ECONOMIC CURRENTS - Grant ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ECONOMIC CURRENTS

December 06, 2021

Groundhog Day:

Variants and the Outlook for 2022

Diane C. Swonk, Chief Economist

Living through the pandemic has been a bit like being Bill The inability to vaccinate the world and suppress the

Murray’s character in the 1993 film Groundhog Day. We spread of the virus exacerbated global supply chain

emerged from the first wave of infections and lockdowns disruptions. The Delta variant was particularly costly.

hoping to return to the world we left behind only to realize

we were entering a loop of recurring infections and Unprecedented fiscal stimulus and interventions by

disruptions that proved hard to escape. central banks provided a much-needed bridge for

those who could not work to traverse COVID-tainted

Once the reality of his predicament set in, Murray started waters. Chart 1 shows the boost to the level of real GDP

to slide down a rabbit hole of riskier behaviors, living life that everything from enhancements to unemployment

as “if there were no tomorrow.” He even drove off a cliff insurance and stimulus checks to forgivable loans and

in one scene only to reawaken to the sound of Sonny and transfers to the states provided and are expected to

Cher singing “I Got You Babe” again on his alarm clock. continue to provide to real GDP through early 2023. In

He was stuck reliving February 2. response, inflation also accelerated along with wages.

The only constant in our world is the virus, the havoc it The question for the Federal Reserve is whether what

wreaks and our unwillingness to leverage the tools we we are enduring will morph into a more entrenched,

have to wrestle the virus to its knees. Fatalities worldwide wage-price spiral, in which wage hikes start to feed into

are now approaching those of other pandemics, after inflation. That would require an aggressive jump in rates.

adjusting for the undercount in developing economies

and the surge in excess deaths they have endured. This The most recent Delta and Omicron waves are hitting

is despite the breakneck speed at which vaccines were when the private sector appears to be picking up the

developed and can be altered to target variants. baton from the public sector to carry growth. The fourth

quarter of 2021 will easily be the strongest of the year

The resulting loss of life and fear of infection have for the U.S.; annual growth is poised to reach 5.7%, the

resulted in labor shortages and wage hikes, much as fastest since 1984. This is despite the expiration of much

we have seen in other pandemics. What is unique is the of the direct aid to individuals and businesses.

synchronous surge in inflation. Pandemics typically

trigger a slowdown in inflation or all-out price declines This edition of Economic Currents takes a closer look

because of the destruction of demand. at the outlook for 2022, with the hope we make the

transition from a pandemic to an endemic - an illness that

This time is different. Technology accelerated the shift is seasonal and more manageable. We have the tools -

of economic activity online and kept large swaths of vaccines, rapid testing, masking and better therapeutics.

the population working and spending, even as fear of The challenge is to use them to their fullest, which we

contagion and mitigation efforts kicked in. have thus far failed to do.

Special attention will be paid to the outlook for inflation, The ranks of the unemployed fell to a pandemic low of

the risks of a wage-price spiral even in the absence of 4.2% even as participation in the labor market moved

additional fiscal stimulus and how the Fed is likely to significantly higher. The ranks of long-term unemployed

react. It is now convinced that the disruptions created continued to shrink, while those working only one instead

by outbreaks will compound underlying inflationary of multiple jobs held at a million fewer than we saw in

pressures, and that will need to be combated with rate February 2020.

