Regime change Economic and financial outlook 2022 Research Department 17 december 2021 - IMI Corporate & Investment Banking

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Economic and financial outlook 2022 Regime change Research Department 17 december 2021

1. Macroeconomic outlook inflation risk matters more than the inflation level Luca Mezzomo Head of Macroeconomic Analysis – Research Department

Are we heading towards a new Great Inflation as in

2

the 1970s?

In the 1970s, it started at 5%, then it turned

double-digit

The alleged similarities:

Energy and other supply-side shocks:

oil shocks in the 1970s, oil/natural gas

and supply chains in 2021-22

Loose mix of fiscal policy and

monetary policy: subordination in the

1970s, “cooperation” through

negative rates and asset purchases in

2020-21

Excess demand

Stronger wage dynamics: wage

negotiations in the 1970s, low

participation and the Great

Resignation in 2021

In our view, the institutional changes

since the 1970s, make a new Great

Inflation very unlikely. Instead, they

will prompt an earlier turnaround of Source: IMF, International Financial Statistics

the monetary policy cycle in

advanced countries. Let us see why.

3

The supply-chains issue: mixed signals

Freightos container indexes by route Signs of improvement:

Rising inventories of

inputs/intermediate goods

Lower congestion indexes at US ports

Cost of moving containers is lower

(from Asia to US) or stable (from Asia

to EU)

But the situation is still far from

normal:

Delivery times are still rising (though

less than before in EU and US)

Stocks of final goods remain low

Output struggles to keep pace with

orders.

Improvement expected in 2022-23

(slower growth in demand, capacity

increases and reduction in backlog)

Source: Freightos

Downstream, inventories of inputs rise but the

4

situation remains far from normal

Stock of purchases are now rising… … but delivery times are still unreliable

(Manufacturing PMI surveys) (Manufacturing PMI surveys)

Source: IHS Markit Source: IHS Markit

Energy prices: past the peak, but new bouts of

5

volatility are likely in 2022

We expect energy prices to have peaked, crude oil in particular (demand-

supply balance is turning more negative). But yearly average prices will be 10%

higher, nonetheless. And new seasonal volatility bouts are more likely for natural

gas, owing to very low stocks, geopolitical risks and structural factors.

The baselina assumptions about oil prices …and natural gas prices

Source: Refinitiv and Intesa Sanpaolo forecasts Source: Refinitiv and Intesa Sanpaolo forecasts

6

Fiscal stance: too loose for too long?

Aggregate demand in the US and in the euro area is growing too fast, given

the constraints on supply.

Fiscal policy will remain too loose in 2022, in the US especially.

Cyclically adjusted primary balance (% of potential GDP, gap vs. 2015-19)

2

1

0

-1

-2

-3

-4

-5

-6

-7 euro area UK US Japan

-8

2020 2021 2022 2023

Source: IMF, Fiscal Monitor, October 2021

Monetary policy has been “cooperative” with fiscal

7

policy, so far

Indeed, monetary policy has actively cooperated with fiscal policy in 2020

and 2021, when the focus was on overcoming the pandemic crisis.

Central bank balance sheets hit record Global rates are record low

levels in 2021, as % of GDP

60%

% of aggregate GDP

50%

40%

30%

20%

10%

0%

2008 2010 2012 2014 2016 2018 2020 2022 2024

Fed ECB BoJ G7+

Source: Intesa Sanpaolo calculations and projections from Source: Intesa Sanpaolo and Oxford Economics. Average

central banks’ data. of 44 advanced and emerging economies.

8

However, the labour market is not that of the 1970s…

(1) The Great Inflation was preceded by strong wage growth, in a tense

political and social environment. The wage increases of 2021-22 are instead

the side-effect of strong economic growth, and are significantly lower.

(2) Nowadays, there is a significant share of temporary workers

(3) there is no automatic indexation of wages to prices

The Great Inflation of the 1970s was …while at present the increase in labour

introduced by strong wage rises… costs is not runaway

20 20

18

15 16

14

10 12

10

5 8

6

0 4

2

-5 0

USA UK DEU FRA ITA NLD USA UK DEU FRA ITA NLD

Nominal wages(1) Real wages(1) ULC(2) Nominal wages Real wages ULC

Source: (1) R. Flanagan, D. Soskice, L. Ulman: "Wage problems Source: Intesa Sanpaolo projections

since the mid-60s", in Unionism, Economic Stabilization and

Incomes policies: European experience, The Brookings

Institution 1983; (2) OECD, Main Economic Indicators.

…and central banks are now committed to achieve

9

price stability

Fed, ECB, Bank of England, Bank of Canada all have the mandate

to pursue price stability.

In the 1970s, central banks could pursue price stability only in so far as it did not

jeopardize Treasury refinancing plans; and, when faced with supply-side shocks,

they gave priority to employment, rather than price stability

Instead, the latest strategy reviews have confirmed the primacy of price stability,

while introducing correctives to allow for limited flexibility (ECB: temporary

overshooting of 2%, medium-term orientation; Fed: inflation averaging; Bank of

Canada: inflation range 1-3%)

Asset purchase programmes have been always performed only during periods of

inflation persistently below target.

Sustainability of government debt vs price stability?

A conflict between the mandate to achieve price stability and government debt

sustainability may occur in the future, given high debt ratios.

Not in 2022-23, however: (a) cost of debt will rise only very slowly, because of

negative interest rates and large share of debt owned by central banks; (b)

refinancing risk mitigated by rollover of large QE portfolios, despite lower net

purchases.

Lower political acceptance of inflationECB: step-by-step reduction of net asset purchases

10

in 2022

ECB’s purchase programmes will be scaled

down in 2022

Net PEPP purchases will be scaled down

in Q1 2022 and suspended afterwards.

They could resume if the pandemic ABS CBPP

impacts the inflation outlook again. 200

CSPP PSPP

180

APP net purchases: 40Bn in Q2, 30Bn in

Q3, 20Bn from October 2022. To be PEPP Total

160

suspended shortly before first rate hike.

140

Reinvestments: until Dec 2024 for PEPP, 120

until well after first rate hike for APP.

100

Policy rates: they will be raised when

inflation forecasts after mid-point of the 80

horizon reach 2% and underlying inflation 60

is consistent with headline inflation stable

at 2%. This could be possible in 2023. 40

20

Refinancing operations: no reason to

expect a TLTRO IV. The ECB will just 0

View: we expect the APP to be -20

suspended in first half of 2023. First rate

hike possible from spring 2023 (current Source: ECB data, Intesa Sanpaolo projections.

assumption: September 2023).11

Implications: (1) towards slower GDP growth

2021Q4 and especially 2022Q1 will be negatively affected by the new

contagion wave. GDP growth will slow down in most countries (main

exceptions: oil producing countries, Japan, Spain).

