Rethinking Your Small Business Growth Strategy? Tips and Tools for Embracing Change - Fiserv

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Rethinking Your Small Business Growth Strategy? Tips and Tools for Embracing Change Navigating the Journey in Warp Speed Digital Space May 18, 2021 – Charlton Laird, Senior Strategist Did your financial institution effectively support the needs of your small business clients during the pandemic and are you prepared to meet future expectations with your strategy? Quoting Captain Kirk from Star Trek, “To boldly go where no one has gone before,” financial institutions are continuing with their core mission to grow and develop new and existing business relationships, but are doing so in a universe that has been upended into a digitally-integrated future. Small business owners and operators quickly pivoted to available digital options to survive during the pandemic and forever changed business operations and customer connections. According to a recent Raddon Research Insights survey, approximately two out of five small businesses with up to $10 million in annual sales applied for and were approved for some amount of Payment Protection Program (PPP) funding in 2020. And three out of four small businesses applying for PPP relied on their primary financial institution to acquire this funding. 1 © 2021 Fiserv, Inc. or its affiliates. | FISERV PUBLIC

Financial Institution Used for PPP Loan Source: Raddon Research Insights So far in 2021, according to the ABA Data Bank, small businesses have shown continued demand for funding in the third round of the PPP. The clear opportunity remains that small businesses are overwhelmingly looking first to their primary financial institution to deliver financial solutions and support, not only for their immediate needs, but also for their long-term success. With new investments in integrated digital transactions, treasury management, loan origination and client management, these commercial tools are being prioritized to make processes easier both for the financial institution and the small business. As you look back on lessons learned in 2020 to develop and execute your strategies for 2021 and beyond, has your leadership team embraced the changing frontier? Consider the following tips and tools: Follow a Tactical Roadmap Like retail consumers, small business owners are looking to their financial institution to make banking easier. They want an Amazon-like experience and anytime access to accounts to bank where they want, when they want using a mobile device. Small business owners want to be empowered to apply and get approved for a loan or open a new account without the hassle of a face-to-face meeting for every request – and many financial institutions are already delivering. 2 © 2021 Fiserv, Inc. or its affiliates. | FISERV PUBLIC

Source: Fiserv Digital Ecosystem Advantage Regional and community financial Institutions need to be mindful that digital solutions for small business banking and treasury management are typical offerings from larger financial institution competitors. While trying to keep pace with the latest and the greatest, and associated costs, for digital innovation seems daunting, having a tactical roadmap provides a framework and pace for your digitization and automation strategy that will safeguard you from losing out to the larger competitors. Along with directing its small businesses to utilize digital channels for banking and communication, financial institutions must adapt how they connect with small business owners to manage and grow relationships. Establish Dedicated Relationship Managers According to the J.D. Power 2020 U.S. Small Business Banking Satisfaction Study, small business banking customer satisfaction is significantly higher when a dedicated relationship manager is assigned. The aphorism that “Relationships Matter” has proven to be a competitive differentiator for financial institutions with small businesses in the wake of the pandemic. From an analysis of PPP data by the Federal Reserve Bank of New York, businesses that already had a lending relationship with a financial institution were more likely to obtain a PPP loan from that financial institution. 3 © 2021 Fiserv, Inc. or its affiliates. | FISERV PUBLIC