hikes. The only question is how aggressive those rate

hikes will have to be. That was at the same time that everything we know about

in the labor market in November was improving. Initial

The 2022 Outlook: claims for unemployment insurance continued to fall; the

Institute for Supply Management (ISM) for services hit a

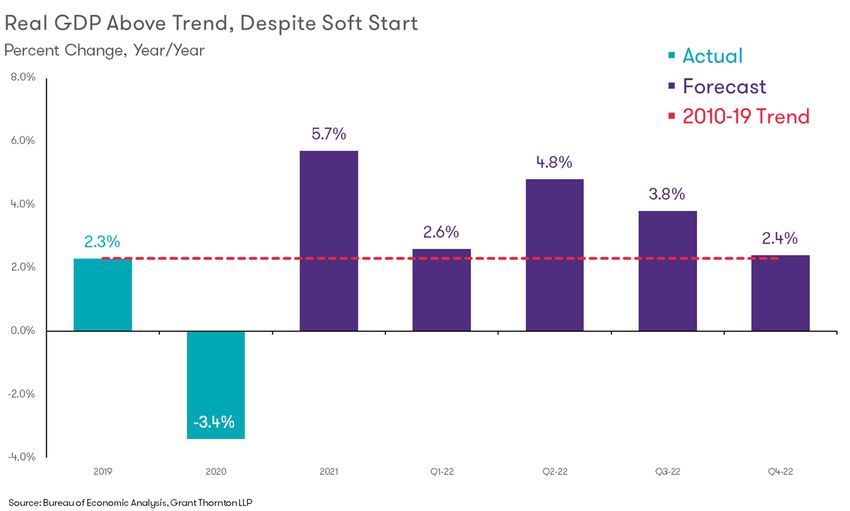

Chart 2 shows the forecast for growth in 2022. The

record high; plans to hire picked up; and, the ADP report

economy is expected to slow but remain robust with

on payrolls showed hiring held above a half a million jobs

overall growth still averaging more than 4% for the year.

for the fourth consecutive month. Many of those trends

That is nearly double the annual average from 2010-2019.

carried into early December. Google searches for how to

apply for unemployment insurance benefits fell through

The private sector is expected to pick up the baton from

early December.

the federal government in 2022. Payroll employment

slowed in November, but those figures likely understated

Separately, hiring by state and local governments is

the actual strength in the labor market. The response rate

expected to pick up. Their coffers are brimming with cash

on the establishment survey dropped to a decade low this

as understaffing is rampant. The largest hurdle is public

year, which has meant subsequent upward revisions.

sector compensation, which grew at about half the pace

of that in the private sector over the summer.

The household survey, which is not subject to revision,

revealed a much more robust labor market and more

Any setback in hiring as a result of Delta and Omicron

healing in November. It showed more than 1.1 million jobs

is likely to show up in early 2022 as hospitals are

were generated, with more than half a million workers

overwhelmed. Lockdowns have already been implemented

rejoining the labor force.

abroad. That could further disrupt supply chains that

were beginning to uncoil.

Chart 1

There is little tolerance for lockdowns in the U.S. but fear

is its own tax on the economy. Look for governments

and firms to push harder to get the unvaccinated to be

vaccinated. It is the only way out of a vicious cycle.

Consumer Spending Pivots

After an initial setback at the start of the year, consumers

are expected to pivot back into spending on services over

goods. That shift will generate less spending than the

surge we saw on goods. The pent-up demand for services

is inherently different from that for goods. Haircuts lost to

the pandemic cannot be replaced.

The wild card is the $2.5 trillion in excess savings amassed

during the pandemic. Low-income households are

expected to deplete their savings by year-end when they

reach the cliff in monthly child tax credits provided by the

last round of fiscal stimulus. High-income households tend

to spend their incomes but not their savings.

2 Monthly Economic Outlook: Groundhog Day

Spending on travel, tourism and medical services Investment Remains Robust

delayed by outbreaks is expected to see the strongest

gains. Leisure travel has already rebounded close to Large corporations are awash in cash and eager to offset

precrisis levels. The backlog for elective surgeries and the crimp in profit margins associated with rising wages

routine medical exams is substantial and likely to suffer with productivity-enhancing technologies. This gives them

another setback with a winter wave of infections. the means and motivation to invest and automate, which

will further shift the demand for workers away from the

Housing Bubbles Intensify less to more educated.

Home buyers scrambled to lock in what they feared Large tech-savvy retail behemoths, who are driving the

may be the last, low rates in late 2021. Higher mortgage gains in wages for the lowest paid workers, have greatest

rates and already high prices are expected to dampen incentives and scale to do so. That is good news for low-

demand in 2022. Home building is also expected to wage workers, who are finally getting a moment in the

slow, but only after some catch-up on backlogs due to sun after years in the shadows. There could be a problem,

materials and labor shortages early in the year. medium-term. Large firms are better able to erect barriers

to workers unionizing than midsize firms.

Investors will provide the most support for sales. They

are paying cash and snapping up properties unseen to The shifts we are seeing are challenging the business

flip to rent instead of sell. This has already crowded out models of many small and midsize firms. That could

many first-time buyers and could keep home values, undermine dynamism in the broader economy, which

which are already pushing up shelter costs up along with could curb innovations and keep productivity gains

rents, rising at a scorching pace. Some properties are triggered by new technologies concentrated in larger

in rural areas, which lack the broad-band necessary to firms instead of being shared across firms and with the

support remote work. broader economy.

Chart 2

3 Monthly Economic Outlook: Groundhog Day

Chart 3 A pickup in spending by state and local governments is

expected to more than offset the slowdown in federal

spending. A surge in retail sales and real estate tax

revenues, and transfers from the federal government, has

filled the coffers of many state and local governments.

