Climate risks & Net Zero - FIRM March 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Climate risks & Net Zero FIRM March 2021

PwC has been actively shaping the ESG agenda and

contributing with thought leadership and market-leading tools

We are actively involved in standard setting (orange letters indicate PwC involvement) We help orchestrating the regulatory agenda and support clients globally

Umbrella reporting frameworks Detailed standards Umbrella enablers

UK: FCA is consulting on corporate Germany: BaFin published guidance

Global reporting initiative (GRI)

Environment (E): • Accounting for Sustainability disclosure of climate risks and in December 2019 on how FS firms

CDSB, CDP, TCFD, Natural • Corporate Reporting Dialogue is focusing on ‘greenwashing’; should manage sustainability risks

Capital Protocol, Greenhouse

gas protocol, Science Based

• EFRAG BoE plans to introduce climate

Integrated Reporting Council (IRC) stress tests

Targets • European Commission Hong Kong: Securities & Futures

Social (S): • Focus capital for the long term Commission announced Strategic

IASB – MD&A project • Impact Measurement Project Framework for Green Finance in 2018

International organisation for EU: EBA Sustainable Finance

standardisation (ISO26000), • NGFS (contributions) Action Plan; EU taxonomies,

Sustainability Accounting Standards Board UN guiding principles framework • The Capitals Coalition ECB Guide on management of Singapore: MAS exploratory work to

UN Global Compact Communication Governance (G): • UN Sust. Development Goals climate risks; various reporting incorporate climate-related stress

COSO Framework • UNEP FI and disclosure requirements scenarios

• Value Balancing Alliance

WEF International Business Compact • World Business Council for

Sustainable Development

We have developed market-leading tools

PwC's “Climate Excellence” tool for climate scenario

analysis supports investors and companies in getting

We shape global ESG discussions through Thought Leadership their portfolios ready for the risks and opportunities of

climate change.

Our recent publications/projects include In this way, the potential for value enhancement, adequate

risk management and communication with regulators and

• Advice and review: UNEP FI PSI work on climate risks in insurance

stakeholders can be fully exploited.

• The growth opportunity of a century - onset of a paradigm shift in investment Market Recognition:

• Network for Greening the Financial System (NGFS)

• Sustainable Finance for Asset Managers – a revision to the non-financial • UNEP FI TCFD Pilot at insurers

reporting and regulatory requirements based on the EU Green Deal • TCFD Knowledge Hub

• UN PRI

• “Privatkundenstudie Sustainable Finance” – detailed survey of private customer

• Standard and Poor’s

expectations on ESG offerings and preferences, and growth opportunities

• Kepler Chevreux

• Pathways to Paris (in collaboration with WWF): develop transformation tools for • Green and Sustainable Finance Cluster Germany

sectoral decarbonization in Germany and connect real economy with financial

sector in Germany

Climate Risks & Net Zero March 2021

PwC 2

Agenda

1. Why climate?

2. Climate risks and Net Zero – what does it mean?

3. Spotlight on climate risk

4. Spotlight on Net Zero

5. What does it mean for the risk function?

March 2021

PwC 3

Why climate?

March 2021

PwC 4

Even if we are limiting global warming, we will see tangible

changes in our world

Legend

Source: IPCC (2019) SR15 Summary for Policymakers, https://www.ipcc.ch/site/assets/uploads/sites/2/2019/05/SR15_SPM_version_report_LR.pdf

Climate Risks & Net Zero March 2021

PwC 5

Awareness is increasing that we will be facing

climate risks, no matter what we do

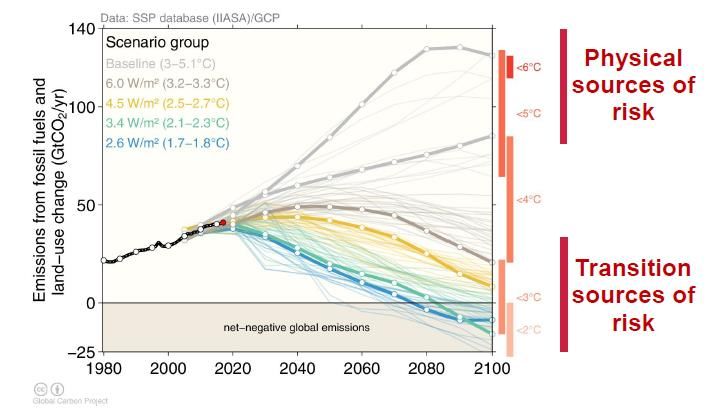

More Physical Risks

01 If we do not contain climate change,

physical risks will materialize.

