The Income-Distributional Impacts of Canadian Monetary Policy and Commodity-Price Shocks

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Income-Distributional Impacts of Canadian

Monetary Policy and Commodity-Price Shocks

Carlo Tolentino

Bachelor of Arts (Honours), University of Victoria, 2019

An Extended Essay Submitted in Partial Fulfillment

of the Requirements for the Degree of

MASTER OF ARTS

in the Department of Economics

We accept this extended essay as conforming

to the required standard

Dr. Graham Voss, Co-Supervisor

Department of Economics, University of Victoria

I hereby approve Carlo’s essay as complete. This is in lieu of my

signature.

Dr. Judith Clarke, Co-Supervisor

Department of Economics, University of Victoria

©Carlo Tolentino, 2021

University of Victoria

All rights reserved. This extended essay may not be reproduced in whole or in part,

by photocopy or other means, without the permission of the author.

Abstract This paper examines the income-distributional impacts of commodity-price shocks and monetary shocks by analyzing the impacts of these shocks on income-specific consumer price indices (ISCPI) in Canada. An ISCPI is the price index for the aggregate consumption basket for households within a range of income. I construct ISCPIs using consumer spending micro-data and disaggregated price index data from Statistics Canada, which I convert to income-specific inflation rates (ISIRs). I then estimate exogenous monetary and commodity-price shocks using a Structural Vector Autoregression. Finally, I estimate the impulse response functions (IRFs) of the ISIRs to commodity-price shocks and monetary shocks using the Local Projections Method (Jordà, 2005). I find no statistically significant di↵erence between the IRFs of di↵erent ISIRs to monetary shocks. In contrast, the IRF of the ISIR for middle- income households, as a response to commodity-price shocks, is larger than the IRFs for the ISIRs of low-income and high-income households. I find no statistically significant di↵erence between the IRFs of the ISIR of the bottom-income and top- income households to commodity-price shocks.

1 Introduction

Carolyn Wilkins, The Deputy-Governor of the Bank of Canada, states that

Canadian monetary policy “will be judged against how they a↵ect the distribution of

income and wealth in [Canada]” (Press, 2020, p.1). Monetary policy has distributional

impacts if it heterogeneously a↵ects prices of consumption baskets because of variations

in income. Similarly, commodity-price shocks will have distributional impacts if

it also heterogeneously a↵ects prices of consumption baskets. This essay aims to

analyze how Canadian monetary policy and commodity-price shocks impact the

price of di↵erent Income-Specific Consumer Price Indices (ISCPI). An ISCPI is the

price index of the aggregate consumption basket for households within an income-

percentile range. An income-percentile range is defined as a range of income between

two percentile values of household income. This topic’s premise is that if monetary

and commodity-price shocks a↵ect the prices of goods heterogeneously, and households

of di↵erent incomes consume di↵erent goods, then these macroeconomic shocks have

income-distributional impacts.

I compare three income-percentile ranges of ISCPIs: The bottom 10%, the top

10%, and the ISCPI for those between the 45th and 55th of percentiles of household

income. I convert each ISCPI into income-specific annual inflation rates (ISIR).

Therefore, let ⇡tB denote the income-specific inflation rate for households making

less than the 10th percentile of household income. Let ⇡tM denote the income-

specific inflation rate for households making between the 45th and 55th percentiles of

1

household income. Let ⇡tT denote the income-specific inflation rate for households

making more than the 90th percentile of household income.

I find no statistically significant di↵erence between the responses of the three

ISIRs to monetary shocks. However, I find a statistically significantly di↵erent

response of ⇡tM , from the responses of ⇡tT and ⇡tB , to commodity-price shocks.

The responses of the ⇡tT and ⇡tB to commodity-price shocks are not statistically

significantly di↵erent from each other. More specifically, after two quarters, a one

percentage-point change in commodity-price causes: a 0.032 percentage-point increase

in ⇡tB , a 0.041 percentage-point increase in ⇡tM , and a 0.036 percentage point increase

in ⇡tT . The policy implication of my results show that monetary policy may not

have distributional impacts in Canada. However, my results show that positive

commodity-price shocks may harm middle-income households more than low-income

or high-income households, since they have greater unanticipated price increases in

their consumption basket.

The main literature this essay builds upon is the econometric results of Cravino,

Lan, and Levchenko (2020). Cravino et al. (2020) analyze the distributional impacts

of monetary policy along the income-distribution, using data from the US. In this

essay, I analyze the same research question as Cravino et al. (2020) but using

Canadian data. I also expand on Cravino et al. (2020) by also looking at the

distributional impacts of commodity-price shocks on Canadian households. Cravino

et al. (2020) find that the consumption baskets of high-income and low-income

2households are less price-volatile than middle-income households because middle-

income households consume more goods that are more price volatile, relative to

high-income and low-income households. Cravino et al. (2020) also find that the

impulse responses of the ISCPI for those in the top 1% household income are one-

third smaller than the ISCPI of middle-income1 households as a response to monetary

shocks. One main di↵erence between this essay and Cravino et al. (2020) is that

Cravino et al. (2020) uses the Romer Narrative approach to identify monetary policy

shocks (Romer and Romer, 2004). In contrast to Cravino et al. (2020), I am using

a Structural Vector Autoregression (SVAR) to identify exogenous shocks2 . I use

the same Local Projection Method (Jordà, 2005) to estimate IRFs as Cravino et al.

(2020).

A paper that uses Canadian data to analyze monetary policy’s distributional

impacts in Canada is Kronick & Villarreal (2019). Kronick & Villarreal (2019) uses

the same method as Cravino et al. (2020) and the same Canadian data that I

am using in constructing ISCPIs. However, Kronick & Villarreal (2019) focus on

analyzing how low inflation a↵ects inequality and how inequality a↵ects monetary

transmission. Using an SVAR technique, Kronick & Villarreal (2019) find that

expansionary monetary policy increases income inequality in Canada, as measured

by the GINI Index (Gini, 1921). Secondly, Kronick & Villarreal (2019) find that

1

The middle-income households in Cravino et al. (2020) are households who are between the

th

40 and 60th percentile of household income

2

I am not able to do narrative approach in this essay because of time-constraints in writing this

essay. To my knowledge, only one paper has analyzed monetary shocks in Canada using a narrative

approach (Champagne & Sekkel, 2018). A further discussion on the narrative approach is in Section

6

3the estimated inflation response to monetary shocks could be overestimated if the

estimation does not account for inequality. Like, Cravino et al. (2020), my focus

is on the di↵erence in the responses ISCPIs to macroeconomic shocks, rather than

overall inequality.