The cost saving triggered by the move to online learning

left many public school districts awash in cash. The

problem is getting those funds out the door. Public

sector wages are rising much slower than private sector

wages. Some teachers are quitting to become substitutes

because the pay is better. The blows to morale and

staffing are so widespread that school districts extended

the Thanksgiving holiday with little to no notice; that left

parents scrambling to find child care.

Trade Deteriorates

The U.S. is expected to continue to grow faster than most

other major economies, which means imports should

outpace exports over the course of the year. The pivot in

Inventories Rebuild spending to services over goods means fewer imports per

dollar consumers spend; much of trade is trade in goods,

Inventories fell to rock-bottom lows as supply chain not services, which tend to be domestically produced.

disruptions worked their way around the globe. We have

seen uncoiling of backlogs as we entered the fall, but Risks: Risks to the near-term outlook are to the downside,

could suffer additional setbacks as the current Delta given the current Delta wave and the threat posed

wave and Omicron circle the globe. by Omicron. The bet is that Congress holds back on

additional stimulus given the surge in inflation. That said,

That said, inventories have begun to rebuild and are 2022 is an election year; stranger things have happened.

expected to be more fully replenished by year-end.

Double ordering to hedge against future shortfalls and a Inflation Simmers

pivot from just-in-time to just-in-case inventories systems

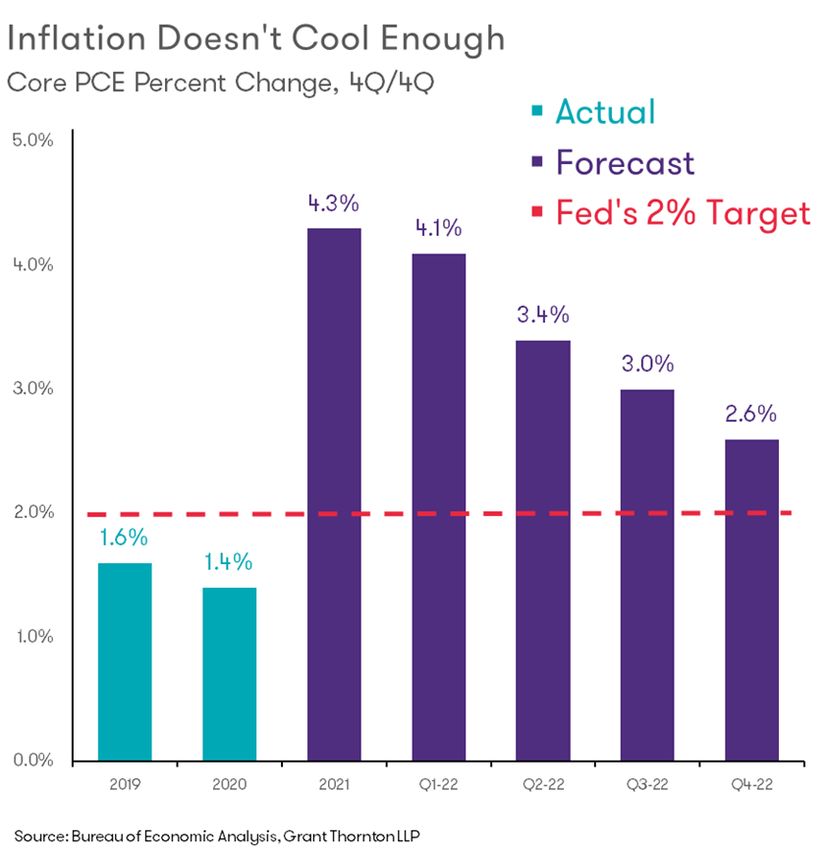

virtually assures rebuilding. We could even see a bullwhip Chart 3 shows the forecast for the core personal

effect, or unwanted surge in inventories, in 2023. consumption expenditures (PCE) index, which the Fed

watches the closest. Inflation is expected to moderate in

Transfers to State and Local Governments are Spent 2022 from the red-hot pace we saw in the fall of 2021 but

remain elevated through year-end:

Congress kicked the can down the road on debate

• Commodity prices have begun to cool in response to

over the administration’s Build Back Better plan with

the threat posed by Omicron;

a continuing resolution that will keep the government

funded into February of 2022. That means that what is • Supply chain disruptions have begun to uncoil, allowing

left of support for individuals - monthly child tax credit production to ramp up; and

checks - will lapse December 31, 2021. • A surge in inflation in the spring of 2021 should temper

year-on-year comparisons by the spring of 2022.

