Reimagining aged care - June 2017

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Reimagining aged care.

What we will cover today

• Dynamics of elderly care

• Importance of care delivery at-home

• Quick intro to Curo and behavioural monitoring

• How to make an insurance pilot work

• InsurTech and the challenges of startups working

with insurers

Scalemodel – Privileged and Confidential Page 2

Demographic shifts placing extraordinary pressure Australian

Market

on already strained Aged Care services sector

Baby boomers growing at nearly twice the …and are the most expensive age group to

rate… treat

Population growth by age group Healthcare spend per person

(2015-2021) (%) (A$K)

Scalemodel – Privileged and Confidential Page 3

Note: Healthcare spends includes expenditure by governments, individuals and non-governments sources (e.g. private health insurers)

Source: ABS; AIHW

The Aged Care market is large, and evolving, both in

Australia, and around the world

Home & EOL Hospital &

Care Type Home Care Residential Care

Community Care Hospice Care

Description Home support Services to help Accommodation and Purpose built facility

services to promote seniors remain at comprehensive day for complex healthcare

independent living home when in poor support, spanning only

for longer health (medical, medical & non-medical

domestic & services

community)

Annual Gvnt. Spend $1.9B $1.3B $10.6B ~$3B

($B)

Annual Total Spend $2.1B $1.4B $16.1B ~$3B

($B)

CAGR (‘12-’15) 11% 8% 5% ~3%

Scalemodel – Privileged and Confidential Page 4

Note: Non-gov. funding includes private and other sources

Source: Deloitte access economics; ACFA 2013-16; IBISWorld; Palliative Care Australia

Receiving Aged Care in your own home is a universally

better outcome

1. 2.

Physical Health Mental Wellbeing

3. 4.

Personal

System Costs

Preference

Scalemodel – Privileged and Confidential Page 5

Note: Non-gov. funding includes private and other sources

Source: Deloitte access economics; ACFA 2013-16; IBISWorld; Palliative Care Australia

Two major trends are redefining the provision of

Aged Care, in Australia (and other global markets)

Residential Care & Hospitals Time & Materials

Care & Wellness @ Outcome-Focused

Home Care

Scalemodel – Privileged and Confidential Page 6

These changes present a range of opportunities to

health insurers among their older member cohorts

• Increased opportunity to take a more direct, ’hands

on’ role in care delivery

• Ability to build outcome-delivery into product design

• New [insurance] products designed to support older

cohorts with independent living at home

• Greater adoption of new technology to support the

wellbeing of members

Scalemodel – Privileged and Confidential Page 7

Curo is re-imagining the way in which technology is

used in the Aged Care industry

Under-invested

Lack of Excessive, Radical shift in

in technology as

outcome- wasted cost care delivery

tool for

focused across the Care (CDC regulation,

efficiency and Feb 2017)

decision making Ecosystem

cost-reduction

Technology that delivers care outcomes,

rather than simply supporting operations

Scalemodel – Privileged and Confidential Page 8

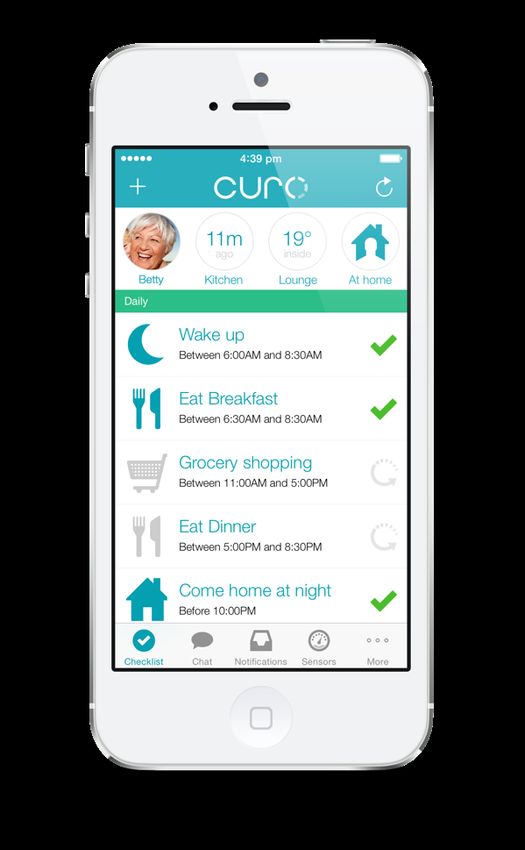

Curo’s puts in-home sensors in the homes of aged adults to passively monitor their behaviour Scalemodel – Privileged and Confidential Page 9

Curo measures behavioural data, and adherence of an individual to a predictable pattern of activity Curo collects 1000’s of pieces of data from a single home in a day. We visualize data in an intuitive way that relates to behavior, not technology. Behavioural tasks are customised to every senior, and their current level of independence Scalemodel – Privileged and Confidential Page 10

We share this information in the form of actionable

insights, with family members and professional carers

Providers

Carers

Cloud platform

Family

Scalemodel – Privileged and Confidential Page 11Curo is a data and analytics business; we share

actionable insights that provoke reaction

Changes in wellness score are the best

indicator that something is wrong.

