LONG - Team Members: Grace Ee Jordon Woon Sean Pan Serene Koh Justin Kuan - NTU-IIC

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

LONG

Current price: USD497.98

(as of 19 Jan 2021)

12-month price target:

USD600.00 (20.49% upside)

Team Members:

• Grace Ee

• Jordon Woon

• Sean Pan

• Serene Koh

• Justin Kuan

Company Overview

Business Description Key Historical Financials

36.90% 38.30%

• Founded in 1997, headquartered in Los Gatos, California 25000 40%

32.30% 35%

31.30%

• Provider of subscription streaming entertainment service 20000 29.10%

20156.4

30%

• Acquires, licenses and produces content, including original programing 15794.3

15000 25%

• Allows members to watch a variety of television (TV) series, 11692.7

20%

documentaries and feature films across a wide variety of genres and 8830.7

10000 15%

languages 6779.5

12.90% 10%

• Provides members the ability to receive streaming content through a host 5000 10.70%

of Internet-connected screens, including TVs, digital video players, 7.80% 5%

5.40% 5.00%

television set-top boxes, and mobile devices 0 0%

2015 2016 2017 2018 2019

• Has approximately 195 million paid members in 190 countries

Revenue (in Millions USD) Gross Margin EBITDA Margin

Product Offerings Geographical Presence

Basic Standard Premium

DVD By-Mail

Monthly cost* (United $8.99 $13.99 $17.99 Netflix Revenue Growth by Region

1 Membership Services

States Dollar)

3000

Number of screens you 1 2 4

can watch on at the 2500

same time 2000

1500

Production of Number of phones or 1 2 4

2 Content tablets you can

have downloads on

1000

500

0

Unlimited movies and TV ✓ ✓ ✓

shows Q1 - Q2 - Q3 - Q4 - Q1 - Q2 - Q3 - Q4 - Q1 - Q2 -

2018 2018 2018 2018 2019 2019 2019 2019 2020 2020

Streaming Content Watch on your laptop, ✓ ✓ ✓

3 Membership Services

TV, phone and tablet United States and Canada Europe, Middle East, and Africa

HD available ✓ ✓ Latin America Asia-Pacific

Ultra HD available ✓

Historical Share Price Performance

583.00

3 60.00mm As at 19 Jan 2021

533.00

50.00mm Share Price 497.98

483.00

40.00mm

Shares Outstanding 441.8M

433.00

1

Share Price

383.00

2 Market Capitalization 225.49B

30.00mm

333.00

Enterprise Value 233.15B

20.00mm

283.00

10.00mm

233.00 Stock Price History

Transaction Volume

183.00 0 52-week High 556.55

52-week Low 298.84

Netflix, Inc.Axis Title

(NasdaqGS:NFLX) - Volume

S/N Date Event Price (USD) EV/EBITDA P/E

1 Jul 24 2018 Netflix establishes its first European production hub in Madrid 357.32 111.15x 263.27x

Netflix reported results for 2019 Q3 – it beat on earnings but slightly missed analysts’

2 Oct 16 2019

expectations for revenue

286.28 47.09x 101.81x

3 Aug 26 2020 Tiktok reportedly approached Netflix in plan for Netflix to acquire its US operations 547.53 62.89x 132.39x

Industry Overview

Netflix’s Main Competitors Key Market Trends

Video-on-demand Subscribers Globally (in millions) • Growth in video-on-demand market size from USD

53.96 billion (2019) to USD 159.62 billion (2027)

30 • Estimated to exhibit a CAGR of 14.8%

30.4 • Rising adoption of mobile devices and smartphones

have led to expansion of customer base

• Improvement of user-experience of VOD due to

134 smartphone applications and high-speed Internet

150 • Growing penetration of 5G broadband influencing

growth of VOD market

195 • Potential deals with operators

North America to Lead Market Asia-Pacific is the highest growth region

North America • Presence of key market Asia-Pacific region is likely to expected to have the highest growth

Video on Demand players such as Netflix,

Market Size • Stricter lockdown

Amazon, Alphabet, HBO,

regulations

Roku etc.

• Change in

USD • Highest future CAGR demand on OTT

• Internet-based video platforms

19.7 services are growing • VOD providers

partnering with

segment, represent 63% of

billion total television revenues

• Massive growth opportunity

movie producers

to release movies

Overview of Investment Thesis

India's Golden Age of Streaming Services

Netflix’s full throttle on expansion Content is King with Japanese style animation, "anime".

