POST-EARTHQUAKE PRICE DYNAMICS IN CHRISTCHURCH/CANTERBURY JUNE 2014

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

www.cdc.org.nz

POST-EARTHQUAKE PRICE DYNAMICS IN

CHRISTCHURCH/CANTERBURY

JUNE 2014

Prepared by: Steven Perdia and Amy McNaughton

PO Box 2962, Christchurch 8140 +64 3 379 5575

Level 1, 99 Cashel Street, Christchurch

Post-Earthquake Price Dynamics in Christchurch/Canterbury

The sections in this document are:

Executive Summary 3

Introduction 4

Methodology 6

Economic Context 8

Analysis and Commentary 9

Summary and Findings 12

Future Characteristics of the Greater Christchurch Economy 15

Appendix 1 16

Appendix 2 17

Appendix 3 18

Page | 2 of 18

Post-Earthquake Price Dynamics in Christchurch/Canterbury

EXECUTIVE SUMMARY

It is recognised that some prices have noticeably changed at a local level, compared with national

averages, as a result of recovery and rebuild activity. These prices are wages in some sectors, average

house and rental prices, costs of production for business, hospitality and local retail.

This paper examines and forecasts pricing patterns in greater Christchurch using Canterbury

Development Corporation (CDC) statistical research and a workshop process with external

stakeholders.

Prices in the local economy subject to change will continue to do so during the rebuild process and in

particular will be time locked to three future points over the next six years:

The insurance funded rental market slows as claims are settled by insurers

A period of economic easing where the city is fully resourced for the peak of its rebuild activities

The rebuild economy dissipates and reattaches with the underlying economy

Understanding the position of the underlying economy will become more important as the rebuild moves

through its cycle. Estimating the value of the underlying economy and its growth rate will be critical in

monitoring its health and when the rebuild economy is mostly complete.

Following on from this research it is recommended a sensitivity analysis be completed to determine the

effect of changes under conditions such as timing of insurance settlement claims. It is also

recommended that the findings be tested with other groups before being used to inform work streams

to reduce risk for business and government.

Page | 3 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

INTRODUCTION

Dynamic economic conditions are already present in the Canterbury economy. The leading driver of this

dynamism, the rebuild, still has some way to go. Several years prior to the earthquakes Canterbury had

started to decouple from Wellington and Auckland in broad Consumers Price Index (CPI) measures

which might be because it was later than other regions to exhibit the effects of the Global Financial

Crisis (GFC). However, the margin has amplified post-quake signalling rebuild related price inflation in

the region.

CPI Regional Broad Region - Broad Groups

Source: Statistics New Zealand

1250

1200

1150

1100

1050

1000

950

900

Auckland Wellington Canterbury

Not all local prices will be impacted during the rebuild. Some prices will be pegged to national settings

such as government wages, tobacco and petrol. It is more likely we will see movement in prices that are

determined by local factors and are unregulated (such as a local retail shop).

The table below shows CPI price change from 2006 to 2014 across three cities; Auckland, Wellington

and Christchurch. It provides an indication of which prices are likely to be more susceptible to local

drivers and those which are pegged to national prices as indicated by the degree of change relative to

the other cities.

Where the price change is similar across all three cities we assume that price is nationally influenced,

such as alcohol. Where price change is variable between cities, such as clothing and footwear, we

assume local conditions are affecting price.

Page | 4 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

CPI Change For June 2006 To March 2014 Auckland Wellington Christchurch

Food 26% 29% 29%

Alcoholic Beverages and Tobacco 41% 40% 42%

Clothing and Footwear -4% -1% 3%

Housing and Household Utilities 30% 26% 39%

Household Contents and Services -9% 5% 6%

Health 22% 27% 25%

Transport 15% 19% 19%

Recreation and Culture -3% -4% -3%

Miscellaneous Goods and Services 21% 22% 24%

Source: Statistics New Zealand and CDC.

The data in the table above highlights price change in housing, clothing and footwear retail, housing and

household utilities, housing services and health services.

Anecdotal commentary from business suggests change in wages, insurance and business rents.

CDC hosted a stakeholder workshop where this information was discussed, along with other statistics,

with the intent of coming to a common agreement on which prices are changing rapidly and what is likely

to happen to prices in the region over the coming years.