While Cravino et al. (2020) and this essay focus on a consumer’s entire consumption

basket, Kim (2019) looks at monetary policy’s e↵ect among the same product category

with variations in quality. Kim (2019) finds that high-quality products are more price

rigid than low-quality products in the same product category, such as milk-based

drinks. Kim (2019) finds that consumers with higher incomes tend to buy higher-

quality products than low-income consumers. Therefore, Kim (2019) concludes that

an expansionary monetary shock will benefit high-income consumers more than

low-income consumers. Conversely, Kim (2019) finds that contractionary monetary

shocks will harm high-income consumers more than low-income consumers.

Generally, Kim (2019) and Cravino et al. (2020) both find that monetary shocks

has significant distributional impacts in the US, particular between the middle-

income Americans and high-income Americans; In contrast, I find that Canadian

Monetary shocks has no significant distributional impact between middle-income

Canadians and high-income Canadians. A potential explanation why monetary

shocks has greater impact in the US, in contrast to Canada, may be due to the wider

income-gap between the middle-income Americans and high-income Americans. Saez

& Zucman (n.d.) find that in 2019, a median-income person in American earns about

4$48,000 USD per year, while an American in the 99th percentile of income earns about

$580,000 USD per year. In Canada, Statistics Canada (n.d.D) finds that in 2018, the

median-income Canadian earns about $36,000 CAD a year while a Canadian in the

99th percentile of income earns about $250,000 CAD a year. Although the exchange

rate between the Canadian and US dollar is not a perfect one-to-one exchange, there

is still a substantial di↵erence between the top 1% of earners in the US compared to

the top 1% of earners in Canada; This di↵erence in income could result in di↵erences

in consumption baskets, which leads to di↵erences in reaction to monetary shocks.

My essay contributes to the literature on the distributional impacts of monetary

policy and commodity-price shocks in Canada; More specifically, my paper analyzes

the impact of these macroeconomic shocks on the price of income-specific consumption

baskets, which, to my knowledge, has not been analyzed in Canada.

This essay proceeds as follows: Section 2 introduces the data. Section 3.1

explains the Structural Vector Autoregression (SVAR) for identifying exogenous

shocks. Section 3.2 explains the Local Projection Method (LPM) empirical strategy

for estimating the IRFs of the ISIRs. Section 4 presents and discusses key results

from the SVAR procedure. Section 5 discusses the results of the LPM. Section 6

concludes this essay with a discussion and o↵ers potential extensions to this essay.

Appendix I presents an additional set of figures and tables not included in the main

body of this essay. Appendix II presents the rest of the IRFs from the SVAR not

discussed in Section 4.

52 Data

2.1 Construction of the Income-Specific CPIs

An Income-Specific CPI, for those in an income-percentile range p, at time t, is

defined as

n

X

CP Ipt = wip Xit (1)

i

Where wip denotes the expenditure weights for item category i for the income-

percentile range p, Xit is the price index for category i at time t, and n is the number

of product categories included. I construct the expenditure category weights, wip 3 ,

as

ip

wip = Pn (2)

i ip

Where ip is the total expenditure in category i for those in the pth income-percentile

range. Note that the denominator is the total expenditure of the categories included,

not total expenditure in the survey (since I have omitted some categories), and not by

total income since the average propensity to consume di↵ers among di↵erent income

groups.

Therefore, constructing the ISCPI requires finding the income cuto↵s for each

income-percentile range, constructing the expenditure weights, and combining the

3

The expenditure weights are time-invariant because I only have data for 2017. Ideally, if

consumer spending data was available for every time-period, expenditure category weights would

be indexed by time.

6expenditure weights with a price index. I use the 2017 version of the Survey of

Household Spending (SHS) from Statistics Canada (Statistics Canada, 2019a) and

Table-18100004 from Statistics Canada (n.d.A), henceforth ”CPI dataset,” to construct

the ISCPIs.

The CPI dataset has price indices for di↵erent item categories, which is a table

of 330 monthly series of consumer price indices for di↵erent categories of goods

and services, with monthly observations from 1941-01 to 2020-07. However, not all

categories have observations for every date. I only use a sample length from 1989-1

to 2020-3. The CPI dataset is not seasonally adjusted and contains price indices at

di↵erent levels of aggregation, from “All-Items” to “Non-durable goods” and to finer

levels like “Butter.”

The Survey of Household Spending (SHS) from Statistics Canada (Statistics

Canada, 2019a) contains household spending and household income data. The SHS

encompasses all provinces and territories of Canada and is a representative sample

of Canada. The survey has two components, the “Interview” and the “Diary.” A

sample of 12,492 responded to the Interview component, then a sub-sample of those

who did the Interview responded to the Diary. The Diary has a sample size of 4012

respondents, which has finer expenditure categories compared to the Interview. The

Interview collection method involves a questionnaire asking the respondents to recall

their expenditure within a specific period (i.e. last month, last three months, etc.).

In contrast, the Diary requires a respondent to journal their expenditure within a

7two-week time frame. The SHS data collection occurs throughout the year, so the

SHS respondents do not report their spending all in the same time-frame. The

survey reports annual income and annual expenditure; therefore, reported values are

annualized when survey respondents answer a question with less than a 12 month

recall period.

I only use the Diary component for this essay as it is a more detailed spending

dataset. Statistics Canada has a user guide for the SHS, further explaining the

dataset in more detail (2019b). The SHS also comes with a document titled “Expenditure

category hierarchy,” which explains the spending categories and the hierarchy of

categories and subcategories within the Interview and Diary (Statistics Canada,

2019c).

The SHS orders the spending categories in six levels. Table 1 in Appendix I

reports a sample from each category to illustrate the disaggregation in each level.

I mostly work with level 3 category expenditures, occasionally using level 2 or 4

because certain categories in the Diary could not be matched with the CPI dataset.

Table 2 in Appendix I shows the categories I use and their labels in both the Diary

and CPI dataset. I match the labels from the Diary to the CPI dataset in creating the

ISCPIs. Given that the Diary and CPI dataset both came from the same statistical

agency, I was able to find similar labels between the CPI dataset and the Diary,

which I am assuming that similar labels across the dataset are referring to the same

goods. I omit four categories because they did not match well between the two

8datasets: “Pet expenses,” “Garden supplies and services,” “Games of Chance,” and

“Miscellaneous expenditures.”

I use the total household income reported in the SHS to calculate the income

cuto↵ values in constructing the ISCPIs; These values are reported in Table 3 in

Appendix I.

I then combine the expenditure weights with the CPI dataset using equation (1) to

construct the ISCPIs. The frequency of ISCPIs is originally at a monthly frequency,

which I convert to a quarterly series by averaging over the quarter. For each ISCPIs,

I apply the natural log, take the fourth seasonal di↵erence and multiply by 100,

which ultimately creates an annualized ISIR from 1990Q1 to 2020Q1. I denote the

annualized ISIR as ⇡tp , where p denotes the income-percentile range. Specifically,

let ⇡tB denote the income-specific inflation rate for those making less than the 10th

percentile of household income. Next, let ⇡tM denote the income-specific inflation

rate for those making between the 45th and 55th percentiles of household income.