GDP growth will slow down after the 2021 Average 2022-23 GDP growth will be stronger

bounce than in 2018-19, but with notable exceptions

2019 2020 2021f 2022f 2023f

10%

United States 2.3 -3.4 5.6 4.1 2.4

Euro Area 1.6 -6.5 5.1 3.9 2.6 8%

GDP growth 2022-23

Germany 1.1 -4.9 2.7 4.1 2.7

France 1.8 -8.0 6.6 3.5 2.3 6% World

Italy 0.4 -9.0 6.2 4.3 2.4 Advanced

Spain 2.1 -10.8 4.5 5.4 4.0 4%

China

OPEC -1.5 -5.2 3.3 4.9 4.2

Eastern Europe 3.0 -3.1 4.8 4.0 3.3 2% Emerging

Latin America 1.3 -6.4 6.5 2.8 2.7

0%

Japan -0.2 -4.5 1.7 3.3 1.6

China 6.0 2.3 8.2 5.5 5.6

-2%

India 4.8 -7.0 8.2 7.0 6.2 -2% 0% 2% 4% 6% 8% 10%

World 2.8 -3.3 5.9 4.6 3.7

GDP growth 2018-19

Source: Intesa Sanpaolo Source: Intesa Sanpaolo and Oxford Economics’

projections12

In the Eurozone, GDP growth will be driven by domestic

demand…

Consumption and investments will support the

recovery also in 2022. Contribution of net exports

substantially neutral

Between Q4 2021 and Q1 2022,

consumption will be held back

by the contagion wave.

15 15

In the short term, investments in

10 10 machinery will continue to suffer

5 5 from supply bottlenecks

0 0 The rise in energy prices will also

-5 -5

weigh on private spending and

investments at the turn of the

-10 -10 year

-15 -15

2017 2018 2019 2020 2021 2022

However, the fundamentals for

consumer spending gov. cons.

domestic demand remain

GFCF stockbuilding robust and point towards a

Net exports GDP growth (y/y %)

Source: Refinitiv Datastream reacceleration from Q2 2022

Note: contributions to y/y % growth.

Source: Intesa Sanpaolo calculations on Refinitiv-

Datastream data13

…employment recovery and reduction of excess

savings will support consumer spending…

The rise in infections could temporarily slow Even partial spending of the extra savings

down but not reverse the resumption of could further support private consumption

hiring

PMI Comp

60 3

2

55

1

50

0

45 PMI - jobs (lhs) -1

Employment, y/y

40 Employment, q/q -2

35 -3

14 15 16 17 18 19 20 21

Source: Refinitiv Datastream

Source: Intesa Sanpaolo calculations on Markit and Source: Intesa Sanpaolo calculations on Eurostat data

Eurostat data.14 … and the outlook for industry and services will brighten after the winter months The catch-up potential for activity in more Bottlenecks may have peaked... The order contact-intensive services is still large, but backlog and the need to replenish inventories the gap will only close once the health risk provide solid grounds for industry once supply has been reduced. constraints are reabsorbed Nota: 2019Q4= 100. Fonte: elaborazioni Intesa Sanpaolo su Fonte: elaborazioni Intesa Sanpaolo su dati Refinitiv- dati Refinitiv-Datastream Datastream

Inflation: headline inflation may have peaked, core

15

inflation may rise further

Base effects will lower headline inflation sharply in 2022 – barring new energy

price shocks. Core measures on inflation will diverge in the first half of next

year, with more subdued developments in Japan and euro area.

Headline inflation, quarterly averages CPI excluding energy, quarterly averages

(y/y % changes) (y/y % changes)

7.0 6.0

6.0 5.0

5.0 4.0

4.0

3.0

3.0

2.0

2.0

1.0

1.0

0.0

0.0

-1.0

-1.0

-2.0

-2.0

2019 2020 2021 2022 2023

2019 2020 2021 2022 2023

Canada United States Japan Canada United States Japan

United Kingdom Eurozone United Kingdom Eurozone

Source: national statistical offices and Intesa Sanpaolo Source: national statistical offices and Intesa Sanpaolo

forecasts forecasts16

Euro area: inflation to drop markedly in 2022, but the

end point will depend on energy prices

The HICP is expected to rise by 3.1% in 2022. The impact of supply bottlenecks, the partial

transfer of energy prices and better conditions on the labor market will lead to a

recovery of the core index (2022 estimate: 1.9%). Energy will explain about a third of the

price dynamics and will remain a key source of shocks.

Euro area inflation will drop below 2% in Q4 ...but a repetition of the 2021 shock on

2022… natural gas would keep headline inflation

above 2% until Q4 2023

4.0

3.5

3.0

2.5

2.0

1.5

1.0

Baseline forecasts Natural gas shock

Source: Refinitiv-Datastream, Intesa Sanpaolo forecasts Source: Refinitiv-Datastream, Intesa Sanpaolo projections17

(2) Less capital flows to emerging markets

The sharp acceleration of monetary policy tightening in the US will negatively

affect emerging markets. Capital flows to EMs are already shrinking, after the

end-2020 bounce. Some will be forced into monetary tightening, or will face

currency crises.

Capital flows to emerging markets are Turkey opts for a currency crisis, Brazil for

already shrinking tighter monetary policy

100

Total Flows

75

50

25

0

-25

China Debt Flows

-50 China Equity Flows

EM ex-China Equity Flows

-75

EM ex-China DebtFlows

-100

nov 19 mag 20 nov 20 mag 21 nov 21

S

Source: IIF, Capital Flows Tracker Source: Refinitiv18 (3) Change of regime for financial markets? Market reaction to the change of regime has been very orderly so far. Currency markets: more volatility because of de-synchronized business cycles and monetary policy action? Yield curves: higher real rates? Flatter or steeper slope? Will breakeven inflations stay well anchored, and which way will they move? Implications of decreasing central bank support for sovereign spreads and credit spreads Implications of higher inflation and a maturing business cycle for equity markets

2. Macroeconomic outlook US: the rise in inflation is not transitory and the FED is ready to remove the punchbowl Giovanna Mossetti Economist, Macroeconomic Analysis – Research Department

20

US - The Covid recession is history, excess demand is

everywhere

GDP growth is a tale of two sides: super-strong GDP already above pre-Covid levels and close

demand and insufficient supply to pre-Covid trend, employment way behind

Source: Refinitiv-Datastream, Intesa Sanpaolo forecasts Source: Refinitiv-DatastreamWhat’s in store for 2022? More of the same, with

21

demand outstripping supply for goods…

Shipments cannot keep up with Demand for goods marching on,

skyrocketing orders supply constraints notwithstanding,

services catching up

Source: Refinitiv-Datastream Source: Refinitiv-Datastream22

…and labor: where have all the workers gone?

