INTEREST RATE UPDATE - Associated Bank

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INTEREST RATE UPDATE

Capital Markets Department

Chicago | Milwaukee | Green Bay

866-524-8836

August 11, 2021

Thomas Toerpe A TURNING POINT FOR INTEREST RATES?

Economic data have been pointing to strong and durable growth. The July jobs report was a winner

across the board, with 943,000 net new jobs created, upward revision in the June jobs tally, a drop in the

unemployment rate from 5.9% to 5.4%, and steady labor force participation. Despite auto industry

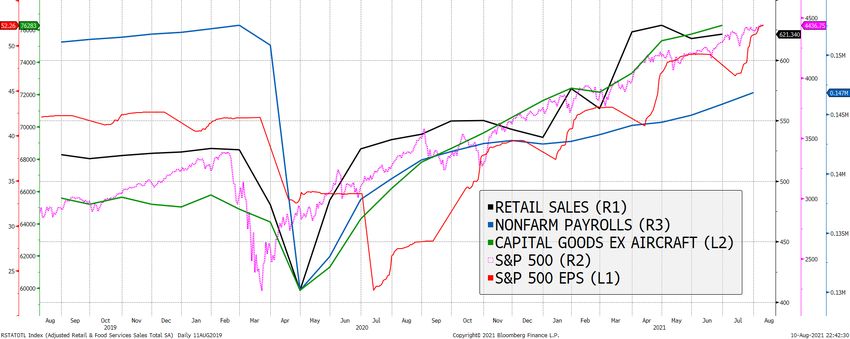

bottlenecks and difficulty finding workers in the hospitality/leisure sector, June retail sales topped $621

billion, down only slightly from the record $629 billion in April. Capital goods shipments (excluding defense

and aircraft) surged to a record $74 billion in June, and new orders continued to pour in as well, reaching $76

billion. July month-over-month inflation moderated to 0.5% from June’s torrid 0.9% pace. Corporate profits

also have hit records, with earnings per share up 91% from last year, and 22% higher than the same period

in 2019 pre-pandemic. Not surprisingly, the S&P 500 stock index continued to reach new highs as a result.

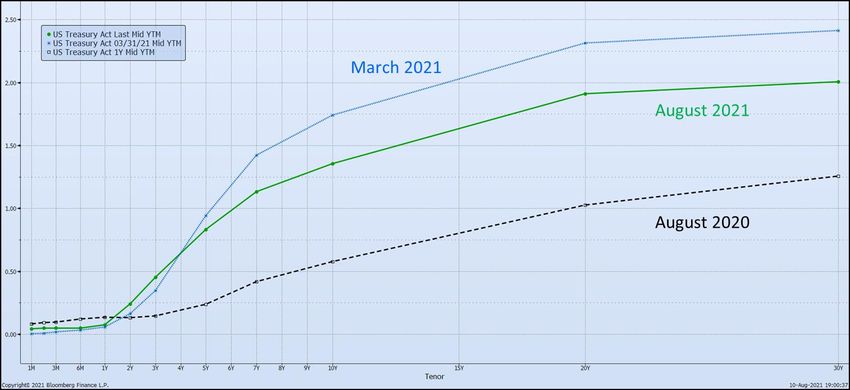

U.S. Treasury yields, surprisingly, have been moving in the opposite direction since March, typically a

sign of a weakening economy. The ten-year yield, which reached a post-pandemic high of 1.74% in spring,

has dropped steadily since then, briefly touching 1.14% at the beginning of August. Despite a 20-basis point

rebound in the past week, interest rates remain well below the 2021 peak, and are more than 100 basis

points lower than they were in 2018. Several factors account for the unexpected downdraft:

• Demand for liquidity: Savings rates for both households and businesses surged at the height of the

pandemic and have only moved up since then. With cash continuing to flood the system, much of it is

finding its way into the world’s most popular savings instrument, U.S. Treasury securities.

• A patient Federal Reserve: The U.S. central bank continues to purchase $120 billion per month in

Treasury bonds and mortgage-backed securities, supplementing private demand. Fed Chair Jay

Powell hasn’t been in a hurry to begin tapering these purchases despite “transitory” inflation

pressures, though monetary policymakers are starting to discuss how and when to do so. With overall

unemployment still above 5%, unemployment for African Americans even higher at 8.2%, and

employment of women still four million below its pre-pandemic level, the Fed remains well short of its

statutory goal of full employment.

• Renewed concerns over COVID-19: With hospitalizations for the highly transmissible delta variant

rising to worrisome levels across the U.S. and globally, many jurisdictions are reinstating masking,

shut-downs and work-from-home protocols to protect their populations. As a result, global investors

are using the U.S. Treasury market as a safe haven, helping to tamp yields down despite the solid US

economic recovery.

