Accumulated pension savings, 2016

Pillar • 612 billion USD

Funded, DC: • 216% of GDP

• ATP: compulsory, all

contribute; relatively low

contribution rates

• OP: employment

relationship or collective 2nd Benefits, per person, annual, EUR, 2018

agreement between social Pillar • Basic flat-rate pension 10.059

partners • Means-tested supplements 10.851

• Total 20.911

PAYG, DB:

• Basic flat-rate pension

Public expenditures, 2016

• Means-tested

supplements 1st Old-age pension

• Indexed to wages * Pillar • 128 billions of DKK / 6,6% of GDP

Early retirement benefits

Source: Statistics Denmark & Danish FSA & OECD • 14 billions of DKK / 0,7% of GDPPublic pension (PAYGO)

Finland vs. Denmark, 2018

in EUR Denmark Finland Difference

monthly yearly monthly yearly monthly yearly

Denmark

Basic amount (same for everyone) 838 10056

Supplements Illustration of

means-testing

if married/cohabiting 448 5374

if single 904 10847

Finland

Basic maximum amount (means tested)

if married/cohabiting 629 7546

if single 558 6693

Supplementary guarantee pension

if married/cohabiting 146 1757

if single 217 2610

Total maximum amount

if married/cohabiting 1286 15429 775 9303 -510 -6126

if single 1742 20903 775 9303 -967 -11600

Source: Ældre Sagen & KelaPublic, old-age transfer payments, DK

Old-age pensions & early retirement benefits

DKK mio.

140 000

120 000

100 000

80 000

60 000

40 000

20 000

-

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Old-age pensions including supplements Early retirement

Source: Statistics DenmarkThe Bismarckian Factor Estimates for selected countries Source: Krieger, T. and S. Traub (2013). Note: data not available on empty cells.

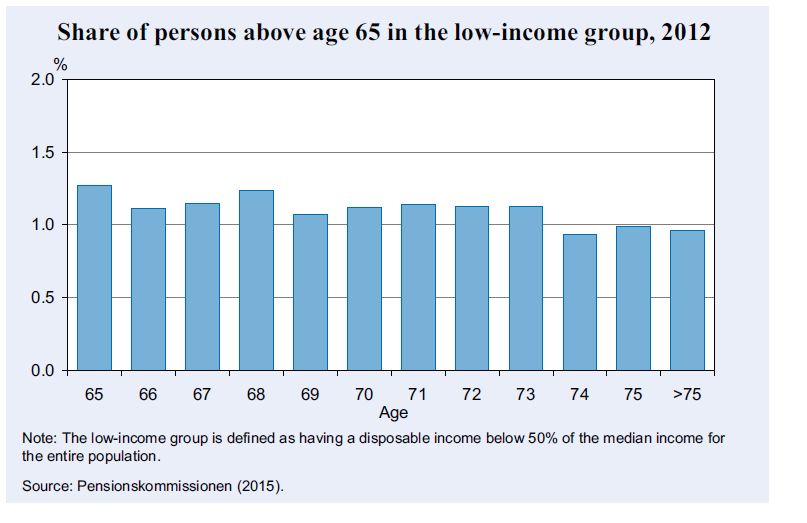

Risk of poverty

Share of persons in the low-income group*

9%

8%

7%

6%

5%

4%

3%

2%

1%

0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total, DK Old-age pensioners, DK

*the low-income group is defined as having a disposable income below 50% of the median income of the entire population

Source: Statistics DenmarkRisk of poverty Share of elderly in the low-income group