Not enough workers to satisfy demand Unemployment plummeting, participation

still almost flat

Source: Refinitiv-Datastream Source: Refinitiv-Datastream23

Labor supply constrained by retirements, quits and

behavioral changes

More job openings than unemployed The labor market is tight, wage increases

fail to lift supply (so far)

55 1,6

50 1,4

45 1,2

40 1,0

35 0,8

30 0,6

25 0,4

20 0,2

14 15 16 17 18 19 20 21

JOB OPENINGS/UNEMPLOYED, rhs

% firms w/1 or more hard to fill jobs

Recession

Fonte: Refinitiv Datastream

Fonte: Refinitiv-Datastream Source: Refinitiv-Datastream24

“Rapid progress toward maximum employment”

(J. Powell, 15/12/2021)

Pre-Covid employment could be reached …and the unemployment rate is likely to hit

by 2022 Q3… 3.5% in 2022Q1, unless the participation

rate recovers

Forecast:

unempl. rateThe Fed’s mandate on inflation is already more than

25

met, with second-round effects in full sight

Firms plan higher selling prices and The average budgeted salary increase

higher compensation for 2022 jumps to 3.9%, highest rate in 20

years

4.5 4

3.5

3.9

4

3

2.5

3.5

2

1.5

3

1

0.5

2.5

0

2 -0.5

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

budgeted salary increases cpi, rhs

Source: Refinitiv-Datastream Source: Conference Board business survey for «budgeted

salary increase», FRED for CPI26

Price changes not peaking (yet) for goods…

2 yr inflation rates: these are NOT effects Core commodities have more room

from Covid! ahead

Source: Refinitiv-Datastream Source: Refinitiv-Datastream27

…and services

Double-digit salary increases in the food Rents and owner equivalent rents react

service industry lead higher prices with a lag to home price increases: the

shelter component are expected to

reach record highs in 2022

Tight labor

market effect

Covid effect

Source: Refinitiv-Datastream Source: Refinitiv-Datastream28

Underlying inflation: red alert!

This inflation will not go away on its own Measures of underlying inflation homogeneously hot

nov-20 nov-21 mean

2009-19

8.0

Core CPI 1.7 5 1.9

7.0 Mar 2022: core FRB Cleveland median 2.2 3.5 2.2

5.4% CPI

6.0 FRB Cleveland 16% 2.1 4.6 1.9

Trimmed mean CPI

5.0 Sep 2022

core 3.6% Atlanta Fed sticky CPI 2 3.4 2.1

4.0 Core PCE 1.4 4.1 1.6

Market- based Core PCE 1.3 3.8 1.4

3.0

FRB Dallas Trimmed -Mean 1.8 2.6 1.7

2.0 PCE

FRB San Francisco 2.8 4.6 2.3

1.0 Cyclical Core PCE

Cyclically Sensitive 1.9 3.9 1.5

0.0

Inflation (Stock-Watson

Jun-18

Jun-19

Jun-20

Jun-21

Jun-22

Jun-23

Mar-18

Mar-19

Mar-20

Mar-21

Mar-22

Mar-23

Sep-18

Sep-19

Sep-20

Sep-21

Sep-22

Dec-18

Dec-19

Dec-20

Dec-21

Dec-22

2019)

CPI CPI core

Source: Atlanta Fed. Note:green: within target range (-/+0.25

from target); light blue: between 0.25 and 0.50 ppt target; red: more than 0.50 ppt > target. Oct.

data for PCE measures .29

Real rates are stimulating demand further: this explains

the Fed’s urgency to bring forward the lift-off

All possible versions of the Taylor Rule The «new» Fed looks a lot like the

imply a fed funds rate around 6% «old» Fed..

8.0

4.0

0.0

-4.0

-8.0

-12.0

-16.0

02/12

08/12

02/13

08/13

02/14

08/14

02/15

08/15

02/16

08/16

02/17

08/17

02/18

08/18

02/19

08/19

02/20

08/20

02/21

08/21

Taylor Rule/unempl Actual Fed Funds Rate taylor Rule/GDP

Source: Atlanta Fed. Laubach-Williams R star (natural real Source: Refinitiv-Datastream

interest rate) estimated currently at 0.36%)30 J. Powell in his own words (15/12/2021) ”The balanced approach provision (…) says that in effect in situations in which the pursuit of the maximum employment goal and the price stability goal are not complementary, we have to take account of the distance from the goal and the speed at which we’re approaching it. It is a provision that would enable us to, in this case because of high inflation, move before achieving maximum employment. Now, we’re—as I said, we’re making rapid progress toward maximum employment in my thinking, in my opinion. I don’t at all know that we will—that we’ll have to invoke that paragraph.” “You have to make an assessment that what’s—what is the level of maximum employment that is consistent with price stability in real time”. “We have to make policy now, and inflation is well-above target.” “When we communicate about what we’re going to do, the markets move immediately to that. So financial conditions are changing to reflect, you know, the forecasts that we made”. “We had our first discussion about the balance sheet (…), and we went through the way the sequence of events regarding the runoff (…) last time. But people pointed out that this is a significantly different economic situation that we have at the current time, and that those—the differences that we see now would tend to influence how we think about the balance sheet.”

31

Back to the future: Fed in inflation-fighting mode

Higher inflation, fueled by supply constraints

and strong demand, is now entrenched in the

economy. A wage/price spiral is already under

way. Supply may normalize in 2022H2, but

demand must be reined in now. Hence, the Fed ISP forecast: first hike in June 2022, or March if

is back to a pre-90’s regime, positioning necessary, end-point at 2.25% in 2024

monetary policy to bring inflation under control

The outlook has upside risks for inflation and rates in 2022

through a reduction of excess demand.

2021 2022 risks 2023 risks

2022 2023

The labor market is the crucial factor for the

GDP 5.6% 4.2% down 2.4% down

2022 scenario. In the absence of a significant

CPI 4.7% 4.0% up 2.4% up

pick-up of labor supply, the Fed may have to

CPI core 3.6% 4.0% up 2.4% up

tighten more than factored in by current

# Rate hikes 0 3 up 3 even

forecasts. Risks are for excessive tightening and

Source: Intesa Sanpaolo forecasts. CPI, CPI core and GDP

a growth slowdown in 2023. are annual averages.

Inflation is now also a political problem:

Congress and the Administration will not stand

in the Fed’s way when rates go up. Finally, fiscal

policy is frozen in limbo. The Build Back Better

Act may never pass and some support for lower

income households may expire. The political

outlook is dire for Democrats, with likely losses of

both the House and the Senate at the 2022

Midterm elections.3. The outlook for rates and government bonds Sergio Capaldi Fixed Income Strategist – Macroeconomic Analysis, Research Department

