2018 Spring Update Customer Service - WE MAKE ENERGY HAPPEN - Williams

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

WE MAKE ENERGY HAPPEN

2018 Spring Update NYSE: WMB

williams.com

Customer Service

Forward-looking Statements

> The reports, filings, and other public announcements of Williams Partners L.P. (WPZ) and Transcontinental Gas Pipe Line Company, LLC (Transco) may

contain or incorporate by reference statements that do not directly or exclusively relate to historical facts. Such statements are "forward-looking

statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as

amended. We make these forward-looking statements in reliance on the safe harbor protections provided under the Private Securities Litigation Reform Act

of 1995. Forward-looking statements can be identified by various forms of words such as “anticipates,” “believes,” “seeks,” “could,” “may,” “should,”

“continues,” “estimates,” “expects,” “forecasts,” “intends,” “might,” “goals,” “objectives,” “targets,” “planned,” “potential,” “projects,” “scheduled,” “will,”

“assumes,” “guidance,” “outlook,” “in service date” or other similar expressions. These forward-looking statements are based on management's beliefs and

assumptions and on information currently available to management and include, among others, statements regarding:

– Our and our affiliates future credit ratings;

– Amounts and nature of future capital expenditures;

– Expansion and growth of our business and operations;

– Financial condition and liquidity;

– Business strategy;

– Cash flow from operations or results of operations;

– Rate case filings;

– Seasonality of certain business components

– Natural gas, natural gas liquids, and olefins prices, supply, and demand; and

– Demand for our services

> Forward-looking statements are based on numerous assumptions, uncertainties and risks that could cause future events or results to be materially different

from those stated or implied in this presentation. Many of the factors that will determine these results are beyond our ability to control or predict. Specific

factors that could cause actual results to differ from results contemplated by the forward-looking statements include, among others, the following:

– Availability of supplies, market demand, and volatility of prices;

– Inflation, interest rates, and fluctuation in foreign exchange rates and general economic conditions (including future disruptions and volatility in the

global credit markets and the impact of these events on customers and suppliers);

– The strength and financial resources of our competitors and the effects of competition;

– Whether we are able to successfully identify, evaluate and execute investment opportunities;

– Our ability to acquire new businesses and assets and successfully integrate those operations and assets into our existing businesses as well as

successfully expand our facilities;

– Development of alternative energy sources;

– The impact of operational and developmental hazards and unforeseen interruptions;

– Costs of, changes in, or the results of laws, government regulations (including safety and environmental regulations), environmental liabilities,

litigation, and rate proceedings;

2

Forward-looking Statements (cont’d)

– Williams’ costs and funding obligations for defined benefit pension plans and other postretirement benefit plans;

– Our allocated costs for defined benefit pension plans and other postretirement benefit plans sponsored by our affiliates;

– Changes in maintenance and construction costs;

– Changes in the current geopolitical situation;

– Our exposure to the credit risk of our customers and counterparties;

– Risks related to financing, including restrictions stemming from debt agreements, future changes in credit ratings as determined by nationally-recognized

credit rating agencies and the availability and cost of capital;

– The amount of cash distributions from and capital requirements of our investments and joint ventures in which we participate;

– Risks associated with weather and natural phenomena, including climate conditions and physical damage to our facilities;

– Acts of terrorism, including cybersecurity threats and related disruptions;

– Additional risks described in our filings with the Securities and Exchange Commission (SEC)

> Given the uncertainties and risk factors that could cause our actual results to differ materially from those contained in any forward-looking statement, we caution

investors not to unduly rely on our forward-looking statements. We disclaim any obligations to and do not intend to update the above list or announce publicly the

result of any revisions to any of the forward-looking statements to reflect future events or developments.

> In addition to causing our actual results to differ, the factors listed above may cause our intentions to change from those statements of intention set forth in this

presentation. Such changes in our intentions may also cause our results to differ. We may change our intentions, at any time and without notice, based upon

changes in such factors, our assumptions, or otherwise.

