THE DAILY BRIEF MARKETUPDATE TUESDAY,13JULY2021 GLOBAL MARKETS - CAPRICORN ASSET MANAGEMENT

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The Daily Brief Market Update Tuesday, 13 July 2021 Global Markets Asian shares climbed in early trade on Tuesday after Wall Street hit record highs overnight, as investors awaited the second-quarter earnings season and a batch of economic data, including key U.S. inflation figures later in the day. Investors are bracing for an eventful week which will include the start of the U.S. earnings season, inflation data from several countries and a testimony by Federal Reserve Chair Jerome Powell. The testimony will be scrutinised for any clues on the timing of potential U.S. tapering. MSCI's broadest index of Asia-Pacific shares outside Japan was up 0.5%, tracking a Wall Street rally overnight. The index is down 3.1% so far this month. Australian shares were up 0.49%, while Japan's Nikkei stock index rose 0.79%. China's blue-chip CSI300 index was down 0.1%, while Hong Kong's Hang Seng index rose 0.65%. Overnight, Wall Street's main indexes closed at their highest levels ever, lifted by Tesla and bank stocks. Tesla rallied over 4% and was the top contributor to gains in the S&P 500 and Nasdaq. CEO Elon Musk insisted in court on Monday he does not control Tesla, and he said he did not enjoy being the electric vehicle company's chief executive as he took the stand to defend the company's 2016 acquisition of SolarCity.

The S&P 500 banks index climbed 1.3% ahead of quarterly earnings reports this week from major banks. JPMorgan Chase rose over 1% and Goldman Sachs rallied more than 2%, fuelling the Dow's gains. "Financials have been unloved for the best part of two months as yield curves have flattened and reflation bets unwound. With earnings season upon us and U.S. (10-year) yields now looking like they may have found a bottom, we could see some rotation back into banks," said ANZ analysts in a note. The next question is whether company earnings will support Wall Street's run higher. S&P 500 companies' earnings per share for the June quarter are expected to rise 66%%, according to IBES data from Refinitiv. JPMorgan, Goldman Sachs, Bank of America and other big banks kick off results from Tuesday. U.S. inflation data on Tuesday will also be in particular focus as investors try to gauge whether recent price pressures in the world's largest economy persist. Concerns that climbing cases of the Delta variant around the world could derail a global economic recovery have fuelled appetite for safe-haven U.S. Treasuries. The benchmark U.S. 10-year bond yield fell last week to a five-month low of 1.25%. While markets have since stabilised, yields are not far off 4-1/2 month lows at 1.3695%. In currency markets, the dollar index, which tracks the greenback against a basket of major currencies, was last down at 92.214, after touching a three-month top of 92.844 last week. U.S. crude ticked up 0.3% to $74.32 a barrel. Brent crude rose to $75.37 per barrel. Gold was slightly higher. Spot gold was traded at $1807.35 per ounce. Domestic Markets South Africa's rand tumbled more than 2% on Monday, battered by an outbreak of violence and looting after the jailing of former president Jacob Zuma. The government deployed soldiers on the streets to quell violence that has left at least six people dead and more than 200 arrested after Zuma was sentenced to 15 months in prison for contempt of court during an investigation into high-level corruption. The rand slipped as much as 2.2% to 14.5025 against the dollar, close to a two-month weak point it touched in early July. It traded at 14.4175 at 1500 GMT - down 1.51% on the day.

"The outbreak of violence due to the jailing of ex-president Jacob Zuma is weighing on the rand as

investors might fear an escalation," said Elisabeth Andreae, emerging market analyst at

Commerzbank. "Today's hearing of Zuma's application at the Constitutional Court to get the

sentence reviewed might bring further escalation," she added, referring to a session of the country's

top court to rule on a challenge by Zuma against his prison term, which began on Monday.

Compounding pressure on the rand was a fall in copper prices amid concerns over slowing growth in

China as well as fears that extended, tight COVID-19 restrictions might hit the fragile recovery in

Africa's most industrialised economy. The rand has outperformed many other emerging market

currencies since the start of the year, but Monday's tumble reduced its gains since the start of the

year to 1.4%.

Other assets were broadly unfazed. Yields on local 10-year government bonds nudged a touch

higher at 8.89%, while the benchmark equity index gained 1.43%. The All-share index climbed 1.37%.