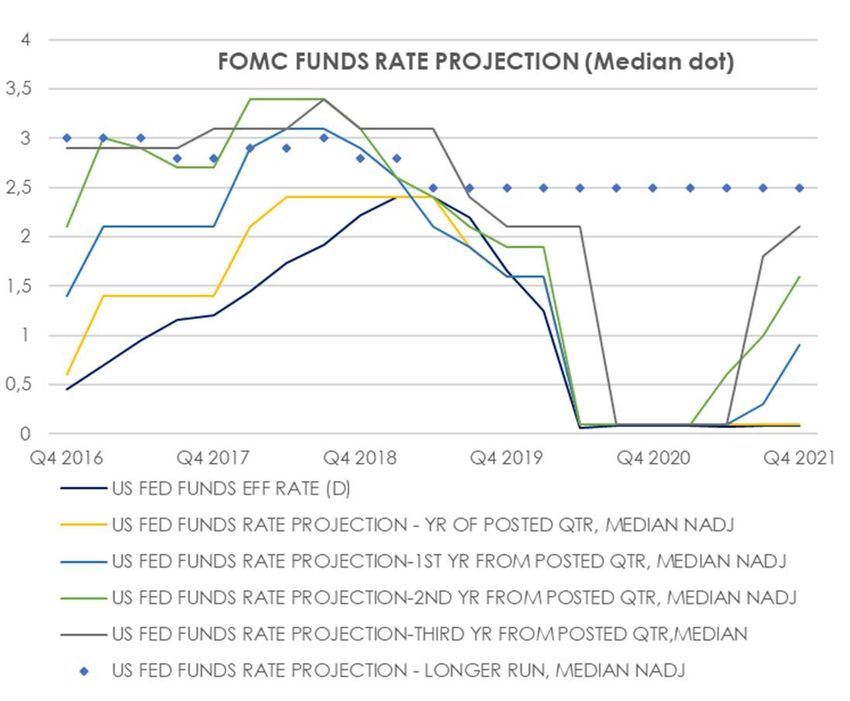

33 Inflation will be the real issue of 2022 Inflation has emerged as the talking point of financial market in the last few months. The long awaited slowdown in inflation dynamics has been replaced with a staggering acceleration thanks to supply bottlenecks and excess demand especially in the US. The Fed’s pivot on inflation has ended the debate regarding being “behind the curve”. According to the “dot plot” the Fed is now above the market in term of rate hikes priced in. Despite the fact the inflation is still seen as an essentially transient phenomenon by Central Banks, the risk of de-anchoring inflation expectations has triggered them in action. Not only the Fed but also the BoE and other Central Banks have steered the wheel of monetary policy towards a less accomodative stance to restore neutrality more quickly than previously anticipated. The most important bet for next year is the forecast that inflation will go down without the need for Central Banks to restrain growth in an abrupt way.

34

Markets still price the current inflation spike as

transitory…

10Y inflation breakevens

The spike in the 10-year Bei has

been staggering both in the US

and in the Eurozone reaching

multi-year highs.

Most of the surge in the US is

due to a repricing of the short-

term dynamics of inflation

leaving the long-end nearly

untouched.

USD swap forward 1y-inflation EUR swap forward 1y-inflation

Source: Bloomberg, Intesa Sanpaolo35

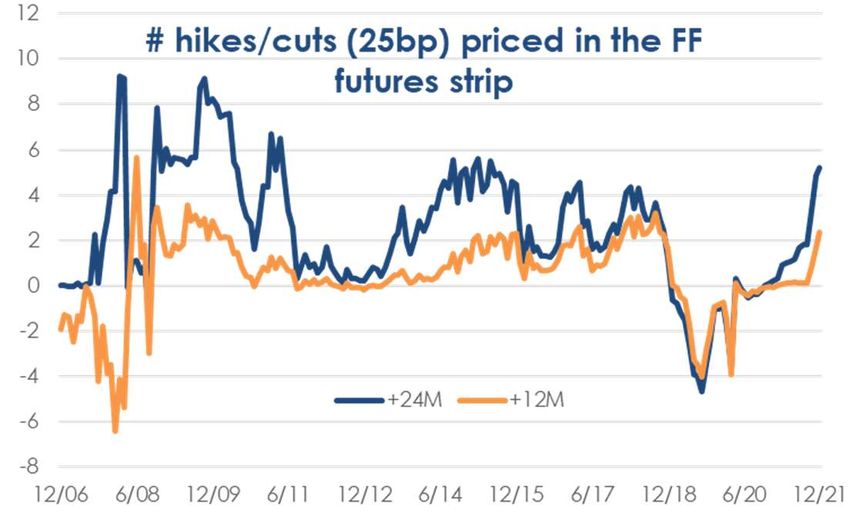

… but sticky enough to call for a policy response

The Fed after month reiterating the view of the transitory

nature of the recent spike in inflation, has had its Chairman

openly abandoning the “transitory” terminology in favour of a

much more hawkish wording.

The risk that current inflation could de-anchor long term

inflation expectations has pushed other Central Banks around

the world on the same path.

BoC, BoE, Fed, RBNZ, Norges, Riksbank and other CB have

clearly shifted their policy emphasis towards the risk of inflation.

Markets are pricing in future hikes36

Real yields have not participated in this year sell-off

of nominal rates

Despite the strong rebound in activity real yields have not shown

signs of rebound yet.

Long-term real yields are still nearby the historical low (US) or

marking new ones (Germany) prolonging the long term downward

trend for this variable.

Real yields are at ultra-low levels

Source: Bloomberg, Intesa Sanpaolo37

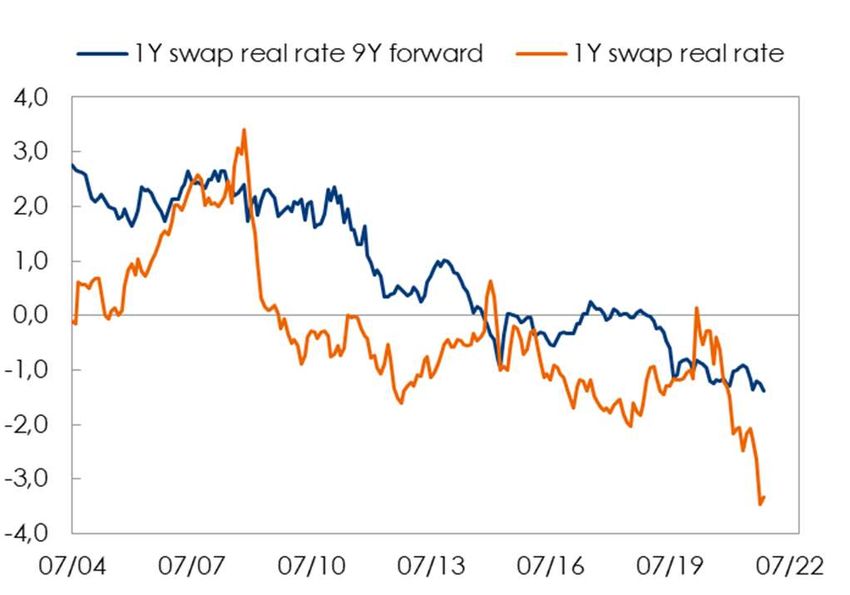

Forward real rates are at very low levels also at the

long-end

The fundamental reason for this behavior must be ascribed not

only to the ultra-accommodative stance of monetary policies but

also to the fall of the long-term natural rate.

EUR swap real rates (%) USD swap real rates (%)

Source: Bloomberg, Intesa Sanpaolo38

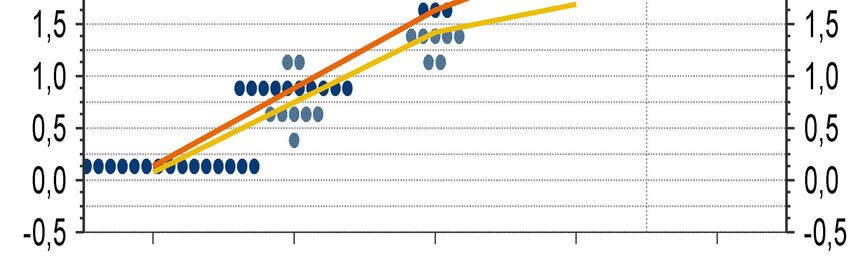

Fed’s path to “neutrality” will be short …

When the Fed will start raising

rates next year the The Fed aims at «normallizing» policy

unemployment rate will have

already reached levels

compatible with price stability

while the inflation rate will still be

well above the target.