Expansion to Africa

Varied Offerings to Reflect Diverse Global Perspectives

Netflix’s distinct competitive advantages Emphasis on Original Content Despite Pandemic Restrictions

cements its position as a market leader

High Quality and Quantity of Original Content

Highly Accurate Predictive Proprietary Algorithm

Renewed lockdown across Europe, Netflix’s greatest market

Short-term and long-term secular tailwinds

Uncertainty around the COVID-19 vaccine progress

intact

Rapid advent of 5G takes OTT media viewing to new heights

Thesis 1: Full Throttle on Expansion

India's Golden Age of Streaming Services

• Netflix spent $400 million in developing original content as well as

licensing other content for the Indian market between 2019 and 2020.

• Strategic alliance with Jio to give free mobile-only subscription to

postpaid plans starting at 199 rupees per month as well as free

subscription to basic plans for Jio’s fixed broadband service to cater to the

mass market of India.

• Industry revenues from streaming in India are set to jump from $500

million in 2018 to as much as $5 billion in 2023.

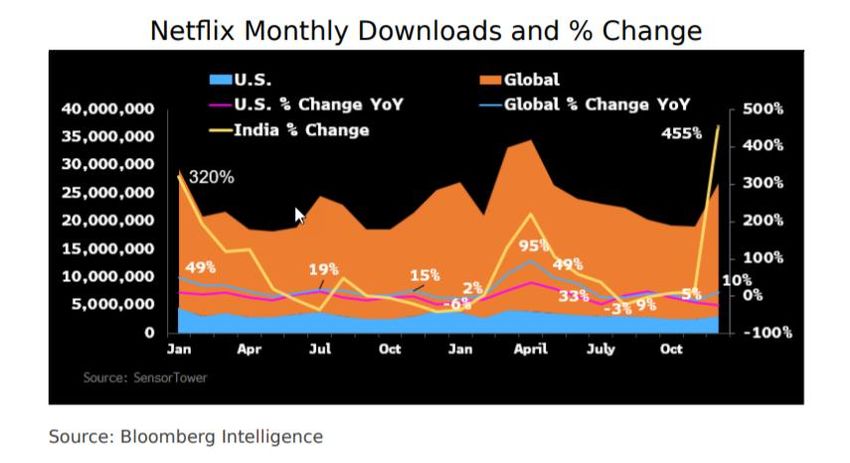

• India Stream Fest Brings 455% December Surge

• Content investments not fully portrayed in India. Increased original

content budget has yet to show up on the service.

• Licensing deals maturing in the near period.

• This framework suggests meaningful upside even relative to the post Q4

run up in the stock price. Netflix is likely to account for its undisclosed

potential upsides from the India market in the next two quarters.

Thesis 1: Full Throttle on Expansion

Content is King with Japanese style animation, "anime".

• Increased viewership of more than 50% on 2019.

• Anime titles appeared in top ten lists in almost 100 countries so

far this year.

• Netflix is exclusively streaming, producing, and making anime.

• Netflix aligns anime themes to the UCAN market, they tend to

choose fantasy, science fiction, violence.

• The popularity of "engineered" anime into Netflix

will potentially attract more subscribers in the UCAN, which

would increase Paid Net Additions.

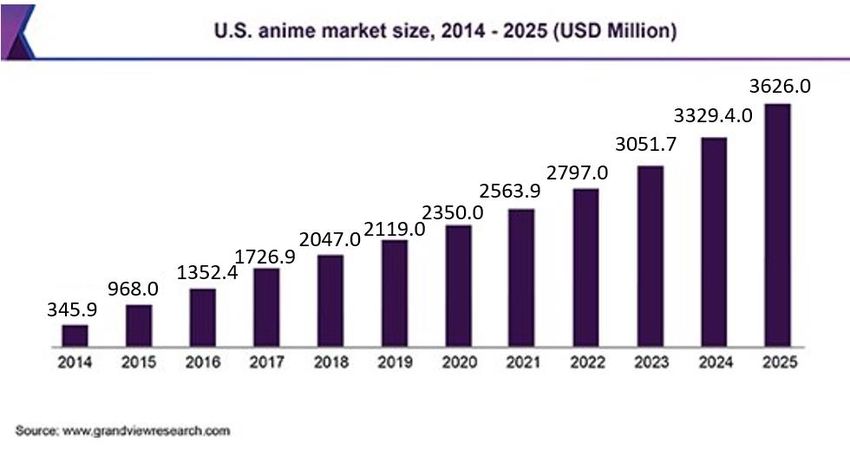

• This is accompanied by the global anime market is expected to

grow at a compound annual growth rate of 9.1% from 2020 to

2025 to reach USD 36.26 billion by 2025

Thesis 1: Full Throttle on Expansion

Expansion to Africa

• Expansion to Africa:

