Walter Teng DIGITAL ASSET STRATEGY ASSOCIATE - Anchor Protocol Update - Dynamic Earn Rate - FSInsight

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Market Data Insight for Actionable Strategy

Crypto DeFi Digest April 7, 2022

Anchor Protocol Update - Dynamic Earn Rate

Walter Teng

DIGITAL ASSET STRATEGY ASSOCIATE

Dynamic Earn Rate NFT Genesis Mint 1/69

For important disclosures, see Page 14 Page 1

Crypto DeFi Digest April 7, 2022

Anchor Introduces Update to Earn Rate Calculation

Two issues ago, I wrote about Anchor Protocol, a dynamic savings platform that leverages

money market demand and diversified staking rewards to pay out attractive stablecoin

yields.

Much has developed since - as they say, one week in the depths of DeFi feels like one year in

real life.

Acknowledging how the macro environment has affected its micro mechanics, Anchor

Protocol garnered enough support on March 24th to pass Poll #20, in which a Terra protocol

researcher suggested the following changes to the Anchor Earn Rate:

% Earn Rate Change = min (abs (1.5%, ((YR % Change)), where

YR = Yield Reserve

Page 2

Crypto DeFi Digest April 7, 2022

Figure: Poll #20 Results

Source: Anchor Protocol

Effectively, this change allows Anchor to adjust the monthly yield payout to UST depositors

in proportion to the monthly rate of increase or decrease of the Yield Reserve balance.

The Anchor Earn Rate can be adjusted by a maximum of +1.5% in either direction. For

example, if the Yield Reserve increases by 10%, the Anchor Earn Rate increases by 1.5%. If

the Yield Reserve decreases by 0.5%, the Anchor Earn Rate can be adjusted by a maximum

of -1.5% and -0.5%. Here, Anchor Earn Rate reduces by 0.5%.

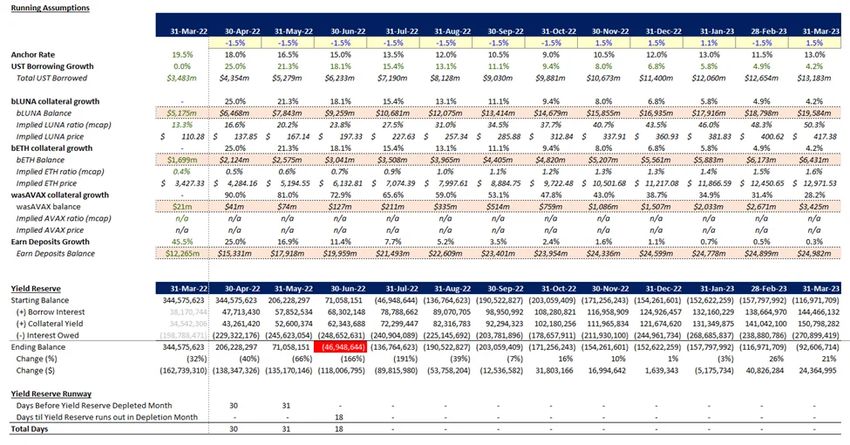

Updating Our Model

Given this material protocol update, I have expanded on the model from our Anchor

introductory issue to account for these changes and introduced other moving parts to more

precisely define the variables affecting the Anchor Run Rate, including these assumptions:

Firstly, I’ve introduced the dynamic earn rate according to the previous periods’

change in yield reserve balance.

Due to the sheer size of UST borrowed, however, the Anchor Earn rate will

consistently reduce by 1.5% per month until the Yield Reserve gets depleted.

Page 3

Crypto DeFi Digest April 7, 2022

I also assume bETH and bLUNA collateral growth starting at 25.0% (Oct’ 21 - Mar’ 21

growth rates stood at 23.5%), with growth rates adjusted downward by a factor of

0.80 from month to month.

Because wasAVAX is a new collateral addition, I assume growth starts at 90%

and is adjusted downward by a factor of 0.90 month to month. These

assumptions project $15.3b, $5.0b, and $3.4b in bLUNA, bETH, and wasAVAX

collateral respectively for Mar’ 23.

These are probably the most fluid assumptions in the model and are subject to

change quite frequently. However, this provides us with a proper framework to

estimate collateral runway.