Barring further shocks, the Fed

will raise rates just to implement a

less accommodative policy and

be better positioned to restore

neutrality.

However the neutrality will be

reached before the 2.5% set by

the “median dot” in Fed’s long-

term forecast.

Source: Bloomberg, Intesa Sanpaolo39

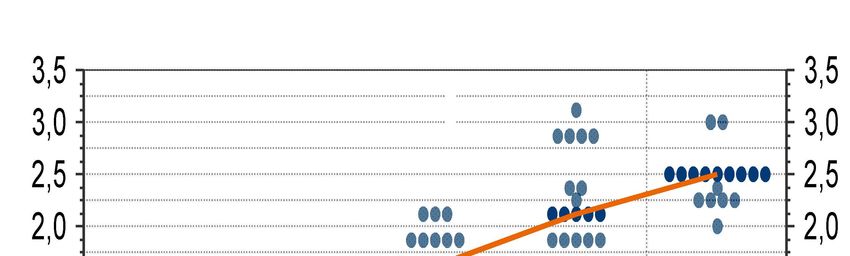

… and entail a gradual flattening impulse to the UST

curve

Compared to the last

tightening cycle the next one

will likely be shorter.

In fact, the terminal point

should reveal (once again)

lower than previous ones.

The hiking pace should not

exceed three hikes a year on

average while budget

normalization will take years

and be lived as a non-event.

These assumptions entail a

very gradual flattening bias to

the UST curve.

Source: Bloomberg, Intesa Sanpaolo40

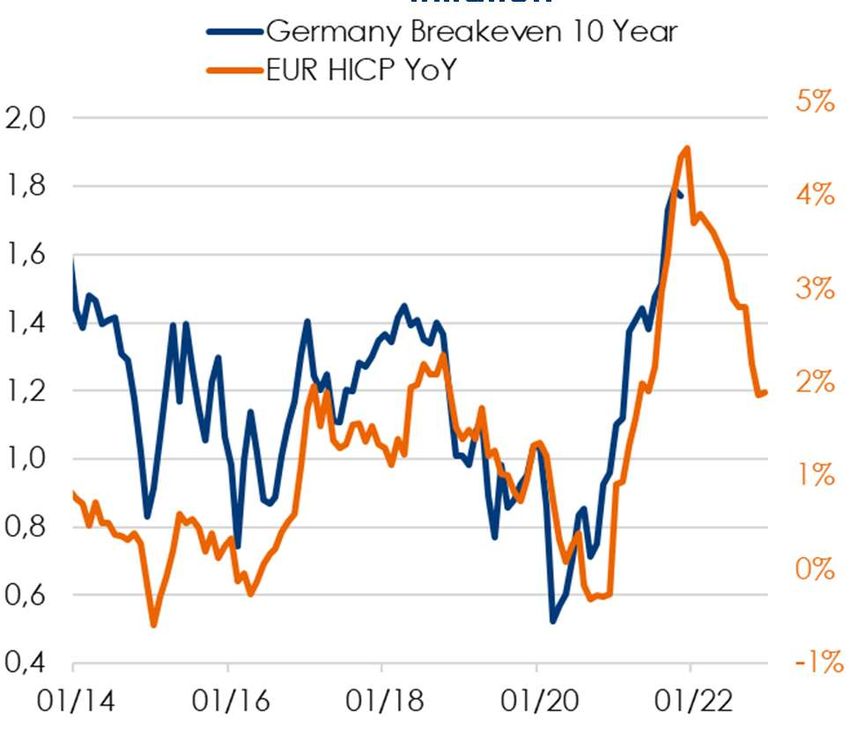

Current inflation close to the local peak

In the second half of 2022, total inflation is expected to near the 2%

objective.

We retain a negative bias on market measures of inflation as beta

between BEIs and actual inflation is high.

US TIPS inflation breakeven and inflation DBRei inflation breakeven and Eurozone

inflation

Source: Bloomberg, Intesa Sanpaolo41

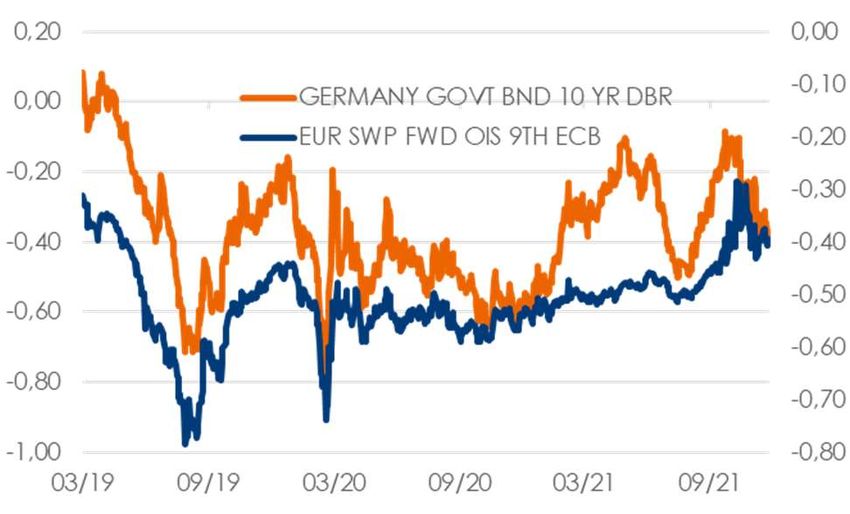

The market is betting on a premature hike from the ECB

3M Euribor future rates (%)

The market has priced in a first

hike few months after the closing

of the PEPP in March 2022.

We are skeptical that this will be

the case. There are few chances

for the ECB to raise rates before

the second half of 2023.

While the current inflation shock

will be dissipated the ECB will face

again a disinflationary

10Y Bund & EUR OIS (%)

environment that will challange its

statutory objectives.

The German sovereign curve

should marginally steepen in a

scenario of no-imminent rise in

policy rates and of gradual

increase in same duration UST.

Source: Bloomberg, Intesa Sanpaolo42

ECB purchases under our baseline scenario including

a first rate hike in Sep’23

ECB monthly purchases under APP and EGB net and gross issuance net official

PEPP (EUR Mln) purchases (ISP forecasts, EUR Bn)

APP Monthly net purchases 2021 2022 2023

PEPP Monthly net purchases

Bond

180,000 redemptions 658 733 717

160,000

Deficit 768 501 360

140,000

RRF loans 18 24 26

120,000

100,000 Net Issuance 542 430 317

80,000

Gross Issuance 1194 1163 1034

60,000

ECB net

40,000 purchases 716 368 55

20,000 Net supply net

QE -179 62 262

0

ITALY Net

-16 2 48

12/20

12/21

12/22

12/23

3/20

6/20

9/20

3/21

6/21

9/21

3/22

6/22

9/22

3/23

6/23

9/23

supply net QE

EU gross

issuance 140 95 105

Source: Bloomberg, Intesa Sanpaolo

Note: RRF grants are not considered a funding source as directly

included in the budget as a revenues.EGB: the ECB has shielded the peripheral market

43

from the crisis

The end of the ECB purchasing programmes will leave peripheral

debtors at the mercy of financial markets.

The sustainability of the Italian debt is at risk without a substantial

correction of fiscal structural balances.

