Value Creation Through Constructive Activism - Investor Presentation August 2017 1 - Draft

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Value Creation Through Constructive Activism

Investor Presentation

August 2017

1

Certain Notices and Disclaimers

This presentation (“Presentation”) contains certain forward-looking statements relating to the investment

objectives, strategy, and approach of 180 Degree Capital Corp. (“180”). Forward looking statements generally can

be identified by the use of forward-looking words or phrases such as “believe,” “expect,” “anticipate,” “may,”

“could,” “intend,” “intent,” “belief,” “estimate,” “project,” “plan,” “likely,” “will,” “should” or similar words or phrases.

Forward-looking statements are inherently subject to risks and uncertainties and actual results and outcomes may

differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. 180

may not be successful in executing and implementing their investment strategies and reaching their investment

objectives. Prospective investors are urged not to place undue reliance on these forward-looking statements.

Prospective investors should carefully review and consider the risks and uncertainties. Any performance data set

forth herein represents past performance. Past performance does not guarantee future results.

This Presentation is provided for informational purposes only and does not constitute an offer to sell or a

solicitation of an offer to buy any security. Any such offering will be made only by means of a registration statement,

private placement memorandum, subscription agreement, or other documents as permitted by law. This

Presentation does not purport to be complete and is for discussion purposes only. If and when an investment

opportunity is offered to you, you must carefully read all of the distributed materials, including any included Risk

Factors (the “Disclosure Package”). All information provided in this Presentation is qualified in its entirety by the

disclosure set forth in any Disclosure Package.

This presentation on is intended solely for the party to whom it has been distributed. Any reproduction,

distribution or dissemination of this Presentation or the information included herein is expressly prohibited.

2

Firm Overview

Current Entity/Business

Prior Entity/Business

• Changes Effective in March 2017

• New Structure: Registered Closed-End Fund

§ Reduced operating costs and regulatory burden

• Established 1981; IPO in 1983 § Resources focused on value creation/investments

• Structure: Business Development Company • New Investment Focus:

§ Public Microcap Companies

• Investment Focus: Venture Capital § Deep Value

§ Constructive Activism

• New Leadership:

§ Kevin Rendino joined as CEO 3

180’s Philosophy and Core Beliefs

We are Graham and Dodd Investors

• The price we pay relative to the business we buy is the most important driver of investment returns.

• Markets overreact to near-term internal or environmental challenges creating attractive valuations.

• Out-of-favor companies and industries create opportunities to identify investments that offer

asymmetric return-to-risk potential.

• Companies with strong franchises, managements, and balance sheets are the best positioned to

turnaround, gain market share, and improve profitability in an industry recovery.

A portfolio of strong business franchises, purchased at the right price,

outperforms over a market cycle.

4

Firm Overview

• Differentiated Investment Strategy

• Rigorous, Analytical Investment Process

• Experienced Management Team

• Constructive Activism

• Managed Funds and Special Purpose Vehicles

• Active Risk Management

5

Differentiated Investment Strategy • We focus on investments in

Differentiated Investment Strategy

• Opportunity for value creation in US micro-capitalization publicly traded

stocks exists because management and boards often:

• Prioritize growth over cash flows

• Overvalue market perception of story versus certainty

• Favor status quo rather than change

• Lack intimate knowledge of desires of ”buy side” investors and the workings of the

public markets in general

• Mischaracterize “short-term viability” as detractor of “long-term growth”

• Manage for quarterly results

• Entrench themselves to protect their jobs and positions

• Few investors are willing/able to spend the time and energy identifying,

conducting diligence and actively engaging with such companies.

7

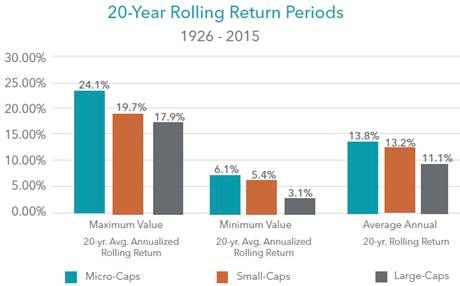

Differentiated Investment Strategy

• Minimal Analyst Coverage • High relative returns

25

22.5%

20

16.5%

15

12.0%

10

7.0%

5

2.2%

0

$12B

Source: Furey Research Partners, March 2016 via Grant Wasylik, Uncommon Wisdom Daily. Source: Ibbotson Classic Yearbook, 2015 via Grant Wasylik, Uncommon Wisdom Daily.