Floods and Extreme weather

Drought higher sea level Heat events Wind

More Transition Risks

If we embark on a transition path, transition

02 risks will materialize. An orderly transition

is preferred over an abrupt and disorderly

transition.

Technological Climate law and regulation Market

Source: Global Carbon Project innovation

Climate Risks & Net Zero March 2021

PwC 6

Net Zero is a pressing issue for society

GOAL to make 1.5C possible:

-> Net zero carbon emissions before

Transition Pathways:

2050, 50% reduction by 2030.

PwC’s Low Carbon Economy Index 2019

The Net Zero tidal wave (since 2019):

- >120 countries commit to net zero

by 2050,

- >450 net zero cities

- Ca. 300 net zero global

businesses (“Race to Zero”)

- WEF and WBCSD membership

requirement 1-2yrs

- Investors controlling $45Tr AUM

commit to net zero by 2050

> quarter of global CO2 emissions and

more than half of the global economy

covered by net-zero commitments

Climate Risks & Net Zero March 2021

PwC 7

The finance sector is impacted by three significant climate-

related changes

ESG assets perform better The market commits to disclosing The market commits to net zero

climate risks and opportunities decarbonization

ESG leaders’ equity performed better during the Corona Climate risks and opportunities have become part of the Market participants are increasingly committing to

crisis compared to ESG laggards: market and regulatory conversation. decarbonize their portfolios to net zero emissions.

>1500 signatories

>$12 trillion market 30 signatories

capitalization >$9 trillion AuM

Source: TCFD Signatories website (December 2020)

Source: Net Zero Asset Manaegers Initiative Website (December 2020)

33 signatories

>$5 trillion AuM

>3000 signatories

>$103 trillion AuM Source: UNEP FI Website (December 2020)

Source: PRI Signatories website (December 2020)

>60 Financials taking action

Source: AXA (2020) Coronavirus: How ESG scores signaled

resilience in the Q1 market downturn, retrieved here. Source: SBTi Website (December 2020)

If we don’t act …

… we will lose market share, … … we will not fulfill investee expectations, … … we will not fulfill our commitments.

Climate Risks & Net Zero March 2021

PwC 8

Case example: Climate risk heat maps focus attention

MSCI world analysis

Example: Portfolio

Unweighted 1.8°C Scenario

The MSCI World could risk losing 5% in profitability if Benefits

companies weren’t acting

MAINSTREAM: 2019 - 2030 • Understanding financial

materiality of climate risks

Percentage annual change of EBITDA

: in portfolios and focusing

the attention going forward

as heatmaps highlight

Total MSCI World material sectors and

Mining geographies

-1.41%

cumulated growth (2019-2030):

+ 3.4% in Mainstream • Identification of potential for

Utilities reweighting

+3.86% - 4.9% in Inaction

• Key input into reporting

EBITDA CHANGE as compound annual growth

rate (CAGR) compared to previous period

- 1% +1%

Climate Risks & Net Zero Negative financial Positive financial March 2021

impact of scenario impact of scenario

PwC 9

Stakeholders are taking a harder look at climate

US Asia Europe

Climate Risks & Net Zero March 2021

PwC 10Climate risks and Net Zero –

what does it mean?

March 2021

PwC 11TCFD as SBT can conceptually interlock seamlessly with a

shared scenario basis: IEA below 2°C 1

Task Force on Climate-Related Financial Disclosures Science-Based Targets Initiative (SBTi)

EUR CO2/t

Taxonomy

4°C

Paper Sector Curve

2°C (based on 2° IEA 1)Extract Absolute Impact: Net zero does not equal no risk

Can a CO2 footprint be a good indicator for risks and opportunities?

Comments

• Portfolio choice:

• Two test portfolios were built based on Europe’s top 20

utilities companies

• Test portfolio A chose those 3 out of those 20 companies

that showed the highest climate resilience in both

scenarios and with and without strategic adaptation

assumption (highest EBITDA change)

• Test portfolio B chose those 3 out of the 20 companies

that had the lowest CO2 footprint

• Result: A is a lot more resilient, while growth could be similar

in the best case for both, B could experience -0,9% EBITDA

change p.a. – average change in A lies at +0,8% p.a. and at

+0,2% for B

• Rationale: companies in A show a diversified technology

Best, average and worst annual earnings performance (EBITDA)

portfolio and are globally diversified. Companies in B are

of the two test portfolios A and B over the period 2020 to 2050 rather focusing on Europe and mostly have RE, nuclear in their

based on a 1.8°C and a 2.7°C climate scenario respectively with mix.

and without strategic adaptation of the companies.

