The S&P Liquidity Adequacy Ratio and its Role in Upper Management Decision Making - Energy Risk USA 2007 May 16th, Houston, Texas

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The S&P Liquidity Adequacy Ratio

and its Role in Upper Management

Decision Making

Energy Risk USA 2007

May 16th, Houston, Texas

John Wengler, Chief Risk Officer

Entergy Services, Inc.Overview

Calculating the ratio between available liquidity

and potential liquidity demands

The different S&P Liquidity Adequacy ratios by

energy sector

Perspectives from Standard & Poor’s

Communicating liquidity adequacy to upper

management to enhance decision making

Customizing your own stress scenarios

Industry Perspectives

Page 2Background on Entergy

Geographic Scale Entergy’s Business Model

Entergy’s Businesses Entergy Nuclear

30,000 MW electric • 6 non-utility units owned at

generating capacity 5 sites (5,000 MW) Supply/Demand Climate/Weather Data

Long Positions

2nd largest U.S. nuclear • 1 plant managed (800 MW) Environment Competitive Behavior

generator 45% of 07 earnings Fuel Prices Legislation/Regulation Structured

Structured Strict

2.6 million customers guidance midpoint Credit Markets Capital Markets Contracts

Contracts Risk

$10 billion revenues Limits

14,500 employees

Rigorous Asset

Asset

Analysis Development

Development

/Acquisitions

/Acquisitions

Portfolio

Portfolio

Current Management

Management

Point of Asset

Asset

View Disposition

Disposition

Structured

Structured

Business Create Contracts

Contracts

Business Create

Strategy

Strategy Options

Options Short Positions

Produce

Produce

Driven by: Products/

Products/

Markets Services

Services

Skills Competitor/

Utility Non-Nuclear Wholesale Industry

5 electric utilities (5 regulators) Scale Operational

Operational Achieve

Achieve

Assets Standards

4 contiguous states – Arkansas, Scope Excellence

Excellence Productivity

Productivity

1,500 MW non-

Louisiana, Mississippi, Texas Positions

nuclear wholesale

22,000 MW of generating capacity capacity owned Manage

Manage

15,500 miles of transmission Relationships

Relationships

lines

55% of 07 earnings guidance

midpoint (includes Parent &

Other)

Page 3The Methodology Helps Answer the Question of Whether a

Company Has Adequate Liquidity If …

The company was suddenly downgraded below

investment grade

and

Market prices instantaneously increased (or

decreased)

Page 4How to Calculate “S&P Liquidity Adequacy Ratio”?

It’s the ratio of: Primary Liquidity / Potential Liquidity Demands

Primary Liquidity

Unrestricted Cash

Unused and Available Credit Facilities

Discretionary Gas/Oil Inventory

Potential Liquidity Demands

Assumes negative Mark-to-Market exposure (MtM) with hard credit

thresholds would be collateralized with cash or Letters of Credit (LCs)

if firm is downgraded. Any corporate guarantees assumed to be

converted to cash or LCs

Negative MtM associated with contracts with adequate assurance (soft

trigger) is cash collateralized

Current 30-day accounts payable are immediately paid

Commercial paper with pay down terms in event of downgrade

Static margin at exchanges and regional transmission organizations

Triggers in various loans and contracts

Page 5How to Calculate “S&P Liquidity Adequacy Ratio”?