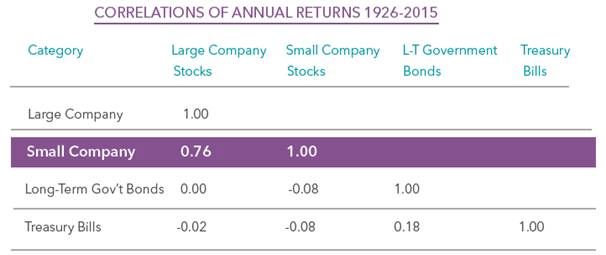

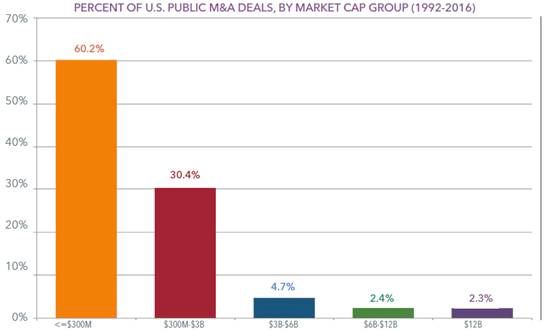

• Low correlations to other asset classes • High frequency of takeovers

70%

60.2%

60%

50%

40%

30.4%

30%

20%

10% 4.7% 2.4% 2.3%

0%

$12B 8

Source: FactSet via Grant Wasylik, Uncommon Wisdom Daily. Source: Furey Research Partners, March 2016 via Grant Wasylik, Uncommon Wisdom Daily.

Differentiated Investment Strategy

Traditional, Long-Only

180 Degree Capital Corp

Micro-Capitalization Funds (Constructive Activism)1

(Passive Investing)

Active engagement with management of investee

Wait passively for identified catalysts to realize value

companies to impact timing of catalysts

Not often willing to run proxy campaigns Ability to run proxy campaigns, if required

Generally not able to hold board seats

Able to hold board seats at portfolio companies

on portfolio companies

Concentrated portfolios available, but Able to offer co-investment opportunities on a single-

not often single-position focused funds company basis through special purpose vehicles

(1) Subject to applicable laws and regulations.

9Experienced Management Team

• Joined as Board Member in 2016 and Chief Executive Officer and Portfolio Manager in March 2017.

• 25+ year career in deep value investing at BlackRock / Merrill Lynch

• Value team leader managing $13B in assets over 11 funds.

• Member of BlackRock’s leadership committee.

• Frequent contributor to financial focused television and media outlets.

• Since 2012, served as Chief Executive Officer of RGJ Capital, LLC, a firm focused on deep value investing in micro-

capitalization publicly traded companies.

Kevin M. Rendino

• Joined 180’s predecessor company in 2004; now serves as President and Portfolio Manager.

• 13+ year career managing the investments and operations of a publicly traded investment company

• Sourced, executed and managed investments across multiple asset classes including private and public equities and debt.

• Actively led and participated in multiple capital formation efforts at 180 and its portfolio companies.

• Responsibility for day-to-day operations, finance, legal and compliance functions of the firm.

• Current and past member of the board of multiple privately held and publicly traded portfolio companies.

Daniel B. Wolfe 10Rigorous, Analytical Investment Process

Fundamental Plan

Screening Research Development Execution Exit

>250k Companies 300-600 Companies 30-40 Companies 10-15 Companies

• InitiallyConstructive Activism

• We are not corporate raiders. Our ultimate goal is to engage constructively with existing boards and

management teams to unlock value through:

• Realignment of financial performance to achieve growth of cash flows not just revenues

• Improving investor relations strategies and outreach

• Evaluation of strategic options including mergers, acquisitions, sales, and divestitures

• Identification of complementary talent and expertise

• Introductions to value-add resources and capabilities

• Alignment of interests with and support from large shareholders

• We are not adverse, however, to pursuing change through other routes including:

• Private and public shareholder communications

• Proxy solicitations

• All efforts will be grounded by and based on our fundamental research and diligence.