Scalemodel – Privileged and Confidential Page 12Curo’s rich behavioural data set delivers benefits for

every participant in the Care Ecosystem

For Care Workers For Providers

• Real time insight into what • Efficiently prioritize and

happens when you can’t manage client care

be there • Reduction in individual

• Prioritise visits and care care costs, through insight

needs through Wellness

Score

For Families For Insurers

• Peace of mind from • Directly impact health

understanding of what is outcomes for senior

happening at home members

• Personalised alerts to • Lower disbursement

provide guidance when costs through reduced

something has changed hospitalisation rates

Scalemodel – Privileged and Confidential Page 13We are currently piloting our monitoring product with

providers, insurers & health systems in US & Australia

Outcomes Commercial Models Satisfaction levels

(health & wellness, system-wide cost (Provider subsidised, MBS funded, (Aged adult, families, care giver, HF

reduction, time spent at home) private pay, member benefit, etc) member)

Scalemodel – Privileged and Confidential Page 14Australian

Insurer

CASE STUDY: Insurance Co. Pilot Program

Pilot Program Dynamics Key Outcome Measurement

• 500+ pilot participants reduction in hospitalisation

% (rate, cost)

• Range of age cohorts,

starting at 65 reduction in overall member

% claim costs

• Engaged family members to

engage with data and insights increased rates of member

satisfaction

• Curo managing recruitment,

installation and execution increased level of family

engagement in care giving

Scalemodel – Privileged and Confidential Page 15Australian

Insurer

PROGRAM CONCEPT: Operational Alignment

Insurer Curo

• Scaled membership adoption • Designed for home; intuitive functionality

• High level of member utilization • Passive technology (no user interaction)

• Ease of launch & maintenance • Simple deployment; low-touch utilization

• Multiple use-cases • Diverse insight capabilities

Scalemodel – Privileged and Confidential Page 16“InsureTech” investment is growing, but seriously

lagging “Fintech” by deal volume and magnitude

$9.9B

Deal value ($M) No. deals

$1,000 90

78

$900 80

$800

70

$700

60

52

$600

$496 50

$483

$500

40

$400 30

24 30

$300

$161 20

$200

$109

$100 10

$0 0

2013 2014 2015 2016 2016

FinTech

$ #

>80% investment into classic

business models with new edge

Scalemodel – Privileged and Confidential Page 17

Source: CBInsights, September 2016; ”Pulse of Fintech”, KPMG, September 2016The insurance industry is ripe for massive disruption

over the coming three years

Approx. Global

market share

(disruptors) 0% 25% 50% 75% 100%

Scalemodel – Privileged and Confidential Page 18

Source: Leading Edge Forum, 2016 (http://www.computerweekly.com/opinion/The-pace-of-digital-disruption-varies-widely-by-industry)Close to half of insurance executives don’t anticipate

digital disruption in 2017/18

Scalemodel – Privileged and Confidential Page 19

Source: “Digital Pulse 2015”, by Russell Reynolds & AssociatesEngaging with early stage businesses can help

insurers in a range of ways

Support

§ Create PR/brand halo

Innovation PR

§ “Innovative” work place – tool for employee recruitment/engagement

agenda

§ Insight on key trends & emerging technologies to inform strategy

Learning +

§ Identify and recruit scarce talent

education

§ Exposure to new ways of working & structures

Scale

§ Actively participate in the disruption of insurance industry through sponsorship of new

development &

products, services & business models

commercialisation

Support growth & § Support material future growth plays

diversification § Proactive management of economic outcomes through the cycle

Pure financial § Deliver material ($$), above average returns (>25% IRR) on capital deployed

returns § Invest into categories/deals where insurer brings unique capability

Scalemodel – Privileged and Confidential Page 20

Source: “Digital Pulse 2015”, by Russell Reynolds & AssociatesStart-ups working with larger corporates is fraught with

challenges

For Insurers For Start-ups

• Feels unstructured, and high- • Feels slow and cumbersome

risk

• Challenging to get to the right

• Hard to engage a large internal people

team

• Large scale projects can

• Requires deep self-reflection consume lots of critical

(to sponsor cannibalisation) resources

• Internal processes typically

cannot accommodate new

ways of working

Scalemodel – Privileged and Confidential Page 21

Source: “Digital Pulse 2015”, by Russell Reynolds & AssociatesA [potential] recipe for success

• Start with a clear, agreed understanding of objectives and

measures of success for innovation

• Align activity (internal, external) to these objectives

• Choose activities carefully, but commit to them hard

• Recognise the barriers that start-ups face when working

with larger companies, and work to address them

Scalemodel – Privileged and Confidential Page 22

Source: “Digital Pulse 2015”, by Russell Reynolds & AssociatesBasic Copyright Notice & Disclaimer ©2017 This presentation is copyright protected. All rights reserved. You may download or print out a hard copy for your private or internal use. You are not permitted to create any modifications or derivatives of this presentation without the prior written permission of the copyright owner. This presentation is for information purposes only and contains non-binding indications. Any opinions or views expressed are of the author and do not necessarily represent those of Swiss Re. Swiss Re makes no warranties or representations as to the accuracy, comprehensiveness, timeliness or suitability of this presentation for a particular purpose. Anyone shall at its own risk interpret and employ this presentation without relying on it in isolation. In no event will Swiss Re be liable for any loss or damages of any kind, including any direct, indirect or consequential damages, arising out of or in connection with the use of this presentation.

You can also read