Pension investments

% of GDP, 2016

250%

Exceptionally high in

218%

Denmark

200%

155%

150%

135%

100%

80%

57%

50%

6% 7%

0%

Denmark Netherlands Finland Germany Italy Sweden United States

Source: OECDOP schemes

Contribution rates

Public employees

YearAccumulated pension savings in Denmark

1998-2015, billions of DKK

Investor 1998 2000 2005 2010 2015

1. Life insurance companies 511 650 953 1.351 2.074

2. Multi-employer pension funds 214 270 381 478 672

3. Pension funds, firms 38 43 42 51 60

4. Banks 191 215 298 405 446

5. Public pension funds 255 330 479 817 831

a. ATP 200 247 365 758 781

b. SP 6 21 51 2 0

c. LD 49 62 64 57 50

Total 1,208 1.507 2.154 3.103 4.083

Share of GDP 1,02 1,14 1,36 1,71 2,01

Source: Finanstilsynet (Danish FSA)Composition of pension schemes

2010-2016, billions of DKK

2010 2011 2012 2013 2014 2015 2016*

1. Annuities 43,7 42,5 50,6 54,6 56,6 59,4 61,6

2. Periodic installments 45,1 48,9 41,0 48,8 50,1 48,2 49,1

3. Indexed 0,10 0,08 0,07 0,05 0,04 0,02 0,02

4. Capital or supplementary lump-

sums 16,0 15,5 15,9 0,08 0,03 0,02 0,02

5. Age savings - - - 1,7 3,1 4,0 4,4

Total pension schemes 104,9 107,0 107,6 105,2 109,8 111,6 115,1

a. Of which banks 17,7 17,6 15,6 10,1 9,8 7,1 6,6

b. Of which insurance companies 87,2 89,4 91,9 93,4 96,9 100,5 104,1

c. Of which unclassifiable - - - 1,7 3,1 4,0 4,4

Source: SKATDecreasing number of pension funds Number of Danish pension funds Source: Insurance and Pension (2017)

Public vs. private pensions Private pensions will dominate from app. year 2040

Replacement rates

International comparison, 2016

120

100

80

60

40

20

0

Men Women

Source: OECDAverage replacement rates At age 66, across income deciles, 2012

Official retirement age

International comparison

68

67 67

67 66,6

66 66

66 65,5 65,5 65,6

65,0 65,0 65 65 65 65 65 65

65

64 63,8

62,9

63

62

61

60

Men Women

Source: OECD•Reforms…

Recent reforms

Postponing the retirement age

• Welfare reform (2006) and retirement reform

(2011)

• Discrete changes:

– Increasing the early retirement age from 60 to 62

years over the period 2014–17.

– Shortening the early retirement period from five

to three years over the years 2018–19 and 2022–

23.

– This implies an early retirement age of 64 in 2023,

and the pension age will increase from 65 to 67

years over the period 2019–22.Recent reforms

Postponing the retirement age

• Welfare reform (2006) and retirement reform

(2011)

• Longevity indexation scheme (“autopilot”):

– The early retirement age and the official pension

age are indexed to the development in life

expectancy at the age of 60.

– The aim is to target the expected pension period

to 14.5 years (17.5 including early retirement) in

the long run.

– Currently, these are about 18.5/23.5 years,

respectively.Recent reforms

Postponing the retirement age

• Welfare reform (2006) and retirement reform (2011)

• Key design characteristics:

– The system is semi-automatic: a change has to be

approved in parliament every fifth year.

– The changes are smoothened: the change in one year can

never be below 6 months and above 12 months.

– The changes are pre-announced with a lead of 15 years:

the first change will be implemented in year 2030 for

pension age (year 2027 for early retirement age).

– Specifically, in year 2015 it was agreed that the official

retirement age will be increased to 68 years in year

2030.Longevity adjustment of the retirement age

Different scenarios

Longevity atforage

Dansk periodelevetid 60

60-årige Retirement age

Folkepensionsalder for forskellige LC-modeller

85

LC 1975-2014 (median)

LC 1985-2014 (median)

LC 1995-2014 (median)

30

80

lifetime (in yeras)

Kvinder

Women

Folkepensionsalder

Retirement age

Restlevetid (år)

25

75

Remaining

Observed 70

Men Observeret

20

LC 1975-2014

LC 1985-2014

Mænd LC 1995-2014

65

2000 2020 2040 2060 2000 2020 2040 2060 2080 2100

YearÅr Year

År•Challenges…

The hammock problem…

•Mind the gap… •ETT or TTE

Old-Age Expenditures and Taxation of Pension

Savings (DKK, billion)