• Kenya's E&M market is set to see growth at a 10.3% CAGR over the next five years,

reaching nearly US$3.0 billion in 2023.

a. Empowering African content makers and creative to tell their stories

i. The narrative is shifted to a potential margin expansion with a heavy focus on

local content.

ii. Local content can account for over 90% of viewership for the mass market

segments.

iii. Has the power to influence cross-culturally

b. Strategic Alliance with Telecoms:

i. Overcome challenges including slow and expensive internet and the lack of

proper payments infrastructure in the 55-nation continent. (By add subscription

bills to post-paid sim cards, allow pre-downloaded streaming through wifi)

• Netflix is well positioned to capitalize on a rapidly changing global market where

demand for diverse content is greater than ever before.

• Abundance of a “Rich cultural bed” on the continent waiting to be explored

• Africa subscribers will be attracted by the flexibility and the content that Netflix is able

to provide. Similarly, global subscribers would have greater exposure to African content.

• The ramped up local content, alongside the strategic tie-ups with telecoms

in West Africa would likely persuade more Africans to partake in Netflix

Subscription services, which will in turn increase the Net Paid additions.

Thesis 2: Netflix Competitive Advantages

Varied Offerings to Reflect Diverse Global Perspectives

Region Shows Movies

• Netflix's content effectively reflects global perspectives United States 1326 4339

and stories. 63% of young people felt that its content American Samoa 1078 4573

more accurately reflects daily life compared to content Puerto Rico 1073 3807

Martinique 803 3736

from other streaming platforms French Guiana 803 3710

Guadeloupe 769 3731

• As Netflix expands internationally, it recognises an Aruba 712 3389

Benin (Dahomey) 462 3171

increasingly diverse global audience featuring a larger Montserrat 661 2967

range of races, ages, and sexual orientations British Virgin Islands 666 2940

Canada 629 2942

Brazil 562 2951

• Netflix also appeals to local viewers’ palettes by offering a

different list of shows to different viewers depending on

their geographical location, targeting demographics by

catering to local tastes and preferences

Sources: Comparitech, Investopedia, David Deal, Varsity, PC,

Deadline

Thesis 2: Netflix Competitive Advantages

Emphasis on Original Content Despite Pandemic Restrictions

• Netflix's growth can be attributed to its

commitment to the creation of original content known

as "Netflix Originals", spending over US$17 billion

in 2020. However, this proved to be challenging for

both Netflix and its rivals amidst the pandemic

• Despite this, Netflix’s originals roster has been

relatively unaffected by production shutdowns with 50

titles completed since the beginning of Covid-19.

• Netflix can carry on productions due to its set of

meticulously crafted safety protocols, especially for

intimate scenes, investing up to 20% more for

production costs to carry on production. While this

pushes production cost, the availability of new content

is believed to accelerate growth and retention of

subscribers

Sources: Varsity, Bloomberg, Hollywood Reporter, What’s on Netflix,

Financial TimesThesis 2: Netflix Competitive Advantages

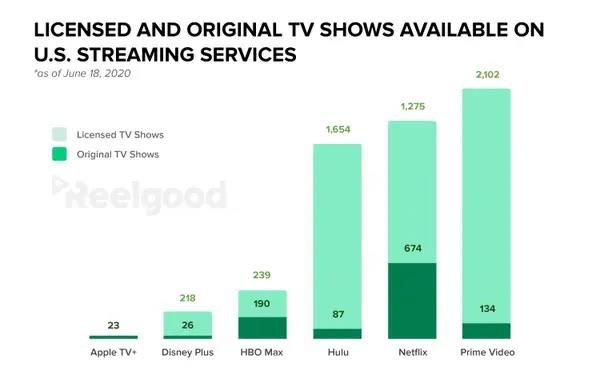

High Quality and Quantity of Original Content

• Netflix leads its rivals in original TV shows by a wide

margin in both quantity and quality. Netflix has 674

original TV shows, beating other major rivals like Hulu

(87) and Amazon Prime Video (134).