Source: Datastream, Intesa Sanpaolo44

The Italian debt will remain on the border of the

Investment Grade region

The improvement in Italy

short-term growth prospect

brought about by the NGEU

IG threshold

will not affect its long-term

growth potential upon which

the credit rating is based on.

Spain and Portugal appear

better positioned to benefit

from the improvement in

structural fiscal balances.

The reinvestment policy of

the ECB will represent a

stabilizing factor for all

peripheral but it is unlikely that

will avoid a measured

widening of the BTP-Bund

spreads.45

Government yield forecasts

US Treasury Bund

13/12/21 03/22 06/22 09/22 12/22 13/12/21 03/22 06/22 09/22 12/22

2Y Forecast 0.65 0.80 0.90 1.00 1.10 2Y Forecast -0.68 -0.60 -0.60 -0.50 -0.40

Forward 0.86 1.03 1.18 1.32 Forward -0.70 -0.71 -0.71 -0.73

5Y Forecast 1.23 1.40 1.50 1.60 1.60 5Y Forecast -0.59 -0.46 -0.40 -0.30 -0.20

Forward 1.32 1.40 1.47 1.54 Forward -0.57 -0.55 -0.54 -0.53

10Y Forecast 1.43 1.70 1.70 1.80 1.80 10Y Forecast -0.36 -0.20 -0.10 0.00 0.10

Forward 1.50 1.56 1.61 1.66 Forward -0.33 -0.30 -0.28 -0.27

30Y Forecast 1.82 2.00 2.00 2.10 2.00 30Y Forecast -0.06 0.20 0.28 0.40 0.40

Forward 1.84 1.86 1.88 1.89 Forward -0.06 -0.06 -0.05 -0.04

Slope Slope

2/10Y 78 90 80 80 70 2/10Y 32 40 50 50 50

Forward 65 53 43 34 Forward 38 40 43 46

2/5Y 58 60 60 60 50 2/5Y 10 14 20 20 20

Forward 46 37 29 22 Forward 13 15 17 20

10/30Y 38 34 31 27 23 10/30Y 30 40 38 35 32

Forward 34 30 27 23 Forward 26 25 23 23

US Treasury-Bund

Spread OAT-Bund Spread

14/12/21 03/22 06/22 09/22 12/22 14/12/21 03/22 06/22 09/22 12/22

2Y 133 140 150 150 150 2Y 3 5 5 10 10

5Y 181 186 190 190 180 5Y 20 18 23 25 25

10Y 180 190 180 180 170 10Y 35 30 40 40 40

30Y 188 180 172 170 160 30Y 69 65 75 65 65

BTP-Bund Spread Bonos-Bund Spread

14/12/21 03/22 06/22 09/22 12/22 14/12/21 03/22 06/22 09/22 12/22

2Y 42 50 50 40 40 2Y 13 20 20 10 10

5Y 76 90 105 110 110 5Y 29 30 40 35 35

10Y 128 130 140 140 140 10Y 69 70 70 60 60

30Y 180 180 185 185 185 30Y 116 110 105 95 95

Source: Bloomberg, Intesa SanpaoloImportanti comunicazioni

Certificazione degli analisti

Gli analisti finanziari che hanno predisposto la presente ricerca, i cui nomi e ruoli sono riportati nella prima pagina del documento dichiarano che:

(1) Le opinioni espresse sulle società citate nel documento riflettono accuratamente l’opinione personale, indipendente, equa ed equilibrata degli analisti;

(2) Non è stato e non verrà ricevuto alcun compenso diretto o indiretto in cambio delle opinioni espresse.

Comunicazioni specifiche

Gli analisti citati non ricevono, stipendi o qualsiasi altra forma di compensazione basata su specifiche operazioni di investment banking.

Comunicazioni importanti

Il presente documento è stato preparato da Intesa Sanpaolo S.p.A. e distribuito da Intesa Sanpaolo SpA-London Branch (membro del London Stock Exchange) e

da Intesa Sanpaolo IMI Securities Corp (membro del NYSE e del FINRA). Intesa Sanpaolo S.p.A. si assume la piena responsabilità dei contenuti del documento.

Inoltre, Intesa Sanpaolo S.p.A. si riserva il diritto di distribuire il presente documento ai propri clienti. Intesa Sanpaolo S.p.A. è una banca autorizzata dalla Banca

d’Italia ed è regolata dall’FCA per lo svolgimento dell’attività di investimento nel Regno Unito e dalla SEC per lo svolgimento dell’attività di investimento negli Stati

Uniti.

Le opinioni e stime contenute nel presente documento sono formulate con esclusivo riferimento alla data di redazione del documento e potranno essere oggetto

di qualsiasi modifica senza alcun obbligo di comunicare tali modifiche a coloro ai quali tale documento sia stato in precedenza distribuito. Le informazioni e le

opinioni si basano su fonti ritenute affidabili, tuttavia nessuna dichiarazione o garanzia è fornita relativamente all’accuratezza o correttezza delle stesse.

Le performance passate non costituiscono garanzia di risultati futuri.

Gli investimenti e le strategie discusse nel presente documento potrebbero non essere adatte a tutti gli investitori. In caso di dubbi, suggeriamo di consultare il

proprio consulente d’investimento.

Lo scopo del presente documento è esclusivamente informativo. In particolare, il presente documento non è, né intende costituire, né potrà essere interpretato,

come un documento d’offerta di vendita o sottoscrizione di alcun tipo di strumento finanziario. Inoltre, non deve sostituire il giudizio proprio di chi lo riceve.

Intesa Sanpaolo S.p.A. non assume alcun tipo di responsabilità derivante da danni diretti, conseguenti o indiretti determinati dall’utilizzo del materiale contenuto

nel presente documento.

Il presente documento potrà essere riprodotto o pubblicato esclusivamente con il nome di Intesa Sanpaolo S.p.A..

Il presente documento è stato preparato e pubblicato esclusivamente per, ed è destinato all'uso esclusivamente da parte di, Controparti Qualificate / Clienti

Professionali, ad eccezione dei clienti professionali su richiesta, così come definiti dalla Direttiva MiFID II o eventualmente da parte di operatori dei Mercati o

Investitori Istituzionali, che sono finanziariamente sofisticati ed in grado di valutare autonomamente i rischi di invest imento, sia in generale sia in

relazione a particolari operazioni e strategie di investimento.

Tale documento, pertanto, potrebbe non essere adatto a tutti gli investitori e i destinatari sono invitati a chiedere il parere del proprio consulente finanziario per

qualsiasi necessità di chiarimento circa il loro contenuto.

Per i soggetti residenti nel Regno Unito: il presente documento non potrà essere distribuito, consegnato o trasmesso nel Regno Unito a nessuno dei soggetti

rientranti nella definizione di “private customers” così come definiti dalla disciplina dell’FCA.

Per i soggetti di diritto statunitense: il presente documento può essere distribuito negli Stati Uniti solo ai soggetti definiti ‘Major US Institutional Investors’ come definiti

dalla SEC Rule 15a-6. Per effettuare operazioni mobiliari relative a qualsiasi titolo menzionato nel presente documento è necessario contattare Intesa Sanpaolo IMI

Securities Corp. negli Stati Uniti (vedi sotto il dettaglio dei contatti).