Finally, let ⇡tT denote the income-specific inflation rate for those making more than

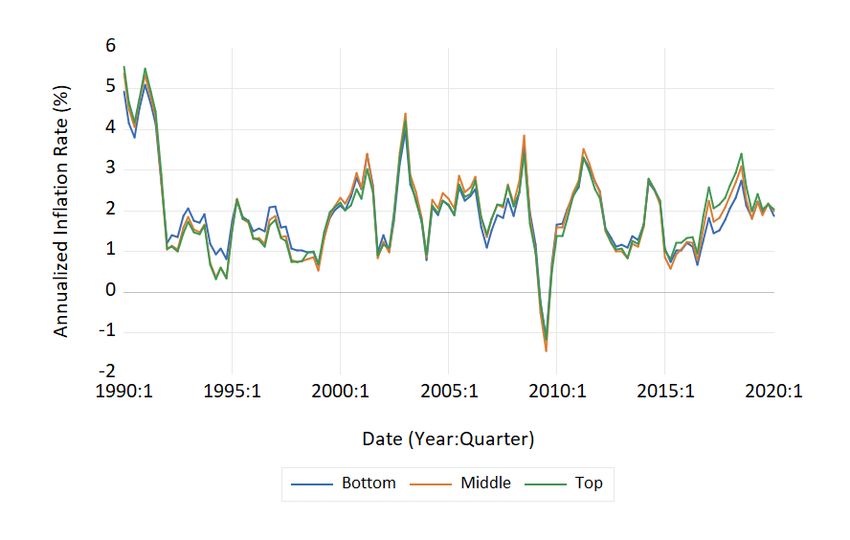

the 90th percentile of household income. Figure 1 depicts the time-series graph of

the ISIRs and shows that the ISIRs are indeed heterogeneous.

9Figure 1: Time-series Plot of the Income-Specific Inflation Rates.

2.2 Data for the Structural Vector Autoregression

The CPI dataset also contains a monthly series for the all-item CPI. I use the

all-item CPI from 1989-01 to 2020-03, converting into a quarterly series by averaging

over the quarter. I take the natural log and the fourth seasonal di↵erence of the

all-item CPI and multiply it by 100, which creates the annualized inflation rate in

Canada, from 1990Q1 to 2020Q1. I denote the Canadian inflation rate as ⇡tall .

Similarly, I use a monthly series of the all-commodities price index from Statistics

Canada (n.d.B) from 1989-01 to 2020-03. I convert the all-commodities price index

10to a quarterly series by averaging over the quarter. Again, I apply the natural log

and the fourth seasonal di↵erence of the all-commodities price index and multiply

the series by 100, which I denote as dlCt .

Next, I use a quarterly series that measures the Canadian output gap using an

extended multivariate filter, from 1990Q1 to 2020Q1 from the Bank of Canada (n.d.),

which I denote as CANt . I also create a measure of the US output gap by using a

quarterly series of the US Real GDP (seasonally adjusted annual rate) from the

U.S. Bureau of Economic Analysis (n.d), which I take the natural log of the series,

applying the Hodrick-Prescott Filter (Hodrick and Prescott, 1997) with a smoothing

parameter of 1600, and then multiplying the series by a 100. I denote the series for

the US output gap as U St .

Finally, I also use a monthly series of the 7-day average annualized overnight

rate in Canada from Statistics Canada (n.d.C) from 1989m9 to 2020m3. I convert

the overnight rate series into a quarterly series by averaging over the quarter, which

I denote as it . Figure 1 in Appendix I displays it in levels, which appears to be

trending. I test for the presence of a unit-root using the Augmented Dickey-Fuller

test (Dickey and Fuller, 1979), in which I fail to reject the presence of a unit root. I

take the first di↵erence of it to induce stationarity. I denote the annualized overnight

interest rate, in first di↵erences, as it . The series it spans from 1990Q1 to 2020Q1.

In summary, I have a quarterly series from 1990Q1 to 2020Q1 of the variables

11listed in Table 1. Table 1 summarizes the notation of each variable and provides a

description. Figure 2 in Appendix I shows the time-series plots of dlCt , U St , it ,

⇡tall , and CANt .

Table 1: Summary of Variables

Variable Notation Description of Variable

dlCt All-Commodities Price Index in logs and fourth-seasonal-di↵erences

U St US Output Gap

CANt Canadian Output Gap

it Overnight Rate in Canada in first-di↵erences

⇡tall Canadian Annual Inflation Rate

⇡tB Income-specific Annual Inflation Rate for households making less

than the 10th percentile of household income

⇡tM Income-specific Annual Inflation Rate for households making

between the 45th and 55th percentile of household income

⇡tT Income-specific Annual Inflation Rate for households making more

than the 90th percentile of household income

123 Empirical Strategy

3.1 Identifying Monetary Shocks

To identify exogenous monetary shocks I use the following Structural Vector

Autoregression (SVAR)

2 32 3 2 3 2 32 3

a 0 0 0 0 dlCt b c c12 0 0 0 dlCt 1

6 11 76 7 6 1 7 6 11 76 7

6 76 7 6 7 6 76 7

6a21 a22 0 0 07 6 7 6 7 6 07 6 U St 1 7

6 7 6 U St 7 6b2 7 6c21 c22 0 0 76 7

6 76 7 6 7 6 76 7

6a 07 6 7 6 7 6 c35 7 6CANt 1 7

7 6

6 31 a32 a33 0 7 6CANt 7 = 6b3 7+6c31 c32 c33 c34 7+

6 76 7 6 7 6 76 7

6 7 6 all 7 6 7 6 7 6 all 7

6a41 a42 a43 a44 0 7 6 ⇡t 7 6b4 7 6c41 c42 c43 c44 c45 7 6 ⇡t 1 7

4 54 5 4 5 4 54 5

a51 a52 a53 a54 a55 it b5 c51 c52 c53 c54 c55 it 1

2 32 3 2 3

d d 0 0 0 dlCt 2 ✏

6 11 12 76 7 6 1t 7

6 76 7 6 7

6d21 d22 0 0 07 6 7 6 7

6 7 6 U St 2 7 6✏2t 7

6 76 7 6 7

6d 76 7 6 7

6 31 d32 d33 d34 d35 7 6CANt 2 7 + 6✏3t 7 (3)

6 76 7 6 7

6 7 6 all 7 6 7

6d41 d42 d43 d44 d45 7 6 ⇡t 2 7 6✏4t 7

4 54 5 4 5

d51 d52 d53 d54 d55 it 2 ✏5t

In matrix notation, the SVAR is

AXt = B + CXt 1 + DXt 2 + ✏t (4)

where Xt is a vector containing the endogenous variables. The matrix A is the

parameters for the contemporaneous relationships among the endogenous variables.