• This investment has also resulted in a transformation

from being a mere video streaming provider to the

premier content creator. Netflix has smashed past its

closest competitor, HBO, in terms of Emmy

Nominations in 2020 – picking up 160 compared to

HBO's 107

• Netflix has also dominated viewership from the

average person, producing 12 of the 30 most-watched

streaming video on demand (SVOD) released movies in

the U.S

Sources: Fortune, Deadline, Observer, Business Insider, ReelGoodThesis 2: Netflix Competitive Advantages

Highly Accurate Predictive Proprietary Algorithm

• Netflix uses machine learning and algorithms to help

break viewers’ preconceived notions and find shows

that they might not have initially chosen. To do this, it

looks at nuanced threads within the content, rather

than relying on broad genres to make its predictions,

distinguishing it from other streaming services

• Netflix's personalised recommendation engine

has been valued at over US$1 billion a year arising

from cost savings and customer retention, with a churn

rate of only 3.1%, the lowest amongst its major

competitors

• More than 80% of the TV shows people watch on

Netflix are discovered through the

platform’s recommendation system, further

demonstrating its accuracy in its predictive function.

Sources: Varsity, Business Insider, Bloomberg IntelligenceThesis 3: Short-term and Long-term Secular Tailwinds Intact

Renewed lockdowns in Europe suggests a possible replication of impressive historical streaming and subscription growth

• With new lockdowns re-imposed in Europe due to the spread of a new variant

of virus, this indicates a bullish outlook for Netflix in Q1 2021 given that it is a

market leader controlling over 53% of the SVOD market in Europe

• Impact of COVID-19 early 2020 has been strongly positive for SVOD demand,

with Netflix adding a record 37 million new subscribers during the year (31%

increase from 2019) despite a price hike of 29% introduced in Oct’20 →

similar growth witnessed in 2020 likely to continue in 2021

• While such growth also encompasses a pressing need for more exclusive

2019 Budgets / Releases By Studio ($M)

content to keep new subscribers satiated, Netflix already has 500+ titles

6,000 60

currently in post-production and has ambitious plans to release at least one 5,000

Netflix far surpasses its competitors

5,000 55 50

in producing more films

new original film every week in 2021

4,000 40

• Even in 2019, Netflix has been charging hard into original films, releasing 3,000 30

1,983

almost 2.5-3x the annual output of a major studio, with more than 55 2,000 20 20

17 17

1,041 890 15

movies. In 2020, Netflix has undoubtedly been more aggressive than ever, 1,000 10

773

9

750 625 606 9 10

taking advantage of the pandemic-induced movie-going standstill by buying - -

Netflix Disney Warner Universal Fox (20th Sony Lionsgate Paramount

multiple film titles Bros Century) Columbia

Estimated Studio Budget ($M) Number of Films

Sources: Bloomberg Intelligence, Netflix annual reportThesis 3: Short-term and Long-term Secular Tailwinds Intact

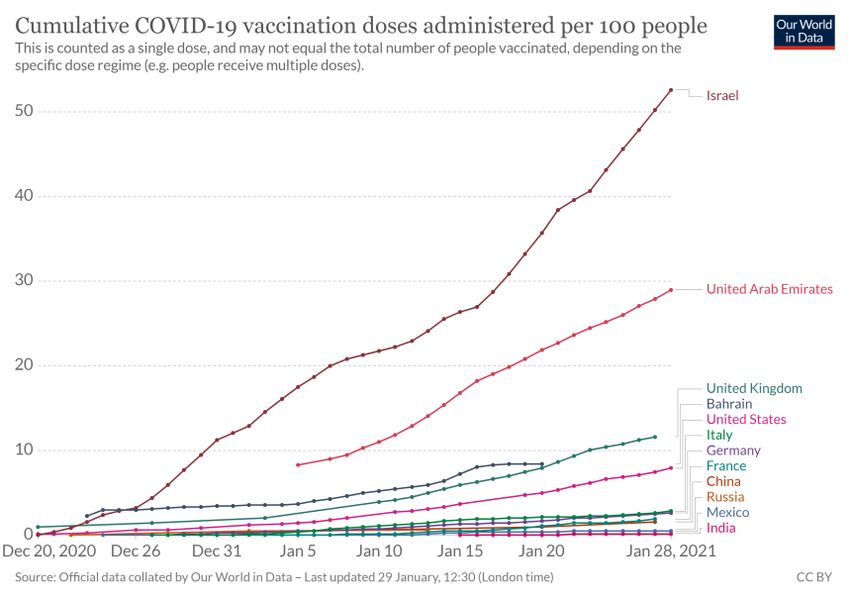

Uncertainty of vaccine progress adds to continued growth of subscribers

• New variants of COVID-19 from the UK that could possibly have a higher

death rate than the other variants, resulting in possible delay in vaccine

approval

• Lower efficacy rate of current COVID-19 vaccine towards newer strains

(Novavax vaccine: 95.6% for original variant vs 85.6% for new variant)