> Investors are urged to closely consider the disclosures and risk factors in WPZ’s and Transco’s annual reports on Form 10-K filed with the SEC on Feb. 25, 2015,

and each of our quarterly reports on Form 10-Q available from our offices or, in the case of WPZ, from our websites at www.williams.com and

www.investor.williams.com

3

Commercial Operations - Customer Services

Gary Duvall

VP Transco

Commercial

Hector Alatorre

Director

Customer Services

Keith Higginbotham John Cassapo Suzanne Heiser

Bill Eiser Martha Janousek

Manager Laurie Catlett

Manager

Leads

Business Business

Development – Development – Customer Service

Customer Service Production Area Market Area Contracts Transportation

Marketing

Paul Prodoehl

Toi Anderson

Celyna Ebohon

Cindy Hungate

Laarni Hernandez

Andrea Beltran

Karen Gallardo

James Corley

Liz Hughes

Contract Analysts

Sean Xin

Customer Service

Representatives

4

Strategic Asset Position

CONNECTING THE BEST

SUPPLIES

Marcellus-Utica,

Gulf Coast

TO THE BEST MARKETS

New York City, Washington

D.C., Philadelphia, Florida,

Atlanta, LNG export

• Nations largest-volume interstate

pipeline system

• 9,700 miles of pipeline with 14.98

MMdth of gas per day for system-

wide delivery capacity (As of

12/31/17)

• 50 compressor stations, four

underground storage fields and

one LNG storage facility

• Competitively positioned between

strong supply and demand areas

along eastern seaboard

5

Transco Peak Day Deliveries and System Capacity

Note: Includes all system deliveries and all Zones.

6

Weather

Location January 4, 2018 January 5, 2018 January 6, 2018

High / Low High / Low High / Low

New York 29 / 19 19 / 9 13 / 6

Charlotte 34 / 18 36 / 8 34 / 12

Atlanta 35 / 20 38 / 16 39 / 20

Tampa 56 / 38 60 / 35 61 / 41

7

Peak Day Delivery Quantities by State

3,500

3,000

2,500

MMscfd

2,000

1,500

1,000

500

0

TX LA MS AL GA SC NC VA MD PA NJ NY

1/5/2018 1/8/2017 1/18/2016

8

Takeaways From Winter &

Opportunities Going Forward

> Transco system was stressed, but performed well. Many teams worked long hours managing equipment

issues, storage changes, gas scheduling activity, etc.

> Peak day occurred on a Friday which allowed the system to recover over the weekend.

> OFO issuance and limitations on availability of non-primary firm transportation helped manage capacity

and system suppliers performed well given the temperatures and potential production freeze off issues.

> The Transco system continues to expand and has transformed into a bi-directional system, highlighting the

need for additional collaboration between Pipeline Control and Operations and customer activity driving

dynamic system operations, requiring frequent operating changes.

> Large deliveries dependent on a fixed set of assets requiring timely and frequent communication and

coordination, both internal and external.

> Increase opportunities for dialogue and collaboration between Pipeline Control and customers, better

understanding their needs and enhancing operating relationships.

> Opportunities for additional pipeline control focus and engagement on near and longer term system

outage and modernization needs.

9

Supply / Demand Forecast: 2016-2021

Anadarko, Arkoma and Appalachian Basin

+15

23 38

+1 +1 +2

14 15 11 12 15 17

+1

13 14

+3

35 38 +10 +3

26 36 12 15

Regional Production change,

2016 to 2021 (Bcf/d) (1)

Regional Demand change,

2016 to 2021 (Bcf/d) (1)

(1) Size of bubble indicates magnitude of 2021 production or demand

Source: Wood Mackenzie 1H 2017, excludes impact of net Canadian imports.

Data contained in this slide is property of Wood Mackenzie. Per Williams’ agreement, data may only be used for

individual customer meetings unless prior consent is received. Do not duplicate or alter information in any way.

