THEMANAGEMENT MINDSET - TEPAP

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

T HE M ANAGEMENT

M INDSET

Dr. David M. Kohl

Professor Emeritus, Agricultural and Applied Economics

Member of Academic Hall of Fame, College of Agriculture & Life Sciences

Virginia Tech, Blacksburg, VA

(540) 961-2094 (Alicia Morris) | (540) 719-0752 (Angela Meadows) | sullylab@vt.edu

Macro Clinic Video Blog: www.compeer.com/education

Road Warrior of Agriculture: www.cornandsoybeandigest.com

January 12, 2021 Ag Globe Trotter: www.northwestfcs.com

Dave’s GPS & Dashboard Indicators: www.farmermac.com

2 Management Mindsets for the 2020s

Poll #1

Which would best describe your business? (select

one)

a) startup from scratch

b) family business in transition

c) existing business in growth mode

d) scaling down, becoming more efficient

e) stable, no change

3

Median Net Farm Income- All,

High 20% and Low 20%

2019 Update:

High 20%= $236,000

Low 20%= $ -49,000

4

Aligning with Mindsets

Producer A Producer B

How do I compare? Will a lender finance me?

What are others doing? Will I survive for another

think longer term & what is year?

on the horizon often a know it all or

victim

School vs. Real World Perspective:

In school, you get the lesson first, then the test.

In the real world, you get the test first, then the lesson.

5

Management Assessment

Greens Yellows Reds

adaptive to a success because of waiting for prices &

situation- proactive equity & history vs. markets to save

5% rule profitability & cash them

flow excuse game, not

get efficient before

getting bigger preparing the next my fault

generation lose money, equity

sweat the small stuff

bigger before better, keeps them going

plan, strategize, examine human

execute & monitor 80/20 rule is alive &

horse power well

process oriented magic bullet- the

advisory teams next big thing

6

Business IQ: Management Factors

Critical Questions for Crucial Conversations

Farmer Checklist Your Score Green (3 points or 4*) Yellow (2 points) Red (1 point)

1. Knows cost of production Written In head No idea

2. Knows cost of production by enterprise Written* In head No idea

3. Goals - business, family, & personal Written* In head No idea

4. Record keeping system Accrual Schedule F (one & done) No idea

5. Projected cash flow Written* In head No idea

6. Financial sensitivity analysis Written* In head No idea

7. Understand financial ratios, break evens Written* In head No idea

8. Work with advisory team and lender Yes* Sometimes Never

9. Marketing plan written and executed Yes Sometimes Never

10. Risk management plan executed Yes Sometimes Never

11. Modest lifestyle habits, family living budget Yes* Sometimes Non existent

Written plan for improvement executed &

12. Yes* Sometimes Non existent

strong people management

13. Transition plan/Business Owner plan Yes Working on plan Non existent/controversy

14. Educational seminars/courses Yes Sometimes Never attend

15. Attitude Proactive* Reactive Indifferent

Total 0

*Extra Points: Score Overall Analysis

- Progressive Business may receive 4 points for #2,6,7,8,14

35-50 Strong management rating & viability

- Struggling Business Attempting Turnaround may receive 4

points for #3,5,8,11,12 20-34 Moderate risk & viability; will most likely show previous refinancingBusiness IQ Exercise

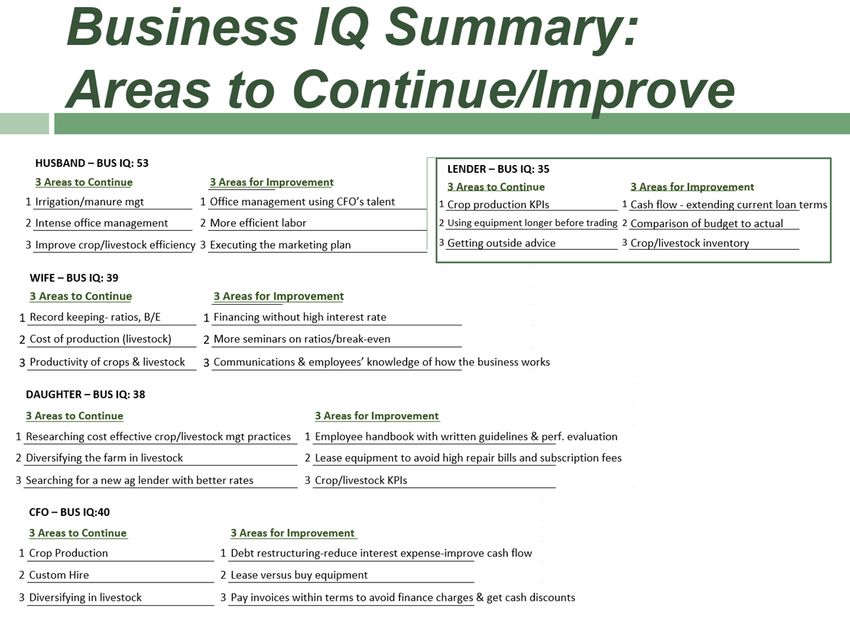

After completing the Business IQ: Management Factors

Scorecard, what are three areas/points in your business

that you will continue and three areas/points for

improvement?