• Vaccine shortages, low willingness for vaccination amidst worries of

vaccine safety and efficacy against new variants could deter the rate at

which COVID-19 will be brought under control

• Increasing duration of lockdowns and prolonged work-from-home

arrangements

• With the probability of limited COVID-19 containment in 2021, this will

result in continued uptake of streaming services by customers, leading to

prolonged, optimistic revenue growth for Netflix as witnessed in 2020

Sources: Our World in Data, McKinseyThesis 3: Short-term and Long-term Secular Tailwinds Intact

Rapid advent of 5G takes OTT media viewing to new heights, benefitting Netflix as a key content provider

• Currently, 5G networks are still in their infancy and we believe that the rise 5G speeds far exceed 4G speeds

of 5G adoption will enable OTT platforms to draw in more viewers and get a

(for major network services providers)

Download Speed Comprison (in Mbps)

bigger slice of the pie 75.6

70 71

• With lower latency and 10x faster download speeds, 5G can transform the 67.1

53.3

user experience with VR and AR applications, powering seamless,

37.1

immersive experiences within subscribers’ favourite shows 32.5

36.3

• Apart from easing access to customers with a broadband connection, the

push for 5G could open up streaming options to at least 24 million

consumers who are not currently able to access high-quality streaming AT&T Sprint T-Mobile Verizon

services (Pew Centre, 2018) 5G Speed 4G Speed

• By utilising state-of-the-art technologies, such as VR and 8K, Netflix will be

able to offer a better-quality streaming service with increased content Increased 5G Partnerships Between

quality, improved customer satisfaction, allowing it to stay ahead in the Streaming Giants & Tech Players

streaming wars Emerging 5G adoption of content providers suggests how 5G

will likewise increasingly become a core focus for Netflix &

continue to expand its partnerships.Financial Analysis – Increasing Return on Equity

Return on Equity (%)

35.0%

Higher Return On Investor Equity YoY

29.5% 30.6% 30.1% 29.5%

29.1% 28.5%

30.0% 27.5%

• There has been an increasing return on

25.0%

17.9%

equity from FY16A to FY19A with ROE

20.0%

increasing at a decreasing rate.

15.0%

10.0% 7.6%

• While we note a trend of increasing net

5.0%

profit margin, there is a trend of

0.0%

FY16A FY17A FY18A FY19A FY20E FY21E FY22E FY23E FY24E decreasing asset turnover and hence the

increase in ROE is at a decreasing rate.

Historicals Projection

Financial Analysis FY16A FY17A FY18A FY19A FY20E FY21E FY22E FY23E FY24E • The decreasing asset turnover implies a

decreasing efficiency in the company’s

Dupont Analysis

assets to generate sales which could be

Gross Margin (%) 29.1% 31.3% 36.9% 38.3% 41.6% 43.3% 45.0% 46.8% 48.5%

reflective of the increasing competition in

Operating Margin (%) 4.3% 7.2% 10.2% 12.9% 14.6% 16.1% 18.1% 19.7% 21.4% the entertainment industry.

Net Profit Margin (%) 2.1% 4.8% 7.7% 9.3% 9.7% 10.7% 12.0% 12.9% 13.9%

Asset Turnover (x) 0.742x 0.717x 0.702x 0.672x 0.675x 0.668x 0.642x 0.604x 0.561x

Financial Leverage (x) 4.852x 5.206x 5.100x 4.676x 4.347x 4.141x 3.970x 3.854x 3.800x

Return on Equity (%) 7.6% 17.9% 27.5% 29.1% 28.5% 29.5% 30.6% 30.1% 29.5%Financial Analysis – Decreasing Liquidity Concerns but Increasing Solvency Concerns

Quick Ratio (x) Debt/Equity (x)

7.000x

Decreasing Liquidity Concerns

6.519x 2.500x

6.000x 2.350x

• Quick ratio has been increasing

2.188x

2.260x

from FY16A to FY19A which implies

4.789x 2.000x 2.128x

5.000x

1.978x 1.947x

2.046x Netflix’s increasing ability to pay off

1.814x

its short-term liabilities.