10Receipt

or

Volume (MMscf)

Receipt or Receipt / Delivery / Net Supply Overview

Lateral 04-01-2016 to 04-01-2017 to

% Chg

03-31-2017 03-31-2018

McMullen 61 / (17) / 44 61 / (33) / 28 (36%)

CTGS 204 / (96) / 108 164 / (29) / 135 25% Leidy

SWLA 105 / (80) / 25 82 / (852) / (770) (3180%) Lambertville

CENLA 102 / (5) / 97 121 / (9) / 112 15% Rivervale

Lower Chanceford

Zone 3 M/L Total 751 1,503 100%

Pleasant Valley

SELA 185 / (92) / 93 138 / (52) / 86 (8%)

Zone 6

Sta85 Receipts 2,110 2,399 14% Nokesville

Mobile Bay 559 / (1,333) / (774) 517 / (1,198) / (681) (12%)

Boswells Tavern

Black Warrior 25 31 23%

Cascade Creek 109 125 15%

Boswells Tavern 176 95 (46%) Cascade Creek

Nokesville 68 66 (4%)

Zone 5

Pleasant Valley/Cove 75 66 (12%)

Point

Lower Chanceford 828 846 2%

Sta85 Receipts

Lambertville 67 72 7% Peak Day Information

Rivervale 213 209 (2%) Peak Day deliveries to Cheniere affect SWLA and

Zone 4 Mainline interconnects in Zone 3.

Leidy 2,976 / (972) / 2,004 3,107 / (983) / 2,124 6%

Black Warrior Station 85 receipts at 3.3 BCF.

Zone 3 Mobile Bay flow southward peaks as Florida sees

Zone 2

peak conditions.

Mobile Bay

Large increases in numerous mid Atlantic receipts as

Zone 1 gas demand rises in Zone 5.

McMullen

SWLA Large decrease in deliveries to Elba.

SELA

Cove Point Pipeline sends over 500 MMCF to

CENLA

CTGS Transco.

Leidy receipts at over 4.0 BCFMarket Transitions Drive More Volume Southward

Sta090

Northbound Flow

Sta130

Sta065

Sta165

Sta030

Southbound Flow

Sta195

Sta045

12Transco Deliveries to End Users by State

2,000,000

1,800,000

1,600,000

1,400,000

1,200,000

Dth

1,000,000 2013

2014

800,000 2015

2016

600,000 2017

400,000

200,000

0

13Growth Volumes Well Balanced Among Customers

LDC / Industrial LNG Exports

19% 23%

Distribution of total

volume growth (7.2

Bcf/d) for 2017 to 2020

32% 26%

Producer Power Generation

14Leidy Line & Wharton Storage Update &

System Maintenance

Leidy Line

> Transco has completed the requirements of the Corrective Action Order (CAO).

> In addition to CAO compliance activities, integrity testing was also performed on other pipelines on the Leidy system.

This includes over 325 miles of pipeline.

> The tests included the use of various pigging technologies, hydrotests, etc.

> All of Transco Leidy Lines are back to normal operations.

Wharton Storage

> Transco is currently undertaking a comprehensive assessment of Station 535, the storage field and the related injection

and withdrawal lines to and from storage.

> The target is to have the assessments and all necessary repairs complete on both the storage field and the compressor

station in time to provide service for the 2018-2019 withdrawal season.

> The objective of the assessment is to ensure that that all of the Wharton Storage Facilities continue to operate in a safe

and reliable manner once the repairs are complete and placed back in service.

> Transco intends to continue to implement measures designed to mitigate potential impacts of this event on its ability to

provide Rate Schedule GSS service.

> We will keep you appraised of any additional developments, including any limitations on the availability of storage

services provided under Rate Schedule GSS.

System Maintenance

> Williams takes steps for prevention measures through a continual Operations and Maintenance Program.

> Schedule found at www.1Line.Williams.com.

15Modernization Program

> Modernization Program – Evaluation

– A strategic and defined program to upgrade and/or replace HP/Compression and

pipeline facilities that

• Require replacement based on risk profile

• Require upgrades to meet new / emerging PHMSA and EPA rules

• Provides reliability improvements to meet current and future flow conditions

– Focuses on capital optimization that evaluates systems with a life-cycle viewpoint

– An evaluation of the various cost recovery methods acceptable to FERC policy (PL15-

01-000)