12Constructive Activism

Initial Focus Future Focus

Level 1 Engagement: Level 2 Engagement: Level 3 Engagement:

Near-term potential winners that do not Near-term potential winners that may Longer-term projects where we

require substantial time/involvement require a bit of time/involvement, but not instigate/lead turnarounds of businesses

substantial allocations of time.

Approach: Identify quality, deeply Approach: Identify deeply undervalued

undervalued companies with strong Approach: Identify quality, deeply companies in need of substantial changes.

management teams in the process of undervalued companies with strong

executing a turnaround. management teams but where we believe Constructive Activism (Levels 1 and 2+):

small changes can result in increased value

Constructive Activism: and management is interested in engaging • Propose changes to management

constructively. and/or board.

• Introductions to our institutional • Propose fundamental changes to

investors and/or individual investors Constructive Activism (Level 1+): business, including potential sale of

that own or have owned our stock. company.

• Leverage our general knowledge of the • Actively suggest changes to IR strategy • If required, run competing proxy

public markets gained over our and/or messaging. campaigns.

collective 40+ years of experience for • Actively suggest changes in business • Take seat(s) on board

advice and value-add introductions. related primarily to financial • Leverage ownership/control to drive

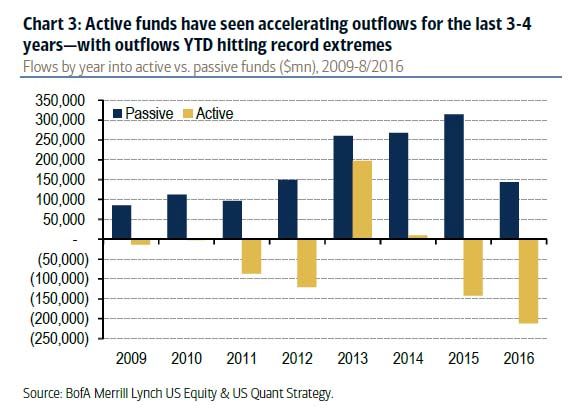

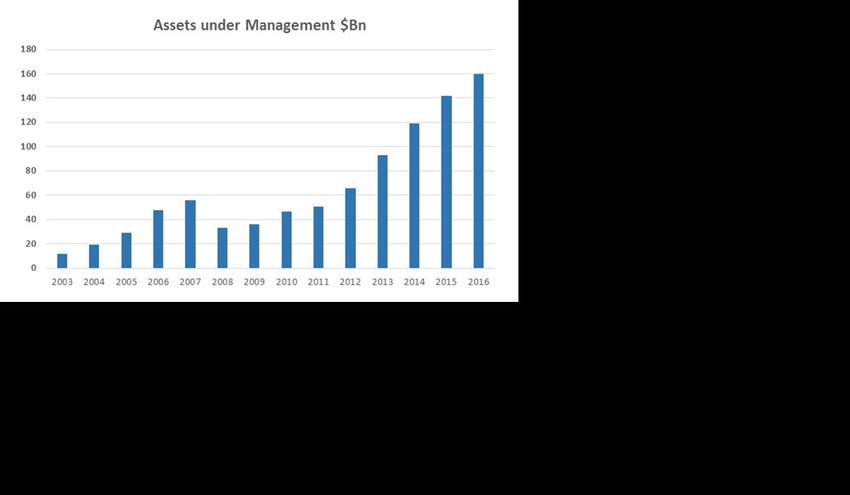

performance improvements. change. 13Assets Allocated to Activist Funds are Growing

While assets are flowing out of actively managed funds at record rates,

assets allocated to activist strategies are growing.