4.000x

3.421x

1.500x

3.000x • This means that Netflix has lower

2.240x chances of immediate default risk

1.255x

2.000x

1.418x 1.000x

concerns from not paying off its

1.000x 0.732x

short-term liabilities

0.516x 0.585x

0.320x

0.000x 0.500x

FY16A FY17A FY18A FY19A FY20E FY21E FY22E FY23E FY24E FY16A FY17A FY18A FY19A FY20E FY21E FY22E FY23E FY24E Increasing Solvency Concerns

Historicals Projection

• Debt/Equity ratio has been

Financial Analysis FY16A FY17A FY18A FY19A FY20E FY21E FY22E FY23E FY24E

increasing from FY16A to FY19A

Liquidity Indicators

which implies Netflix’s increasing

Current Ratio (x) 1.247x 1.403x 1.494x 0.901x 1.583x 2.472x 3.662x 5.065x 6.834x

risk of defaulting on its long-term

Quick Ratio (x) 0.320x 0.516x 0.585x 0.732x 1.418x 2.240x 3.421x 4.789x 6.519x

liabilities.

Solvency Indicators

Debt/Equity (x) 1.255x 1.814x 1.978x 1.947x 2.046x 2.128x 2.188x 2.260x 2.350xDiscounted Cash Flow – Target Price: $613.81

Revenue Drivers Historicals Projection

in thousands of USD FY15A FY16A FY17A FY18A FY19A FY20E FY21E FY22E FY23E FY24E

Revenue Growth

Revenue

• Three revenue streams up

Domestic Streaming Segment 4,180,339 5,077,307 6,153,025 7,646,647 9,243,005 11,676,425 14,846,115 18,211,878 22,664,882 27,434,714 till FY18A.

Dom Stream % YOY Growth 21.46% 21.19% 24.27% 20.88% 26.33% 27.15% 22.67% 24.45% 21.05%

• Growth in Global Streaming

Dom Stream as % of Total Revenue 61.66% 57.50% 52.62% 48.41% 45.86% 45.00% 45.30% 44.50% 44.65% 43.75%

International Streaming Segment 1,953,435 3,211,095 5,089,191 7,782,105 10,616,225 14,011,710 17,697,355 22,509,062 27,918,668 35,116,433

Int Stream % YOY Growth 64.38% 58.49% 52.91% 36.42% 31.98% 26.30% 27.19% 24.03% 25.78% Paid Memberships

Int Stream as % of Total Revenue 28.81% 36.36% 43.52% 49.27% 52.67% 54.00% 54.00% 55.00% 55.00% 56.00% forecasted to increase

Domestic DVD Segment 645,737 542,267 450,497 365,589 297,217 259,476 229,410 204,628 177,664 156,770

annually at an increasing

Dom DVD % YOY Growth -16.02% -16.92% -18.85% -18.70% -12.70% -11.59% -10.80% -13.18% -11.76%

Dom DVD as % of Total Revenue 9.52% 6.14% 3.85% 2.31% 1.47% 1.00% 0.70% 0.50% 0.35% 0.25%

rate and surpass 300m in

Total Revenue 6,779,511 8,830,669 11,692,713 15,794,341 20,156,447 25,947,611 32,772,880 40,925,568 50,761,214 62,707,917 FY23E.

Total Revenue % YOY Growth 30.26% 32.41% 35.08% 27.62% 28.73% 26.30% 24.88% 24.03% 23.54%

• Average Revenue Per Paying

Global streaming paid members at end of

period (in thousands) 70,839 89,090 110,644 139,259 167,090 200,090 235,090 273,090 315,090 362,090 Membership forecasted to

Global streaming paid net membership

increase at a constant rate

additions (in thousands) 16,363 18,251 21,554 28,615 27,831 33,000 35,000 38,000 42,000 47,000

of 7.50% annually.