Congress did approve the bipartisan infrastructure bill.

The bulk of those funds will not show up until the mid- But,

2020s, as infrastructure projects take time to ramp up.

• Shelter and medical costs, both key drivers of inflation,

have just begun to accelerate;

4 Monthly Economic Outlook: Groundhog Day

Chart 4 Fed Chairman Jay Powell formally retired the word

“transitory” from the Fed’s language on inflation during

his most recent testimony to Congress. He underscored

his concern inflation is becoming broad-based. He is

not alone. Fed officials as a group have grown far more

concerned about the persistence of inflation, even as

commodity prices have cooled. This could prompt them to

act much more aggressively than currently forecast.

Risks: Chair Powell has said the Fed would be patient but

not hesitate to raise rates. The risk is that they panic and

raise rates too rapidly as they chase inflation for the first

time since the 1980s.

Treasury Bonds

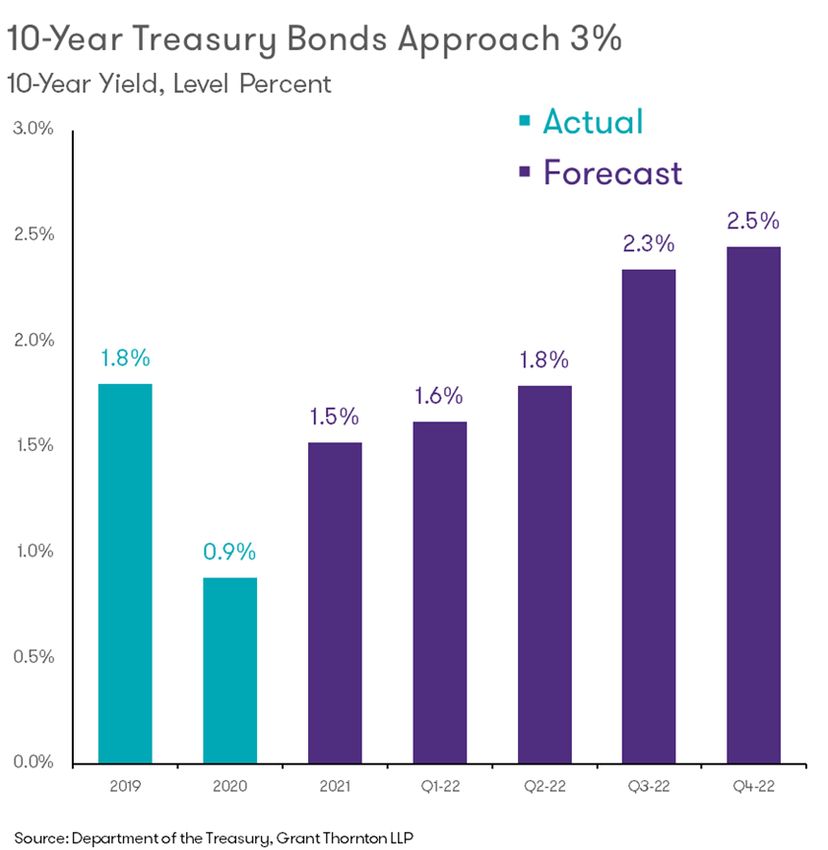

Chart 5 shows the forecast for the 10-year Treasury bond.

Yields are expected to rise after a setback in response to

Omicron. The yield curve has actually flattened in recent

weeks. Short-term rates have risen as the Fed’s intent to

raise rates has become clear, while long-term rates have

• Surge pricing on services is expected to offset some of

fallen, either because bond traders believe the Fed will

the slowdown in inflation in goods; and

be successful in reining in inflation or they will overshoot,

• Services, which are more dependent on labor costs causing the economy to cool even faster than expected.

than goods prices, could start to see a wage-price

spiral begin to take root. Risks: More rapid rate hikes by the Fed could trigger

an inversion of the yield curve. That is when short-term

Medical care is particularly sensitive to staffing rates rise above long-term rates; it can signal a coming

shortages; assisted living facilities have lost the most staff recession.

and face the worst labor shortages. The latter is one of

the places I would look first for a wage-price spiral. Chart 5

Risks: The current Delta wave and threats from Omicron

have already triggered lockdowns and restrictions in

travel. The risk is that those shifts could trigger another

round of supply chain disruptions and put more workers

on the sidelines. The result would reverse some of the

progress we are making in backlogs and exacerbate the

upward pressure on inflation absent commodity prices in

the near term.