– Transco will continue to keep Customers updated on the progress of the modernization

program

16Priority of Service Summary

> No-notice priorities of service offered by Transco: Traditional, Non-Traditional, Secondary

and IT to continue providing additional flexible service

– Flexible services will continue to be available when operationally feasible

– Only Traditional and IT no-notice are provided by current tariff in Section 5.1 (b) of Rate Schedule FT, FTG, FDLS

and IT

> No-notice is related to the primary contract path

– Supported in current tariff in Section 4.7 of Rate Schedule FT, FTG, and FDLS

> Removal of Path for HBLV no-notice requests without a supply of gas

– No-notice is received and delivered at the point of delivery and is supported by Section 5.1 (b) of Rate Schedule FT,

FTG, and FDLS

> Imbalances held in zone of receipt; HBLV no-notice receipt is at the SSDP

– No changes to Imbalance Resolution GT&C Section 25 or Cash Out GT&C Section 37

> No additional capacity needed to use Station 95 Pool; No transportation fee or fuel

between Station 85 and Station 95 transactions

– Segmentation allows shipper to relocate low burn requests from OIA 1 to OIA 2

– Proposed tariff changes to GT&C Sections 28, 37, 51 and 52 to accommodate additional Station 95 pool in Zone 4

> Transportation and fuel charges assessed as provided in current tariff

– No additional charges are proposed for transactions on system

17Regulatory Update

> On March 16, 2018, Transco filed to change the pooling rules in its tariff effective October 1, 2018 to

begin charging commodity and fuel rates on transactions leaving the zones 5 & 6 pools rather than

applying those charges to transactions going into those pools. The proposed change will make

Transco’s pooling rules consistent at all of its market area pools.

> On March 27, 2018, Transco filed an application with the Commission to abandon approximately 1.4

bcf of Eminence capacity effective April 1, 2018, due to the company’s decision to operate the

caverns at a lowered pressure.

> On March 15,2018, the Commission issued a revised Policy Statement in Docket No. PL17-1-000,

which revises its policy regarding the recovery of income tax costs in rates of jurisdictional natural

gas pipelines. Because the Commission found that an impermissible double recovery results from

granting a Master Limited Partnership (MLP) pipeline both an income tax allowance and a return on

equity pursuant to the discounted cash flow methodology, the Commission revised its policy and will

no longer permit an MLP to recover an income tax allowance in its cost of service. The Commission

further found that, while all partnerships seeking to recover an income tax allowance will need to

address the double-recovery concern, the Commission will address the application of its revised

Policy Statement to non-MLP partnership forms as those issues arise in subsequent proceedings.

> The Commission also issued a contemporaneous Notice of Proposed Rulemaking in Docket No.

RM18-11-000, that proposes a process that will allow it to determine which jurisdictional natural gas

pipelines may be collecting unjust and unreasonable rates in light of the recent reduction in the

corporate income tax rate in the Tax Cuts and Jobs Act and the FERC’s revised Policy Statement.

Transco is evaluating the impact of these issuances on its business.

18Rate Case Update

> As agreed in Article VI of the Stipulation and Agreement in Docket No. RP12-993, et al.,

Transco will file a NGA Section 4(e) general rate case no later than August 31, 2018.

> Assuming that the filing date is August 31, 2018, the base period for the rate case will be

June 1, 2017 – May 31, 2018 and the test period will be June 1, 2018 – February 28,

2019.

> Assuming a full five month suspension period for the new rates, the effective date of the

rates will be March 1, 2019.

19Unsubscribed Capacity

FT Capacity

313,850 FT; Non-seasonal; Mobile Bay MP261 to Pooling Station 85 Z4A

37,346 FT; Non-seasonal; Southeast Louisiana Lateral Station 62-65

3,763 FT (ACQ) Available 8/1/2018; Seasonal (March 1- November 30) Telescoped

Capacity

Washington Storage

124,200 dt Storage Capacity; Withdrawal 1,307 dt/d; Injection 690 dt/d.

available 5/1/2018.

262,678 dt Storage Capacity; Withdrawal 2,765 dt/d; Injection 1,459 dt/d.

available 8/23/2018, pending the outcome of an open season.

Eminence EESWS

62,201 dt; Withdrawal 7,446 dt/d; Injection: 621 dt/d.

Eminence ESS Rate Schedule

2,018,705 dt; Withdrawal: 239,949 dt/d; Injection: 20,042 dt/d.