Net membership additions as a percentage of

total paid members 23.10% 20.49% 19.48% 20.55% 16.66% 16.49% 14.89% 13.91% 13.33% 12.98%

Average Revenue Per Paying Membership $ 95.70 $ 99.12 $ 105.68 $ 113.42 $ 120.63 $ 129.68 $ 139.41 $ 149.86 $ 161.10 $ 173.18

Average Monthly Revenue Per Paying

Membership $ 7.98 $ 8.26 $ 8.81 $ 9.45 $ 10.05 $ 10.81 $ 11.62 $ 12.49 $ 13.43 $ 14.43

Average Monthly Revenue Per Paying

Membership % YOY Growth 3.57% 6.62% 7.32% 6.36% 7.50% 7.50% 7.50% 7.50% 7.50%Discounted Cash Flow – Target Price: $601.26

Levered Market Cap Unlevered Weighed Average Cost of Capital (WACC)

Comparable Company Name Ticker Beta (USD) Total Debt Tax rate Beta

Amazon.com, Inc. NasdaqGS:AMZN 1.20 2,221,511.9 (77,535.00) -17.75% 1.15

• Comparable companies were chosen

Apple Inc. NasdaqGS:AAPL 1.28 1,596,923.5 (122,278.00) -16.86% 1.17

on the basis of providing media

DISH Network Corporation NasdaqGS:DISH 2.00 323,515.6 (14,282.30) -41.27% 1.88

Comcast Corporation NasdaqGS:CMCS.A 1.00 235,812.2 (111,989.00) -31.47% 0.62

entertainment.

The Walt Disney Company NYSE:DIS 1.20 50,662.2 (62,323.00) 24.41% 0.62

AMC Entertainment Holdings, Inc. NYSE:AMC 2.50 454.4 (10,352.90) 0.91% 0.11 • Beta was obtained from Yahoo

Unlevered Beta 0.98 Finance which were levered beta

Netflix, Inc. NasdaqGS:NFLX 0.92

values

Netflix, Inc. NasdaqGS:NFLX 1.05 225,492.2 16,203.5 9.47% 0.98

Cost of Debt 4.24%

Risk Free Rate 1.84%

Adjusting close on 19 Jan 21

for 30 Year Treasury

• 30-years US treasury bond rate as

Equity Risk Premium 3.20% Chosen between 3% to 10%

risk-free, estimated at 1.84%

Cost of Equity using comparables derived beta 5.20%

Cost of Equity using historical beta 4.62% • Cost of Equity using comparable

WACC 4.57% Using historical beta Cost of Equity companies derived levered beta is

5.20% whereas Cost of Equity using

Netflix’s historical beta is 4.62%Discounted Cash Flow – Target Price: $601.26

Projection

Discounted Cash Flow Valuation FY20E FY21E FY22E FY23E FY24E

Discounted Cash Flow (DCF)

Total Revenue 25,947,611 32,772,880 40,925,568 50,761,214 62,707,917

EBIT 2,960,071 4,116,322 5,784,607 7,731,883 10,227,600 • Discounted Cash Flow was

Less: Tax (444,011) (617,448) (867,691) (1,159,782) (1,534,140)

NOPAT 2,516,060 3,498,873 4,916,916 6,572,101 8,693,460 projected based on a 5 year

Plus: Depreciation and amortization of Property, Equipment and Intangibles

Plus: Amortization of streaming content assets

84,783

12,050,070

110,987

14,787,123

141,040

17,943,406

175,134

21,545,902

213,584

25,766,683

horizon.

Plus: Other non-cash items 41,516 36,706 32,740 28,426 25,083

Plus (Increase)/Decrease in working capital (14,289,256) (17,646,403) (20,451,049) (23,960,966) (27,939,010)

Less: Capex (259,476) (311,342) (368,330) (431,470) (501,663) • Present Value (PV) of each year

FCF 143,697 475,944 2,214,724 3,929,127 6,258,138 and the Terminal Value (TV) of

Yearfrac 1.0 2.0 3.0 4.0 5.0 the final year was calculated to

arrive at Enterprise Value (sum

Discount Factor 0.96 0.92 0.88 0.84 0.80

PV FCF 137,415 435,240 1,936, 778 3,285,815 5,004,711

of all PVs)

FCF

Sum of FCFs 10,799,960 • Implied share price of $601.26

TV

FCF in FY24E 5,004,711

was obtained.

Perpetuity Growth 3.00%

TV in FY24E 328,026,774

PV of TV 262,327,104

Enterprise Value 273,127,064

Cost of Equity

Less: Long-Term Debt (20,662,964)

4.72% 4.67% 4.62% 4.57% 4.52%

Perpetuity Growth

Plus: Cash and Cash Equivalent 10,767,300

Implied Equity Value 263,231,400 2.90% 530.29 547.10 564.87 583.66 603.57

Basic Shares Outstanding as of FY 2019 437,799 2.95% 545.96 563.71 582.50 602.41 623.55

