INDICATA Market Watch - Edition 14 March 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INDICATA Market Watch COVID-19 Rough waters continue but some glimmers of hope Edition 14 March 2021

Executive Summary

• Used car market still blighted by the impact • Total used car stock levels going into March

of Coronavirus restrictions. 2021 are 3.2% lower than the previous month

but 6.2% higher than March 2020, and 12.3%

• February used car sales volumes ease back above the same month in 2019.

0.6% compared to January 2021.

• Stock turn for BEVs increases by 7%

• Year-on-Year February 2021 used car sales year-on-year as other powertrains

down 5.2% and 8.1% down year-to-date. sees a small fall.

• Typical ex-fleet vehicles aged 3-5-years old, • ICE vehicles (diesel 6.0x, petrol 5.3x) remain

faring better than older used cars. the fastest selling used cars.

• Turkish market showing the strains • The start of the year saw our pricing index

of a market returning to normality. rise in line with the usual seasonal trends as

• Poland sees some tactical sales activity to try 3-year-old cars are reset to 2018 first

to fill supply constraints. registrations compared to 2017 first

registrations tracked through 2020. With a

• Only France and Austria are showing tactical consistent pool of vehicles, we would expect

sales activity. the lifecycle to show a steady downward

movement in average prices

• Used petrol (-9%) and diesel cars (-11%) see month-on-month, but most markets are

sharp falls in used car sales YoY but there are bucking this trend.

supply constraints in some markets.

• Online sales have become a key part of

• YoY used car sales increase for BEVs (+131%) selling used cars through the Covid-19 crisis

and hybrids (+85%) as alternative powertrains and going forward there is little evidence to

become increasingly popular. BEV sales are support a full return to pre-crisis operating

up 7% month-on-month and hybrids up 9%. models.

INDICATA Market Watch March 2021 - Edition 14

2

European Markets

Online B2C sales down 8.1% for the first two months of 2021

Across the EU region that we cover and February 2021

excluding Turkey, online B2C online

used car sales fell 5.2% in February 2021

compared to February 2020. Overall,

that puts the market 8.1% down for the

first two months of the year. February

should signal the end of negative sales

compared to a year earlier with March

being the first comparator to a Covid-19

lockdown period.

The impact of lockdowns and Covid-19 is

also continuing to impact not just how

people are buying used cars, with

increased online activity but also when.

After the New Year rush in January for

most markets, and before the

registration plate change in the UK,

February usually sees used car sales fall

month-on-month by around 7.5%

however, the pent-up demand resulted

in sales remaining almost on par with

January with just a 0.7% decline. Austria Germany Denmark Spain France United Kingdom Italy Netherlands Poland Portugal Sweden Turkey

Country

With several countries experiencing a

third wave of Covid-19, and vaccinations

not happening rapidly in several However, dealers are increasing their online presence developing in later Market Watch editions this year.

mainland European countries, it looks which is resulting in some of the growth in online B2C

like a lot of 2021 could still see much of sales we are seeing. We are currently carrying out In the meantime, we will continue to follow how

the region in and out of lockdowns, some research on this topic and we hope to be able Covid-19 is impacting the industry, staying focused on

impacting new and used car sales. to bring you more information on how this is both volumes and market stock turns in our report.

INDICATA Market Watch March 2021 - Edition 14

3

Used off lease vehicles doing better than the rest of the market

Sales may be down across the region Year-on-Year Changes (February 2021 vs February 2020):

but the increase in online selling is

working well for dealers who are

trading in the typical off-fleet ages of

vehicles at 3-5 years of age. Whilst

sales were almost flat year-on-year you

need to consider that we are

comparing a Covid-19 restricted

February 2021 with a relatively

unaffected February 2020. Also, worth

noting is how much better off-fleet cars

are performing compared to younger

used vehicles and against the older end

of the market.

Sales of young used cars are down

compared to a year ago but the fall of

6% is far smaller than the 25% YoY

drop last month. The indications are

that some manufacturers are starting

to support some tactical sales in

certain markets which dealers are then

able to support through the increase in

online selling. There is further evidence

of this with stock turn up 10% YoY for

the very youngest cars to 4x.