The matrices C and D are the matrices of parameters for the vector autoregression

for the first and second lags of the endogenous variables. The Hannan–Quinn

information criterion (Hannan & Quinn, 1979) and Akaike information criterion

13(Akaike, 1981) indicate the SVAR should have two lags. Vector B consists of

constants, and vector ✏t consists of the structural shocks.

Since the SVAR aims to identify exogenous monetary shocks, I impose an additional

restriction on the SVAR that the structural shocks are uncorrelated4 .

2 3

2

1 0 0 0 0

6 7

6 7

60 2

0 0 07

6 2 7

6 7

E(✏t ✏t ) = 6

0

60 0 2

3 0 07

7 (5)

6 7

6 2 7

60 0 0 4 07

4 5

2

0 0 0 0 5

The restrictions on matrices A, C, and D impose that the previous period’s

and current values of the Canadian domestic variables do not impact commodity-

prices or the US output gap. However, the SVAR allows for the current period’s

commodity-price and the US output gap, as well as its lags, to influences the current

period’s Canadian domestic variables. I justify these restrictions on matrices A, C,

and D using the assumption that Canada is a small-open economy. As a small open

economy, world prices and the US economy are likely to be important external factors

for Canada, a small open economy. In contrast, we can assume that the Canadian

variables do not directly a↵ect the world commodity prices and the US economy.

4

Uncorrelated structural shocks is generally a standard assumption in the SVAR literature, since

it is necessary to identify exogenous shocks. Since the SVAR is just-identified this assumption can

not be tested.

14The lower-triangular restriction on matrix A imposes that variables listed first in

vector Xt (from top to bottom) will contemporaneously impact variables listed after

it; however, variables will not contemporaneously a↵ect variables listed before it.

Therefore, I impose the restriction that the overnight rate will not impact inflation

or the Canadian output contemporaneously. I am assuming that it takes time for the

economy to adjust to monetary policy, hence why the Canadian inflation rate and

Canadian output may not react to changes in the overnight rate contemporaneously.

3.2 Estimating Impulse Responses of Income-Specific Inflation

I estimate the IRFs of the ISIRs to the commodity-price shocks and overnight

rate shocks using the Local Projections Method (LPM) (Jordà, 2005). The LPM

is also the method Cravino et al. (2020) use in estimating IRFs. Since the SVAR

estimates the structural shocks, the LPM allows for a convenient way to extract

the structural shocks and separately estimate the IRFs without estimating another

SVAR which includes the ISIRs. The LPM also has other desirable properties such

as being more robust to misspecification and can be estimated by OLS. (Jordà, 2005).

Let h denote the number of quarters after a shock that occurs at time t. I

estimate the following regression using OLS, h number of times, for each income-

specific inflation rate.

j k

p

X X p

⇡t+h = ↵h + h Shockt + hi Shockt i + hi ⇡t i + eth (6)

i=1 i=1

15where ⇡tp is the ISIR for the pth income-percentile range and Shockt is the structural

shock of interest, which is estimated using equation (4). The coefficient of interest is

h, which gives the impulse response of ⇡tp at the hth period after a monetary shock

occurring at time t.

The control variables are j number of lags of the shock of interest, denoted by

Shockt j , and k number of lags of the ISIR, denoted by ⇡t k . The number of lags

for the shock of interest and ISIR are chosen to ensure that the residuals are a

approximately a white-noise series.

Essentially, estimating equation (6) using LPM involves first estimating

j k

X X

⇡tp = ↵0 + 0 Shockt + 0i Shockt i + p

0i ⇡t i + et0 (7)

i=1 i=1

and storing the estimated coefficient b0 ; then applying the lead operator to the

dependent variable and estimating

j k

p

X X p

⇡t+1 = ↵1 + 1 Shockt + 1i Shockt i + 1i ⇡t i + et1 (8)

i=1 i=1

which iterates h numbers of times, yielding b0 = [ b0 , ..., bh ]. Plotting b over time

produces the IRFs graphs of the ISIR to the shock of interest.

I specify the control variables of LPM for the overnight rate shock as j = 6 and

k = 6. I specify the the control variables of LPM for the commodity-price shock

16as j = 2 and k = 6. Again, j and k are selected to ensure that the residuals

of the LPM are approximately a white-noise series. In choosing the appropriate

control variables, I estimate a regression of aggregate inflation against overnight rate

shocks and commodity-price shocks, and inspecting the residuals ex post. Table

4 in Appendix I shows the correlogram of the residuals from regressing aggregate

inflation against overnight rate shocks, six lags of overnight rate shocks, and six

lags of aggregate inflation. Table 5 in Appendix I shows the correlogram of the

residuals from regressing aggregate inflation against commodity price shocks, two

lags of commodity-price shocks, and six lags of aggregate inflation.

Finally, let b standard error of the estimated coefficient5 . I construct the 90%

confidence interval (CI) for the LPM IRFs using

CIh = bh ± 1.65 ⇤ ch (7)

5

Since the structural shocks are generated regressors, the standard errors may be incorrectly

estimated (Pagan, 1984). A potential extension to this paper could re-estimate the standard errors

using simulation methods.

174 Results of the Structural Vector Autoregression

In this section, I discuss the key results of the SVAR. I particularly present the

IRFs of the Canadian domestic variables to the overnight rate shocks and commodity-

price shocks. I then compare the results of the SVAR to other papers that estimate

shocks through di↵erent SVAR methods. Appendix II contains the rest of the IRFs

not discussed in this section.

In macroeconomic theory, a central bank can increase interest rates to lower

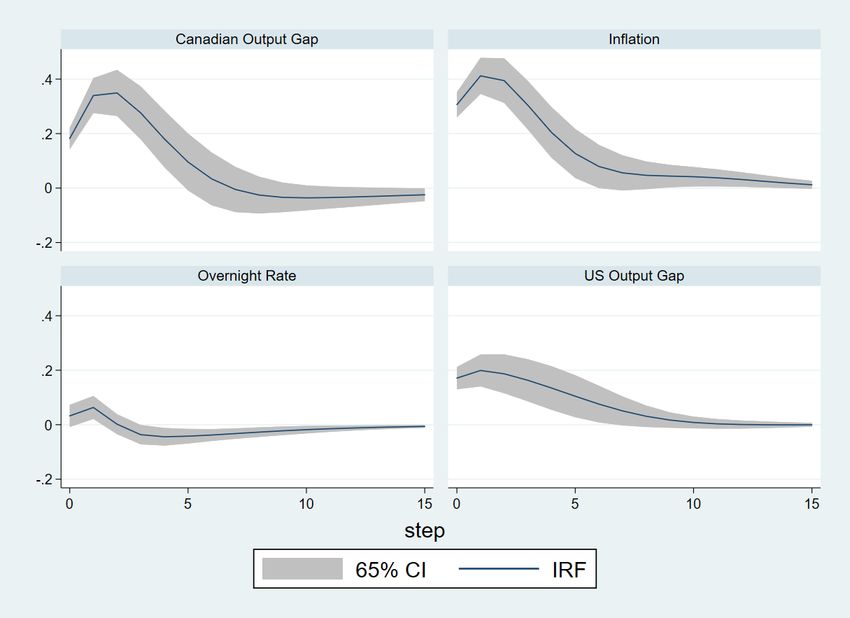

economic output and ultimately lower inflation. Figure 2 depicts the reaction of ⇡tall

and CANt to a one standard deviation shock to it . The results are as follows: A

one standard deviation shock to it causes a peak fall of -0.079 percentage-point

to the CANt two quarters after the shock, and a peak fall of -0.062 percentage-

point to ⇡tall three quarters after the shock. Papers that use a structural model

to identify monetary shocks also find a negative response of output and inflation to

overnight rates shocks, such as Bhuiyan (2012), Cushman (1997), and Raghavan et al.