Three areas/points to continue: Three areas/points to improve:

• ______________________ • ______________________

• ______________________ • ______________________

• ______________________ • ______________________

8How Can Team Members Use Business IQ as a Tool for Producers? screener for attitude to improve each family member, business partner, spouse complete the Business IQ separately assists in prioritizing improvements communication tool- internal and external to team of advisors customer develops plan for improvement to improve or buy in objective way to measure management monitoring tool, year over year 9

Business IQ: Management Factors

Critical Questions for Crucial Conversations

Farmer Checklist HUSBAND Green (3 points or 4*) Yellow (2 points) Red (1 point)

1. Knows cost of production 3 Written In head No idea

2. Knows cost of production by enterprise 4 Written* In head No idea

3. Goals - business, family, & personal 4 Written* In head No idea

4. Record keeping system 3 Accrual Schedule F (one & done) No idea

5. Projected cash flow 4 Written* In head No idea

6. Financial sensitivity analysis 4 Written* In head No idea

7. Understand financial ratios, break evens 4 Written* In head No idea

8. Work with advisory team and lender 4 Yes* Sometimes Never

9. Marketing plan written and executed 2 Yes Sometimes Never

10. Risk management plan executed 3 Yes Sometimes Never

11. Modest lifestyle habits, family living budget 4 Yes* Sometimes Non existent

Written plan for improvement executed &

12. 4 Yes* Sometimes Non existent

strong people management

13. Transition plan/Business Owner plan 3 Yes Working on plan Non existent/controversy

14. Educational seminars/courses 3 Yes Sometimes Never attend

15. Attitude 4 Proactive* Reactive Indifferent

Total 53

*Extra Points: Score Overall Analysis

- Progressive Business may receive 4 points for #2,6,7,8,14

35-50 Strong management rating & viability

- Struggling Business Attempting Turnaround may receive 4

points for #3,5,8,11,12 20-34 Moderate risk & viability; will most likely show previous refinancing

(See pg. 2 for Progressive and Attempting Turnaround definitions)Business IQ: Management Factors

Critical Questions for Crucial Conversations

Farmer Checklist WIFE Green (3 points or 4*) Yellow (2 points) Red (1 point)

1. Knows cost of production 3 Written In head No idea

2. Knows cost of production by enterprise 2 Written* In head No idea

3. Goals - business, family, & personal 3 Written* In head No idea

4. Record keeping system 3 Accrual Schedule F (one & done) No idea

5. Projected cash flow 3 Written* In head No idea

6. Financial sensitivity analysis 3 Written* In head No idea

7. Understand financial ratios, break evens 1 Written* In head No idea

8. Work with advisory team and lender 3 Yes* Sometimes Never

9. Marketing plan written and executed 2 Yes Sometimes Never

10. Risk management plan executed 3 Yes Sometimes Never

11. Modest lifestyle habits, family living budget 3 Yes* Sometimes Non existent

Written plan for improvement executed &

12. 2 Yes* Sometimes Non existent

strong people management

13. Transition plan/Business Owner plan 3 Yes Working on plan Non existent/controversy

14. Educational seminars/courses 2 Yes Sometimes Never attend

15. Attitude 3 Proactive* Reactive Indifferent

Total 39

*Extra Points: Score Overall Analysis

- Progressive Business may receive 4 points for #2,6,7,8,14

35-50 Strong management rating & viability

- Struggling Business Attempting Turnaround may receive 4

points for #3,5,8,11,12 20-34 Moderate risk & viability; will most likely show previous refinancing

(See pg. 2 for Progressive and Attempting Turnaround definitions)Business IQ: Management Factors

Critical Questions for Crucial Conversations

Farmer Checklist DAUGHTER Green (3 points or 4*) Yellow (2 points) Red (1 point)