The move away from the traditional internal Before totally writing off the ICE cars in the used

Whilst stock turn for all other ages is combustion engine “ICE” continues in the used car car market it is worth noting that stock turn for

down compared to February 2020 the market with used diesel cars down 19% YoY in diesel (6x) and petrol (5.3x) are only marginally

average of around 6.2x for 3-year-old January and a further 11% decline this month down on this time last year and selling much faster

cars and above is an improvement on versus a year earlier. Used petrol cars followed a than battery electric vehicles “BEVs” (3.5x) and

the 5.8x seen last month providing similar path with a 9% fall in February YoY hybrid cars (4x).

some home for the future. following on from the 21% drop we saw last month.

INDICATA Market Watch March 2021 - Edition 14

4

Stock levels remain

high year-on-year

heading into March

With March opening stock levels still much higher in

Turkey (YoY +74%) than a year ago, due to falling sales

since quarter 3 2020, we have excluded the distorting

effect it would have in reporting the total regional stock

levels as being 6.2% above March 2020 levels.

Compared to February 2021 the levels of used stock did

fall 3.2% month-on-month as dealers remain cautious

about taking on too much stock whilst Covid-19 continues

to impact businesses generally, considering they are

already so heavily stocked compared to a year ago.

Supply constraints continue to be a problem for some

markets with Poland seeing sales fall but still eating into

dealer’s online stock which fell a further 6.6% compared

to February 2021 and which is down 21.1% compared to

March 2020.

Covid-19 continues to drive various restrictions on

non-essential physical shopping across the region, when

combined with an increasing number of online retailers,

even in the used car sector, it has resulted in consumer

confidence growing for e-commerce. With much of the

left-hand drive market in Europe sharing the euro and

with less restrictions and red tape on moving vehicles

between European Member states there are definite

opportunities to supply used vehicles on more than just

the domestic market. This would help flatten some of the

supply peaks and troughs, but any pan-European strategy

still faces challenges from tax authorities and legislators

which should not be underestimated.

INDICATA Market Watch March 2021 - Edition 14

5

Austria Dealer sales lead the way Online B2C used car sales rose 19.3% in February year-on-year as the Austrian used car market saw its third consecutive month of growth after a 2.8% rise in January and a 10.3% increase in December. Almost all that growth happened in the typical franchise dealer segment of used cars up to 5-years-old as online sales continue to become more compelling for customers and dealers alike. Hybrid vehicles continue to lead the charge in sales growth of alternative powered cars with sales up 194% in February compared to a year earlier, following a 137% YoY increase the previous month. BEVs also continue to enjoy increased demand as sales rose 156%. Last month’s report highlighted signs of a potential supply constraint in the market for the internal combustion engine cars and a month later the signs are even clearer. Despite sales of used diesel cars increasing by a healthy 15% YoY, with used petrol doing slightly better (+16%) compared to a year earlier the sharp rise in stock turn shows how the sales growth could have been even higher. Stock turn for used petrol cars rose 34% YoY to 5.1x but demand for used diesels saw stock turn hit 5.9x, a 38% increase compared to the same month last year. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month but used car demand is having some inflationary impact on prices in the Austrian market. Contact: Andreas Steinbach ash@autorola.at INDICATA Market Watch March 2021 - Edition 14

Denmark Lockdown continues to hit used car market The coronavirus lockdown for the whole of January and February continues to decimate the Danish used car sector. After online B2C used car sales fell by 21.3% in January year-on-year, February saw a further 10.1% decline over the same month last year. Young used cars, those up to 3-years-old, are a key part of many franchise dealer’s sales but with non-essential shops on lockdown it is not surprising to see sales of these vehicles taking the brunt of the drop in YoY sales Denmark continues to see some of the highest growth rates for BEVs with sales up 205% in February 2021 YoY, following a 362% increase in January over the same period in 2020. Sales of hybrids have seen more modest growth over this time last year. The internal combustion engine “ICE” cars continue to make up the most sales in volume terms but February saw yet another double-digit decline year-on-year in a trend which shows no signs of slowing down. Whilst stock turn remains predictably down for all powertrains compared to a year ago it is the 26% fall in BEVs to a 2.8x turn which is most concerning. With BEV sales still growing rapidly the slow speed of sale indicates a significant oversupply, particularly in the current Covid-19 environment. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month-on-month but used car demand is having some inflationary impact on prices in Denmark. Contact: Thomas Groth Andersen tga@bilpriser.dk INDICATA Market Watch March 2021 - Edition 14

