Department of Local Government Finance Budget Workshops, Gateway, and Budget Adoption - Fred Van Dorp Budget Division Director ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Department of Local Government Finance

Budget Workshops, Gateway, and

Budget Adoption

Fred Van Dorp

Budget Division Director

fvandorp@dlgf.in.gov

317-234-3937

Agenda

• DLGF Summer Budget Workshops Recap

• Calendar Overview

• Form 3 Overview and Best Practice

• CNAV

• Binding Units

• Form 4 Overview and Best Practice

2

Summer Budget Workshops

• From July 19 through August 30, the Department conducts

voluntary summer budget workshops. This is an opportunity to

meet with your Department’s Budget Field Representative to

discuss budget concepts, statutory or procedural changes,

deadlines.

• Units can also request that the Department uploads the Current

Year Financial Worksheet, Form 2, Form 4B, and Form 3 into

Gateway.

• Through August 13, 2021, the Department has completed:

• Number of Workshops: 1402

• Number of Uploads: 813

3

Summer Budget Workshops

• While Summer Budget Workshops are designed to help units get

off to a fast start for the budget cycle, there are additional steps,

both inside and outside of Gateway, that must be completed after

the workshop in order to successfully adopt a budget.

• The Department’s Budget Field Representatives (“FRs”) will

provide a listing of these steps with a memo called “2022 Budget

Submission and Review to be Completed in Gateway.”

4Gateway - Budget

• Approximately 60% of Summer Workshops end with the

Department uploading data into Gateway on behalf of the unit.

• Whether a local official uses the Department upload or manually

enters their information, they must still review and submit their

budget information.

• Gateway Budget uses a visual cue to identify which form(s) have

been submitted. Units can use this visual cue to quickly identify

where they are in the process for each form.

5• On the budget main menu, all forms initially highlighted in yellow.

• If a unit manually populated all required fields or if the unit received a

DLGF upload, the menu will still be highlighted in yellow until the Form is

submitted.

6• Once a Form is submitted, the highlight will change to green.

• As a rule, by the of the end of budget cycle, all Forms should be

highlighted in green.

• The Debt Worksheet is the exception to this rule. For units without

debt, this Form will still be yellow at the end of the cycle.

7Form 3 and Budgetnotices.in.gov

8Form 3 – Notice to Taxpayers

• The Form 3 (Notice to Taxpayers) is often the first budget form to

be submitted.

• IC 6-1.1-17-3 requires online advertisement of the Notice to

Taxpayers to be submitted at least 10 days before the public

hearing.

• Online advertisement will be completed by submitting the Form 3

from the Budget Form Menu in Gateway.

• Once submitted, the online advertisement will be available at:

www.budgetnotices.in.gov.

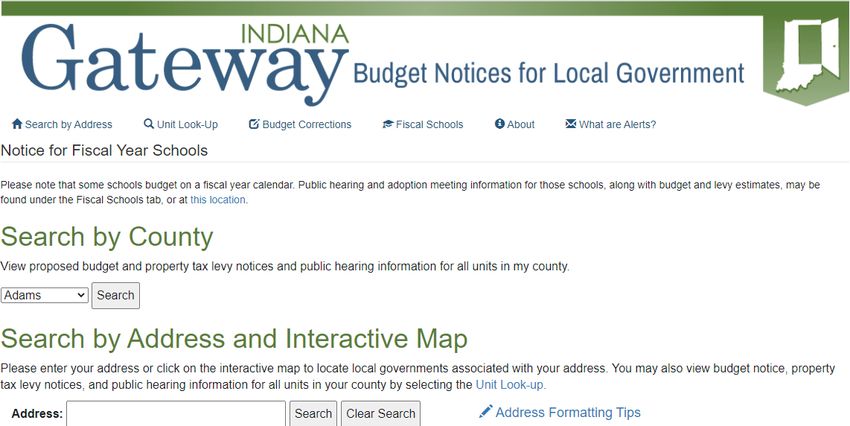

9Budget Notices

• The advantage of the online advertisement is that it gives the

Department the ability to consolidate and post all Notices to

Taxpayers in a single centralized location.