1. Knows cost of production 2 Written In head No idea

2. Knows cost of production by enterprise 2 Written* In head No idea

3. Goals - business, family, & personal 3 Written* In head No idea

4. Record keeping system 3 Accrual Schedule F (one & done) No idea

5. Projected cash flow 2 Written* In head No idea

6. Financial sensitivity analysis 2 Written* In head No idea

7. Understand financial ratios, break evens 2 Written* In head No idea

8. Work with advisory team and lender 2 Yes* Sometimes Never

9. Marketing plan written and executed 2 Yes Sometimes Never

10. Risk management plan executed 2 Yes Sometimes Never

11. Modest lifestyle habits, family living budget 4 Yes* Sometimes Non existent

Written plan for improvement executed &

12. 3 Yes* Sometimes Non existent

strong people management

13. Transition plan/Business Owner plan 3 Yes Working on plan Non existent/controversy

14. Educational seminars/courses 3 Yes Sometimes Never attend

15. Attitude 3 Proactive* Reactive Indifferent

Total 38

*Extra Points: Score Overall Analysis

- Progressive Business may receive 4 points for #2,6,7,8,14

35-50 Strong management rating & viability

- Struggling Business Attempting Turnaround may receive 4

points for #3,5,8,11,12 20-34 Moderate risk & viability; will most likely show previous refinancing

(See pg. 2 for Progressive and Attempting Turnaround definitions)Business IQ: Management Factors

Critical Questions for Crucial Conversations

Farmer Checklist CFO Green (3 points or 4*) Yellow (2 points) Red (1 point)

1. Knows cost of production 3 Written In head No idea

2. Knows cost of production by enterprise 3 Written* In head No idea

3. Goals - business, family, & personal 3 Written* In head No idea

4. Record keeping system 3 Accrual Schedule F (one & done) No idea

5. Projected cash flow 2 Written* In head No idea

6. Financial sensitivity analysis 3 Written* In head No idea

7. Understand financial ratios, break evens 2 Written* In head No idea

8. Work with advisory team and lender 2 Yes* Sometimes Never

9. Marketing plan written and executed 2 Yes Sometimes Never

10. Risk management plan executed 2 Yes Sometimes Never

11. Modest lifestyle habits, family living budget 3 Yes* Sometimes Non existent

Written plan for improvement executed &

12. 3 Yes* Sometimes Non existent

strong people management

13. Transition plan/Business Owner plan 3 Yes Working on plan Non existent/controversy

14. Educational seminars/courses 3 Yes Sometimes Never attend

15. Attitude 3 Proactive* Reactive Indifferent

Total 40

*Extra Points: Score Overall Analysis

- Progressive Business may receive 4 points for #2,6,7,8,14

35-50 Strong management rating & viability

- Struggling Business Attempting Turnaround may receive 4

points for #3,5,8,11,12 20-34 Moderate risk & viability; will most likely show previous refinancing

(See pg. 2 for Progressive and Attempting Turnaround definitions)Business IQ: Management Factors

Critical Questions for Crucial Conversations

Farmer Checklist LENDER Green (3 points or 4*) Yellow (2 points) Red (1 point)

1. Knows cost of production 3 Written In head No idea

2. Knows cost of production by enterprise 3 Written* In head No idea

3. Goals - business, family, & personal 2 Written* In head No idea

4. Record keeping system 3 Accrual Schedule F (one & done) No idea

5. Projected cash flow 3 Written* In head No idea

6. Financial sensitivity analysis 3 Written* In head No idea

7. Understand financial ratios, break evens 3 Written* In head No idea

8. Work with advisory team and lender 3 Yes* Sometimes Never

9. Marketing plan written and executed 1 Yes Sometimes Never

10. Risk management plan executed 1 Yes Sometimes Never

11. Modest lifestyle habits, family living budget 1 Yes* Sometimes Non existent

Written plan for improvement executed &

12. 1 Yes* Sometimes Non existent

strong people management

13. Transition plan/Business Owner plan 3 Yes Working on plan Non existent/controversy

14. Educational seminars/courses 3 Yes Sometimes Never attend

15. Attitude 2 Proactive* Reactive Indifferent

Total 35

*Extra Points: Score Overall Analysis

- Progressive Business may receive 4 points for #2,6,7,8,14

35-50 Strong management rating & viability

- Struggling Business Attempting Turnaround may receive 4

points for #3,5,8,11,12 20-34 Moderate risk & viability; will most likely show previous refinancing

(See pg. 2 for Progressive and Attempting Turnaround definitions)15

Financial Ratios Across

Business IQ Percentiles

Debt/Total Asset

58.20%

50.08%

32.30%

28.70%

20.52%

17.45%

TOP 1/3 MIDDLE 1/3 BOTTOM 1/3

Median Mean

Preliminary Study of Kentucky Farm Business Management Association data - Ben Isaacs, Undergraduate Research Study

at University of Kentucky

16Financial Ratios Across

Business IQ Percentiles

Return on Assets

3.16%

2.25%

0.94%

0.173%

0.45%

-0.20%

TOP 1/3 MIDDLE 1/3 BOTTOM 1/3

Median Mean

Preliminary Study of Kentucky Farm Business Management Association data - Ben Isaacs, Undergraduate Research Study