The purpose of this paper is to synthesise the data with trends and commentary from the stakeholder

group discussion and present a position on price dynamics in Christchurch/Canterbury that can be used

to identify issues and opportunities and mitigate business and government risk associated with rapidly

changing prices.

Page | 5 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

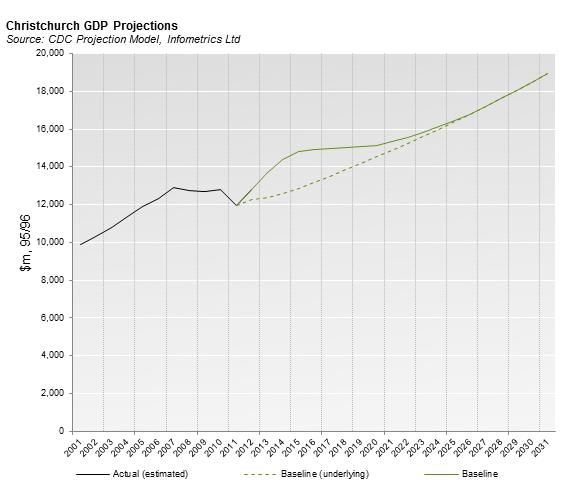

METHODOLOGY

CDC used a stakeholder workshop framework. Participants discussed drivers of price change and their

inter-relationships across the economy. A matrix of time verses activity in areas of the economy was

used as a platform for discussing changing prices over time.

The ‘time’ series was divided into phases. It started with the earthquakes and rebuild moving into phases

that were expected to occur over the coming years. These are described using the CDC GDP forecast

graph below:

$m, 95/96

The ‘areas’ of the economy were arranged into groups with similar characteristics. These are

described in the box below:

Area Description

Individuals Represents a single person or family

Business All business regardless of size or turnover

Macro City/Region and Civic Macroeconomic activity such as labour which cannot be attributed to

a single economic activity, regional affects and activities related to

local government

Page | 6 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

National Economy Macroeconomic activity which cannot be identified to a single

economic activity which is constrained to New Zealand

International How the City/region is perceived as a destination for business,

travel, migration and investment

It was recognised during the process that individuals and families can be affected in different ways, for

example retired people will be affected in a different way to increasing house prices than a beneficiary

in that a retired person may more likely to stay near family where a beneficiary may be more mobile.

Workgroups were asked to complete a matrix identifying, discussing and mapping drivers of price

change in ‘areas’ of the economy over ‘time periods’.

The full group then compared and discussed their team results towards a general consensus. The final

report is a combination of the workshop findings with CDC forecasts, data and anecdotal commentary

from business.

Page | 7 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

ECONOMIC CONTEXT

It was expected that following the rebuild boom

there would be a period of economic easing

before GDP recoupled with the underlying

economy. This has been detailed in CDC’s GDP

modelling for the Christchurch Economic

Development Strategy 2013 (refer to

‘Background Paper to the Christchurch Economic

Development Strategy’ at www.cdc.org.nz).

A conversion of the GDP projections into growth

rates highlights the city scaling up for the rebuild,

a period of easing (required scale reached)

followed by a gradual return to normal economic

activity. A projection of the underlying economy

was added from CDC modelling.

The growth rate forecast has been cross

referenced with other rebuild variables to assess

its timing validity. This includes private insurers’

forecasts, public sector works programmes, EQC

timetables and the infrastructure rebuild

programme. The variables largely align.

The growth rate peaked at 9 percent for

Christchurch City and although still strong, the

growth rate has been declining. GDP growth has

tracked almost identical to an exponential forecast

from September 2013 (immediate right). Linear

and other polynomial extrapolations were trialled

however the exponential curve was the best fit with

the trending data.

Based on these observations the economic growth

rate is forecast to be less than 2 percent in

Christchurch by 2017. Economic easing from end-

2016 is expected to last for three to four years and will see GDP growth between 0.5-2.0 percent.