Intesa Sanpaolo S.p.A. pubblica e distribuisce ricerca ai soggetti definiti ‘Major US Institutional Investors’ negli Stati Uniti solo attraverso Intesa Sanpaolo IMI Securities

Corp., 1 William Street, New York, NY 10004, USA, Tel: (1) 212 326 1199.

Incentivi relativi alla ricerca

Ai sensi di quanto previsto dalla Direttiva Delegata 593/17 UE, il presente documento è classificabile quale incentivo non monetario di minore entità in quanto:

− contiene analisi macroeconomiche (c.d. Macroeconomic Research) o è relativo a Fixed Income, Currencies and Commodities (c.d. FICC Research) ed è reso

liberamente disponibile al pubblico indistinto tramite il sito web della Banca - Q&A on Investor Protection topics - ESMA 35-43-349, Question 8 e 9.Metodologia di distribuzione Il presente documento è per esclusivo uso del soggetto che lo riceve da Intesa Sanpaolo e non potrà essere riprodotto, ridistribuito, direttamente o indirettamente, a terzi o pubblicato, in tutto o in parte, per qualsiasi motivo, senza il preventivo consenso espresso da parte di Intesa Sanpaolo. Il copyright ed ogni diritto di proprietà intellettuale sui dati, informazioni, opinioni e valutazioni di cui alla presente scheda informativa è di esclusiva pertinenza del Gruppo Bancario Intesa Sanpaolo, salvo diversamente indicato. Tali dati, informazioni, opinioni e valutazioni non possono essere oggetto di ulteriore distribuzione ovvero riproduzione, in qualsiasi forma e secondo qualsiasi tecnica ed anche parzialmente, se non con espresso consenso per iscritto da parte di Intesa Sanpaolo. Chi riceve il presente documento è obbligato a uniformarsi alle indicazioni sopra riportate. Metodologia di valutazione Le Trading Ideas si basano sulle aspettative del mercato, il posizionamento degli investitori e gli aspetti tecnico-quantitativi o qualitativi. Tengono conto degli eventi macro e di mercato chiave e di quanto tali eventi siano già scontati dai rendimenti e/o dagli spread di mercato. Si basano inoltre su eventi che potrebbero influenzare l’andamento del mercato in termini di rendimenti e/o spread nel breve-medio periodo. Le Trading Ideas vengono sviluppate su mercati cash o derivati di credito e indicano un target preciso, un range di rendimento o uno spread di rendimento tra diverse curve di mercato o diverse scadenze sulla stessa curva. Le valutazioni relative sono realizzate in termini di rendimento, asset swap spread o benchmark spread. Coperture e frequenza dei documenti di ricerca Le trading ideas di Intesa Sanpaolo S.p.A. sono sviluppate sia in un orizzonte temporale di breve periodo (il giorno corrente o i giorni successivi) sia in un orizzonte temporale compreso tra una settimana e tre mesi, in relazione con qualsiasi evento eccezionale che possa influenzare le operazioni dell’emittente. Comunicazione dei potenziali conflitti di interesse Intesa Sanpaolo S.p.A. e le altre società del Gruppo Bancario Intesa Sanpaolo (di seguito anche solo “Gruppo Bancario Intesa Sanpaolo”) si sono dotate del “Modello di organizzazione, gestione e controllo ai sensi del Decreto Legislativo 8 giugno 2001, n. 231” (disponibile sul sito internet di Intesa Sanpaolo, all’indirizzo: https://group.intesasanpaolo.com/it/governance/dlgs-231-2001) che, in conformità alle normative italiane vigenti ed alle migliori pratiche internazionali, include, tra le altre, misure organizzative e procedurali per la gestione delle informazioni privilegiate e dei conflitti di interesse, ivi compresi adeguati meccanismi di separatezza organizzativa, noti come Barriere informative, atti a prevenire un utilizzo illecito di dette informazioni nonché a evitare che gli eventuali conflitti di interesse che possono insorgere, vista la vasta gamma di attività svolte dal Gruppo Bancario Intesa Sanpaolo, incidano negativamente sugli interessi della clientela. In particolare, l’esplicitazione degli interessi e le misure poste in essere per la gestione dei conflitti di interesse – facendo riferimento a quanto prescritto dagli articoli 5 e 6 del Regolamento Delegato (UE) 2016/958 della Commissione, del 9 marzo 2016, che integra il Regolamento (UE) n. 596/2014 del Parlamento europeo e del Consiglio per quanto riguarda le norme tecniche di regolamentazione sulle disposizioni tecniche per la corretta presentazione delle raccomandazioni in materia di investimenti o altre informazioni che raccomandano o consigliano una strategia di investimento e per la comunicazione di interessi particolari o la segnalazione di conflitti di interesse e successive modifiche ed integrazioni, dal FINRA Rule 2241, così come dal FCA Conduct of Business Sourcebook regole COBS 12.4 – tra il Gruppo Bancario Intesa Sanpaolo e gli Emittenti di strumenti finanziari, e le loro società del gruppo, nelle raccomandazioni prodotte dagli analisti di Intesa Sanpaolo S.p.A. sono disponibili nelle “Regole per Studi e Ricerche” e nell'estratto del “Modello aziendale per la gestione delle informazioni privilegiate e dei conflitti di interesse”, pubblicato sul sito internet di Intesa Sanpaolo S.p.A all’indirizzo https://group.intesasanpaolo.com/it/research/RegulatoryDisclosures. Tale documentazione è disponibile per il destinatario dello studio anche previa richiesta scritta al Servizio Conflitti di interesse, Informazioni privilegiate ed altri presidi di Intesa Sanpaolo S.p.A., Via Hoepli, 10 – 20121 Milano – Italia. Inoltre, in conformità con i suddetti regolamenti, le disclosure sugli interessi e sui conflitti di interesse del Gruppo Bancario Intesa Sanpaolo sono disponibili all’indirizzo https://group.intesasanpaolo.com/it/research/RegulatoryDisclosures/archivio-dei-conflitti-di-interesse ed aggiornate almeno al giorno prima della data di pubblicazione del presente studio. Si evidenzia che le disclosure sono disponibili per il destinatario dello studio anche previa richiesta scritta a Intesa Sanpaolo S.p.A. – Macroeconomic Analysis, Via Romagnosi, 5 - 20121 Milano - Italia. Intesa Sanpaolo Spa agisce come market maker nei mercati all'ingrosso per i titoli di Stato dei principali Paesi europei e ricopre il ruolo di Specialista in Titoli di Stato, o similare, per i titoli emessi dalla Repubblica d'Italia, dalla Repubblica Federale di Germania, dalla Repubblica Ellenica, dal Meccanismo Europeo di Stabilità e dal Fondo Europeo di Stabilità Finanziaria.

Important Information

Analyst Certification

The financial analysts who prepared this report, and whose names and roles appear on the first page, certify that:

(1) The views expressed on companies mentioned herein accurately reflect independent, fair and balanced personal views;

(2) No direct or indirect compensation has been or will be received in exchange for any views expressed.

Specific disclosures

The analysts who prepared this report do not receive bonuses, salaries, or any other form of compensation that is based upon specific investment banking

transactions.