I assume the same conservative growth assumptions for Anchor Earn deposits,

starting at 25% (March growth rates were 45.5%) and adjusted downward by a factor

of 0.8, resulting in $20b UST deposited by early June. The model also assumes staking

rewards remain unchanged throughout the projection year (neglecting Ethereum 2.0’s

projected post-merge surge in staking yields).

Figure: Anchor Dynamic Earn Rate Model

Source: Fundstrat

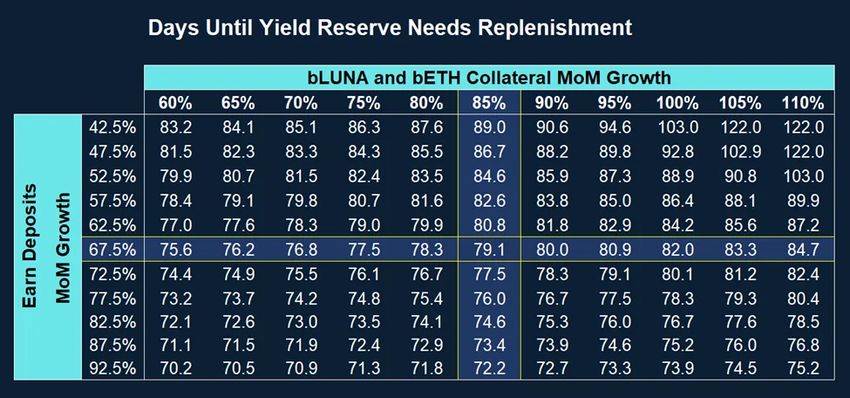

To understand the relative impact of each variable in the model above, we can again

sensitize the Anchor Earn deposits and collateral growth inputs below.

Page 4

Crypto DeFi Digest April 7, 2022

Figure: Days Until Yield Reserve Needs Replenishment Sensitized Against bLUNA and bETH Collateral

Growth and Earn Deposits Growth

Source: Fundstrat

Unsurprisingly, the takeaways are not dissimilar to my previous point-in-time analysis. As it

stands, Anchor has 80 days of run rate assuming bETH and bLUNA grow at 85% from their

end March collateral balances, and Anchor Earn deposits grow at 67.5%. These are fairly

aggressive for estimating the run rate (giving Do the benefit of the doubt), given that Earn

deposits have grown by 45.5% in March.

Since writing, Anchor emissions that subsidize bETH and bLUNA collateralized UST

borrowings have also dropped - seekers of leverage are currently paying a net 4.43% APR.

The strategic thinking behind this move eludes me, as lesser emissions translate to more

expensive (and less) borrowing, which results in less interest used to subsidize the Anchor

Earn Rate.

Page 5

Crypto DeFi Digest April 7, 2022

Figure: Net Borrowing Rate on Anchor as of 4/7

Source: Anchor Protocol

The preliminary takeaways here are that:

increasing collateral growth is helpful in closing the gap between the sources and uses

of the Anchor Protocol, but slowing deposits has a greater relative effect, and

regardless of actions taken, the sensitivity ranges presented above would only result

in at 43 days of the incremental runway at maximum

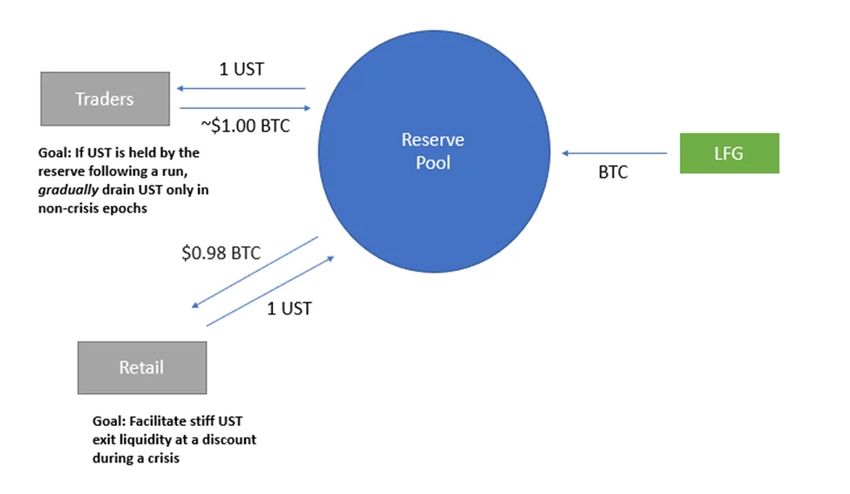

Bolstering the Peg by Purchasing BTC using Luna Foundation Guard (LFG)