Source: Eric Lefebvre, Ernst & Young, LLP

14Shareholder Activism in

Small-to-Micro Capitalization Companies is Growing

“... firms with a market capitalization of

between $50 million and $1 billion have

constituted the majority of U.S. activism targets

for the second year in a row, and 2017 is

expected to be on pace with that trend. Several

factors could beat play in this development,

such as the lower cost of building a significant

position and the ease of employing M&A

strategies (including more viable buyers), not to

mention a broader array of potential targets

across all sectors within this market cap range. ”

Source: Duncan Harrington, Raymond James in

Activist Investing 2017 Year in Review,

Published by Activist Insight and Schulte Roth & Zabel

15Level 1 Engagement Example: USA Truck, Inc. (USAK)

35 180 Invests Company Profile

$1.6m @

30

avg. $6.59/share

H2 2017/2018 Catalysts: • USA Truck provides a broad range of truckload and

25 Introduced to Improving Demand and Pricing

USAK logistics services to customers in a variety of industries.

20 Reduced Debt

15 Increased Operating Efficiency • New CEO and management team joined in

10

ELD Mandate Q4 2016-Q1 2017.

5

• Implementing turnaround plan to drive profitable

0

revenue growth and improve operational execution.

180 Investment and Level 1 Engagement

Valuation Analysis ($ million)

• Introduced in Q1 2017 through internal screen; began

2016 2017 2018 2019 diligence including meeting with management team.

(Actual) (Modeled)1 (Modeled)1 (Modeled)2

EBITDA $30.3 $25.9 $39.8 $50.5

• Invested $1.6 million @ avg. PPS of $6.59 in open

market purchases through June 30, 2017.

Growth Rate (YoY) (55%) (14.5%) 53.7% 26.8%

EBITDA/Rev. Multiple N/A 7.6x3 6.2x4 5.4x4 • Active ongoing dialogue with management and plan

efforts to raise awareness of the company.

Stock Price @ EBITDA/Rev. Multiple5 N/A $8.663 $14.53 $17.59

Modeled Change from 180 Avg. Purchase Price N/A 31% 121% 167% • We believe there are upside opportunities for

1. Models based on analyst estimates as listed on Bloomberg. Actual results may be materially different than those modeled.

improving operating efficiency by leveraging the diverse

2. Estimated using half of 2017 to 2018 growth rate. Actual results may be materially different than those estimated. backgrounds of the new management team.

3. Multiple and stock price as of June 30, 2017.

4. 2019 multiple is based on median EV/EBITDA multiple 2009-2016. 2018 multiple is average of June 30, 2017 and 2019 multiples. 16

5. Calculations based on cash of $0.1 million and outstanding debt of $129.3 million.Level 2 Engagement Example: Adesto Tech. Corp. (IOTS)

$9.00 13D/A Filed:

$8.00 Company Profile

H2 2017 and 2018

IOTS Stock Closing Price

Shift to Constructive

$7.00 Activism and Engagement Catalysts: • Adesto sells low-power memory solutions that enable

$6.00

broad classes of connected devices.

$5.00 1. Profitability

$4.00

2. New Products • Formed based on proprietary memory technology and

$3.00 acquired flash-memory product lines from Atmel.

IPO @

(EcoXip, Mavriq)

$2.00 ~140%

$1.00 $5.00/Share 3. IoT Growth • Focused on growing Internet-of-Things (IoT) sector.

Increase

$0.00

• Top-tier, diversified customer base.

180 Investment and Level 2 Engagement

Valuation Analysis ($ million) • 180 owns 8.8% of Adesto (top five shareholder).

2016 2017 2018 2019

(Actual) (Modeled)1 (Modeled)1 (Modeled)2

• Shifted to constructive activist engagement in early

January 2017 focused on improving:

Revenues $44.0 $54.5 $67.0 $82.4

§ investor communications;

Growth Rate (YoY) 1.6% 23.9% 22.9% 22.9%

§ presentation materials;

Modeled Stock Price 2x EV/Revenue § financial operating performance.

N/A $6.07 $7.28 $8.76

Multiple3

Modeled change from PPS • Many of 180’s suggestions were implemented by

N/A 34% 60% 93%

on June 30, 2017: $4.55 Adesto’s management.

1.

2.

Models based on analyst estimates as listed on Bloomberg. Actual results may be materially different than those estimated.

Model based on same year-over-year growth as that modeled for 2017 to 2018. Actual results may be materially different than

• Adesto’s stock up ~140% since 180’s 13D/A filing.*

those estimated. Actual trading multiple may be materially different than that used in the model above.