(2016). For example, Cushman (1997) estimates an SVAR for the Canadian economy

using the US macroeconomic variables (such as output, industrial production and

the federal funds rate) as a source of exogenous shocks to the Canadian economy.

Cushman (1997) finds that a contradictory monetary shock causes a slight decrease

in Canadian output and Inflation. Raghavan et al. (2016) use a structural Vector

Autoregressive Moving Average (SVARMA) with oil-price shocks and the US federal

funds rate as external shocks to the Canadian economy. Raghavan et al. (2016) find

18that a positive shock to the Canadian overnight rate causes output and inflation to

decline. Similarly, using a Bayesian SVAR, Bhuiyan (2012) also finds that Canadian

monetary shocks cause a decrease in Canadian output and inflation.

Commodities are a major component of Canada’s economic output; hence we can

expect a positive shock to commodity-prices should be expansionary to the Canadian

(and the US) economy. Figure 3A depicts the reaction of the other variables in the

SVAR to a one standard deviation shock to dlCt . The result are as follows: A one-

standard-deviation shock to the dlCt causes a 0.1992 percentage-point increase in

U St after a quarter, a 0.3492 increase to CANt after two quarters, a 0.4120 increase

in ⇡tall , and a 0.0632 increase to it after one quarter. Figure 3B depicts the reaction

of dlCt to shocks to itself, which shows that dlCt will increase in the first year, but

its reaction is quite muted afterwards. Martel (p.9, 2008) also finds that “an energy

price shock implies a sharp increase in the price of energy, but this e↵ect is somewhat

muted thereafter.” Martel (2008) finds that oil-price shocks cause a positive increase

in Canadian output and inflation rate. Raghavan et al. (2016) also find that oil-price

shocks cause a positive increase in US Output, Canadian output, Canadian inflation

and Canadian interest rates.

19Figure 2: The Impact of it Shocks to the Canadian Variables

Note: The impulse variable is a one standard deviation shock to it . The gray area

represents a 65% confidence interval.

20Figure 3A: The Impact of dlCt Shocks

Note: The impulse variable is a one standard deviation shock to the dlCt . The gray

area represents a 65% confidence interval.

21Figure 3B: The IRF of dlCt to dlCt Shocks.

Note: The impulse is a one standard deviation shock to dlCt . The gray area

represents a 65% confidence interval.

225 Results of the Local Projections Method

My main objective in this paper is to examine the distributional impacts of

commodity-price shocks and overnight rate shocks. Figure 4 shows the IRFs of each

ISIR, with 90% confidence intervals, to overnight rate shocks. I use a 90% confidence

interval, rather than the 65% confidence interval, for the LPM IRFs since the LPM

estimates the IRFs using OLS, which I expect to be a more efficient estimator in

comparison to an SVAR. Figure 5 shows the IRFs of the three ISIR to overnight rate

shocks in the same graph.

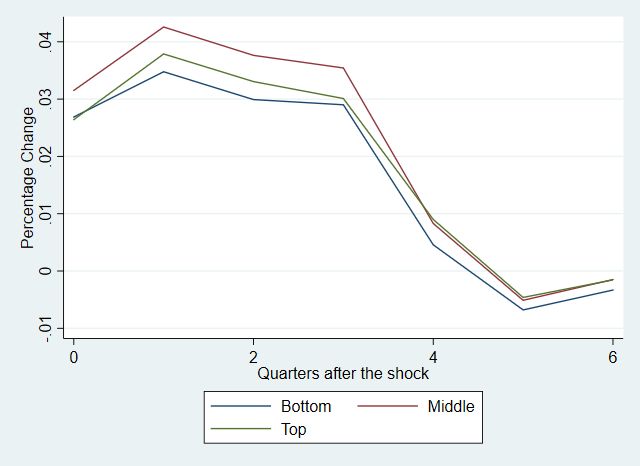

Figure 4 indicates that overnight rate shocks have the greatest impact on the

ISIRs at the 15th quarter after the shock, and these impacts are statistically significantly

di↵erent from zero at a 10% significance level. Focusing on the 15th quarter after a

shock to the overnight interest rate, a one percentage-point increase in the overnight

rate decreases: ⇡tB by 0.407 percentage-points, ⇡tM by 0.467 percentage-points, and

⇡tT by 0.429 percentage-points. However, re-estimating the LPM regressions as a

system and testing for coefficient equality shows that the responses of the ISIR to

overnight rate shocks are not statistically significantly di↵erent from each other.

Note that the IRFs from the LPM are di↵erent to the SVAR IRFs in terms of the

time-horizon in which monetary shocks a↵ect inflation; This may be attributed to

the fact that the SVAR contains the additional e↵ects from the fall from output,

while the LPM only contains the lags of the overnight rate and its lags. However,

the result of interest still remains that the reaction of the di↵erent ISIRs are not

23statistically significantly di↵erent from each other.

My results are in contrast to Cravino et al. (2020), who finds an economic and

statistically significant di↵erence between the responses of the top-income household

to the middle-income households. However, Cravino et al. (2020) define middle-

income households as households between the 40th and 60th percentile of household

income and compares it to the top 1% of households in household income; while I

define middle-income households those who are between the 45th and 55th percentile

of household income, and I compare the middle-income households to the top 10%

of households. To be consistent with Cravino et al. (2020), I construct the ISIR for

those between the 40th and 60th percentile of household income, which I denote as

⇡tx , as well as the ISIR of the top 1% of households, which I denote as ⇡ty . Figure

6A shows the IRF of ⇡tx , while Figure 6B shows the ISIR for ⇡ty , and Figure 7 shows

the two IRFs in a single graph. Focusing on the 15th quarter after the overnight

rate shock, I find no statistically significant di↵erence between the IRF of ⇡tx and

⇡ty . These results show that monetary policy may not have distributional impacts,

at least for the percentiles and definitions that I consider.