54,996 dt; Withdrawal 6,518 dt/d; Injection 544 dt/d. available 11/1/2018, pending the

outcome of an open season.

47,484 dt; Withdrawal 5,684 dt/d; Injection 474 dt/d. available 3/1/2019, pending the

outcome of an open season.

20Atlantic Sunrise (ASR) Project – 1Line Changes

> New “ROUTE” data element will be added to 1Line with the ASR Project in-service date

– The Atlantic Sunrise (ASR) project will include the new Central Penn Line South (CPLS), giving

shippers an alternate route option for some Zone 6 transactions.

• A NAESB nomination element, ROUTE, will be required for affected Zone 6 transactions and will be effective with the

ASR Project in-service date.

• Valid Route options will be displayed in 1Line for affected nominations and secondary capacity release transactions.

• EDI and Flat File formats will include the new ROUTE option. To ensure EDI files work correctly, customers must

participate in testing.

• Presentations with more details on the new ROUTE element, including EDI and Flat File testing information:

– http://www.1line.williams.com/Transco/files/EDIASRCommunication.pdf

– http://www.1line.williams.com/Transco/files/presentations/NewNominationDataFieldWebinar.pdf

> River Road Transfer Point

– The junction of the new Central Penn Line South (CPLS) and Transco’s mainline, north of Station 195

will be a Transfer Point

• Delivery and Receipt volumes at the Transfer Point must match for each transaction.

• “Lesser of” rule will apply for out of balance transactions across Transfer Point

• Transport charges will apply on both deliveries to and receipts from Transfer Point

21Atlantic Sunrise (ASR) Project – 1Line Changes

> Nominations and non-ASR secondary Leidy -

capacity releases with paths that cross or Dominion

are within any of the red brackets require

Sta. 517

Route selection.

> 3 Route Options

– Non-CPLS: transaction moves on the

North-CPLS

Mainline or Leidy Line only

– South-CPLS: transaction moves DOWN

CPL-South (CPLS)

the CPLS to the Mainline

– North-CPLS: transaction moves UP the 210 Pool

South-CPLS

CPLS to the Leidy Line

> Valid Route options will be displayed in

1Line.

> No Route option for:

– Transactions with paths that do not cross

into the bracketed triangle Sta. 195

River Road

– Primary capacity releases Zone 6 Transfer

– Secondary capacity releases of ASR

contracts Zone 5 BG&E

22Major Expansion Projects

Gateway Project Mdt/d

Pre-construction Atlantic Sunrise Q1 2021

Rivervale Atlantic Sunrise 1,700

Under construction Mid 2018

Q4 2019

In Service Garden State 180

Garden State

Q3 2017 / Q1 2018 Gulf Connector 475

St. James Supply 162

Southeastern Trail Northeast Supply

Q4 2020 Q4 2019 / Q1 2020 NESE 400

Hillabee – Phase II 207

Hillabee Phase 2 Rivervale South to Market 190

Q2 2020 Southeastern Trail 296

Gulf Connector Gateway 65

Q1 2019

Total Expansion Capacity 3.26

Current Transco Capacity* 14.98

Total Post-Expansions 18.24

St. James Supply

Q2 2019 * Includes 20 MDth/d for Garden State and

400 MDth/d for Atlantic Sunrise placed in service in 2017

23Northern Market: Continuing Strong Growth

Rivervale South to

Market New York Bay

• 195 Mdt/d • 115 Mdt/d

• Q4 2019 • October 6, 2017

Leidy Hub

Gateway New York City

• 65 MDth/d

• Q1 - 2021

Atlantic Sunrise

• 1,700 Mdt/d

• Mid 2018 210 Northeast Supply

Enhancement

• 400 Mdt/d

• Q4 2019 / Q1 2020

195

Garden State

• 180 Mdt/d

• March 23, 2018

VA

Note: In-service dates and capacities for projects not yet in service represent expected in-service dates and capacities