Hawks Flock at Fed

Chart 4 shows the forecast for the fed funds rate in

2022. We expect the Fed to announce it will conclude

its purchases of Treasury bonds and mortgage-backed

securities in March instead of June at the December

meeting. That will leave the door open for a liftoff in rates

in June. Our forecast includes three rate hikes in 2022.

5 Monthly Economic Outlook: Groundhog DayFinancial Market Turbulence

Bottom Line

A lot of financial assets seemed to be priced to perfection

The pandemic just became a lot more difficult to endure.

in a wholly imperfect world. Rising rates could not only

Hollywood endings don’t tend to come to fruition in the

take the steam out of broader equity prices; they could

real world, but for now, I would like to believe they are

tip the apple cart. The reach for yield has prompted

possible. Bill Murray’s character was not able to escape

excessive risk taking, upping the ante on a more

Groundhog day, February 2, until he pivoted away from

disruptive market correction in 2022.

seeing each day as if there were no tomorrow. With the

help of his love interest, Andie MacDowell, he started to

The forecast, which includes robust growth with rate

see each day as a chance to improve his own life as well

hikes, translates to a 6% correction in broader stock

as those around him.

market indices. Markets tend to react in a nonlinear

fashion to a Fed that is chasing instead of preempting

He used his time to learn the piano and improve the

inflation.

quality of his own life as well as the lives of those he

touched. He even became a hero for his good deeds. But

Risks: An overshoot on rate hikes by the Fed could

it wasn’t until he fully abandoned his own narcissism,

destabilize financial markets at home and abroad.

and embraced an unconditional love for MacDowell’s

Developing markets are especially vulnerable, as they will

character, that he escaped February 2. Once that

be forced to raise rates to defend their currencies when

occurred, he woke up to Sonny and Cher singing a

the Fed moves. That will increase debt service burdens on

different tune on the clock radio, and the break of a

a mountain of debt and increase the risk of an outright

new day, February 3. There are a lot of lessons in that

sovereign debt default.

metaphor for where we are and how to escape it. I would

like to believe that we have the capacity to learn them.

6 Monthly Economic Outlook: Groundhog DayEconomic forecast — December 2021

2021 2022 2023 2021:2(A) 2021:3 2021:4 2022:1 2022:2 2022:3 2022:4 2023:1 2023:2

National Outlook

Chain Weight GDP1

5.7 4.2 2.3 6.7 2.1 7.1 2.5 4.8 3.9 2.4 1.8 1.5

Personal Consumption 8.1 3.5 2.0 12.0 1.7 5.9 1.7 3.5 2.7 1.9 1.7 1.6

Business Fixed Investment 7.6 6.3 4.1 9.2 1.6 5.6 8.1 7.4 6.4 5.0 3.3 2.8

Residential Investment 8.7 -5.6 -4.9 -11.7 -8.3 -4.2 -6.3 -3.8 -0.7 -9.5 -6.8 -4.6

Inventory Investment (bil $ '12) -76 112 138 -168 -73 28 48 97 141 163 158 143

Net Exports (bil $ '12) -1258 -1288 -1240 -1236 -1304 -1274 -1298 -1286 -1289 -1278 -1264 -1245

Exports 4.3 5.5 7.5 7.6 -3.0 12.2 0.8 7.3 8.5 9.0 7.7 6.8

Imports 13.3 4.4 3.7 7.1 5.8 4.2 3.1 3.3 5.8 4.6 3.5 2.5

Government Expenditures 0.6 1.3 1.2 -2.0 0.9 -1.2 3.9 1.7 1.7 1.4 1.5 0.6

Federal 0.7 -1.5 -0.2 -5.3 -4.9 -4.1 2.0 -1.1 -0.1 -1.2 0.2 0.1

State and Local 0.5 3.1 2.1 0.2 4.7 0.6 5.0 3.5 2.9 2.9 2.2 0.9

Final Sales 5.5 3.2 2.2 8.1 0.0 5.0 2.2 3.8 3.0 2.0 1.9 1.7

Inflation

GDP Deflator 4.1 3.9 2.4 6.0 5.9 5.9 2.2 3.2 3.1 1.9 1.5 3.4

CPI 4.6 3.7 2.3 8.5 6.6 7.2 0.4 2.9 2.7 1.7 2.1 2.7

Core CPI 3.5 3.8 2.6 8.2 5.3 4.5 2.1 3.6 3.2 2.4 1.9 3.2

Special Indicators

Corporate Profits2 12.3 3.5 -1.2 45.1 20.7 12.3 7.3 0.0 -3.0 3.5 2.2 -0.7

Disposable Personal Income 2.2 -3.0 2.6 -29.1 -4.0 -5.8 -0.9 2.8 3.6 2.1 3.1 2.0

Housing Starts (mil ) 1.58 1.42 1.27 1.59 1.56 1.57 1.48 1.48 1.42 1.31 1.28 1.27