Page 6

Crypto DeFi Digest April 7, 2022

Jump Trading’s Proposal

Source: Terra’s Agora Forum

In addition to reducing the Anchor Earn Rate, Do Kwon and his investors have been working

hard at restoring users’ confidence in the Terra ecosystem.

One high-profile initiative includes LFG’s purchases of BTC detailed in last week’s Crypto

Weekly, in which Sean wrote extensively about the effects of these purchases on spot price.

The $1.3b bitcoin (out of $3b) purchased is currently held in LFG’s wallet. LFG has indicated

that the reserve created through the $3 billion capital injection will effectively act as a

“release valve” for UST redemptions; it is designed to ensure that the price of the stablecoin

remains pegged to that of the dollar during sharp selloffs in crypto markets.

The introduction of LFG’s BTC reserve should temporarily appease concerns from investors

(as the market has indicated with LUNA and BTC rallying) in the broader Terra ecosystem in

the short term, but potentially introduces other vectors of risk.

By enabling redemption of UST for BTC instead of LUNA, BTC might see additional liquidity

flowing into exchanges from the Terra ecosystem during market distress. Nevertheless, this

new redemption mechanism is in aggregate safer (than without it), albeit at the cost of the

broader crypto ecosystem.

Page 7

Crypto DeFi Digest April 7, 2022

… And Leveraging DeFi 1.0 Giants…

Figure: Do Kwon Announcing 4pool on Curve

Page 8

Crypto DeFi Digest April 7, 2022

Source: Twitter

Additionally, Terra plans to deploy a permissionless pool on Curve called 4pool, consisting of

UST, FRAX, USDC, and USDT. The 4pool will be tested on Fantom and Arbitrum before

launching on the Ethereum mainnet once some Curve infrastructure is enabled.

Through a partnership with FRAX, the 4pool will realize Convex (CVX) and Curve (CRV)

synergies by leveraging Votium (delegated voting power protocol) incentives. Additionally,

4pool enables UST to become a collateral asset for the partially backed stablecoin FRAX

(apart from FXS).

By doing this, Do has also hinted at intentions to ‘starve’ the 3pool, comprised of DAI, USDC,

and USDT. For context, DAI, the overcollateralized stablecoin from MakerDAO, has long been

a rival of UST and Terra. To this point, Do frequently states that ‘Decentralized economies

need decentralized money’, alluding to the need for UST over its centralized competitor, DAI.

Should this vampire attack succeed, it will be a huge win for both leading algorithmic

stablecoins FRAX and UST, which we will cover in-depth in a future issue.

Page 9

Crypto DeFi Digest April 7, 2022

… And Recruiting the Help of Degens

Leveraging Protocol-Owned-Liquidity mechanics first popularized by OlympusDAO,

Redacted Cartel is a layer on top gauges (like Curve Finance) with the mandate of

accumulating control over the CRV, CVX, FXS, TOKE, and gOHM ecosystems. Its treasury

boasts over $100m in governance tokens, and has developed plans with Terra to leverage it

symbiotically.

Firstly, the Terra will leverage Redacted Cartel’s Hidden Hand, a generalized incentive market

protocol for veTokens to secure a Tokemak Reactor. With the Hidden Hand marketplace,

protocols will be able to create markets for their ve-tokens while Redacted captures a fee

that is redistributed to lockers of BTRFLY.

Secondly, debtDAO will issue its first UST-denominated loan to Redacted Cartel, piloting the

decentralized debt marketplace catering to other protocols.

Last but certainly not least, Terra will be leveraging Redacted Cartel’s influence over Curve

and Convex.