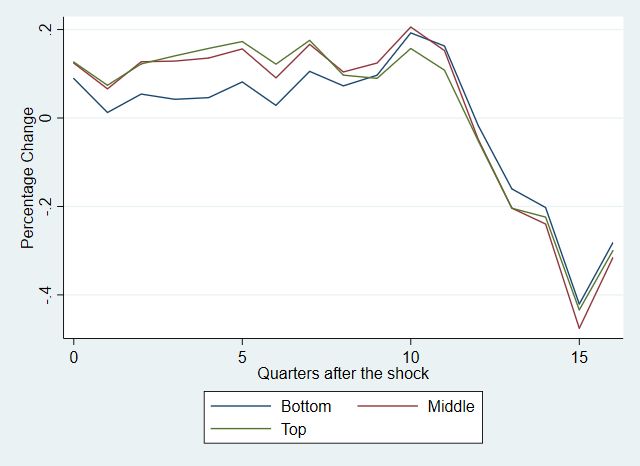

Figure 8 shows the IRFs of each ISIR, with 90% confidence intervals, to commodity-

price shocks. Figure 9 shows the IRFs of the three ISIR to commodity-price shocks,

in the same graph. Figure 8 indicates that commodity-price shocks have the peak

impact on ISIRs at the 1st quarter after the shock, and these impacts are statistically

significantly di↵erent from zero at a 10% significance level. Therefore, focusing on the

241st quarter after a shock to dlCt , the results show that a one-percentage-point change

in dlCt increases: ⇡tB by 0.032 percentage-points, ⇡tM by 0.041 percentage-points, and

⇡tT by 0.036 percentage-points. Re-estimating the LPM IRFs as a system and testing

for coefficient equality shows that the response of ⇡tM is statistically significantly

di↵erent, at a 1% significance level, to the responses of ⇡tT and ⇡tB , to commodity-

price shocks. I find no statistically significant di↵erence between the response of ⇡tT

and ⇡tB to commodity shocks. My results show that positive commodity shocks may

harm middle-income households more than low-income or high-income households

because they have greater unanticipated price increases in their consumption basket;

A further discussion of these results are in Section 6.

25Figure 4A: IRF of ⇡tB to Overnight Rate Shocks.

Note: The shock is a one percentage point increase in the overnight rate. The green

lines denote a 90% confidence interval.

26Figure 4B: IRF of ⇡tM to Overnight Rate Shocks.

Note: The shock is a one percentage point increase in the overnight rate. The green

lines denotes a 90% confidence interval.

27Figure 4C: IRF of ⇡tT to Overnight Rate Shocks.

Note: The shock is a one percentage point increase in the overnight rate. The green

lines denotes a 90% confidence interval.

28Figure 5: IRF of ⇡tB , ⇡tM and ⇡tT to Overnight Rate Shocks.

29Figure 6A: IRF of ⇡tx to Overnight Rate Shocks.

Note: The shock is a one percentage point increase in the overnight rate. The green

lines denotes a 90% confidence interval.

30Figure 6B: IRF of ⇡ty to Overnight Rate Shocks.

Note: The shock is a one percentage point increase in the overnight rate. The green

lines denotes a 90% confidence interval.

31Figure 7: IRF of ⇡tx and ⇡ty to Overnight Rate Shocks.

32Figure 8A: IRF of ⇡tB to Commodity-Price Shocks.

Note: The shock is a one percentage-point increase in dlCt . The green lines denote

a 90% confidence interval.

33Figure 8B: IRF of ⇡tM to Commodity-Price Shocks.

Note: The shock is a one percentage-point increase in dlCt . The green lines denote

a 90% confidence interval.

34Figure 8C: IRF of ⇡tT to Commodity-Price Shocks.

Note: The shock is a one percentage-point increase in dlCt . The green lines denote

a 90% confidence interval.

35Figure 9: IRF of ⇡tB , ⇡tM and ⇡tT to Commodity-Price shocks.

366 Conclusion

This essay aims to examine the distributional impacts of commodity-price shocks

and monetary shocks along the income-distribution. I construct income-specific

inflation rates (ISIR) using micro-data and price index data from Statistics Canada.

I estimate the impulse response of these ISIRs, to macroeconomic shocks, using the

Local Projections Method (LPM) (Jordà, 2005). I find no statistically significant

di↵erence between the reaction of the ISIRs among di↵erent income groups to monetary

shocks. In contrast, the reaction of the ISIR of middle-income households is greater

than the reactions of ISIRs of high-income and low-income households to commodity-

price shocks.

To understand why middle-income households are more reactive to commodity-

price shocks, a potential extension could analyze the reaction of the price index of

di↵erent categories of goods to commodity shocks and contrast these reactions with

the weights of each category in di↵erent income-specific consumption baskets. Table

6 in Appendix I shows each category’s weights in constructing the ISIR for each

income-group. Table 6 in Appendix I shows that “vehicle operations” has a higher

weight in the consumption basket of middle-income households in comparison to

low-income and high-income households. One particular sub-category contained in

“vehicle operations” is gasoline consumption. Since gasoline prices may be volatile

and reactive to commodity-price shocks, this may be one of the reasons why middle-

income household are more reactive to commodity-price shocks, in comparison to

37low-income and high-income households.

Since commodity-price shocks and overnight rates shocks are the residuals of

an SVAR, these shocks are therefore generated regressors. As Pagan (1984) points

out, the estimated standard errors for generated regressors are incorrectly estimated.

Therefore, a potential extension to this essay is to correct for the incorrectly estimated

standard errors of the generated regressor through simulation methods. Another

potential extension to this paper is to estimate exogenous monetary shocks for

Canada using a narrative-approach (Romer and Romer, 2004). Monetary shocks

estimated through a narrative-approach is what Cravino et al. (2020) use in estimating

the IRFs of income-specific inflation rates to monetary shock. Identifying monetary

shock through a narrative-approach would require cataloguing press statements from

the Bank of Canada to track the exact date when the Bank of Canada changes the

overnight rate and by how much the Bank of Canada changes the interest rates. A

narrative-approach also circumvents the issues associated with generated regressors

since a separate SVAR is no longer be required to identify exogenous shocks. To my

knowledge, Champagne & Sekkel (2018) is the only paper that apply the narrative-

approach in Canada.

38References

Akaike, H. (1981). Likelihood of a model and information criteria. Journal of

Econometrics, 16(1), 3-14.

Bank of Canada (n.d.). Product Market: Definitions, Graphs and Data, Estimates

of the Output Gap. https://www.bankofcanada.ca/rates/indicators/capacity-and-

inflation-pressures/product-market-definitions. Accessed September 15, 2020.

Bhuiyan, R. (2012). Monetary transmission mechanisms in a small open economy:

a Bayesian structural VAR approach. Canadian Journal of Economics/Revue canadienne

d’économique, 45(3), 1037-1061.

Champagne, J., & Sekkel, R. (2018). Changes in monetary regimes and the

identification of monetary policy shocks: Narrative evidence from Canada. Journal

of Monetary Economics, 99, 72-87.