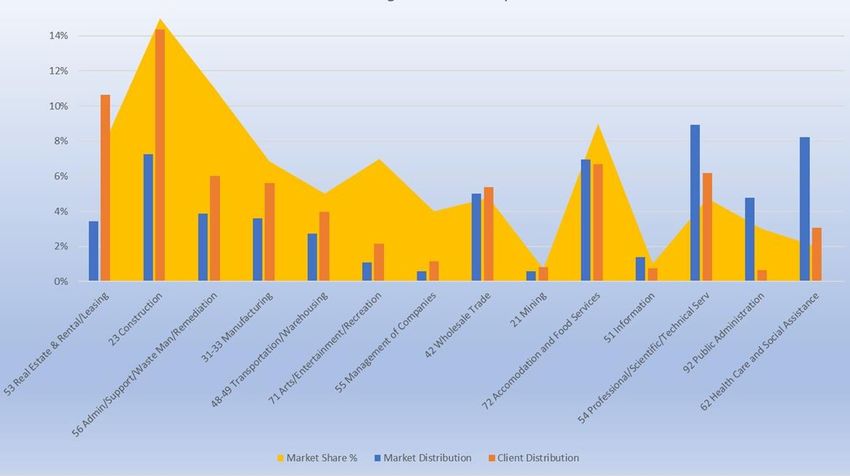

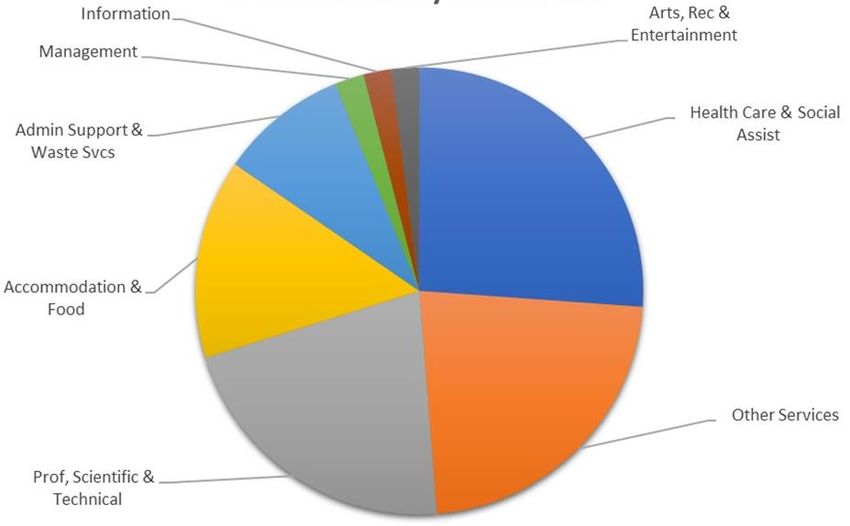

Leverage a CRM Solution Financial institutions that have relied primarily on their employees to handhold and manage the profitable business relationships should consider solutions that aggregate data and optimize their valuable business development resources. Leveraging a customer relationship management (CRM) solution can provide the financial institution the ability to use all its various stakeholder resources to help anticipate and solve small business needs and provide added value to every interaction. Without losing the personalized human-to human interaction that has been the foundation of small business relationships and with a 360-degree view of the small business, financial institutions can be proactive and present valuable financial solutions targeted directly to the anticipated need at the right time. Engage a Data-Driven Market Strategy As crucial as it is for financial institutions to advance their relationship and engagement strategies with existing small business relationships, it is also just as imperative to realize an understanding of your small business market, the size and industry mix, growth opportunities and local competitive makeup, as well as recognize the internal value your financial institution can provide the local small businesses owner. Service Industry Market Mix Source: Bank Intelligence Solutions Source: Bank Intelligence Solutions 4 © 2021 Fiserv, Inc. or its affiliates. | FISERV PUBLIC

Using market and industry data analytics tools enable financial institutions to evaluate local market opportunity, prioritize business development and growth tactics in their markets, and identify business industries that have better acquisition opportunity. Employing a data-driven market strategy for new business acquisition and growth will improve efficiency and allow the financial institution to allocate limited resources effectively. NAICS Segmentation Analysis Source: Bank Intelligence Solutions Whatever stage your financial institution is at with your small business strategy, it is important to recognize the velocity at which the pandemic has shifted the behavior of small businesses toward digital engagement. Financial institutions are also being held to a higher standard for products and services offered to small businesses. Identifying the technology resources necessary to help develop and support your digital space roadmap for long term growth and sustainability will keep your institution from being outperformed (or inhaling space dust) by your competitors for the small business opportunities in your markets. Set course and engage. Contact us for more information. 5 © 2021 Fiserv, Inc. or its affiliates. | FISERV PUBLIC

You can also read