Civilian Unemployment Rate 5.4 3.7 3.5 5.9 5.1 4.3 4.2 3.7 3.5 3.5 3.5 3.5

Total Nonfarm Payrolls (thous)3

5810 764 310 1847 1883 1252 529 1006 981 540 475 321

Vehicle Sales

Automobile Sales (mil.) 3.4 3.9 4.0 3.9 3.1 2.7 3.4 3.8 4.1 4.1 4.2 4.0

Domestic 2.2 2.5 2.5 2.6 2.0 1.8 2.2 2.4 2.6 2.6 2.6 2.5

Imports 1.1 1.4 1.5 1.3 1.1 0.9 1.2 1.4 1.5 1.5 1.6 1.5

Lt. Trucks (mil.) 11.7 12.0 12.7 13.0 10.3 10.5 10.9 11.9 12.4 12.6 12.8 12.8

Domestic 9.1 9.3 9.8 9.9 7.8 8.2 8.5 9.3 9.7 9.8 9.9 9.8

Imports 2.7 2.6 2.9 3.1 2.5 2.3 2.4 2.6 2.7 2.8 2.9 3.0

Combined Auto/Lt.Truck 15.1 15.8 16.7 16.9 13.3 13.2 14.3 15.7 16.5 16.7 17.0 16.8

Heavy Truck Sales 0.5 0.5 0.4 0.5 0.4 0.5 0.5 0.5 0.5 0.5 0.4 0.4

Total Vehicles (mil.) 15.6 16.3 17.1 17.4 13.8 13.7 14.8 16.2 17.0 17.2 17.4 17.2

Interest Rate/Yields

Federal Funds 0.1 0.3 1.3 0.1 0.1 0.1 0.1 0.2 0.4 0.7 0.9 1.2

10-Year Treasury Note 1.5 2.1 2.7 1.6 1.4 1.5 1.6 1.8 2.3 2.5 2.6 2.7

Corporate Bond BAA 3.4 3.9 4.6 3.6 3.3 3.3 3.6 3.6 4.2 4.3 4.5 4.6

Exchange Rates

Dollar/Euro 1.19 1.18 1.21 1.21 1.18 1.15 1.16 1.17 1.18 1.20 1.20 1.21

Yen/Dollar 109.9 113.0 110.4 109.5 110.1 114.1 113.7 113.2 112.7 112.2 111.5 110.7

1.

in 2020, GDP was $18.4 trillion in chain-weighted 2012 dollars.

2.

Corporate profits before tax with inventory valuation and capital consumption adjustments, quarterly data represents four-quarter percent change.

3.

Total nonfarm payrolls, quarterly data represents the difference in the average from the previous period. Annual data represents 4Q to 4Q change.

Quarterly data are seasonally adjusted at an annual rate. Unless otherwise specified, $ figures reflect adjustment for inflation. Total may not add up due to rounding.

Copyright © 2021 Diane Swonk – All rights reserved. The information provided herein is believed to be obtained from sources deemed to be accurate, timely and reliable. However, no assurance is

given in that respect. The reader should not rely on this information in making economic, financial, investment or any other decisions. This communication does not constitute an offer or solicitation, or

solicitation of any offer to buy or sell any security, investment or other product. Likewise, this communication serves to provide certain opinions on current market conditions, economic policy or trends

and is not a recommendation to engage in, or refrain from engaging, in a particular course of action.

“Grant Thornton” refers to Grant Thornton LLP, the U.S. member firm of Grant Thornton International Ltd (GTIL), and/or refers to the brand under which the GTIL member firms provide audit, tax and

advisory services to their clients, as the context requires. GTIL and each of its member firms are separate legal entities and are not a worldwide partnership. GTIL does not provide services to clients.

Services are delivered by the member firms in their respective countries. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another’s acts or

omissions. In the United States, visit grantthornton.com for details.

© 2021 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

7 Monthly Economic Outlook: Groundhog DayYou can also read