France Supply constraints are back Used car sales rose 1% in February 2021 compared to February 2020. At first glance this would indicate a weak market which is understandable in these Covid-19 hit times we are currently living in. Dig a little deeper under the headline results though and it may be availability of stock which is holding the market back. Stock turn for all powertrains has increased sharply with the market volume leader diesel seeing stock turn hit 8.9x, a 7% increase YoY. The three other main powertrains all saw annual increases in stock turn of 22% or more with used petrol cars turning over at 9.3x per annum, hybrids at 7.0x and BEVs at 5.9x. Similar increases of stock turn growth are visible at all ages of typical dealer and trader stock, i.e., those up to 6-years-old. This may explain why there is also such a sharp rise in manufacturer backed tactical registrations to increase the volume of used vehicles going into dealers to meet some of the demand and keep the market active. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month, but supply constraints are holding them flat in France currently. Contact: Pierre-Emmanuel BEAU peb@autorola.fr INDICATA Market Watch March 2021 - Edition 14

Germany Return of 19% VAT rate continues to hit used car market New and used car sales in Germany have now had two successive months of decline following the reintroduction of the 19% VAT on 1 January 2021, following the 3% reduction for the second half of 2020. Online B2C used car sales fell 16.3% in January year-on-year followed by a slightly better 5.4% fall in February 2021 compared to the same month last year. The reduced VAT rate of 16% had pulled forward some sales into the latter part of 2020 as consumers sought to exploit the reduction, particularly on new and younger used cars. The impact can be clearly seen in the younger used cars, i.e., under 2-years-old, where sales are down 15% on the 1-2-year-old cars and 21% down on the very young cars, with manufacturers clearly not willing to pay the price for pushing tactical registrations. Sales of used alternative powertrains continue to see high percentage level growth with BEVs outperforming hybrids in growth terms. BEVs are also selling faster than hybrids with a 3.2x stock turn, up 27% compared to February 2020, whilst hybrids have dropped 10% to just a 2.9x turn indicating an excess of supply. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month, but dealers seem unwilling to move prices whilst the market remains a little volatile. Contact: Jonas Maik jmk@indicata.de INDICATA Market Watch March 2021 - Edition 14

Italy New tax regime helps used car sales to a fast start 2021 March sees the introduction of a new bonus-malus scheme for new cars. The new NEDC emissions tax scheme, like the one already in place in France, did not generate enough sales traffic to create growth in new car sales but it did increase sales of higher polluting cars, including some manufacturer tactical registrations in February. The net impact on the current used car market was enough to maintain a ninth consecutive month of growth with used car sales up 4.1% in February. That said the new tax regime is likely to have a dampening effect on the new car market and with it the flow of part exchanges into the used car market. The impact of the tax changes can already be seen in sales of typical dealer stock vehicles in the 3-6-year-old cars where consumers try to beat the tax change brought in their older cars to trade for a new or nearly new one. This part exchange stock then washes through the used car market. Despite this extra used car supply, demand remains strong with all powertrains seeing a year-on-year increase in used car sales, although for internal combustion engine used cars the growth was marginal. That said stock turn particularly for used diesel cars grew sharply YoY (+21%) to 5.9x but that is still behind the faster selling used petrol cars indicating a supply constraint for the ICE vehicles. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month, but supply constraints are creating some inflationary pressures in Italy. Contact: Alberto Ongari ao@autorola.it INDICATA Market Watch March 2021 - Edition 14

