THE DAILY BRIEF MARKETUPDATE MONDAY,28JUNE2021 GLOBAL MARKETS - CAPRICORN ASSET MANAGEMENT

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Daily Brief Market Update Monday, 28 June 2021 Global Markets Asian shares started the week in a cautious mood on Monday, as a spike in coronavirus cases across the region over the weekend hurt investor sentiment while oil hovered around 2-1/2 year highs. MSCI's broadest index of Asia-Pacific shares outside Japan was last a shade weaker at 702.57. Japan's Nikkei slipped 0.2%, with South Korea's benchmark KOSPI down about the same amount. Investors were concerned about a spike in coronavirus infections in Asia, with Australia's most populous city of Sydney plunging into a lockdown after a cluster of cases involving the highly contagious Delta strain ballooned. Indonesia is battling record high cases while a lockdown in Malaysia is set to be extended. Thailand too announced new restrictions in Bangkok and other provinces. Chinese shares were a touch higher with the CSI300 index up 0.2%. Data over the weekend showed profit growth at China's industrial firms slowed again in May as surging raw material prices squeezed margins and weighed on factory activity. Investors will keep a close eye on an official survey of Chinese factory activity due Wednesday. The manufacturing reading is expected to slow to 50.8 from 51. The private sector Caixin Manufacturing PMI will follow later in the week.

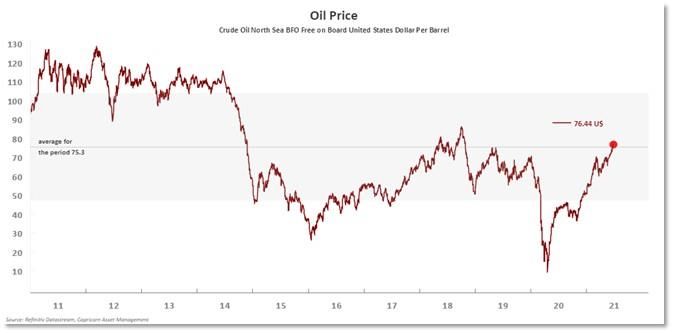

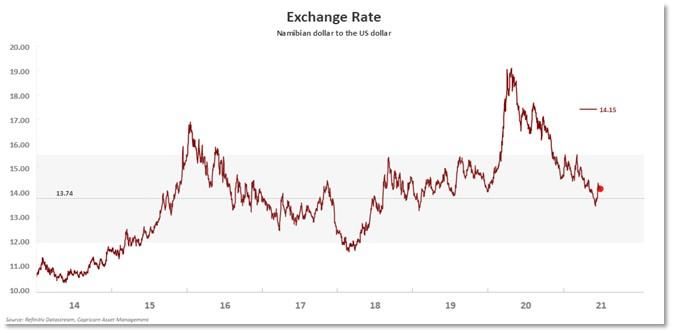

Futures pointed to a cautious open for share markets in Europe as well. Pan-region Euro Stoxx 50 futures slipped 0.05%, while FTSE futures edged 0.01% higher. S&P 500 futures added 0.05%. Global shares weakened about 0.1% after reaching record highs last week as weaker-than- expected U.S. inflation and news of a bipartisan U.S. infrastructure agreement boosted risk appetite. The infrastructure plan is valued at $1.2 trillion over eight years, of which $579 billion is new spending. "Investors are keenly watching the progress of U.S. President Biden's bipartisan infrastructure deal through congress. The package could boost demand significantly, driven by investment in renewables and electronic vehicle (EV) infrastructure," ANZ analysts wrote in a note. Oil prices slipped slightly after earlier climbing to their highest since October 2018 on expectations demand growth will outstrip supply and OPEC+ will be cautious in returning more crude to the market from August. Brent futures lost 8 cents to $76.10 a barrel, while U.S. crude was flat at $74.05. On Friday, the S&P 500 rose 2.7% for the week, its strongest weekly gain since early February after data showed a measure of underlying inflation rose less than expected in May, easing fears of a sudden tapering in stimulus by the Federal Reserve. The Dow climbed 0.7% while the tech-heavy Nasdaq dropped 0.06% after holding near the previous session's record high. Later in the week, a closely-watched U.S. jobs report will be released for June which could point to strong labour demand. Yields for benchmark 10-year U.S. Treasuries, jumped back above 1.50% to close out a week in which rates notched their largest gains since March. Monetary and fiscal stimulus around the world in response to the COVID-19 pandemic is boosting financial assets, despite an uneven pace of recovery between regions. Boston Federal Reserve Bank President Eric Rosengren on Friday warned a build-up of financial stability risks linked to a low interest rate environment could lead to another downturn that interrupts the labour market recovery and impedes a return to maximum employment. In currencies, the U.S. dollar was slightly firmer at 91.856 against a basket of other currencies. The euro eased to $1.19225, while the Japanese yen strengthened to 110.625 versus the greenback. Domestic Markets The South African rand traded stronger on Friday as the dollar weakened on the back of uncertainty as to what direction the U.S. Federal Reserve would take on rate hikes.