Cushman, D. O., & Zha, T. (1997). Identifying monetary policy in a small open

economy under flexible exchange rates. Journal of Monetary Economics, 39(3), 433-

448.

Cravino, J., Lan, T., & Levchenko, A. A. (2020). Price stickiness along the income

distribution and the e↵ects of monetary policy. Journal of Monetary Economics, 110,

3919-32.

Dickey, D. A., & Fuller, W. A. (1979). Distribution of the estimators for autoregressive

time series with a unit root. Journal of the American Statistical Association, 74(366a),

427-431.

Gini, C. (1921). Measurement of inequality of incomes. The Economic Journal,

31(121), 124-126.

Hannan, E. J., & Quinn, B. G. (1979). The determination of the order of an

autoregression. Journal of the Royal Statistical Society: Series B (Methodological),

41(2), 190-195.

Hodrick, R. J., & Prescott, E. C. (1997). Postwar US business cycles: an empirical

investigation. Journal of Money, Credit, and Banking, Vol. 29, 1-16.

Jordà, Ò. (2005). Estimation and inference of impulse responses by local projections.

American Economic Review, 95(1), 161-182.

Kim, S. (2019). Quality, price stickiness, and monetary policy. Journal of

Macroeconomics, 61, Article 103129.

Kronick, J. M., & Villarreal, F. G. (2019). Distributional Impacts of Low for

Long Interest Rates (No. 93483). University Library of Munich, Germany.

40Martel, S. (2008). A structural VAR approach to core inflation in Canada (No.

2008-10). Bank of Canada Discussion Paper.

Pagan, A. (1984). Econometric issues in the analysis of regressions with generated

regressors. International Economic Review, Vol. 25, 221-247.

Press, J. (2020, August). Bank of Canada eyes e↵ect on wealth, income distribution

in review, Carolyn Wilkins says. The Globe and Mail. Retrieved October 18, 2020,

from https://www.theglobeandmail.com/business/article-bank-of-canada-eyes-e↵ect-

on-wealth-income-distribution-in-review/

Raghavan, M., Athanasopoulos, G., Silvapulle, P. (2016). Canadian monetary

policy analysis using a structural VARMA model. Canadian Journal of Economics/Revue

canadienne d’économique, 49(1), 347-373.

Saez, E., & Zucman, G. (n.d.). Tax justice now. Retrieved March 16, 2021, from

https://taxjusticenow.org//

Statistics Canada (n.d.A). Table 18100004, Consumer Price Index, monthly, not

seasonally adjusted, Monthly (table). CANSIM (database). Last updated August

19, 2020. http://dc.chass.utoronto.ca.ezproxy.library.uvic.ca/cgi-bin/cansimdim/c2

arrays.pl. Accessed August 31, 2020

41Statistics Canada (n.d.B). Series V52673496, total, all commodities, Monthly

(table). CANSIM (database). Last updated August 14, 2020. http://dc.chass.

utoronto.ca.ezproxy.library.uvic.ca/cgi-bin/cansimdim/c2 seriesCart.pl. Accessed August

31, 2020

Statistics Canada (n.d.C). Series V122514, Overnight money market financing, 7-

day average (Percent), Monthly (table). CANSIM (database). Last updated August

28, 2020. http://dc.chass.utoronto.ca.ezproxy.library.uvic.ca/cgi-bin/cansimdim/c2

seriesCart.pl. Accessed August 31, 2020

Statistics Canada (n.d.D). Table 11-10-0008-01, Tax filers and dependants with

income by total income, sex and age. https://www150.statcan.gc.ca/t1/tbl1/en/cv.action?pid=1110000

Accessed March 16, 2021.

Statistics Canada. September (2019a). Survey of Household Spending: Public

Use Microdata File, 2017. Statistics Canada Catalogue no. 62M0004X2017001.

Ottawa, Ontario. https://www150.statcan.gc.ca/n1/en/catalogue/62M0004X2017001.

Accessed July 3, 2020

Statistics Canada (2019b). User guide for the Survey of Household Spending

public-use microdata file, 2017. Statistics Canada Catalogue no. 62M0004X2017001.

Ottawa, Ontario. https://www150.statcan.gc.ca/n1/en/catalogue/62M0004X2017001.

42Accessed July 3, 2020

Statistics Canada (2019c). Expenditure category hierarchy public-use microdata

file, 2017. Statistics Canada Catalogue no. 62M0004X2017001. Ottawa, Ontario.

https://www150.statcan.gc.ca/n1/en/catalogue/62M0004X2017001. Accessed July

3, 2020

U.S. Bureau of Economic Analysis (n.d), Real Gross Domestic Product [GDPC1],

retrieved from FRED, Federal Reserve Bank of St. Louis. https://fred.stlouisfed.

org/series/GDPC1. Accessed September 15, 2020.

43Appendix I: Tables and Figures

Table 1: A sample of items from each level in the Diary dataset

Level Diary Code - Expenditure Category Label

1 TC001 – Total current consumption

2 FD001 – Food expenditures

3 FD003 – Food purchased from stores

4 FD100 – Bakery products

5 FD101 – Bread and unsweetened rolls and buns

6 FD102 – Bread

44Table 2: Categories and labels between the Diary and CPI datset

Level Label in the Diary Series Label in the CPI Dataset

3 FD003 - Food purchased from stores Food purchased from stores

3 FD990 - Food purchased from restaurants Food purchased from restaurants

3 SH010 - Owned principal residence & SH040 - Other accommodation Owned accommodation

3 SH003 - Rented principal residence Rented accommodation

3 SH030 - Water, fuel and electricity for principal accommodation Water, fuel and electricity

3 CS001 - Communications Communications

3 CC001 - Child care Child care services

3 HO002 - Domestic and other custodial services (excluding childcare) Housekeeping services

3 HO014 - Paper, plastic and foil supplies Paper, plastic and aluminum foil supplies

2 HF001 - Household furnishings and equipment Household furnishings and equipment

3 HO010 - Household cleaning supplies and equipment Household cleaning products

3 CF001 - Women’s and girls’ wear (4 years and over) Women’s clothing

3 CM001 - Men’s and boys’ wear (4 years and over) Men’s clothing

3 CI001 - Children’s wear (under 4 years) Children’s clothing

45

3 CL007 - Clothing fabric, yarn, thread, and other notions & CL010 - Clothing services Clothing material, notions and services

4 TR003 - Private use vehicles Purchase and leasing of passenger vehicles

4 TR020 - Rented vehicles Rental of passenger vehicles

4 TR050 - Public transportation Public transportation

4 TR030 - Vehicle operations Operation of passenger vehicles

3 PC002 - Personal care products Personal care supplies and equipment

3 PC020 - Personal care services Personal care services

2 HC001 - Health care Health care

3 RE002 - Recreation equipment and related services Recreational equipment and services (excluding recreational vehicles)

3 RE040 - Home entertainment equipment and services Home entertainment equipment, parts and services

3 RE060 - Recreation services Recreational services

3 RV001 - Recreational vehicles and associated services Purchase and operation of recreational vehicles

2 ED002 - Education Education

3 TA005 - Alcoholic beverages Alcoholic beverages

3 TA002 - Tobacco products and smokers’ supplies Tobacco products and smokers’ supplies

Note: The column titled ”Level” refers to the expenditure level of the category in the Diary.Table 3: Income cuto↵s

Percentile Total Household Income (Canadian Dollars)

10 24275

45 67750

55 81500

90 170450

46Table 4: Correlogram of the residuals from regressing inflation against it shocks.