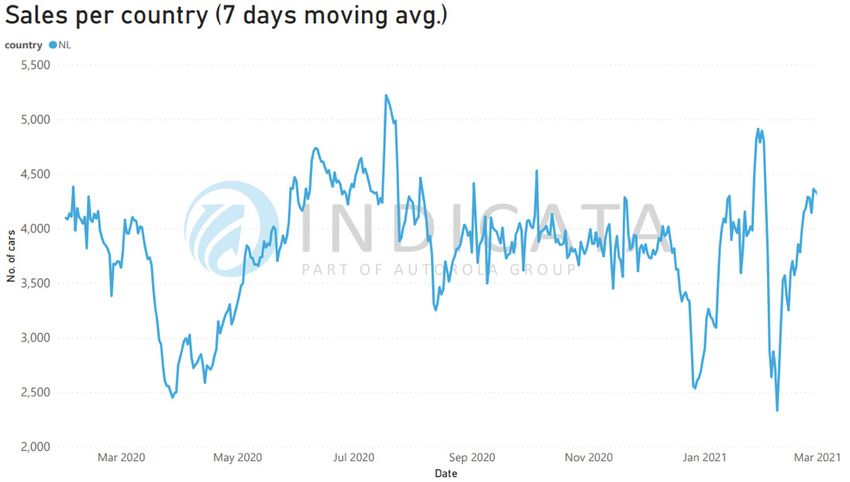

The Netherlands Used car demand low as lockdown continues The ongoing lockdown restrictions throughout February has meant used car sales continue to fall in The Netherlands with a 15.7% year-on-year decline putting the first two months of 2021 7.3% down over the same period last year. This means the used car market has not seen a significant upturn in YoY sales since the 6.6% increase in September 2020. Once again there are no exceptions to the rules across age ranges with February used car sales across just about all ages down compared to the same month last year. When the sales decline is compared to the YoY reductions in stock turn rates per age banding the issue is clearly very much demand driven with consumers generally less willing to go out and invest in a replacement car. On the positive front BEVs continue to see strong percentage growth in sales with the 114% YoY increase in January followed by a 97% increase in February compared to the same period last year. However, the growth in hybrid sales is slowing with sales up 24% in February 2021 compared to February 2020, and to a 40% increase YoY in January. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month. With demand low and sufficient stock to meet that demand, prices are currently falling in line with expectations. Contact: Bobby Rietveld bri@autorola.nl INDICATA Market Watch March 2021 - Edition 14