Implied Share Price 601.26 3.00% 562.57 581.35 601.26 622.40 644.88

3.05% 580.21 600.11 621.25 643.74 667.71

Current Share Price (as of 19 Jan) 497.98 3.10% 598.97 620.11 642.60 666.58 692.19

Potential Upside 20.74%Multiple Analysis (TEV/EBIT) – Target Price: $476.38

Comparable Company Name Ticker TEV/ EBIT Multiple Analysis – TEV/EBIT

Amazon.com, Inc. NasdaqGS:AMZN 84.5

Apple Inc. NasdaqGS:AAPL 35.2 • Comparable companies were chosen on the

DISH Network Corporation NasdaqGS:DISH 11.4

Comcast Corporation NasdaqGS:CMCS.A 17.9 basis of providing media entertainment.

The Walt Disney Company NYSE:DIS 73.8

AMC Entertainment Holdings, Inc. NYSE:AMC NM

• TEV/EBIT multiples for comparable companies

Netflix, Inc. NasdaqGS:NFLX 10.2

were obtained from CapitalIQ .

Highest TEV/EBIT 100th Percentile 84.5

Middle TEV/EBIT

Lowest TEV/EBIT

75th Percentile

50th Percentile

73.8

35.2

• Upper limit TEV/EBIT range was set at 100th

percentile, middle or target TEV/EBIT was set

Netflix EBIT for FY20E 2,960,071

at 75th percentile and lower limit TEV/EBIT was

Highest Netflix TEV 250,125,962 set at 50th percentile.

Middle Netflix TEV 218,453,207

Lowest Netflix TEV 104,194,484

• From the analysis, a range of $215.39 to

Highest Netflix Enterprise Value 240,230,298

Middle Netflix Enterprise Value 208,557,543 $548.72 was derived.

Lowest Netflix Enterprise Value 94,298,820

Basic Shares Outstanding as of FY 2019 437,799

Highest Netflix Implied Share Price 548.72

Middle Netflix Implied Share Price 476.38

Lowest Netflix Implied Share Price 215.39Football Field Valuation Range

52 Week

298.84 556.55

High Low

Analyst

550.00 660.00

Estimates

DCF 530.29 692.19

Valuation

TEV/ 215.39 548.72

EBIT

497.98 600.00

0 100 200 300 400 500 600 700 800

Lowest Range Highest Range Current Price Target PriceESG Factors

Strong tailwinds in ESG – Netflix postured for growth

Key Trends Netflix ESG Score

➢ Growing pressure from ➢ Environmental: In 2019, the company has

Governments, NGOs, managed to change to 50% clean ESG Rating 18.2 (Low Risk)

businesses, and consumers electricity use by installing numerous

to adopt sustainable wind turbines and solar panel systems. Industry:

practices Netflix is planning by 2022 to raise this Media 168 out of 266

number to 80% and by 2025 intend to

➢ Greater transparency owing use 100% clean energy Global

to releasing of relevant Universe 1865 out of 12844

sustainability ➢ Social: Conscious effort in ensuring

reports/practices and the rise representation and diversity of workforce

of credible rating agencies to (women, black etc)

audit such companies (eg.

Sustainalytics, Thomson ➢ Governance: Maximize long-term

Source: Sustainalytics (Morningstar)

Reuters, RobecoSAM, GRESB, shareholder value by ensuring intellectual

SASB) property (IP) protection Accurate as of Dec 22, 2020Investment Risks

Business model leaves Netflix susceptible to consumer demands and external threats

✓ Netflix derives their revenue purely from their 3 subscriptions plans offered

Single source of income ✓ Unable to generate more income from existing user base

✓ An unexpected shift in demand will prove detrimental to their balance sheets

✓ Huge initial outlay needed for content licensing and original content production

High Upfront Costs ✓ Price hikes in service due to rising costs, resulting in dissatisfied customers

✓ Large amounts of debt taken to finance the costs needed, increasing default risk

✓ Apple, Disney+, Amazon Prime Video, HBO threaten Netflix’s market share

Tough Competition and position in the saturated digital streaming industry

✓ Piracy/Illegal content downloading and use of VPN remains a growing concern

✓ Regulations revolving around data collection practices and anticompetitive

behavior could potentially pose more issues for Netflix in the future

Tightening Regulations ✓ Controversial rulings (e.g. in EU) can lead to unnecessary tax liabilities

✓ Netflix is also not available in all countries, with restrictions and

censorship limitations in more than 130 countries

Currency Rates ✓ Vulnerable to fluctuating exchange rates in countries they are operating inYou can also read