2015 2050 Difference

(a) Changes in age-related expenditures

Old-age pension expenditures 102,1 107,8

Old-age service provision 81,9 129,4

Total 184,0 237,2 53,2

(b) Revenues from taxation of pension savings

OP schemes: Pension benefits 63,9 134,7

Income tax revenue of pension benefits 25,5 53,9

Effect on VAT and other indirect taxes 9,4 19,8

Phasing-out of pension supplement 2,9 6,1

Total 37,8 79,8 42,0

Source: DREAM and own calculationsFrom ETT to TTE Taxation

Effects on Structural General Budget Balance

Pct. of GDP

4

3

2

1

0 BL

FC

-1

-2

-3

-4

-5

2010 2020 2030 2040 2050 2060 2070 2080

Baseline TTE fullFrom ETT to TTE Taxation

Effects on Structural General Budget Balance

Pct. of GDP

4 2016

3

2

1

0 BL

FC

-1

-2

-3

2020 2026

-4

-5

2010 2020 2030 2040 2050 2060 2070 2080

Baseline TTE full•OXIT?

Return to pension savings

Incentive problems due to means testing

DKK

160

140

120

100

80

60

40

20

0

Contribution 3 years before Contribution 5 years before Contribution 10 years before

retirement retirement retirement

Without means testing

With means testing

With means testing incl. housing benefitAlternative reform proposals

Tax rates and pension savings

Effect on real, effective tax rate on return to pension savings for persons with

incomes below EUR 47,300 (low-income group)

Real effective tax

rates

Years before retirement

Existing rules

Reform proposal (1)

Reform proposal (2)

Reform proposal (3)OXIT…

Projected time path of private pension funds

5000

4500

4000

3500

3000

2500

2000

1500

1000

500

0

2010 2020 2030 2040 2050 2060 2070 2080

Baseline Abolish OP schemesCrowding out of private saving? •A major study shows that only 15 percent of Danes respond actively to retirement savings policies •This documents why mandatory labour market pension schemes are effective at raising total saving. •Yet, things are changing…

Effects on public finances

Structural primary budget balance

Pct. of GDP

3

2

1

0

-1

-2

-3

-4

2010 2020 2030 2040 2050 2060 2070 2080

Baseline Abolish OP schemesEffects on the current account

Fiscal policy unsustainable

Pct. of GDP

6

4

2

0

-2

-4

-6

-8

2010 2020 2030 2040 2050 2060 2070 2080

Baseline Abolish OP schemesSustainability index • The permanent improvement of the primary budget (measured as a share of GDP) that is needed to guarantee that the government’s intertemporal budget constraint is satisfied. • Baseline: -0.07 • OXIT: -0.93 (app. 15 billion of DKK)

•DB to DC

Is there a future for DB schemes? •Major shift from DB to DC schemes –Low return environment –Increased longevity –More stringent solvency rules

Guaranteed average interest rate products Danish pension fund JØP Date of Admission Level of Guarantee Before 1st January 1990 3,70% or 4,25% 1st January - 31st December 1996 3,70% 1st January 1997 - 30st June 1999 3,00% 1st July 1999 - 1st July 2005 2,00% From 1st July 2005 0,00%

The life expectancy will increase

Life expectancy at 65 (men)

Years

Source: OECD“Society-assumptions”

Summing up • Denmark’s retirement income system comprises a public PAYG basic pension scheme, a means-tested supplementary pension benefit, a fully funded defined contribution scheme, and mandatory occupational schemes. • Denmark maintains #1 position for six consecutive years • Political consensus and a collaborative approach to working with key stakeholders are key to parts of the success. • This is unlike the UK, a more of an individualistic society compared to the inclusive cultures of Denmark, Finland and the Netherlands. • Indeed, the recent downgrade of the UK’s pensions system from a B+ to a B was explained by the government’s decision to introduce freedom and choice at and in retirement.

Summing up

• While the Danish pension system is “world-class”, it

isn’t perfect…

• Still a number of challenges, mainly related to the

OP schemes:

– Poverty trap and means-testing: effective returns

on retirement saving may be low and this may

(strongly) reduce the incentives to save for

retirement…

– Trade union density is falling - and “zeitgeist”

against collective, mandatory arrangements…

– Uncertainty about rule(s) of taxation…You can also read