Two Ratios

CELA: Credit Event Liquidity Adequacy

MCELA: Market & Credit Event Liquidity Adequacy

Price stress by 15% for Year 1 and 20% or Years 2

and beyond

Same stress for all commodities

Test under both increase and decrease; report the

“worst case” outcome

The objective is to have $1 in liquidity to cover

every $1 in potential price-stressed liquidity

demands

This leads to a minimum ratio of 1.0x

It would be more conservative to apply this minimum

threshold to the MCELA ratio

Page 6Liquidity Adequacy Ratios By Industry Sector*

S&P Liquidity Adequacy Ratio1, by Industry Sector (2005)2

Downgrade3

w/out Price Downgrade3 with Price Stress5,

Stress, CELA4 MCELA6

Sector (Median) Median Lowest Highest

Exploration and production 5.90 3.78 0.40 5.30

Merchant energy 5.90 3.93 Not avail Not avail

Regulated electric utilities 2.98 2.11 0.90 5.50

Diversified 2.07 1.46 0.55 3.75

Utilities with large gas-marketing operations 1.23 1.09 0.75 1.85

Integrated oil, midstream and refiners 1.11 0.96 Not avail Not avail

1. Liquidity Adequacy Ratio = Liquidity / Potential Liquidity Demands. Objective is to exceed 1.0.

2. Source: S&P, "S&P Survey Highlights Weakness in Liquidity Risk Management in the U.S. Energy

Industry", 12-May-2005.

3. Downgrade to any credit rating below investment grade or call for adequate assurance.

4. CELA = Credit Event Liquidity Adequacy (Credit event only, no price stress)

5. S&P Price Stress assumes 15% for first 12 months and 20% for Years 2 and beyond.

6. MCELA = Market & Credit Event Liq. Adequacy (Credit event plus price stress)

*Source: S&P, “S&P Survey Highlights Weaknesses in Liquidity Risk

Management in the U.S. Energy Industry,” May 12, 2005.

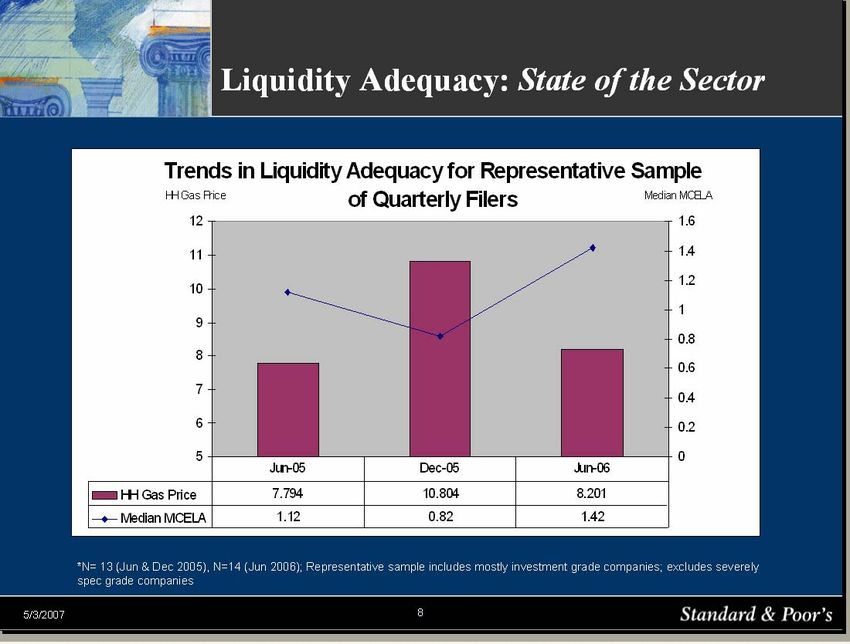

Page 7Trends in Liquidity Adequacy*

*Source: Used by permission by Jeanny Silva, S&P

Page 8S&P’s Perspective of Recent Liquidity Adequacy Trends*

Average MCELA is up 16% relative to a year ago

Average primary liquidity is up 25%

Expanded bank lines account for most of improvement- up

42%

But unrestricted cash balances down 34%

While average total credit exposure is up only 9%

Increase in credit exposure mostly due to higher CP balances

Average total net exposure (MTM+60 day, after netting) is

actually down 4%

MTM still dwarfs 60-day exposure (on average)

Out-of-the money contracts are either rolling off or being

replaced

Collateral posted as % of total net exposure is only

marginally up (2%)

Counterparties have not reduced or otherwise modified

contract credit terms

*Source: Used by permission by Jeanny Silva, S&P

Page 9How Does S&P Incorporate Liquidity Adequacy Ratios

in its Analysis*?