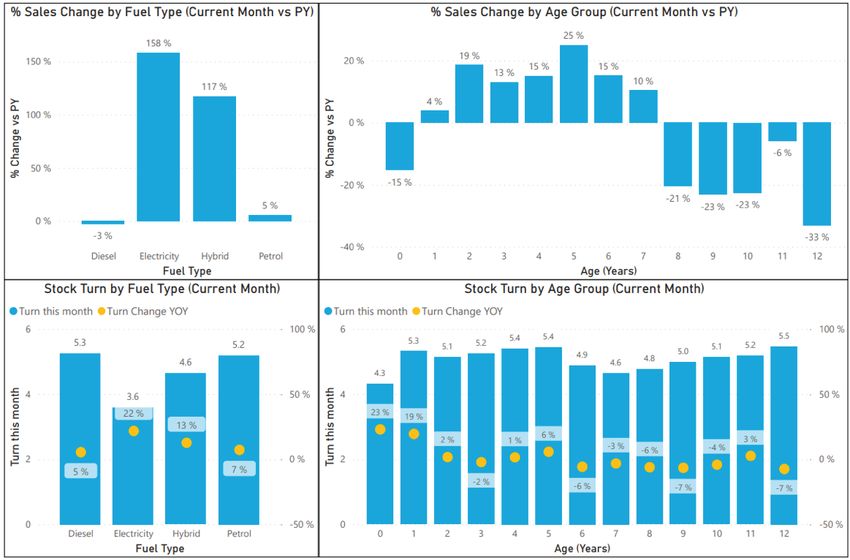

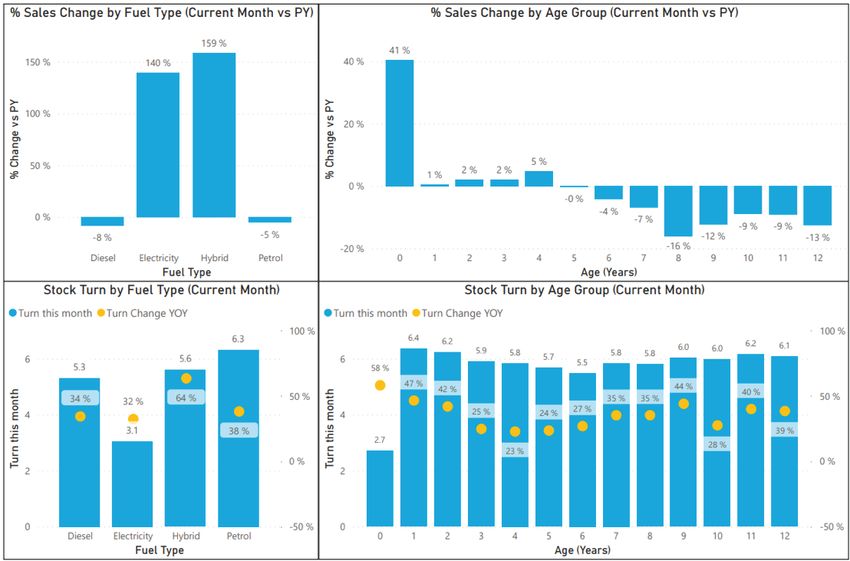

Poland Used car market hit with supply constraints Used car sales fell 3.2% in February 2021 compared to February 2020 as supply constraints continue to hold back the used car market. Overall, this means used car sales for the first two months of 2021 are now down 3.2%. Total stock levels heading into March were 21.1% down on a year earlier and down a further 6.6% over the previous month as dealer struggle to find suitable used stock to meet demand. Manufacturers appear to be trying to ease the situation with an increase in tactical sales and a push on stock turn of younger used cars but as you can see from the table stock turn for all ages of vehicles is well above this time last year as demand outstrips supply. Unlike in some other markets, hybrids are particularly desirable currently in the Polish market with used hybrid sales up 159% YoY, outstripping the 140% growth in BEVs over the same period, and stock turn 64% higher than a year earlier at 5.6x. Used petrol cars remain the fasting selling powertrain with stock turn up 38% to 6.3x. The only powertrain which does not appear to be constrained by stock availability are used BEVs when comparing sales growth to stock turn The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month. Continuing severe supply constraints mean prices are continuing to buck the trend with a further increase in February. Contact: Daniel Steć das@indicata.pl INDICATA Market Watch March 2021 - Edition 14