Page | 8 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

ANALYSIS AND COMMENTARY

The products and services most affected by changes in the economy at a local level are:

Wages in manufacturing, construction sectors

Housing

Rental accommodation

Cost of production for business (combination of rents, insurance)

Hospitality and local retail

WAGES

i. A high GDP growth rate is driving low unemployment

ii. Low unemployment is currently putting upwards pressure on wages

iii. Wages that are most impacted are in construction related fields, but also manufacturers who

may be trying to reduce job-hopping

iv. Wages pegged to national rates such as local government, health and education may have

some room for movement but it will be minimal and with a longer lag time

v. During the period of economic easing it is likely that inflated wages, especially in construction

related fields, will have low growth rates allowing other wages to ‘catch up’

vi. In the future it is expected that greater Christchurch will be a higher wage economy, relative

to the national average, than it was pre-quake. Average wages will still be below the New

Zealand average but a narrower gap between them

Median Sale Price

HOUSING (monthly median sale price of dwellings in 000's)

Source: Real Estate Institute of New Zealand Inc, CDC

500

vii. Increases in the cost of building

450

new homes, and land prices, is

400

placing upwards pressure on 350

house prices in general 300

viii. However average house prices 250

have not grown at the same 200

pace as the rental market 150

100

ix. The gap is closing between

50

average house prices in 0

Jan 05

Jan 06

Jan 07

Jan 08

Jan 09

Jan 10

Jan 11

Jan 12

Jan 13

Jan 14

Christchurch and the national

Jul 05

Jul 06

Jul 07

Jul 08

Jul 09

Jul 10

Jul 11

Jul 12

Jul 13

average, but it’s not expected Christchurch New Zealand

to exceed the national average

for a sustained period

Page | 9 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

x. There is a large degree of urban sprawl occurring in the greater Christchurch area

xi. City house prices affect greater Christchurch housing prices, but a significant impact on

house prices outside of Christchurch is not expected

xii. It is expected that the pipeline of housing developments in the region will assist the supply

side of housing to ease some of the price pressure

xiii. Average house prices in Christchurch will re-couple with the New Zealand average soon

xiv. Any closing of the gap between the Christchurch average and the New Zealand average for

house prices will be lost in part during the period of economic easing between 2017 and

end-2018 where growth is forecast at about 1 percent. However house prices can be

downwards sticky and the easing period may be short enough that the price impact is very

minimal

xv. An expected future characteristic is a slightly higher average house price in relation to the

national average, but still below the national average

RENTAL ACCOMODATION

xvi. There are three key drivers of rapidly increasing rental accommodation prices:

Rental properties have been withdrawn from the market post-quake while a large

volume of short term accommodation is required to complete insurance funded

repairs and rebuilds

An insurance subsidised short term rental market

Migration and temporary workers seeking accommodation

xvii. Insurance funding for temporary rental accommodation is two to three times the norm

xviii. Rental accommodation decoupled from a history of being tightly correlated with the national

average (correlated at 0.96 for the six years pre-quake)

xix. Rental growth rates are now significantly higher than the growth rate for house prices

xx. As insurance repairs/rebuilds are settled and the need for insurance funded accommodation

comes to an end it is likely that the rental market will readjust down faster than it grew as it

is a competitive market (many players) and the purchaser is price sensitive

xxi. The need for insurance funded rental accommodation is likely to be of lower significance to

the market in 18-24 months. This is where rents will begin to move back towards normal

prices

xxii. Rental prices for houses are stereotypically a factor of return on investment against the value

of the house. In the six years prior to the quake the ratio of average rent to average house

price in Christchurch was correlated at over 0.8. Therefore, as average house price settles

it could be a good indicator of likely average rental price

xxiii. Net migration is currently well above historical rates

Page | 10 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

xxiv. We forecast net migration to slow in 24-36 months as the economy enters the period of

economic easing. This is coincidentally timed with the slowing of insurance funded rental

accommodation

xxv. Higher numbers of traditional city dwellers (such as workers and students) will explore

renting outside of Christchurch if prices are comparable, commuting is relatively straight

forward and services are accessible. This will be occurring now, but will change as rental

prices and availability eases within the city

xxvi. The most susceptible to a readjusting rental market will be motels (as high paying insurance

funded bookings stop) and landlords outside of the city as renters gravitate closer to services

and places of work/education as prices normalise

BUSINESS COSTS

xxvii. Business cost increases are mostly a function of higher rental prices, higher insurance costs

and wage pressure

xxviii. It is likely that business have adjusted to and absorbed fixed cost increases, for example

during the Global Financial Crisis (GFC) many businesses were able to absorb challenging

cost/revenue situations

xxix. Changes in internal cost structures for business will effect export competitiveness