A raft of mixed signals from the Fed in the last couple of weeks has made the rand jittery as investors

fear rising inflation numbers in the United States could force the Fed to clamp down on a loose

monetary policy in 2022 instead of 2023 as earlier expected.

At 1520 GMT, the local currency was trading at 14.108 rand against a dollar, 0.62% stronger from its

previous day's close.

In early June, the rand had reached a 28-month high, making it the best performing emerging

market currencies on hopes that a dovish Fed would keep the flow of dollars into riskier

markets. Since then it has lost over 5% as investors continue to brace against uncertainty. But they

are hoping it is a transitory period.

"While the U.S. Federal Reserve (Fed) tapering and other central bank news may slow down the U.S.

dollar's devaluation, it seems to us that, for now, the dollar's weakening trend will continue," said

Nolan Wapenaar, co-chief investment officer of Anchor Capital.

Out of every $100 currently circulating in the United States, around. $25 was printed at some point

in the past 18 months, Wapenaar said and this would maintain a steady pressure on the greenback,

keeping the money flow into emerging markets in the short term.

"We think that the local currency's strengthening momentum might persist for just a little while

longer," he said, adding that the brokerage house's long term view was that the fair value for the

rand remains in the 14.5-rand-to-15-rand-per-dollar range.

Shares on the Johannesburg Stock Exchange (JSE) slipped a tad on Friday but the overall

performance was a mixed bag as investors continued to ponder inflation trajectory and a possible

Fed rate hike. Inflation eats into the future value of stock investments and higher interest rates

increase the cost of capital for companies to fund growth.

The benchmark all-share index closed down 0.07% at 66,215 points while the blue-chip index of top

40 companies ended down 0.08% at 60,140 points. In fixed income, the yield on the benchmark

2030 instrument was up 0.1%.

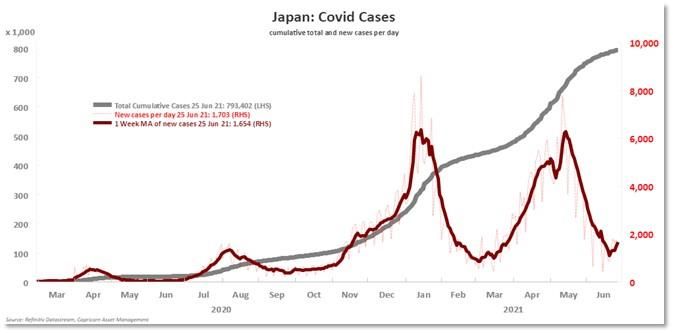

Corona Tracker

The number of new cases is distorted by cut-off times.

Source: Thomson Reuters

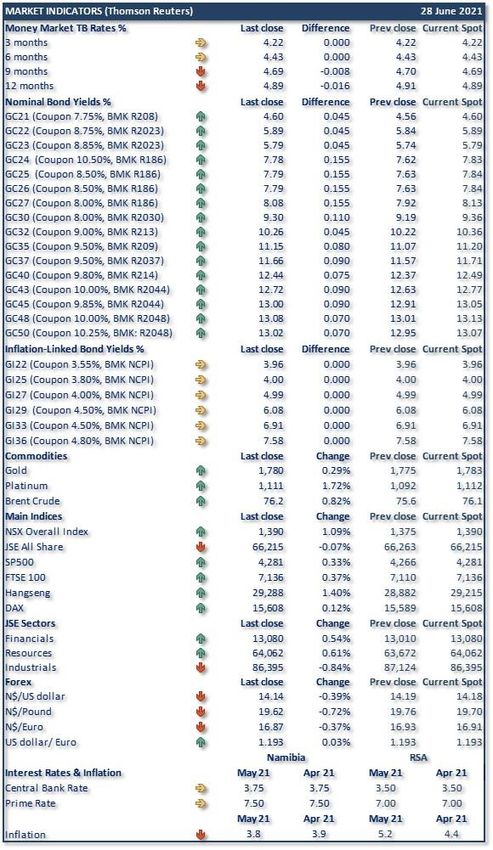

Market Overview

Notes to the table:

• The money market rates are TB rates

• “BMK” = Benchmark

• “NCPI” = Namibian inflation rate

• “Difference” = change in basis points

• Current spot = value at the time of writing

• NSX is a Bloomberg calculated Index

Important Note:

This is not a solicitation to trade and CAM will not necessarily trade at the yields and/or prices

quoted above. The information is sourced from the data vendor as indicated. The levels of and

changes in the yields need to be interpreted with caution due to the illiquid nature of the domestic

bond market.

Source: Thomson Reuters

For enquiries concerning the Daily Brief please contact us at

Daily.Brief@capricorn.com.na

Disclaimer

The information contained in this note is the property of Capricorn Asset Management (CAM). The

information contained herein has been obtained from sources which and persons whom the writer

believe to be reliable but is not guaranteed for accuracy, completeness or otherwise. Opinions and

estimates constitute the writer’s judgement as of the date of this material and are subject to change

without notice. This note is provided for informational purposes only and may not be reproduced in

any way without the explicit permission of CAM.You can also read