Important Disclosures

This research has been prepared by Intesa Sanpaolo S.p.A. and distributed by Intesa Sanpaolo SpA-London Branch (a member of the London Stock Exchange) and

Intesa Sanpaolo IMI Securities Corp (a member of the NYSE and FINRA). Intesa Sanpaolo S.p.A. accepts full responsibility for the contents of this report. Please also note

that Intesa Sanpaolo S.p.A. reserves the right to issue this document to its own clients. Intesa Sanpaolo S.p.A. is authorised by the Banca d'Italia and is regulated by the

FCA in the conduct of designated investment business in the UK and by the SEC for the conduct of US business.

Opinions and estimates in this research are as at the date of this material and are subject to change without notice to the recipient. Information and opinions have

been obtained from sources believed to be reliable, but no representation or warranty is made as to their accuracy or correctness.

Past performance is not a guarantee of future results.

The investments and strategies discussed in this research may not be suitable for all investors. If you are in any doubt you should consult your investment advisor.

This report has been prepared solely for information purposes and is not intended as an offer or solicitation with respect to the purchase or sale of any financial

products. It should not be regarded as a substitute for the exercise of the recipient’s own judgement.

No Intesa Sanpaolo S.p.A. entity accepts any liability whatsoever for any direct, consequential or indirect loss arising from any use of material contained in this report.

This document may only be reproduced or published with the name of Intesa Sanpaolo S.p.A..

This document has been prepared and issued for, and thereof is intended for use by, MiFID II eligible counterparties/professional clients (other than elective

professional clients) or otherwise by market professionals or institutional investors only, who are financially sophisticated and capable of evaluating investment risks

independently, both in general and with regard to particular transactions and investment strategies.

Therefore, such materials may not be suitable for all investors and recipients are urged to seek the advice of their independent financial advisor for any necessary

explanation of the contents thereof.

Person and residents in the UK: This document is not for distribution in the United Kingdom to persons who would be defined as private customers under rules of the

FCA.

US persons: This document is intended for distribution in the United States only to Major US Institutional Investors as defined in SEC Rule 15a-6. US Customers wishing to

effect a transaction should do so only by contacting a representative at Intesa Sanpaolo IMI Securities Corp. in the US (see contact details below).

Intesa Sanpaolo S.p.A. issues and circulates research to Major Institutional Investors in the USA only through Intesa Sanpaolo IMI Securities Corp., 1 William Street, New

York, NY 10004, USA, Tel: (1) 212 326 1199.

.Inducements in relation to research

Pursuant to the provisions of Delegated Directive (EU) 2017/593, this document can be qualified as an acceptable minor non-monetary benefit as it is:

- macro-economic analysis or Fixed Income, Currencies and Commodities material made openly available to the general public on the Bank’s website - Q&A on

Investor Protection topics - ESMA 35-43-349, Question 8 & 9.Method of distribution This document is for the exclusive use of the recipient with whom it is shared by Intesa Sanpaolo and may not be reproduced, redistributed, directly or indirectly, to third parties or published, in whole or in part, for any reason, without prior consent expressed by Intesa Sanpaolo. The copyright and all other intellectual property rights on the data, information, opinions and assessments referred to in this information document are the exclusive domain of the Intesa Sanpaolo banking group, unless otherwise indicated. Such data, information, opinions and assessments cannot be the subject of further distribution or reproduction in any form and using any technique, even partially, except with express written consent by Intesa Sanpaolo. Persons who receive this document are obliged to comply with the above indications. Valuation Methodology Trading Ideas are based on the market’s expectations, investors’ positioning and technical, quantitative or qualitative aspects. They take into account the key macro and market events and to what extent they have already been discounted in yields and/or market spreads. They are also based on events which are expected to affect the market trend in terms of yields and/or spreads in the short-medium term. The Trading Ideas may refer to both cash and derivative instruments and indicate a precise target or yield range or a yield spread between different market curves or different maturities on the same curve. The relative valuations may be in terms of yield, asset swap spreads or benchmark spreads. Coverage Policy And Frequency Of Research Reports Intesa Sanpaolo S.p.A. trading ideas are made in both a very short time horizon (the current day or subsequent days) or in a horizon ranging from one week to three months, in conjunction with any exceptional event that affects the issuer’s operations. Disclosure of potential conflicts of interest Intesa Sanpaolo S.p.A. and the other companies belonging to the Intesa Sanpaolo Banking Group (jointly also the “Intesa Sanpaolo Banking Group”) have adopted written guidelines “Organisational, management and control model” pursuant to Legislative Decree 8 June, 2001 no. 231 (available at the Intesa Sanpaolo website, webpage https://group.intesasanpaolo.com/en/governance/leg-decree-231-2001) setting forth practices and procedures, in accordance with applicable regulations by the competent Italian authorities and best international practice, including those known as Information Barriers, to restrict the flow of information, namely inside and/or confidential information, to prevent the misuse of such information and to prevent any conflicts of interest arising from the many activities of the Intesa Sanpaolo Banking Group which may adversely affect the interests of the customer in accordance with current regulations. In particular, the description of the measures taken to manage interest and conflicts of interest – related to Articles 5 and 6 of the Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No. 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest as subsequently amended and supplemented, the FINRA Rule 2241, as well as the FCA Conduct of Business Sourcebook rules COBS 12.4 - between the Intesa Sanpaolo Banking Group and issuers of financial instruments, and their group companies, and referred to in research products produced by analysts at Intesa Sanpaolo S.p.A. is available in the "Rules for Research " and in the extract of the "Corporate model on the management of inside information and conflicts of interest" published on the website of Intesa Sanpaolo S.p.A., webpage https://group.intesasanpaolo.com/en/research/RegulatoryDisclosures. This documentation is available to the recipient of this research upon making a written request to the Compliance Department, Intesa Sanpaolo S.p.A., Via Hoepli, 10 – 20121 Milan – Italy. Furthermore, in accordance with the aforesaid regulations, the disclosures of the Intesa Sanpaolo Banking Group’s interests and conflicts of interest are available through webpage https://group.intesasanpaolo.com/en/research/RegulatoryDisclosures/archive-of-intesa-sanpaolo-group-s-conflicts-of-interest. The conflicts of interest published on the internet site are updated to at least the day before the publishing date of this report. We highlight that disclosures are also available to the recipient of this report upon making a written request to Intesa Sanpaolo S.p.A. – Macroeconomic Analysis Via Romagnosi, 5 - 20121 Milan - Italy. Intesa Sanpaolo Spa acts as market maker in the wholesale markets for the government securities of the main European countries and also acts as Government Bond Specialist, or in comparable roles, for the government securities issued by the Republic of Italy, by the Federal Republic of Germany, by the Hellenic Republic, by the European Stability Mechanism and by the European Financial Stability Facility. A cura di/ Report prepared by : Sergio Capaldi, Macroeconomic Analysis, Intesa Sanpaolo Aniello Dell’Anno, Macroeconomic Analysis, Intesa Sanpaolo Luca Mezzomo, Macroeconomic Analysis, Intesa Sanpaolo Giovanna Mossetti, Macroeconomic Analysis, Intesa Sanpaolo Andrea Volpi, Macroeconomic Analysis, Intesa Sanpaolo

You can also read