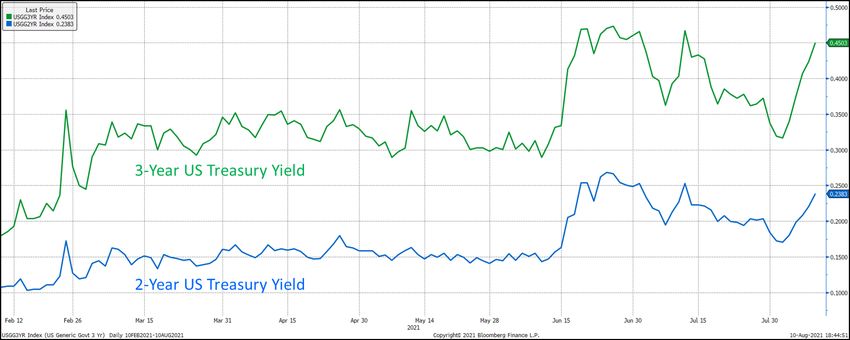

But the 10-year yield’s 20 bp rebound this week suggests we may have reached a turning point; two-

and three-year yields are up as well, approaching their highest levels of the year. The upward move at

the short end of the curve, along with signals from the futures markets, implies the Fed will start hiking short-

term rates in the fourth quarter of 2022. In addition, market participants will pay close attention to news out of

the Fed’s August 26–28 annual conference in Jackson Hole, Wyoming, along with the September 21–22

FOMC meeting, for clearer guidance on when the central bank will begin tapering its bond purchases. With

continued growth in jobs and the economy, elevated inflation readings and increased willingness of Fed

officials to come out in favor of tapering and rate hikes, we can expect to see upward pressure on rates

across the yield curve as we approach the end of 2021.

Capital Markets Department

Chicago | Milwaukee | Green Bay

866-524-8836

Key Statistics: Interest Rates, Unemployment and Inflation

Year-end Year-end Year-end Year-End August 11,

2017 2018 2019 2020 2021

10 yr Treasury yield 2.41% 2.68% 1.91% 0.91% 1.35%

2 yr Treasury yield 1.88% 2.49% 1.57% 0.12% 0.24%

Spread 0.53% 0.19% 0.34% 0.79% 1.11%

Fed Funds Target 1.375% 2.375% 1.625% 0.125% 0.125%

(mid)

1m LIBOR 1.56% 2.50% 1.76% 0.14% 0.10%

SOFR30 NA 3.00% 1.55% 0.07% 0.05%

CPI (y/y change) 2.2% 2.2% 2.1% 1.4% 5.4%

Core PCE (monthly) 1.50% 1.50% 1.59% 1.38% 3.5%

5Y TIPS (market 1.88% 1.49% 1.70% 1.97% 2.58%

breakeven)

U-3 Unemployment 4.1% 3.9% 3.5% 6.7% 5.4%

Real avg weekly 1.2% 1.4% 0.1% 5.3% -0.6%

earnings

Annual change in

2,188,000 2,513,000 2,090,000 -9,380,000 +7,255,000

NFP jobs

U.S. TREASURY CURVE

Source: Bloomberg LP

Capital Markets Department

Chicago | Milwaukee | Green Bay

866-524-8836

ECONOMIC DATA, S&P 500 AND CORPORATE EARNINGS

ARE ALL SIGNALING A STRONG RECOVERY

Source: Bloomberg LP

MEANWHILE, 10-YEAR U.S. TREASURY YIELDS HAVE BEEN MOVING IN A CONTRARY DIRECTION

OVER THE LAST 6 MONTHS

Source: Bloomberg LPCapital Markets Department

Chicago | Milwaukee | Green Bay

866-524-8836

FRONT END OF YIELD CURVE NEARS 2021 HIGH

Data on interest rates, currencies, forecasts and economic indicators were obtained from Bloomberg, LP and the Federal Reserve Bank of St. Louis’s

FRED database.

Associated Bank offers a wide range of instruments for hedging interest rate, commodity and foreign

currency risk, including foreign exchange in more than 75 currencies. Companies interested in

learning more about these instruments should contact their Associated Bank Relationship Banker or

the bank’s Capital Markets Department at 866-524-8836.

All rates shown are indications only and subject to change.

This material is provided to you for informational purposes only; and any use for other than informational purposes is disclaimed. It is a summary and does not purport to

set forth all applicable terms or issues. It is not intended as an offer or solicitation for the purchase or sale of any financial product and is not a commitment by Associated

Banc-Corp, its subsidiaries or affiliates, as to the availability of any such product at any time. The information herein is not intended to constitute legal, tax, accounting, or

investment advice, and you should consult your own advisors as to such matters and the suitability of any transaction. We make no representations as to such matters or

any other effects of any transaction. In no event shall we be liable for any use of, for any decision made or action taken in reliance upon, or for any inaccuracies or errors in,

or omissions from, the information herein. The views expressed here are solely those of the author and do not reflect the views of Associated Banc-Corp, its subsidiaries or

affiliates.

Associated Bank, N.A. Member FDIC. (7/21) P04612You can also read