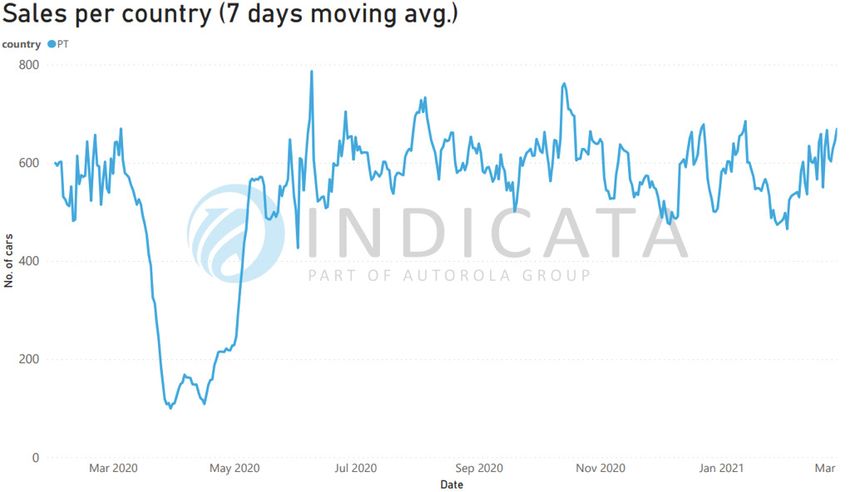

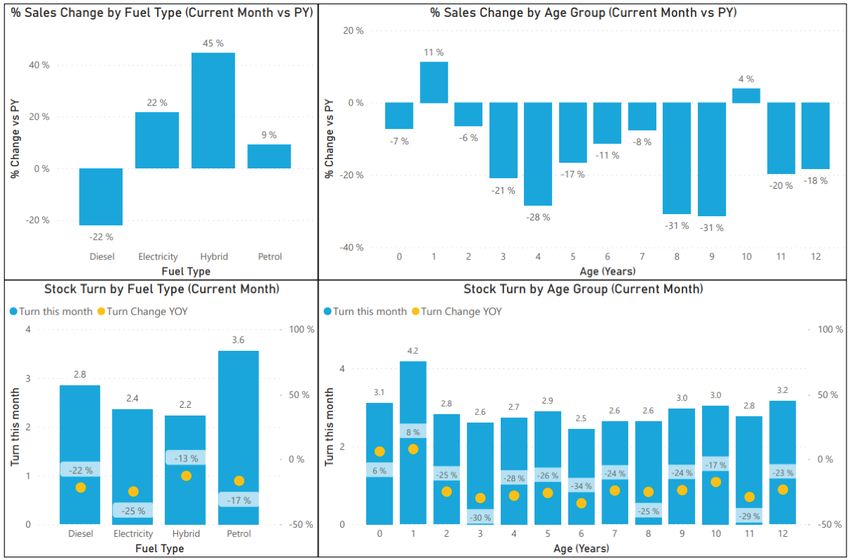

Portugal Used prices hold up well despite stock pressures easing The Covid-19 pandemic and ensuing restrictions and lockdowns has seen online used car sales increase for much of the last 12 months, once the first lockdown eased. But as online sales settle and with February 2020 being a strong month for used car sales February 2021 has seen online B2C used car sales fall 12.0% year-on-year. The tax regime in Portugal continues to help the decline of diesel as used sales fall 22% in February compared to the same month last year. Unlike much of Europe hybrids are seeing the strongest year-on-year growth as online sales rise 45% YoY compared to just a 22% rise in used BEV sales over the same period. The supply constraints which had been visible in the market have now eased with stock levels almost on a par with last month (-0.6%) but 16.8% above where they were at the start of March 2020. Stock turn is also down markedly with all fuel types and all ages seeing a notable decline over this time last year. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month. Whilst supply constraints have eased dealers continue to hold their prices against the natural depreciation expected. Contact: Sandra Sequerra sas@autorola.pt INDICATA Market Watch March 2021 - Edition 14

Spain Used car sales rise 2.5% year-on-year as stock pressures ease Used car sales rose 2.5% in February 2021 compared to February 2020 despite the current Covid-19 restrictions. For the first two months of 2021 this still puts the online used car market 3.8% lower than the same period in 2020. February repeated the pattern we saw in January for sales by powertrain. Used diesel cars saw a YoY drop of 3% (-4% in January) whilst petrol car sales rose 5% (+5% January), hybrids increased by 117% (+91% January) and BEVs outperformed the lot as sales jumped 158% in February following a 120% increase YoY in the previous month. Whilst March opening online used stock levels are 2.0% lower than the previous month, they are 7.6% higher than a year ago. Stock turn is also higher than a year ago with all powertrains selling faster than this time last year although at 3.6x BEVs are clearly in freer supply with lower overall demand. Considering stock levels and stock turn together it looks like the easing of stock constraints which we saw last month are continuing. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month. Whilst supply constraints have eased Spain’s dealers continue to hold their prices against the natural depreciation expected. Contact: Leyre Delgado lde:autorola.es INDICATA Market Watch March 2021 - Edition 14

Sweden Used car sales rose 2.2% in February After kicking off 2021 with an 8.0% fall in used car sales in January 2021 compared to January 2020, February saw some positive news as sales of online used car sales rose 2.2% year-on-year and up 4.3% compared to the previous month. Used hybrid sales continue to do well with sales growth of 79% YoY outperforming the 73% increase in used BEV sales. The internal combustion “ICE” vehicles fared less well with used petrol car sales down 9% compared to February 2020, whilst used diesel car sales remained flat. The performance of the traditional powertrains may in part be due to supply constraints. Stock levels going into February were already 1.4% down on the previous month and by the end of the month they had fallen a further 2.9%. This means stock levels are now 9.9% lower than a year earlier. When you look at the stock turn used petrol cars are at 6.5x, up 27% YoY, whilst used diesel cars are hitting 8.0x a 41% increase on this time last year. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month. With signs of renewed supply constraints, it is not surprising to see prices are holding up and not falling in line with expectations. Contact: Yngvar Paulsen ypn@autorola.se INDICATA Market Watch March 2021 - Edition 14