CELA and MCELA ratios are only part of the overall liquidity

analysis. S&P also considers:

Upcoming debt maturities

Ability to tap capital markets

Ability to work with counterparties/banks to re-negotiate

collateral provisions or increase bank lines

Flexibility to postpone planned capital expenditures

Ability to exit one or more trading business lines if needed

*Source: Used by permission by Jeanny Silva, S&P

Page 10Some Additional S&P Feedback As long as ratio is greater than 1.0x, S&P has traditionally not addressed the ratio further with companies. The emphasis is larger for companies with trading, marketing and/or merchant activities More accepting of

Individual Companies Further Customize or Approach

Liquidity Adequacy from their Own Perspective

Informally surveyed firms on Philadelphia Utilities Index

Most companies use both S&P ratio method but also customize for their

needs

Company A

Created similar model 18 months before S&P first requested; focus on 95%

confidence interval; now considering 99%

Company B

Customizing for worst exposure which increases as prices fall but load volumes

increase. Uses 99% confidence interval. Instead of looking backwards, look

forward over next 90 days. We set risk limits on this measurement and notify as

needed.

Company C

Assume prices returns to historical peak levels plus two sigma accompanied by

a fixed cash drain scenario

Company D

Stress is in 40-50% range. Covert all exposures to BCF Equivalent (BCF).

Compare stressed liquidity demands against available headroom between

primary liquidity and non-stress liquidity demands. Headroom must always be

adequate, particularly during cash-flow “pinch point” months of January and

July.

Page 12Communicating to Upper Management

to Enhance Decision Making

Easy to understand, easy to calculate

Directly links to discussions with Treasury and

Bankers

The “S&P” Good Housekeeping Label helps

Most companies interviewed report both S&P

ratio and customized ratios to their risk

committees and Board of Directors

Page 13Different Graphical Presentation Approaches

Fictional data, does not represent Entergy or any company, and provided for illustrative purposes only

S&P Liquidity Adequacy Ratio Historical Liquidity Adequacy Ratio

Near-term liquidity / price-stressed margin calls (Fictional Company Data)

3.5

Downgrade Only

3.0 (CELA)

S&P Liquidity Ratio

2.5

Downgrade &

2.0 Price Stress

(MCELA)

1.5

1.0 Target (= 1.0)

0.5

0.0

Qtr A Qtr B Qtr C Qtr D Qtr E Qtr F Proj Proj

Qtr F Qtr G

Date

Liquidity and Potential Demands (Stressed)

Quarter A Change in Change in Quarter B Change in Change in Quarter C (Actual and Projections)

Liquidity Demands Liquidity Demands

80.0

70.0

60.0

50.0 Revolver (Avail)

$50 Cash

40.0

$

$40 $45 MTM

$30 $30

30.0 $35 60-Day Demands

20.0 $15

$10

$15 $15

10.0 $15

$20 $20

$15

$20

$10 $10 $10

$5 $5

0.0

A B C D E

tr tr tr tr tr

Q Q Q jQ jQ

ro P ro

P

Page 14Sample of Some Industry Perspectives*

☺

Overall positive industry attitude

&

Does S&P even use?

Helped put liquidity on map, even S&P author did not mention

among non-risk folks liquidity adequacy in Top 10

Does the job even if it is a bit utility issues

quirky Volatility assumptions inverted

Believes that there are more firms and too low

fighting to be BB+ to avoid death Adequate assurance is not 100%;

spirals more like 25-40% pay down

Looking for vendors to help ease Some firms cannot gather data in

calculation order to calculate

Commercial folks must identify or If focus on ratio, can drive

acquire liquidity source before “wrong behavior” by increasing

committing to new contracts liquidity to cover dangerous

Great for “apples to apples” liquidity drains

comparisons Will S&P focus instead on new

PIM?

* Informal survey of integrated electric utilities listed in the Philadelphia Utility Index

Page 15Summary

Relatively easy to calculate… can be customized

for internal analysis

Ratios differ according to underlying risk of

industry sector

Effective communication can enhance decision

making

Generally positive industry attitude even if

companies have not heard a lot of feedback from

S&P itself

Page 16For More Information

John Wengler

Chief Risk Officer

Entergy Services, Inc.

832-681-3367

jwengle@entergy.com

Page 17You can also read