Ruby Project Update Ed Miller Manager, Business Development - California Energy Commission

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

El Paso Western Pipelines

Ruby Project Update

Ed Miller

Manager, Business Development

a meaningful company

doing meaningful work California Energy Commission

delivering meaningful results

1

March 4, 2010

Cautionary Statement Regarding

Forward-looking Statements

This presentation includes forward-looking statements and projections, made in reliance

on the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. The

company has made every reasonable effort to ensure that the information and

assumptions on which these statements and projections are based are current,

reasonable, and complete. However, a variety of factors could cause actual results to

differ materially from the projections, anticipated results or other expectations expressed

in this presentation, including, without limitation, our ability to successfully contract, build

and operate the pipeline projects described in this presentation; changes in supply of

natural gas; general economic and weather conditions in geographic regions or markets

served by El Paso Corporation and its affiliates, or where operations of the company and

its affiliates are located; the uncertainties associated with governmental regulation;

competition, and other factors described in the company’s (and its affiliates’) Securities

and Exchange Commission filings. While the company makes these statements and

projections in good faith, neither the company nor its management can guarantee that

anticipated future results will be achieved. Reference must be made to those filings for

additional important factors that may affect actual results. The company assumes no

obligation to publicly update or revise any forward-looking statements made herein or

any other forward-looking statements made by the company, whether as a result of new

information, future events, or otherwise.

2Ruby Update

3El Paso Pipeline System

Colorado Tennessee

Interstate Gas Gas Pipeline

Wyoming

Ruby Pipeline Interstate

Mojave Cheyenne

Pipeline Plains Pipeline Southern

Natural Gas

El Paso Elba Island

Natural Gas LNG

Mexico Florida Gas

Ventures Transmission (50%)

• 19% of total U.S. interstate pipeline mileage

• 26 Bcf/d capacity (15% of total U.S.)

• 19 Bcf/d throughput (30% of gas delivered to U.S. consumers)

Note: Includes El Paso Corporation and El Paso Pipeline Partners, L.P. 4Horn River

Gas Supply and Pipelines

Basin

Serving the Northwestern US

WCS

B

C A N A D A

B R I T I S H

C O L U M B I A

W A S H I N G T O N

M O N T A N A

Powder River

O R E G O N

Basin

I D A H O

W Y O M I N G

Green River

Basin

Uinta

Basin

U T A H Piceance

N E V A D A Basin K A N S A S

C O L O R A D O

C A L I F .

5Ruby Pipeline Map

Big Horn

O R E G O N Powder River

I D A H O Basin

Basin

GTN

W Y O M I N G

NWPL Wind River

Green River

PG&E Basin

Basin

CIG

Tuscarora

Ruby Opal Hub

Denver

WIC Juelsburg

C A L I F .

Paiute

Cheyenne Cheyenne

U T A H

Uinta Plains

N E V A D A Basin

Piceance

Basin

Kern River

• 680 miles of 42-inch Opal to Malin

C O L O R A D O

• 1,440 psig MAOP

• Measurement—8 locations Raton

Basin

• Four delivery points

• Receipts from the major Rocky

Mountain producing basins

6Ruby Stats

• 1.098 Bcf/d of firm transportation service agreements with customers

• Letters of support from California, Colorado, Nevada, Utah and

Wyoming Governors

• Initial capacity will be 1.25 to 1.5 Bcf/d

– Final sizing will be based on market support

• Estimated cost $2.96 Billion

• Rates:

– Filed recourse rate of $1.02

– $0.95 less than 200 MDth/d; 10-year contract term

– $0.87; 20-year contract term

– $0.85; 30-year contract term

• Begin service in March 2011

7Ruby: The First Carbon Neutral Pipeline

• Collaborative effort between Project Developer and Shippers

• Compressors to be powered by both gas and electricity

• Purchase renewable power (e-tags) to run e-motors

• Internal coating of the pipeline

• Apply Best (methane) Management Practices (BMPs)

• Leadership in Energy and Environmental Design (LEED)

• Reforestation along Ruby route and other locations

• Purchase Voluntary Emissions Reduction (VER) credits

• On-going GHG mitigation costs recovered as part of tariff fuel charge

8Ruby Pipeline Milestones

CPUC Approves PG&E Contract November 2008

Draft EIS June 2009

Partnership with GIP Announced July 2009

Preliminary Determination September 2009

Final EIS January 2010

FERC Certificate March 2010

BLM Record of Decision April 2010

Start Construction May 2010

In-Service March 1, 2011

FERC Certificate Docket No. CP09-54

Website: www.rubypipeline.com

9Ruby Pipeline – A Reality

Here’s why:

• Strong, firm contractual support from credit worthy shippers

• Final environmental impact statement obtained

• Remaining permits due shortly

• Solid financing

– 50% partner with Global Infrastructure Partners

– $1.5 Billion of commitments for Ruby project financing

10Summary of Construction Progress To Date

• Pipe and compression equipment purchased

• High quality Pipeline contractor teams under

contract

– US Pipeline, Precision Pipeline, Associated

and Rockford Corporation

• 87% of ROW acquired

• Aggressive public and NGO outreach

11Gas Available From North is Diminishing

Volume Change 2007-2017 (Bcf/d)

Alaska / Mackenzie Delta

????

Western Canada Price arbitrage LNG into

Production ~2.0 Canada

Demand ~1.5 Imports ~0.5

Eastern Canada

Heavy oil sands

Production ~ 0.0

Demand ~ 0.5

LNG out of

Retirement of

Canada Ontario coal fleet

???

Net Imports into U.S. ª 3.5 Bcf/d

12Rockies versus Western Canada

Long-Term Production Trends

Bcf/d

20

18

Canadian Forecast Rockies Forecast

16

14

12

10

8

6

4

163 Tcf Other

2 Forecast

-

1970 1980 1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090

Source: El Paso, NEB 13Rocky Mountain Production

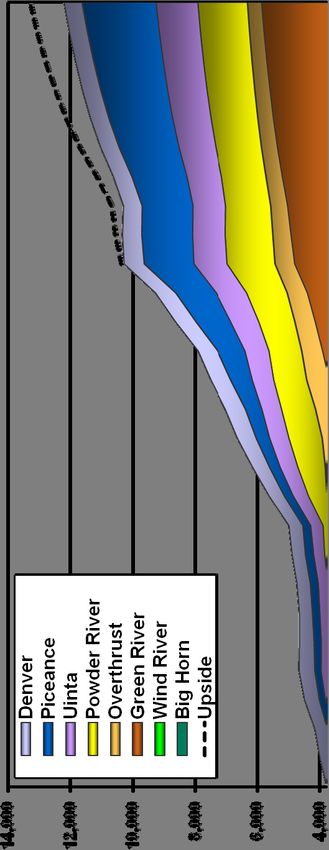

(Volumes are Wellhead – Measured in MMcfd)

Forecast

2.1 Bcf/d of

growth 2008-2017

Forecast by 2017:

High Case 13,274

Mid Case 12,185

Low Case 11,096

1990-2007: Wellhead total data from IHS database

2008-2017: El Paso forecast

14Ruby Pipeline

• Concluding thoughts

¾ Ruby Pipeline will be in-service in early 2011

¾ History has taught us that it is very difficult to

predict the cost and availability of natural gas

¾ Predicating a future gas supply plan on a

developing resource is risky

¾ Ruby Pipeline provides the Western Markets

with the only firm, incremental access to Rocky

Mountain Production and supply diversification

15You can also read