"This (violence and looting) is very short term as far as the markets are concerned. This isn't going to

continue for weeks and months, we're probably over the worst already," said Wayne McCurrie,

portfolio manager at FNB Wealth and Investments.

Hotel and casino owner Sun International topped the gainers, jumping 8.11%, while peer Tsogo Sun

Hotels rose 3.28% and owner of fast food chains Famous Brands gained 5.79% after President Cyril

Ramaphosa announced on Sunday that restaurants will be allowed to open again.

The decision to jail Zuma resulted from legal proceedings seen as a test of post-apartheid South

Africa's ability to enforce the rule of law, including against powerful politicians. The unrest had

initially been concentrated mainly in Zuma's home province of KwaZulu-Natal (KZN) but over the

weekend protests spread to the largest city Johannesburg. The incarceration of Zuma has angered

his supporters and exposed rifts within the ruling African National Congress. Ramaphosa said on

Sunday there was no justification for violence and that it was damaging efforts to rebuild the

economy amid the pandemic.

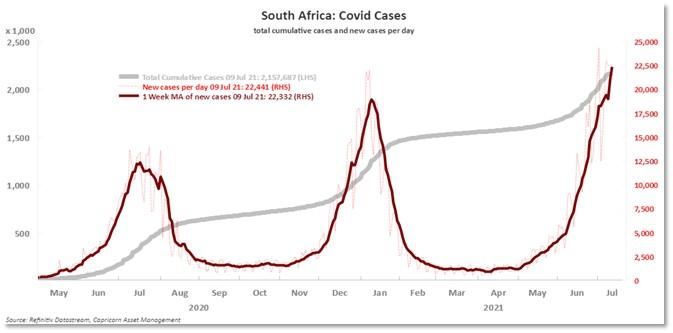

Corona Tracker

The number of new cases is distorted by cut-off times.

Source: Thomson Reuters

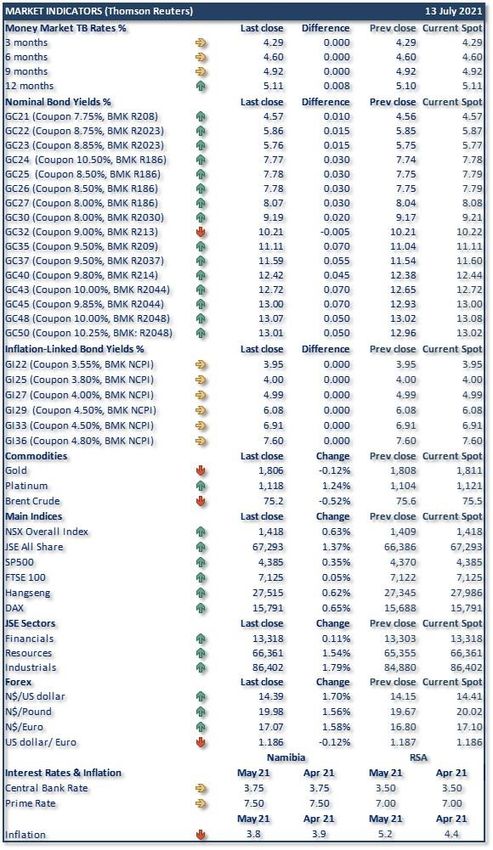

Market Overview

Notes to the table:

• The money market rates are TB rates

• “BMK” = Benchmark

• “NCPI” = Namibian inflation rate

• “Difference” = change in basis points

• Current spot = value at the time of writing

• NSX is a Bloomberg calculated Index

Important Note:

This is not a solicitation to trade and CAM will not necessarily trade at the yields and/or prices

quoted above. The information is sourced from the data vendor as indicated. The levels of and

changes in the yields need to be interpreted with caution due to the illiquid nature of the domestic

bond market.

Source: Thomson Reuters

For enquiries concerning the Daily Brief please contact us at

Daily.Brief@capricorn.com.na

Disclaimer

The information contained in this note is the property of Capricorn Asset Management (CAM). The

information contained herein has been obtained from sources which and persons whom the writer

believe to be reliable but is not guaranteed for accuracy, completeness or otherwise. Opinions and

estimates constitute the writer’s judgement as of the date of this material and are subject to change

without notice. This note is provided for informational purposes only and may not be reproduced in

any way without the explicit permission of CAM.You can also read