For those unfamiliar, Curve Finance is an automated market maker which specializes in

stablecoins swap with low price slippage. As covered in a previous issue of DeFi Digest,

liquidity providers deposit stablecoins into a pool to earn trading fees. The governance token,

CRV, can be locked for a period of 1 to 4 years at 0.25 to 1 conversion rate for veCRV.

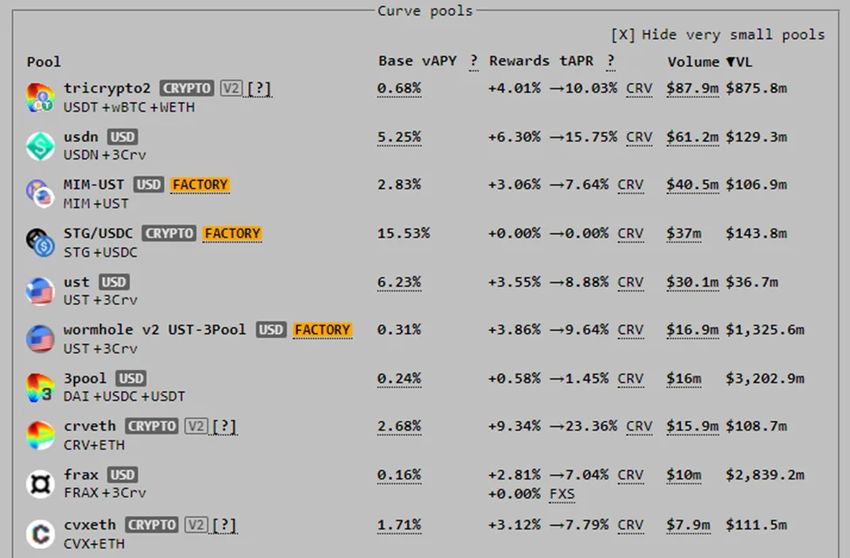

Page 10Crypto DeFi Digest April 7, 2022

Figure: Curve Pools

Source: Curve Finance

This vote-escrowed CRV (veCRV) that represents locked CRV tokens then allows liquidity

providers to earn boosted rewards for their liquidity pools. For example, vote-locking CRV for

1 year gives you 0.25 veCRV, which can boost rewards by a factor of 0.8. Holders of veCRV

can either vote to direct CRV rewards towards their desired LP pool or receive ‘bribes’ from

other protocols to direct votes to them.

Sitting on top of the Curve ecosystem, Convex Finance is another project that attempts to

capture the governance power over CRV emissions. Currently, 43% of veCRV is held by

Convex as vote-locked (vlCVX), signaling that Curve wars have already found a winner.

As such, the power struggle shift towards Convex - whoever controls Convex has influence

over Curve. In comes the Redacted Cartel.

Being the third largest DAO holder of CVX, Redacted Cartel will vote for the 4pool

(UST+3CRV) and claim UST votium incentives. Redacted has also agreed not to sell UST for

other stablecoins and will use it to pay contributors, partake in seed deals, partake in single-

sided LPs, and build their treasury.

Page 11Crypto DeFi Digest April 7, 2022

This partnership appears to be mutually beneficial as Redacted can solely receive a single

stablecoin (UST) instead of multiple tokens from Votium that are not necessarily aligned with

their mission. Terra, on the other hand, introduces another source of yield for UST (apart from

Anchor) and bolsters broader adoption for UST in DeFi.

Bottom Line

Through the Redacted Cartel and Frax initiatives, Do Kwon attempts to ease the pressure on

Luna and the Anchor Yield Reserve from the public lens, but the numbers don’t lie - despite

the proposed changes to the protocol, and apparent new use cases for UST, Anchor

yields cannot sustain at these rates for much longer without significant changes to the

model. When yields compress, market participants will at best leave for greener pastures in

the 4pool or at worst stablecoin farms elsewhere.

While it is tough to estimate the aggregate effects on UST from Terra’s initiatives and the rate

at which Anchor’s Yield Reserve is depleting, one cannot help but wonder: “Anon, 73% of UST

is currently deposited in Anchor. Will Terra be able to support demand for UST before Anchor

Yield Reserve depletes? If not, what happens to LUNA price?”