Source: AbsolutIimpact, Climate Excellence: Bewertung von Klimarisiken und –chancen, Ausgabe 04/2020

Climate Risks & Net Zero March 2021

PwC 13Spotlight on climate risk

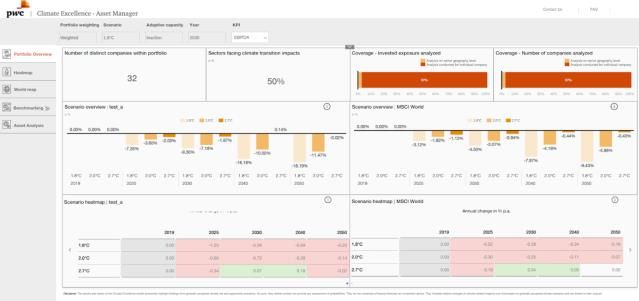

Minimal input from your side and maximum output provided

via the Climate Excellence tool

Input of Your Company Output: Financial

• NACE codes impact per scenario

• ISIN (if listed)

• Company

• Country of operation/geography (ideally not only headquarters)

• Exposure EBITDA

1.8°C

• If possible: revenue breakdown of companies by NACE codes

Climate

2.0°C Sales

Excellence

Input Climate Excellence Model 2.7°C

• Scenario data

• Asset level data

• Validation emission-data

Climate Risks & Net Zero March 2021

PwC 15Climate risks are not a separate risk category but have an

impact on credit, market and operational risks

Credit Risk Market Risk Operational Risk

Physical • Revaluation of credit objects and • Rating downgrades and Exchange rate • Physical losses burden balance sheet;

Risks collateral losses after catastrophes and by impairment the availability of banking

• Rating downgrades creeping sinking productivity services

Transition • Stranded assets • Sudden extreme fluctuations in asset • Image damage due to failure to switch

Risks • Risk shifts prices; stranded assets to sustainable business practices

• Effects on Probability of default (PD) • Long-term price increases due to

and losses in the event of default (LGD) environmental and social changes

Financial • Affectedness of entire industries and • Market-threatening effects of climate • Reputation damage for entire industries/

Stability markets and environmental damage in an entire entire markets

Risks • Economy is no longer insurable at region • Large parts of the financial infrastructure

reasonable cost of a Country/Region

Source: BaFin Perspektiven Ausgabe 2|2019, pg. 23

Climate Risks & Net Zero March 2021

PwC 16The tools guides you through the relevant aspects and delivers

answers for your specific portfolio Transition risk

PF Overview Regional Heatmap Single Asset Benchmark

Identify exposures, portfolio Compare sector performances Illustrate differences in Allows separation of winners and Compare risk drivers for a single

resilience and potentials for of companies performance across countries losers company and analyze company

reshifting in the same segment. within the same sector differentiators.

Company Benchmark Regional Performance Single Asset Risk driver

Climate Risks & Net Zero March 2021

PwC 17Spotlight on Net Zero

March 2021

PwC 18Reaching Net Zero: Different frameworks for target setting

exist

Three target options* for

mandatory Asset Classes: Further approaches:

1) Sector Decarbonization Approach

Potential Net Zero pathway: Four target options

Target for the reduction of the emission

(3 mandatory):

in Billion tonnes CO2 per year (GtCO2/yr)

intensity of individual sectors present

in the portfolio

40

• Absolute emissions target for

(sub)portfolio

2) Portfolio Coverage

20 • Sector intensity targets

Target for the share of portfolio • Engagement targets

companies that set themselves a • Financing Transition targets

0

SBT

-20 3) Portfolio Temperature Rating

2020

2020 2060

2060 2100 2100

Fossil fuel and industry AFOLU Target for the overall temperature

rating (contribution to global warming)

of the entire portfolio

Climate Risks & Net Zero Sources: IPCC SR1.5; SBTi – Financial sector science-based targets guidance, October 2020; *Real Estate and Project Finance has to be calculated using the SDA March 2021

PwC The Unconvened Net-Zero Asset Owners Alliance 2025 Target Setting Protocol; January 2021 19How to use the SBTi to set science-based targets

What does this mean for the different parts of your business?