17

* Based on stock price as of June 30, 2017

3. Calculations based on cash of $31.9M and debt of $15.0M. Comp. median EV/rev mult. is 2.8x. See appendix for list of comps.Level 3 Engagement Example: Xplore Tech. Corp. (XPLR)

XPLR Stock Closing Price

$9.00

Position Acquired Press

Company Profile

$8.00 Letters Sent H2 2017 and 2018

$7.00 to Board

Release

Catalysts:

• Xplore is the second largest supplier of industrial-grade

$6.00 Issued

rugged tablet computers.

$5.00 1. Restructuring of board

$4.00 2. Revenue growth • Acquired product line of competitor, Motion, in 2015.

$3.00 3. Potential sale of

$2.00 • Clean balance sheet and capital structure.

company

$1.00

$0.00

Example of Level 3 Engagement

12/31/13

3/31/14

6/30/14

9/30/14

12/31/14

3/31/15

6/30/15

9/30/15

12/31/15

3/31/16

6/30/16

9/30/16

12/31/16

3/31/17

6/30/17

9/30/17

12/31/17

3/31/18

6/30/18

9/30/18

12/31/18

• Began Level 2 constructive activist engagement through

private communications early 2016 focused on

Valuation Analysis ($ million) improving:

FY2017 FY2018 FY2019 FY2019 § investor communications;

(Actual)1 (Modeled)1,2 (Modeled)1,2 (Modeled)1,2 § presentation materials;

Revenues $77.9 $80.6 $88.4 $97.0 § corporate governance;

Growth Rate (YoY) (22.5%) 3.5% 9.7% 9.7%3 § financial operating performance.

Modeled PPS @ 0.5x EV/Revenue Multiple4 N/A $3.44 $3.80 $4.18 • Some, but not all, recommended changes implemented.

Modeled change from PPS on

N/A 76% 95% 115% • Transitioned to Level 3 with public activism in June 2017

June 30, 2017: $1.95

seeking changes in the composition of the board.

1. Xplore’s fiscal year runs from April 1 to March 31.

2. Models based on analyst estimates. Actual results may be materially different than those estimated. • Preparing for proxy campaign, if required.

3. Model based on same year-over-year growth as that modeled for 2017 to 2018. Actual results may be materially

different than those estimated. Note: XPLR is a personal holding of Kevin Rendino through RGJ Capital, LLC,

4. Calculations based on cash of $0.65 million and outstanding debt of $3.1. XPLR historically traded at a median acquired prior to joining 180. Information provide as example of steps 180 18

and average EV/Rev. of 0.5 and 0.7, respectively. Actual trading multiple may be materially different. would take in Level 3 Engagement.Managed Funds and Special Purpose Vehicles

• Our structure affords a high-level of flexibility in structuring investments and

managing third-party capital.

• Our historical experience of investing in privately held companies enable us

to develop unique financial solutions to unlock value.

• We are actively working on a number of special situations/special purpose

vehicles.

19Risk Management Within a Concentrated Portfolio

• Graham and Dodd value investing philosophy offers a margin of safety.

• Consistent quantitative and qualitative monitoring and evaluation of individual

and aggregate positions.

• Opportunistic trading around liquid positions and hedging to lock in returns /

limit losses.

20Summary

• Differentiated Investment Strategy

• Rigorous, Analytical Investment Process

• Experienced Management Team

• Constructive Activism

• Managed Funds and Special Purpose Vehicles

• Active Risk Management

We are actively seeking opportunities to partner with others seeking similar

strategies and to manage capital alongside our permanent capital.

22Kevin M. Rendino Daniel B. Wolfe

kevin@180degreecapital.com daniel@180degreecapital.com

24Adesto Comparable Company List

Name Ticker EV/Sales

LATTICE SEMICONDUCTOR CORP LSCC US Equity 2.3

POWER INTEGRATIONS INC POWI US Equity 4.3

MAXLINEAR INC MXL US Equity 3.9

RAMBUS INC RMBS US Equity 3.5

IXYS CORPORATION IXYS US Equity 1.3

AMBARELLA INC AMBA US Equity 3.9

INPHI CORP IPHI US Equity 3.9

DSP GROUP INC DSPG US Equity 1.2

MAXWELL TECHNOLOGIES INC MXWL US Equity 1.3

QORVO INC QRVO US Equity 2.8

MICRON TECHNOLOGY INC MU US Equity 1.9

Median 2.8

Source: Bloomberg as of June 30, 2017

25Level 1 Engagement Example: Synacor, Inc. (SYNC)