at University of Kentucky

17Financial Ratios Across

Business IQ Percentiles

Net Farm Income

$202,120

$123,766

$109,947

$45,243 $53,406

$14,349

TOP 1/3 MIDDLE 1/3 BOTTOM 1/3

Median Mean

Preliminary Study of Kentucky Farm Business Management Association data - Ben Isaacs, Undergraduate Research Study

at University of Kentucky

18Other Key Ratios

coverage ratio

top third - 114%

bottom third - 10%

operating expense to revenue ratio¹

top third 68%

bottom third 90%

¹ excluding interest and depreciation

19Management Tests for

Farms/Ranches/Businesses/Households

volatility

agility

resiliency

opportunity

20Passing the Test for Volatility

• working capital 20-25% of expenses

• cash in household budget, 4-6 months of

expenses

• marketing program

• commodity

• value added

• risk management program

• crop insurance

• health insurance, disability

• coverage, equal to or greater than debt levels

21Passing the Test for Agility • working capital/cash • Is it business driven? • Is it lender driven? • optimization versus diversification • resources • talents, skills • marketplace • plan B, C, and D non-farm/ranch gig income/revenue find the balance 22

Passing the Test for Resiliency

• competitive cost of production

• break evens and benchmarking

• trend analysis, positive

• modest to low family living withdraws

• family business needs to prepare for the next

generation – 6 year rule

• startup mentorship

• term debt/EBITDA < 6 to 1

• EBITDA includes farm/non-farm income

23Passing the Test for Opportunity • manage the controllables & manage around the uncontrollables • goal focused • 80-16-4 rule • process focused • follow fundamentals • plan, strategize, execute & monitor • team of advisors • strong Business IQ • 35 = opportunity 24

Chat Question #1

What are your top three actions for

2021?

Click on the Chat button at the

bottom of the Zoom window.

Toggle the drop down to ‘All

panelists and attendees’ then

type your response.

25Lenders Wish List for 2021 For

Producers

projected cash flow

accrued adjusted statements

break evens - cost of production

marketing risk management plan

personal family living budget

written goals

26The Feisty Fifteen: Problems

Your Business Should Have (1)

Your business pays lots of taxes.

find sweet spot of paying taxes vs. deductions

Your lender wants to loan you money.

strong profits/cash flow

war chest for working capital - greater than 25% of operating expenses

You have growth frustrations, just can’t grow fast enough.

overestimate capital and time by 25%

term debt to EBITDA < 5 to 1

working capital to debt service > 5 to 1

human horsepower & management acumen

Everyone wants to work for you.

attract & retain the right people, including family members

be a work culture magnet

over compensate productive people

27The Feisty Fifteen: Problems

Your Business Should Have (2)

Your business has excess cash sitting around.

cash is queen

blocking capital in adversity

opportunity capital for purchases or acquisitions

In a family business, the older generation suddenly wants to exit, and they

have at least 50% of retirement income generated outside the business.

You have time for family & friends when neighboring businesses don’t.

2,500/500 hour rule

You could walk away from the business for one month and it functions fine

without you.

You left money on the table when marketing this year’s crop or livestock.

The younger generation spends too much time in the office on the

computer and in the books.

You must spend money for a facilitator and team of advisors for your

transition/estate plan.

28The Feisty Fifteen: Problems

Your Business Should Have (3)

Your neighbor comments that you spend too much time at seminars and

conferences, and you have heard it all before.

Even though you are financially successful you still spend time refining your

written business plan.

You don’t have to bring your personal checkbook to the business board

meeting.

Mom & Dad, Grandma & Grandpa are upset about those tough questions

that you are asking in developing the business plan.

29Dr. Kohl Unplugged (1)

Do you see any trends in business IQ results across the different

generations? i.e. older generations having higher or lower business

IQ than more recent generations? If so, any ideas of why that might

be?

Often we find producers make quick decisions based on cash flow

for the month. Given COVID volatility, that is understandable. How

would you present the “cost of not doing something”… sometimes

referred to as Type 1 vs. Type 2 error? Do you have an analogy or

examples of these types of discussions?

Based on groups of producers, green, yellow and red; how do you

feel this influences and impacts marketing decisions?

The top 20% of class have a high business IQ. How do they decide

on what investments to make? (Big or small). What gets their

attention when making a purchase?

30Dr. Kohl Unplugged (2)

What are the 2-3 key things that I need to learn from a producer’s

banker/lender to help me be a more effective advisory board

member?

Will COVID-19 change the university education model long-term?

What do you see interest rates doing in the next decade?

You had mentioned that non-meat and non-dairy alternatives gained

more market share when processing plans were hit this year. Do

you think this will continue to grow at an increased rate once the

COVID bug passes?

31Chat Question #2

What is the most enjoyable aspect

of being involved in agriculture?

Click on the Chat button at the

bottom of the Zoom window.

Toggle the drop down to ‘All

panelists and attendees’ then

type your response.

32You can also read