Turkey Used car market slowdown continues 2020 was such an extraordinary year due to Covid-19 it is not surprising to see 2021 starting to return to more normal levels. Whilst a 31.8% year-on-year drop in January 2021 followed by a 32.2% drop in February compared to February 2020 may sound dramatic if you compare February 2021 to February 2019 the fall is only 0.8% well within the realms of business as usual. The traditional petrol and diesel powertrains struggled the most with sales of used diesel cars dropping 34% with used petrol cars dropping only a little less at 31%. However, despite 2020 being a very untypical year in terms of both sales and pricing used alternative powertrains are still doing even better in 2021 as sales have jumped a further 127% in February 2021 compared to the same period last year. The move to more typical sales patterns has had an impact on used stocks with levels going into March 74% above where they were a year earlier and 45.6% higher than February 2019, but this should right itself over time. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month. Whilst higher than a year ago prices are now returning to a pattern in line with expectations. Contact: Aslı GÖKER asl@indicata.com.tr INDICATA Market Watch March 2021 - Edition 14

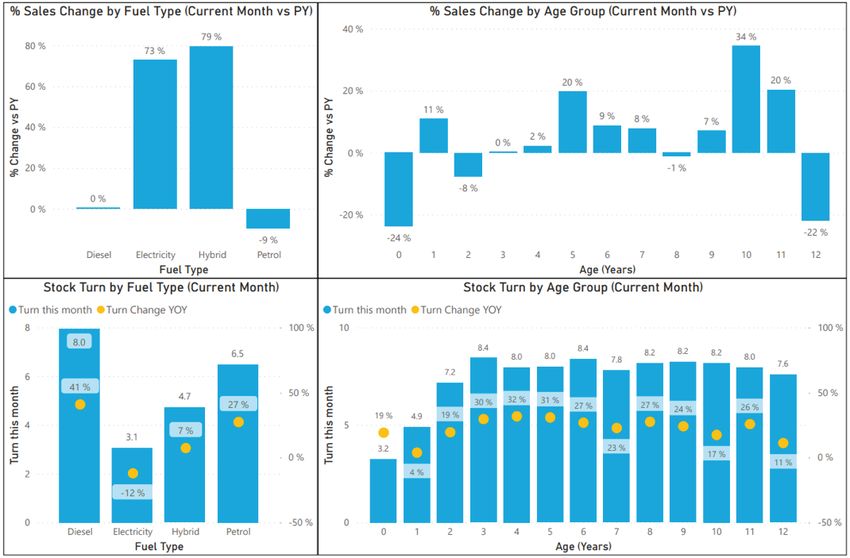

United Kingdom Lockdown continues to depress used car sales With the UK Covid-19 vaccination programme on target to see lockdown restrictions lifting the future offers some hope of a return to normality. Unfortunately, February had the same restrictions that have been in place since Christmas, which means the 28% year-on-year decline seen in January 2021 has been followed by a 14.4% fall in February YoY. However, it is worth remembering that February 2020 was a particularly good month for the used car market, so comparing February 2021 with February 2019 shows a two-year fall of just 8.8%. The reintroduction of a lockdown after Christmas has given dealers little time to adjust their stock levels to match demand resulting in stock levels going into March 2021 11% higher than a year earlier and 7.2% above February 2019 levels. February stock turn levels for all powertrains are down over this time last year confirming no significant supply constraints. As such the 18% fall in used petrol cars and the 16% drop in used diesel cars are merely reflective of the state of the current consumer market. Whilst alternative powertrains are faring better with BEVs up 58% and hybrids up 34% the rates of growth are well behind those seen across the rest of the region. The start of the year saw our pricing index rise in line with the usual seasonal trends as 3-year-old cars are reset to 2018 first registrations compared to 2017 first registrations tracked through 2020. With a consistent pool of vehicles, we would expect the lifecycle to show a steady downward movement in average prices month on month. With an end to lockdown on the horizon dealers are reluctant to take significant pricing action and so prices are currently falling in line with expectations. Contact: Jon Mitchell jm@autorola.co.uk INDICATA Market Watch March 2021 - Edition 14