xxx. In the longer term the region may see some mergers and acquisitions to re-establish margins

through economies of scale, but this will probably be in small numbers

xxxi. Business costs are also sensitive to the exchange rate, which is a dynamic condition and

will impact on the price of imported materials

HOSPITALITY AND LOCAL RETAIL

xxxii. Hospitality and local retail have some autonomy with price setting, being able to increase

prices without significant threat of switching and substitution. However they are subject to

strong market conditions and competition locally

xxxiii. Tourism visitor numbers saw a decline following the recession and earthquakes. As

consumers of hospitality and retail it contributed to a contraction in the number of businesses

and employees. Visitor numbers are currently recovering.

Page | 11 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

SUMMARY AND FINDINGS

Price uncertainty is a risk for both business and government in greater Christchurch.

CDC has gathered information and facilitated a stakeholder workshop to understand the likely price

impacts and patterns over time for the City/region and has identified that there will be a period of sudden

structural change to some prices again in the local economy.

We conclude that the likely areas of significant price change (both upwards and downwards) are wages

in some sectors, housing, rental accommodation, costs of production for business (wages, rent and

insurance), hospitality and local retail.

There will be three points in time where noticeable price change will occur in the aforementioned areas.

Those points are:

The insurance funded rental market slows as claims are settled by insurers and therefore

residential repairs and builds that have insurance funded accommodation nears completion

Economic easing in the economy as the city reaches the point where it has the resources it

requires to complete peak activity in the rebuild

The rebuild economy dissipates and the economy realigns with underlying growth and returns

to normal growth characteristic

Insurers have signalled that claims will be settled by mid-2015. This will result in the correction the two-

tiered rental market in Christchurch removing the over $1000 bracket that services short term insurance

funded accommodation whilst residential repairs and rebuilds are carried out. At the same time this

rental stock will be re-introduced into the normal rental market, easing prices with additional supply.

It is forecast that GDP growth from end-2016 to mid-2020 could be between 0.5 percent and 2 percent,

and below the national average. A challenge for investor and business confidence will be the misnomer

this conveys as it is only the rebuild economy which is slowing and contracting, the underlying economy

will continue to grow. CDC modelling suggests that the reason local GDP won’t fall into negative growth

during this period is because of the level of growth in the rest of the economy.

Page | 12 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

The table below outlines what indicators can be used to monitor the approach of these points in time:

Event When Effect Indicators

Residential builds and End-2016 to Reduction in demand for short- Residential insurance works

repairs that have insurance mid-2017 term rental properties from completion data

funded accommodation near insurers

completion MBIE average rental stats

Reduction in average price of

rental accommodation Advertised average price

Economic easing period End-2016 to GDP growth flattens (is below the GDP data

2020 national average)

(GDP growth 0.5% – 2%) Employment/unemployment

High demand for labour reduces

as economy reaches capacity for Ease of finding skilled and

rebuild activities unskilled labour

Wage pressure eases Migration data

Migration slows CDC underlying economy

modelling

Other price pressures ease such

as housing and rental price

Economy realigns with 2020-2021 GDP growth rate starts to GDP data

underlying Growth and recouple with national average

returns to normal growth House, rent prices

levels Employment grows

Sector wage rates

Certainty of new norms for wage,

house and rental prices identified CDC underlying economy

for region modelling

The key economic impacts for consideration based on the findings of this exercise are:

Continued modelling and understanding of the

underlying economy by CDC is a critical

activity. Although the growth rate is

approximated at 2 percent or below from late-

2016 to 2020 (see graph) the underlying

economy will be growing and creating

employment. The information can be used to

ensure change is understood and maintain

business and investor confidence during the

economic easing phase

There is potential for motels to be affected.

After a period of peaks the sector will return to

business as usual as insurance funded

Page | 13 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

accommodation comes to an end and the rental accommodation market returns to normal

conditions

During economic easing underlying growth will continue to employ labour, but there is a need

to support transition of labour from rebuild related work into other sectors such as Agriculture

and Manufacturing. This will ease pressure on unemployment and deal with a potential tail of

surplus migration

An oversupply of housing and rentals potentially leading to reducing values, but the period of

easing may be short enough that house prices don’t adjust significantly

Assumptions discussed during the stakeholder workshop were:

There is an optimism bias in business

Council rates increases capped at 6.8 percent

Rebuild timelines as at May 2014

Supply constraints do not change

That a significant number of rental bonds were re-lodged post-quake which has had an impact

on rental statistics

A recommended follow on activity from this report is a sensitivity analysis to test the impact of changes

to timeframes and changes to the above assumptions, such as dairy price fluctuations. It is also

recommended that the findings be tested with other groups before being used to inform work streams

to reduce risk for business and government.