Number

Partial

of Autocorrelation Q-Statistic P-Value

Autocorrelation

Lags

1 -0.008 -0.008 0.0069 0.934

2 0.037 0.037 0.1636 0.921

3 0.032 0.033 0.2847 0.963

4 -0.097 -0.098 1.4091 0.843

5 0.062 0.059 1.8651 0.867

6 -0.044 -0.038 2.0998 0.910

7 0.102 0.106 3.3803 0.848

8 -0.279 -0.298 12.997 0.112

9 0.084 0.118 13.886 0.126

10 0.055 0.044 14.272 0.161

11 0.059 0.119 14.709 0.196

12 0.078 -0.031 15.487 0.216

13 -0.007 0.063 15.493 0.278

14 0.144 0.108 18.207 0.198

15 -0.015 0.061 18.237 0.250

16 -0.062 -0.211 18.754 0.282

17 0.078 0.162 19.577 0.296

18 0.010 0.033 19.590 0.356

19 -0.024 0.015 19.669 0.415

20 -0.015 -0.104 19.700 0.477

Note: The control variables for the regression are six lags of it and six lags of

inflation.

47Table 5: Correlogram of the residuals from regressing inflation against dlCt shocks.

Number

Partial

of Autocorrelation Q-Statistic P-Value

Autocorrelation

Lags

1 -0.034 -0.034 0.1400 0.708

2 -0.067 -0.069 0.6814 0.711

3 0.013 0.008 0.7012 0.873

4 -0.091 -0.095 1.6955 0.792

5 0.095 0.091 2.7962 0.731

6 -0.044 -0.053 3.0342 0.805

7 0.057 0.072 3.4407 0.841

8 -0.241 -0.265 10.760 0.216

9 0.051 0.084 11.092 0.269

10 -0.024 -0.104 11.169 0.345

11 -0.134 -0.087 13.485 0.263

12 -0.024 -0.124 13.558 0.330

13 -0.025 0.035 13.642 0.400

14 0.191 0.137 18.513 0.184

15 0.057 0.101 18.956 0.216

16 -0.047 -0.100 19.258 0.255

17 0.072 0.139 19.976 0.275

18 0.056 0.057 20.416 0.310

19 0.039 0.011 20.634 0.357

20 -0.011 -0.064 20.653 0.418

Note: The control variables for the regression are two lags of dlCt and six lags of

inflation.

48Table 6: Weights of each category in each income-specific CPI

Label in the Diary ⇡tB ⇡tM ⇡tT

FD003 - Food purchased from stores 12.41 11.36 8.93

FD990 - Food purchased from restaurants 3.46 4.24 4.72

SH010 - Owned principal residence & SH040 - Other accommodation 11.11 19.72 22.58

SH003 - Rented principal residence 18.19 5.77 1.45

SH030 - Water, fuel and electricity for principal accommodation 5.49 5.10 4.18

CS001 - Communications 5.06 4.52 3.40

CC001 - Child care 0.26 0.65 1.78

HO002 - Domestic and other custodial services (excluding child care) 0.16 0.17 0.52

HO014 - Paper, plastic and foil supplies 0.76 0.66 0.48

HF001 - Household furnishings and equipment 3.40 3.93 4.26

HO010 - Household cleaning supplies and equipment 0.46 0.40 0.30

CF001 - Women’s and girls’ wear (4 years and over) 2.03 2.65 3.10

CM001 - Men’s and boys’ wear (4 years and over) 1.42 1.58 2.08

CI001 - Children’s wear (under 4 years) 0.11 0.18 0.10

CL007 - Clothing fabric, yarn, thread, and other notions & CL010 - Clothing services 0.23 0.18 0.18

TR003 - Private use vehicles 8.24 8.67 9.76

TR020 - Rented vehicles 0.13 0.07 0.27

TR050 - Public transportation 1.78 1.78 3.03

TR030 - Vehicle operations 8.93 10.50 8.71

PC002 - Personal care products 0.85 1.24 1.30

PC020 - Personal care services 0.79 0.97 1.09

HC001 - Health care 4.45 5.27 3.39

RE002 - Recreation equipment and related services 1.01 1.63 1.95

RE040 - Home entertainment equipment and services 0.40 0.32 0.41

RE060 - Recreation services 3.01 3.12 4.91

RV001 - Recreational vehicles and associated services 0.52 0.91 2.20

ED002 - Education 2.73 1.57 2.31

TA005 - Alcoholic beverages 1.42 1.01 0.47

TA002 - Tobacco products and smokers’ supplies 1.17 1.83 2.16

Note: The weights are multiplied by 100.

49Figure 1: Time-series plot of the Overnight Rate

50Figure 2A: Time-series plot of the All-Commodities Price Index.

51Figure 2B: Time-series plot of the US Output Gap.

52Figure 2C: Time-series plot of the Canadian Output Gap.

53Figure 2D: Time-series plot of the Canadian Inflation Rate.

54Figure 2E: Time-series plot of Overnight Interest Rate in First-Di↵erences.

55Appendix II: Other results of the SVAR IRFs

In this section the rest of the IRFs estimated in Section 4.1 is presented. All

IRFs in this section includes a 65% confidence interval, denoted by the shaded grey

area in each of the figures.

Figure 1: The IRF of the Overnight Rate to shocks in the Overnight Rate

Note: The impulse is a one-standard deviation shock to the overnight rate. The gray

area represents a 65% confidence interval.

56Figure 2: The IRFs of the Canadian variables to shocks in Inflation

Note: The impulse is a one standard deviation shock to the Inflation. The gray area

represents a 65% confidence interval.

57Figure 3: The IRFs of the Canadian variables to shocks in the Canadian Output

Gap

Note: The impulse is a one standard deviation shock to the Canadian Output Gap.

The gray area represents a 65% confidence interval.

58Figure 4: The IRF of the US Output Gap to shocks in the US Output Gap

Note: The impulse is a one standard deviation shock to the US Output Gap. The

gray area represents a 65% confidence interval.

59Figure 5A: The Impact of US Output Gap Shocks

Note: The impulse is a one standard deviation shock to the US Output Gap. The

gray area represents a 65% confidence interval.

60Figure 5B: The Impact of US Output Gap Shocks

Note: The impulse is a one standard deviation shock to the US Output Gap. The

gray area represents a 65% confidence interval.

61You can also read