SBTi method

The table shows the SBTi

Estimated SBTi Sector Decarbonisation SBT Portfolio Temperature

approach mapped to your €bn

emissions Coverage Approach Coverage Rating

business.

Residential Mortgages Optional ✔ ⨯ ⨯

Where an activity is out of scope Property & Construction / Commercial Real Estate > 67% actual ✔ ⨯ ⨯

for SBTi, such as car finance, Electricity generation 100% actual ✔ ⨯ ⨯

Project

targets can still be developed and Finance Other n/a ⨯ ⨯ ⨯

set using an appropriate method,

Electricity generation 100% actual ✔ ⨯ ⨯

and would provide you with an

Fossil fuel** > 95% $ ⨯ ✔ ⨯

opportunity to show leadership by

working with the SBTi to pioneer Corporate ✔

Mining and quarrying > 67% $ ✔ ✔

a new methodology. & SME* (iron and steel only)

lending

Transport, aluminium, cement, pulp and paper,

> 67% $ ✔ ✔ ✔

The SBTi are looking to broaden buildings

the framework over the coming Other commercial*** > 67% $ ⨯ ✔ ✔

years, with infrastructure and

asset finance being considered Common and preferred stock, corporate bonds,

Listed exchange traded funds, REITs****, listed real 100% $ ✔ ✔ ✔

for the next twelve months. equity and estate companies, real estate mutual funds

bonds

For your own operations, Funds of funds Optional ✔ ✔ ✔

financial institutions are Private equity and debt, including venture capital Optional ✔ ✔ ✔

encouraged to set targets for * SME lending is optional

scope 1 & 2 emissions. ** Includes Oil & Gas and Coal. SDA approach for oil and gas currently in development

*** Other sectors include all service sectors, tech and education, wholesale, agriculture, manufacturing, and retail and hospitality

**** REITs: If the FI in question is a REIT, 67% of mortgages need to be covered. If the FI in question is investing in REITs, this investment is considered a listed equity, and 100% of

Climate Risks & Net Zero

mortgages need to be covered. March 2021

PwC 20Case example: Achieving net zero requires target setting and

active steering

Example: Portfolio

Energy Relevant questions that need addressing:

Benefits

0,60 1. Where are companies I am investing in situated

0,55 relative to the trajectory? • Credible communication

0,50

2. Comparing titles I hold and sell over time, what are of integrated steering

0,45

0,40 relevant assumptions I need to consider? mechanisms

tCO2 / MWh

0,35 3. In planning decarbonization of my portfolios what • Initial assessment of

0,30

KPIs do I need to consider in the future? financing universe

0,25

0,20

4. How much decarbonization can I expect to • Setting up a future-proof

0,15 achieve in my portfolios through my holdings’ own steering mechanism by

0,10 decarbonization? understanding

0,05

0,00

5. What are implications on my product portfolio? decarbonization needs in

2020 2025 2030 2035 2040 6. Is the investment universe large enough to explore different sectors

Reduction curve from the IEA B2DS Scenario

such a decarbonization journey? • Set decarbonization

Possible portfolio

Illustrative portfolio reduction curve starting points targets and collaborate

with clients to achieve them

Sector decarbonization curves can be built: Existing Asset Holdings Asset Additions

• For different ambition levels (different scenarios)

• For different scenario sources Steering options: Steering options:

• For a number of different sectors • Engagement with issuers • Choose issuers, who are already aligned

• With regional granularity where scenarios provide it • Re-weighting • Choose companies and sectors, who are easy to align

• Based on physical or economic intensities

• Last resort: sell or have credible commitments

• Policies and thresholds

Climate Risks & Net Zero March 2021

PwC 21A steering logic must take into account the development of the

existing portfolio and requirements for new business

Illustrative: Real Estate

Reduction in primary energy demand from the climate scenario for Germany (for comparison).

Calculated reduction of primary energy demand (kWh/m²) according to IEA ETP 2017 B2DS

1 RISK Focus on heat pumps and

Primary energy (kWh/m²) (1 = 100%)

natural gas

Lock-in for new buildings to be considered

Vulnerability

Wie stehe ich of today’s portfolio

da?

Focus on solar heat and heat pumps

→ Necessary to reduce energy

~- consumption through renovation

80%

Paris-Agreement

(Well-below 2°C)

3 SUPPORT

TRANSITION The majority of buildings are

renovated and use efficient,

renewable heat

How can I support the transition?