24Power Generation Fuels Southern Market Expansions

Virginia Southside II

• 250 Mdt/d

• December 1, 2017

165

Dalton Expansion

160

• 448 Mdt/d

• August 1, 2017

Hillabee Expansion Ph I

• 818 Mdt/d

• July 11, 2017 Southeastern Trail

• 296 Mdt/d

• Late 2020

Hillabee Expansion Ph II

85 • 207 Mdt/d

• Q2 - 2020

Note: In-service dates and capacities for projects not yet in service represent expected in-service dates and capacities

25Gulf Coast Area Expansions Serving LNG and

Industrial Customers

65

Gulf Connector

• 475 Mdt/d

• 1st half 2019 50

45 St. James Supply

• 161 Mdt/d

• Q2 2019

30

Gulf Trace

• 1,200 Mdt/d

• February 1, 2017

Note: In-service dates and capacities for projects not yet in service represent expected in-service dates and capacities

26LNG Opportunities

Gas Flows to Sabine Pass in Bcf/d

> Contracted with four of six

3.5

LNG facilities currently 3.0

Daily

in-service or under 2.5

construction (~2 Bcf/d) 2.0

1.5 LNG

– Market access to the other two 1.0

0.5

export facilities -

> Contracted with Sabine

Pass Liquefaction; took

delivery of nearly 90 Bcf

in Nov. 2017 LNG

> Seven additional projects

in development to

LNG

support LNG exports LNG

LNG

LNG

Sabine Pass, Contracted

Other Contracted

Market Access

27Eastern Interstates – Projects in Execution

We are currently executing a total of 10 different expansion opportunities

Constitution

Q3 2019

Station 240 Modernization

Q4 2019

New York Bay Expansion

Rivervale South to Market Q4 2017

Q4 2019

NE Supply Enhancement

Gateway Q4 2019 / Q1 2020

Q1 2021

Atlantic Sunrise Garden State Phase I

Mid 2018 Q3 2017

Garden State Phase II

Southeastern Trail Q1 2018

Q4 2020

Virginia Southside II

Q4 2017

Gulf Trace Dalton Expansion

Q1 2017 Q3 2017

Gulf Connector

Q1 2019

Projects shaded in yellow are Hillabee Phase 1

starting or under construction. Q3 2017

Projects shaded in green are in

service. Stars represent power St. James Supply Hillabee Phase 2

generation Q2 2019 Q2 2020

Shipper FERC Certificate FERC FERC Major

Construction In-service

Commitments Application Filed EIS / EA Certificate

Activities

REGULATORY MILESTONES FOR FULLY CONTRACTED REGULATED EXPANSIONS

NE Supply Enhancement Rivervale South to Atlantic Sunrise Gulf Trace - ISD 2/17

Constitution

Filed 3/17 Market Received 12/14 Began 3/17 Hillabee Ph 1 - ISD 7/17

Rivervale South to Market Received 3/18 Hillabee Ph 2 Gulf Connector Dalton - ISD 8//17

Filed 9/17 Received 2/16 Began 2/18 Garden St Ph 1 - ISD 9/17

Gateway St. James Garden St Ph 2 – ISD 3/18

Filed 11/17 Began 4/17 New York Bay - ISD 10/17

Southeastern Trail VSS II - ISD 12/17

Filed 4/18 28Garden State

Project Status:

• Phase I in service on Sept 9, 2017 (20 MDth/d);

• Phase II placed in-service on March 23, 2018 (160 MDthd).

505

Zone 6

207

PA

210 Pool

205

Trenton

> Expansion from Station 210 in Mercer County, NJ

to a new delivery point with New Jersey Natural NJ

203

on Transco’s Trenton Woodbury Lateral in

Burlington County, New Jersey New Meter and

Compressor

> Service will be provided under Transco’s FT Station

Service.

> Capacity: 180 MDth/d

> Phase I – 20 MDth/d and

> Phase II – 160 MDth/d

> Shipper: New Jersey Natural Gas Company

29Atlantic Sunrise

Project Status:

• All regulatory authorizations/ permits received with

construction underway on all project facilities;

• Target in-service date: Mid 2018.