INDICATA country contacts

If you are interested in contacting INDICATA, please see below a list of country

contacts or register through Indicata.com

Jon Mitchell – UK Andreas Steinbach – Austria Yngvar Paulsen – Sweden

UK Sales Director Autorola | Market Intelligence | Country Manager

Mobile: +44 7714 398799 INDICATA Autorola.se

Email: jm@autorola.co.uk Office: +43 1 2700 211-90 Mobile: +46 736871920

Mobile: +43 664 411 5642 Email: ypn@autorola.se

Pierre-Emmanuel BEAU – France Email: ash@autorola.at

Country manager Thomas Groth Andersen – Denmark

Téléphone: +33 (0)1 30 02 89 01 Jonas Maik – Germany Country Manager

Mobile: +33 (0)6 62 43 09 66 Senior Key Account Manager Bilpriser.dk

Email: peb@autorola.fr Mobile: +49 151-402 660 18 Mobile: +4563147057

Email: jmk@indicata.de Email: tga@bilpriser.dk

Leyre Delgado – Spain

INDICATA Product Management Jan Herbots – Belgium Daniel Steć – Poland

Phone: +34 91 781 64 54 INDICATA Sales Manager Dyrektor Zarządzający

Mobile: +34 630 246 158 Mobile: +32 497 57 43 91 Telefon: +48 22 300 81 88

Email: lde:autorola.es Email: jhe@autorola.be Telefon komórkowy:

Sofia El Barkani – Belgium Mobile: +48 602 188 902

Sandra Sequerra – Portugal INDICATA Support Executive Email: das@indicata.pl

Solutions & INDICATA Business Phone: +32 3 887 19 00

Unit Manager Mobile: +32 485 584 514 Aslı GÖKER - Turkey

Phone: +351 271 528 135 Email: sei@autorola.be Sales Director, INDICATA

Mobile: +351 925 299 243 Phone: +90 212 290 35 30

Email: sas@autorola.pt Bobby Rietveld – The Netherlands Mobile: +90 533 157 86 05

Sales Director Autorola & INDICATA Email: asl@indicata.com.tr

Alberto Ongari – Italy indicata.nl

Head of INDICATA Italy Mobile: +31 (0)6 113 091 58

Autorola.it Email: bri@autorola.nl

Mobile: +39335208233

Email: ao@autorola.it

INDICATA Market Watch March 2021 - Edition 14

18Background What is INDICATA

On the 24th March 2020 INDICATA

Market Watch?

published its White Paper “COVID-19 To

what extent will the used car market be INDICATA Market Watch takes two forms: If you would like FREE access to

affected (and how to survive)?” the web-based INDICATA

1. A regular PDF - Regular market overviews

This document explored: Market Watch tool (and are a

available for all on the INDICATA country

websites (this document)

Senior Manager within the

• Early market trends - Initial impact of auto industry), please contact

the virus and the social distancing 2. Free-to-access web-based reporting - your local INDICATA office.

measures implemented. Available for senior management in all major

Leasing, Rental, OEM and Dealer Groups.

• Market scenarios - A range of impacts

based on infection rate development

How do we produce

and historical market data.

• Mitigation - Risk assessment by

sector coupled with potential our data?

corrective actions.

INDICATA analyses 9m Used Vehicle adverts

across Europe every day. In order to ensure

We committed to keeping the market

data integrity, our system goes through

updated with live data, volume and price, extensive data cleansing processes.

to keep abreast of the fast-moving

environment. The Sales (deinstall data) in this report are

based on advertisements of recognised

As such we are pleased to announce automotive retailers of true used vehicles.

INDICATA Market Watch. As such, it does not include data related to

private (P2P) advertisements.

Where an advert is removed from the

internet, it is classified as a “Sale”.

INDICATA Market Watch March 2021 - Edition 14

19www.indicata.com

You can also read