• Taxpayers, local government officials, and legislators can search

all notices by address, county, taxing unit, or taxing district.

• Taxpayers, local government officials, and legislators can sign up

for email notifications for new notifications being posted.

10• Budget Notices for Local Government is a single centralized

location where you can search for information about the public

hearings for all units Statewide.

11• By clicking the “Alert Me” field, you can enter an email address to

receive an automatic alert when the Notice to Taxpayers

information is available.

12• Using the search by county feature, we can see which units have

officially submitted their Notice to Taxpayers.

• The Form 3 is summarized and will show the current year levy,

ensuing year’s proposed budget, ensuing year’s proposed levy,

and dates for the public hearing and adoption meeting.

13• Budget Notices also lists the units have not yet submitted their

Form 3 in Gateway.

• Once the Form 3 is submitted, the levy, budget, public hearing,

and adoption meeting information will be populated.

14Form 3 – Template and Analysis

15Form 3 – Notice to Taxpayers

• The Form 3 contains:

• Date, Time, Location for Public Hearing

• Date, Time, Location for Adoption Meeting

• Estimated Maximum Levy and DLGF Estimated Property Tax

Cap Credit (Circuit Breaker)

• Fund, Ensuing Year Budget Estimate, Ensuing Year Property

Tax Levy, Estimated Levy Excess appeals, Current Year

property tax levy, Comparison of current year and ensuing

year Levy.

16• The first section of the Form 3 contains the details for date, time,

and location for both the public hearing and the adoption

meeting.

17Form 3 – Rescheduled Hearings/Meetings

• During the budget cycle, it is not enough to just have a public

hearing or an adoption meeting, units must keep their taxpayers

informed of where/when they will be discussing the budget.

• While we all try to plan for all contingencies, occasionally a unit

may need to change the date, time, or location of their budget

meetings.

• If a public hearing or adoption meeting’s date, time, or location

changes, the Form 3 must be updated to reflect those changes. If

you need to make any changes to the Form 3, contact your DLGF

Field Representative.

18• The second section of the Form 3 includes the estimated

maximum levy and the DLGF estimate property tax cap credit

(circuit breaker loss) for the ensuing budget year.

19• The third section of the Form 3 contains a listing of the funds and the

proposed budgets and levies for the ensuing year.

• The information in Columns 2 and 3 can be entered manually or by

drawing information from the advertised column of the Form 4B.

• The section must include all funds, including home rule funds, that a

unit will be spending against in the ensuing budget year.

20• The values on the Form 3 will create a maximum approval amount

for the ensuing budget year.

• The Department cannot certify a budget or levy that is higher

amount listed on the Notice to Taxpayers.

21• Column 1 - Listing of the specific funds that will be used in the

ensuing budget year.

• Column 2 - The proposed budget for the ensuing year.

• Column 3 - The amount of property tax that will be raised for a

given fund in the ensuing year.

• Column 4 - The amount of any proposed excessive levy

appeals that will be applied to the fund.

22• Column 5 - The current year’s certified levy.

• Column 6 - Column 6 demonstrate the change in property tax

levy from the current year to the ensuing year.

Fund 0101 is using 6.13% less levy this cycle.

Fund 0840 is using 37.25% more levy this cycle.

23Form 3 – Best Practices

• Check your meeting dates for holidays, vacations, or other times

when you may not have a quorum.

• Run the Error Prevention Report prior to submitting your Form 3.

• Compare your levies to the maximum levy

• Review Column 6 prior to submitting your Form 3.

• Compare the ensuing year Form 3 to either the current year Form

3 or to the current year Budget Order.

24Certified Net Assessed Value

25Certified Net Assessed Value

Date Description

August 2 Last day for county auditor to certify net assessed values (“CNAV”) to the

Department. The Department will make AV visible to every political subdivision via

Gateway. All units are encouraged to validate the AVs certified by the county

auditor. (IC 6-1.1-17-1)

• The Gross Assessed Value of most property is determined locally

by the County Assessor.