> Expansion of Transco’s Leidy Line to Mid-

Atlantic and Southeast Markets

New York City

> Provides access to markets in Zones 6, 5 and 4 Zone 6

> Service will be provided under Transco’s FT 195

To River Road:

Service 500 Mdt/d

> Capacity: 1,700 Mdt/d

To Pleasant Valley:

> Shipper: Numerous 350 Mdt/d

Shipper Dth/d

Anadarko 44,048

Zone 5 SWN 44,048

Inflection 26,429

Zone 4 Chief 420,000

Cabot 850,000

Seneca 189,405

85

WGL Mid. 44,048

MMGS 22,024

Southern Co. 60,000

Total 1,700,002

30Gulf Connector

Project Status:

• Construction commenced in February 2018;

> Expansion of Transco's mainline from • Target In-Service Date: Q1 2019.

Station 65 to LNG delivery points in Zone 2 MS 85

and Zone 1 LA Zone 4

> Will be provided under Transco’s FT Service

Zone 3

> Capacity: 475 Mdt/d 65

Zone 2 45

TX

Zone 1

30

Freeport LNG – 75 Mdt/d

CCLNG - 400 Mdt/d

31St. James Supply

Project Status:

• Received FERC Certificate on January 18, 2018;

> Incremental transportation from Transco’s • Construction commenced in April 2018;

Station 65 to a new interconnect with the • Target In-Service Date: Q2 2019. 85

proposed YCI M1 facility

> Will be provided under Transco’s FT Service

> Capacity: 161.5 Mdt/d

> Shipper: YCI St. James Enterprises LLC Zone

4

65

Zone

SELA

45 82

3

YCI St. James

Enterprises

62

32Station 240 Modernization

Project Status:

• Transco filed a 30-day advance notice with FERC on

March 1, 2018

• Target In-Service Date: Q4 2019

Project Facts:

• Replace liquefaction plant at Station 240 in Carlstadt,

New Jersey to resolve safety and emissions issues,

liquefaction degradation, operational/reliability

issues.

• Facilities:

Gas Pretreatment

10 MDth/d Liquefaction

Compression

Control System and Transformers

Background:

• Station 240 is a peak-shaving LNG plant constructed in

1964.

• Consists of liquefaction, vaporization, and storage.

• The vaporization was replaced/upgraded in 1991.

• Total Storage is approximately 2,000 MDT

• Contractual Vaporization of 400 MDthd; Contractual

Liquefaction of 10 MDth/d.

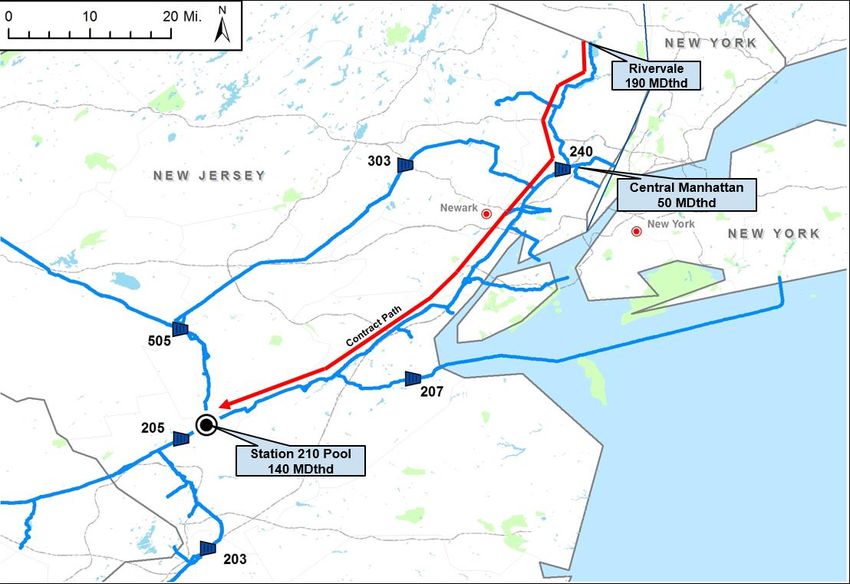

33Rivervale South to Market

Project Status:

• FERC Application filed on August 31, 2017;

• Received EA on March 16, 2018;

> Expansion from the Rivervale interconnect with • Target In-Service Date: Q4 2019.