$4.40

SYNC Stock Closing Price

Introduced to 180 Invests Company Profile

$4.20 SYNC $2.25m @ 2018 Catalysts:

$4.00 $3.50/share AT&T Portal Revenues • Synacor delivers modern, multiscreen experiences and

$3.80 Projected to Begin Meaningful multiplatform services to partners that require scale,

$3.60 Contribution to Business actionable data and sophisticated implementation.

$3.40 Growth in Recurring • New CEO and management team joined in August 2014.

$3.20 Businesses

• Executing on plan to reach $300 million in revenues and

$3.00 $30 million in EBITDA in 2019.

• Won AT&T portal in 2016; launched in Q2 2017;

material contribution to revenues expected in 2018.

Valuation Analysis ($ million)

180 Investment and Level 1 Engagement

2016 2017 2018 2019

(Actual) (Modeled)1 (Modeled)1 (Modeled)1 • Introduced in Q1 2017 by analyst; began diligence

Revenues $127.4 $145.0 $230.8 $296.5 including meeting with management team.

Growth Rate (YoY) 8.6% 13.8% 59.2% 28.5% • Invested $2.25 million in registered offering in Q2 2017.

Modeled Stock Price 0.95x EV/Revenue

N/A $4.10 $6.25 $7.89 • Active ongoing dialogue with management and

Multiple2

investors to raise awareness of the company.

Modeled Change from 180 Avg. Purchase Price N/A 17% 78% 125%

• We believe there are upside opportunities for increased

1. 2017 models based on midpoint of guidance from SYNC management as of 8/9/17. 2018 and 2019 models are based on analyst

estimates listed on Bloomberg as of 8/8/17. Actual results may be materially different than those estimated.

value from recurring businesses (email/CloudID).

2. Calculations based on cash of $23 million and outstanding debt of $4.8 million. Multiple is based on SYNC EV/Rev on June 30, 26

2017. Actual trading multiple may be materially different than that used in the model above.Level 1 Engagement Example: TheStreet, Inc. (TST)

$3.50

$3.00 180 Invests

$890k @ H2 2017/2018 Catalysts:

$2.50

Introduced to avg. $0.89/share Return to profitability

Company Profile

$2.00 TST Revenue growth

$1.50 Resolution of expiring • TheStreet is is a financial news and information

$1.00 agreement with Jim Cramer provider to consumers and businesses.

$0.50 Solution to preferred overhang • New CEO and management team joined in 2016.

$0.00 • Senior management and executive chairman

historically built and sold MarketWatch and

completed a successful turnaround of USA Today.

Valuation Analysis ($ million) 180 Investment and Level 1 Engagement

2016 2017 2018 2019

(Actual) (Modeled)1 (Modeled)1 (Modeled)2

• Introduced in Q2 2017 by analyst; began diligence

including meeting with management team.

Recurring Revenues (Modeled 2x EV/Rev.)3 $49.5 $49.7 $52.0 $54.5

Non-Recurring Revenues (Modeled 1x EV/Rev.)3 $14.0 $14.0 $14.7 $15.4

• Invested $890,000 in open market purchases.

Modeled Stock Price @ Combined Modeled • Active ongoing dialogue with management about

N/A $1.98 $2.11 $2.24

EV/Rev. for Recurring and Non-Recurring Revs. potential ways to unlock value for shareholders.

Modeled Change from 180 Avg. Purchase Price N/A 123% 137% 152%

1. Models based on analyst estimates as listed on Bloomberg and same distribution of revenues as in 2016. Actual results may be materially different than those modeled.

2. Estimate based on same growth rate from 2017 to 2018. Actual results may be materially different than those estimated.

3. Calculations based on cash of $24.9 million, $55 million in preferred stock and no other debt. 27

Multiple is based on financial data subscription companies (recurring revenues) and advertising-based media companies (non-recurring revenues), respectively.You can also read