• The Assessor rolls the Gross Assessed Values to the Auditor and

the Auditor applies the exemptions and deductions to each parcel

to determine the Net Assessed Value.

• Auditor certifies the Net Assessed Values to the Department.

26Public Gateway - CNAV

• Once the County Auditor certifies the NAVs to the Department, the

Department will make the information available to taxpayers and

local government officials through Gateway.

• Gateway - https://gateway.ifionline.org/report_builder/

• Certification of Net Assessed Values by District

• Certification of Net Assessed Values - Detail by District and

Fund

27Budget Order - CNAV

• The Department will provide all units with their Certified Budget

Order by December 31/January 15.

• The Budget Order is a summary of the decisions, financial

priorities, and funding for each unit.

• Of all the information on the Budget Order, the CNAV is the first

value available.

• Randolph County certified their NAVs on 07/09/2021.

28Certification of Net Assessed Values by District

• Certification of Net Assessed Values by District

• Detailed overview of all taxable property.

• Information is presented at the taxing district or the geographic

area level.

• A taxing unit’s tax base can include one or more taxing

districts.

29• The Adjusted Net AV column represents the value of all taxable property in

a taxing district.

• The Department will use this value to calculate each unit's tax rate.

30• While the Adjusted Tax Rate is the final figure, the report contains

a summary of what types of property make up the tax base.

31• The “AV TIF Real Estate” and “AV TIF PP” represent the value of

Incremental TIF assessed value.

• These columns represent AV in county, but these values are not included

32• County auditor may withhold a portion of the taxable property as a

bulwark for potential AV reductions.

• This column represent AV in county, but the values is not included in the

33• The AV TIF Release, or TIF Passthrough, is included as an informational

column to differentiate between permanent and temporary growth.

34• The AV Annex Change is included as an informational column to report

increases or decreases associated with annexations.

35Certification of Net Assessed Values - Detail by

District and Fund

• This reports uses the Adjusted Net AV column at the taxing district

level, but presents the AV by fund for each unit.

• The report also shows the total Net Assessed Value for every fund

the unit uses.

• Units that cover multiple taxing districts, can determine which

areas are currently increasing and decreasing in AV.

36• The Library above’s tax base is spread across two different taxing

districts.

• The “Certification of Net Assessed Values - Detail by District and

Fund” shows the CNAVs for each taxing district, and the total

CNAV for each fund.

37CNAV – Best Practice

• Each year, there are taxing units that identify AV issues during

their 1782 windows or once the Budget Order is certified.

• The Department encourages all units compare use their current

year 1782 or current year Budget Order to the two public CNAV

reports on Gateway.

• If there questions about any of the increases, decreases, and/or

values presented, reach out to the County Auditor to discuss any

discrepancies.

38Binding Units

39Binding Units

Date Description

September Last day for units with appointed boards, including certain libraries, to submit

1 proposed 2022 budgets, tax rates, and tax levies to the appropriate fiscal body for

binding adoption. (IC 6-1.1-17-20; IC 6-1.1-17-20.3)

• There are approximately 220 binding units around the State.

These are units, who receive a certified budget order, but do not

have an elected board to adopt their budget.

• This list includes fire district, airport authorities, solid waste

districts, various sanitary districts, public transportation providers.

• This will also apply to certain libraries and schools around the

State. 40Binding Units

Date Description

September Last day for units with appointed boards, including certain libraries, to submit

1 proposed 2022 budgets, tax rates, and tax levies to the appropriate fiscal body for

binding adoption. (IC 6-1.1-17-20; IC 6-1.1-17-20.3)

• While another fiscal body is responsible for the final budget

adoption, each Binding Unit is responsible for completion and

submission of all Budget Forms in Gateway.

• While non binding units will have access to Gateway through

November, binding units must complete their forms by September

1 at midnight.