Page | 14 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

FUTURE CHARACTERISTICS OF THE GREATER CHRISTCHURCH ECONOMY

The workshop group were asked to consider and discuss what the potential future characteristics of the

greater Christchurch economy might be. A summary of the points discussed are provided below:

Wage, house and rental accommodation prices will be below the nation average, however the

margin between them will be closer than pre-earthquake

The reported average rent will be higher in Christchurch because:

A significant amount of resubmitted bonds post-quake will generate an average rent that

is more representative of the current price

The rental price for new houses will likely be higher, affecting the average rent statistic

The ratio of landlords to property owners may be higher. This would likely result in a lower

turnover of property and less transactions, but a wider range of rental accommodation at

competitive pricing

The residential population outside of Christchurch City that use the City for services, work and

education will be higher

The timing of the Water Management Strategy and its impact on the Agriculture and

Manufacturing sectors is seen as an important employment transition opportunity

Sector structure will be slightly different. The rebuild is driving skilled labour growth in several

sectors. As a result Christchurch could have a higher wage economy than it was pre quake

as the mix of skilled and unskilled workers will be different

The Innovation and Technology sector will grow quickly over the next 10 years

A possibility that offshore investment will come later, rather than earlier, in the rebuild. This is

based on the premise that; offshore investors will need a higher degree of confidence than

local investors, offshore investors are seeking stronger signals on the progress of public sector

projects, offshore investors may follow successful local investment and, they will prefer

stability in local economy activity

Page | 15 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

APPENDIX 1

Workshop programme

Outline 15 mins Introductions

Current state of play and observations

Workshop process

Workshop 10 mins Timeframe Segments

Framework o Initial Response

o Start of Recovery

o Today

o Boom

o Easing

o Future Characteristics

Affected Groups

o Individuals (workers)

o Business

o International (investors/businesses)

o City/Region Civic related

o National economy

Workgroups 30 mins Workgroups are allocated parts of the matrix and their respective

timeframe/affected groups to complete a map of expected impacts

over time.

Presentations 30 mins Each group contributes to the master matrix to time, affected groups

and pricing impacts.

Discussion 45 mins After making final adjustments to the matrix a group discussion about

the cross cutting cause/effect relationships and points of interest.

Develop an understanding of how inflation may affect different groups,

in different ways at different times.

Discussion 20 mins A discussion about the future characteristics of the Christchurch

economy, will it be different or similar to pre-quake?

Page | 16 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

APPENDIX 2

Workshop attendees:

Canterbury Development Corporation

Members of Business Mentors

New Zealand Treasury

Canterbury Employers’ Chamber of Commerce

Inland Revenue Department

Ministry of Business, Innovation and Employment

Christchurch City Council

Page | 17 of 18Post-Earthquake Price Dynamics in Christchurch/Canterbury

APPENDIX 3

Time period descriptions

Period Description

Initial Response After the two major earthquakes

Start of Recovery The establishment and implementation of key rebuild activities such

as CERA and SCRIT and demolition was underway

Today Demolition is largely complete, plans are complete and starting to be

implemented

Boom Period A period of sustained growth and migration above the average

Economic Easing The rebuild spend is coming to an end and growth rates are equal to

or below the national average

Return to normal Growth Where growth rates and other economic indicators re-couple with

national averages

Future Characteristics Differences in the economic structure of Christchurch/Canterbury

compared with pre-quake

Economic area descriptions

Area Description

Individuals Represents a single person or family

Business All business regardless of size or turnover

Macro City/Region and Civic Macroeconomic activity such as labour which cannot be attributed to

a single economic activity, regional affects and activities related to

local government

National Economy Macroeconomic activity which cannot be identified to a single

economic activity which is constrained to New Zealand

International How the City/region is perceived as a destination for business,

travel, migration and investment

Page | 18 of 18You can also read