Long-term minimum standard?

Nearly Zero Energy Buildings (NZEB)

2 STEERING

Combining extreme building efficiency

with renewable heating.

Portfolio starting point „to be aligned“

Source: IEA ETP and Energy Efficiency Strategy Buildings BMWi

Climate Risks & Net Zero March 2021

PwC 22What does it mean for the risk function?

The ambition level defines the way forward for risk integration

Do I want to decarbonize my portfolios as well? Need to integrate on both sides and

ensure consistency of approaches.

What is my decarbonization ambition?

How many scenarios do I want to analyze?

Qualitative/quantitative integration

Start with most material sectors

Climate Risks & Net Zero March 2021

PwC 24Different key pathways for risk integration exist

Metrics for Net Zero need to be

integrated as well and depend on

method decision

Model integration Factor model Qualitative integration

• Quantitative results integration into • Determination of risk drivers across • Qualitative integration into current

current assumptions and existing scenarios assumptions and considerations

models • Define a sector and company

characteristic-specific weighting

• Approximation in the risk model

Selection criteria:

• Ambition level

• Simplicity in implementation

• Transaction and data costs under construction

• Integration capability into the overall control system

Climate Risks & Net Zero March 2021

PwC 25Today’s production portfolio and strategy separates winners from losers

in a 2°C climate scenario

EBITDA developments from steel production up to 2050 in relation to 2016 status

Comment

150% 150% 150%

144%

• ArcelorMittal is transitioning to a

140% 140% 140%

133% regionally and technologically diverse

130% 130% 130% (BOF, EAF & DRI) asset base that makes it

119% resilient to climate change scenarios

120% 120% 120%

113%

110% 110% 110% • thyssenkrupp’s earnings from its steel

100% 100% 99% 100%

100% 100% 100% division could fall until 2030E, due to a

EBITDA [100% in 2016]

EBITDA [100% in 2016]

EBITDA [100% in 2016]

93%

89% lack of regional and technological diversity.

90% 90% 90%

Economic use of CCS technology (w/o

80% 80% 80% hydrogen) only in a time window from 2030

70% 70% 70% 68% to 2040

64%

60% 60% 60% • voestalpine’s earnings could rise by 33%

50% 50% 50% to 2050 as a result of a long-term BOF

40% 40% 40%

divestment strategy, towards DRI-based

steel production (ACT) and can turn highly

30% 30% 30% profitable for voestalpine

20% 20% 20%

10% 10% 10%

0% 0% 0%

2016 2020 2030 2050 2016 2020 2030 2050 2016 2020 2030 2050

S. AMERICA + S. AFRICA N. AMERICA EUROPE GERMANY UNITED STATES AUSTRIA

Source: Kepler Cheuvreux, The CO-Firm. The CO-Firm’s team and tool are now part of PwC

EAF DRI BOF

Climate Risks & Net Zero March 2021

PwC 26Your contact person

Dr. Nicole Röttmer

Climate Leader PwC

Deutschland

Partner, Hamburg

+49 151 40803712

nicole.roettmer@pwc.com

Climate Risks & Net Zero March 2021

PwC 27Develop a future-proof climate strategy with us! Thank you.

Coverage in the licensed tool version will include…

ALL sectors (NACE up to 4th digit)

Open for all scenarios

A - Agriculture, Forestry K – Financial and All business-related scenarios can be analyzed.

E - Construction

And Fishing Insurance activities Focus right now lies on (Integrated) Energy

Sectors

System Models

B - Mining and Quarrying C - Manufacturing L – Real Estate Activties • 1.8°C based on IEA ETP B2DS

• 2.0°C based on IEA ETP 2DS

D - Electricity H – Transport and Storage All remaining NACE* • 2.7°C based on IEA ETP RTS

Financial

Assets Listed corporate bonds, listed equity

Coverage

Companies More than ~70,000 companies; beyond that covering unlisted companies

based on sectoral split

Physical

Assets > 230,000 physical assets

e.g. power plants (wind, solar farms), oil

fields, automotive production lines

Adaptation

measures >135 unique technical adaptation measure packages across sectors per industry

Countries Global Coverage with more than 50 countries in depth

*Our primary analysis is performed based on NAICS classification, as it provides

more granularity for the analysis. We provide a mapping for NAICS to NACE.

Climate Risks & Net Zero March 2021

PwC 29You can also read