Tennessee Gas Pipeline in Bergen County, NJ to

the existing Central Manhattan M&R and Station

210 Pool.

> Will be provided under Transco’s FT Service

Rivervale

> Capacity: 190 Mdt/d

> Shipper(s): Direct Energy (187.5 Mdt/d), UGI

Energy Services (2.5 Mdt/d)

Zone 6 New York City

210 Pool

34Northeast Supply Enhancement

Project Status:

• FERC Application filed on March 27, 2017;

• Draft Environmental Impact Statement received on

March 23, 2018;

• Target In-Service Date Q4 2019 / Q1 2020.

303

> Expansion from Station 195 in York County, PA to

the Rockaway Lateral in New York Bay. Narrows

> Will be provided under Transco’s FT Service.

> Capacity: 400 Mdt/d

Rockaway

> Shipper: National Grid 207 Delivery Point

205 210 Pool

200

Atlantic Sunrise

Project

Proposed River

Transfer Point

195

35Hillabee Phase 2

Project Status:

• FERC Order on Feb 2, 2016 and all other permits

Zone have been received;

4 • Limited work completed to-date;

• Target In-Service Date: Q2 2020.

> Point-to-point lease with Sabal Trail from Station 85

to a new interconnect in Hillabee, AL

> Leased capacity will be used by Sabal Trail to

provide access to Station 85 for its greenfield

pipeline, which will extend to central Florida to

serve Florida markets

> Capacity: 207 Mdt/d

> Shipper: Sabal Trail Transmission

36Gateway

> Expansion from the proposed PennEast

Pipeline Company interconnect in Mercer

County, NJ to the existing Paterson M&R

and Ridgefield M&R.

> Will be provided under Transco’s FT Service

> Capacity: 65 Mdt/d

> Shipper(s): PSEG Power (54 Mdt/d), UGI

Energy Services (11 MDt/d)

210 Pool

Project Status:

• FERC Application filed on Nov 15, 2017;

• Target In-Service Date: Q1 2021.

37Southeastern Trail

> Firm transportation from the existing Zone 5

Pleasant Valley Interconnect with Dominion’s Cove

Point Pipeline south to our existing Zone 3 Pool at Zone 6

Station 65.

> Will be provided under Transco’s FT Service

> Capacity: 296.375 MDt/d

> Shipper(s): PSNC, SCE&G, City of Buford (Ga), City of

LaGrange (Ga), Virginia Natural Gas.

Zone 5

Zone 4

Project Status:

• FERC Application filed on April 10, 2018;

• Target In-Service Date: Q4 2020.

38WE MAKE ENERGY HAPPEN

Projects in Development

39Adelphia Connection Expansion

In Development

Martins Creek Terminal

From MARC1

on Leidy Lower Mud Run

Project Facts:

• Path from MARC 1 and a proposed

interconnection with Adelphia Gateway Pipeline

to markets on Transco's Marcus Hook / Trenton

Woodbury Lateral.

• Facilities: Potential pipeline replacement,

compression addition and meter station 207

additions/ uprates.

• Capacity: 250 MDth/d 210 Pool

205

• Proposed ISD: November 1, 2021

Pennsylvania

203

200

Trenton New Jersey

Woodbury

Lateral

Contract Path

Proposed Interconnect

with Adelphia Gateway

Pipeline

40South Louisiana Market

In Development

Contract Path

Project Facts: Zone

• Path from Transco’s Station 65 to a new interconnect with 3

the methanol facility in St. James Parish, LA.

• Facilities: 0.6 miles of 20-inch Greenfield lateral

• Capacity: 202 Mdt/d

• Proposed ISD: 2021

45

41Bluebonnet Market Express

In Development

Waha Supply Header

Contract Path

Katy Delivery Header

Station 30

Station 35

Station 17

Project Facts: Agua Dulce

• Greenfield pipeline from the Waha Supply Hub in the

Permian basin to the Katy Hub landing area on Transco.

• Facilities: 476 miles of Greenfield pipeline, 5 Greenfield

compressor stations totaling 224,000 hp and 12 receipt

and delivery meter stations.

• Capacity: 2,000 Mdt/d

• Proposed ISD: Late 2020

42You can also read