41Binding Units/Adopting Bodies

• Binding Units

• Continue to populate the budget data into Gateway.

• Work with your fiscal body to coordinate the dates and times

that will be included on the Form 3.

• Adopting Bodies

• Continue to monitor the binding unit’s progress in Gateway.

• Work with your binding units to coordinate the dates and times

that will be included on the Form 3.

42Deadlines

432021 Budget Calendar Overview

Date Description

Oct. 12 Last day to post notice to taxpayers of proposed 2021 budgets and net tax levies

and public hearing (Budget Form 3) to Gateway.

(IC 6-1.1-17-3)

Oct. 22 Last possible day for taxing units to hold a public hearing on their 2021 budgets.

Public hearing must be held at least ten days before budget is adopted.

(IC 6-1.1-17-5)

Note: This deadline is subject to scheduling of the public hearing.

Nov. 1 Deadline for all taxing units to adopt 2021 budgets, tax rates, and tax levies.

(IC 6-1.1-17-5(a))

Note: This deadline is subject to the public hearing.

Nov. 8 Last day for units to submit their 2021 budgets, tax rates, and tax levies to the

Department through Gateway as prescribed by the Department.

44Form 4

• Form 4 is the official ordinance the fiscal body signs to formally

adopt the budget.

• Form 4 contains:

• Fiscal body name, fiscal body type, and budget adoption date

• Listing of all funds, both certified and home rule, that the unit

will be spending against in the ensuing budget year

• List of the fiscal body members, their vote, and their signature

• Attestation line used by certain units during budget adoption

• Information related to planned debt issuances and shortfall

appeals

45• General overview of the group responsible for the budget

adoption include date of the adoption.

• The Department will confirm that the adoption date matches the

adoption meeting date from the Form 3.

46Form 4

• An important component of the Form 4 is the listing of the

budgets, levies, rates for all funds that the unit will use in the

ensuing year.

• This will include both the DLGF Certified Funds and Home Rule

funds.

• The Form 4 will default information loaded onto the adopted

column on the Form 4B.

47• All DLGF reviewed Funds will appear on the Certified Budget

Order.

• These funds must include an adopted budget, tax levy, and tax

rate.

48• Home Rule funds will not appear on the Department’s budget

order.

• Home Rule funds will only include an adopted budget.

49• During the Budget Adoption, the fiscal body members must both

indicate their vote (Aye, Nay, Abstain) and sign the form.

50• The questions above are the newest additions to the Form 4.

• The Department uses the answers to these questions to collect

information about two potential future actions.

• If a unit declares their intent to issue debt in December or to file a

shortfall appeal, the Department will know that there is additional

information that the unit will need to provide before we can work

their budget.

• By marking “Yes” to either of these questions, the DLGF Budget

certification deadline moves to January 15 for the entire county.

51Best Practice – Form 4

• Run the Error Prevention Report

• Compare the budgets and levies to the Form 3 to make sure all

data has successfully pulled onto the Form 4.

• Compare the budgets, levies, and tax rates to the current year

budget or current year Form 4.

• Confirm that any funds with a budget, levy, and tax rate of 0.00

are consistent with your expectations.

• Review the adoption date on the Form 4 to the adoption meeting

date on the Form 3.

52Contact Us

53Resources

• DLGF Webinars: https://www.in.gov/dlgf/continuing-

education/webinars/

• Training Videos

• www.youtube.com/user/DLGFgateway

• https://www.in.gov/dlgf/budget-forms-and-information/

• User Guides

• Information Icons

• DLGF Memos

• https://www.in.gov/dlgf/memos-and-

presentations/memos/

• Email

• Call 54Contact Us

Website: www.in.gov/dlgf

Contact Us: https://www.in.gov/dlgf/contact-us/

Budget Field Representative Map:

https://www.in.gov/dlgf/files/Budget_Field_Reps.pdf

Gateway Support: Support@dlgf.in.gov

DLGF Customer Service Survey: Customer Survey

55You can also read