Page 12Crypto DeFi Digest April 7, 2022

Figure: Anon Trying to Ascertain the Aggregate Effects of All This

It is all too easy to paint a picture of gloom for Anchor, Luna, and UST based on the

commentary above. Nonetheless, I can imagine a world in which UST succeeds as the first

widely-adopted decentralized algorithmic stablecoin (and LUNA price continues its surge up).

Regardless of what happens in the ensuing months, one thing is for sure - Do has proved

himself to be an exceptional community and narrative builder, deserving of the success Terra

has had so far.

If the race to facilitate organic demand for UST started one year ago on Anchor’s birthday, it

surely feels like we are in the homestretch now.

Page 13Crypto DeFi Digest April 7, 2022

Disclosures

This research is for the clients of FSInsight only. FSI Subscription entitles the subscriber to 1 user,

research cannot be shared or redistributed. For additional information, please contact your sales

representative or FSInsight at fsinsight.com.

Conflicts of Interest

This research contains the views, opinions and recommendations of FSInsight. At the time of publication

of this report, FSInsight does not know of, or have reason to know of any material conflicts of interest.

General Disclosures

FSInsight is an independent research company and is not a registered investment advisor and is not

acting as a broker dealer under any federal or state securities laws.

FSInsight is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA

registered broker-dealer that is focused on supporting the independent research industry. Certain

personnel of FSInsight (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA

member firm registered as a broker-dealer with the Securities and Exchange Commission and certain

state securities regulators. As registered representatives and independent contractors of IRC Securities,

such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by

FSInsight clients directly with IRC Securities or with securities firms that may share commissions with IRC

Securities in accordance with applicable SEC and FINRA requirements. IRC Securities does not distribute

the research of FSInsight, which is available to select institutional clients that have engaged FSInsight.

As registered representatives of IRC Securities our analysts must follow IRC Securities’ Written

Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the

facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4)

appropriate use of electronic communications, amongst other compliance related policies.

FSInsight does not have the same conflicts that traditional sell-side research organizations have because

FSInsight (1) does not conduct any investment banking activities, and (2) does not manage any

investment funds.

This communication is issued by FSInsight and/or affiliates of FSInsight. This is not a personal

recommendation, nor an offer to buy or sell nor a solicitation to buy or sell any securities, investment

products or other financial instruments or services. This material is distributed for general informational

and educational purposes only and is not intended to constitute legal, tax, accounting or investment

advice. The statements in this document shall not be considered as an objective or independent

explanation of the matters. Please note that this document (a) has not been prepared in accordance with

legal requirements designed to promote the independence of investment research, and (b) is not subject

Page 14Crypto DeFi Digest April 7, 2022

to any prohibition on dealing ahead of the dissemination or publication of investment research. Intended

for recipient only and not for further distribution without the consent of FSInsight.

This research is for the clients of FSInsight only. Additional information is available upon request.

Information has been obtained from sources believed to be reliable, but FSInsight does not warrant its

completeness or accuracy except with respect to any disclosures relative to FSInsight and the analyst’s

involvement (if any) with any of the subject companies of the research. All pricing is as of the market

close for the securities discussed, unless otherwise stated. Opinions and estimates constitute our

judgment as of the date of this material and are subject to change without notice. Past performance is

not indicative of future results. This material is not intended as an offer or solicitation for the purchase or

sale of any financial instrument. The opinions and recommendations herein do not take into account

individual client circumstances, risk tolerance, objectives, or needs and are not intended as

recommendations of particular securities, financial instruments or strategies. The recipient of this report

must make its own independent decision regarding any securities or financial instruments mentioned

herein. Except in circumstances where FSInsight expressly agrees otherwise in writing, FSInsight is not

acting as a municipal advisor and the opinions or views contained herein are not intended to be, and do

not constitute, advice, including within the meaning of Section 15B of the Securities Exchange Act of

1934. All research reports are disseminated and available to all clients simultaneously through electronic

publication to our internal client website, fsinsight.com. Not all research content is redistributed to our

clients or made available to third-party aggregators or the media. Please contact your sales

representative if you would like to receive any of our research publications.

Copyright © 2022 FSInsight LLC. All rights reserved. No part of this material may be reprinted, sold or

redistributed without the prior written consent of FSInsight LLC.

Page 15You can also read