Rethinking retirement: The impact of demographic change and the pandemic on retirement planning in the 2020s - February 2021 - ASFA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Rethinking retirement: The impact of demographic change and the pandemic on retirement planning in the 2020s February 2021

Contents

1. Introduction 3

2. The demographics of ageing 4

3. The rise of older workers 6

4. Accommodating retirees and the frail elderly 9

5. Impact of the baby bust 12

6. Outlook for retiree personas 15

7. Summary points 17

Introduction

1

This report has been prepared as part of a broader contribution by The

Demographics Group to the ASFA Conference 2021. (See also “Personas”

presentation.)

The coming of COVID-19 has coincided with a number expectancy, the rise of a super retirement class (that

of demographic and cultural changes in Australia is, retiree Baby Boomers), the societal impact of the

prompting the question of what retirement might look baby bust, changes in the way the retirement years

like later in the decade. The 2020s was always going are perceived (for example, more people choosing to

to be a period of transition as Baby Boomers retreated work), trends in accommodation for the elderly, for

from the workforce placing pressure on resources. retirees, for active seniors as well as a review of the

(occasionally outrageous) lifestyle expectations of the

However, the pandemic has pressed the reset button – next generation of retirees.

not just with regard to the retirement plans for many,

but also in the way Australians work, in the kind of There is also a chapter on various retirement

businesses that prosper, and even in matters like trade ‘personas’ developed to showcase the lifestyles of

and alliance relationships. those in retirement or planning for their retirement in

the 2020s and beyond.

It also appears that the pandemic has accelerated

the widespread acceptance of digital transformation. The report concludes with a summary of main points

Indeed, it is fair to say that the retiree of the future and observations.

will be more technologically proficient in matters like

customer interactions.

The balance of this report looks at the change in life

3 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020S

The demographics of ageing

2

There is no great revelation about the ageing of modern Australia. It is a

demographic process that has been underway for more than a century.

Improved public health and medical support have extended the life cycle and

especially in the developed world. In 1940 the life expectancy of the average

Australian was 63 years: a bit more for women and a bit less for men.

Eighty years later and life expectancy has extended to More significant, however, is the fact in 1980 the

an average of 83 years. The grandparents of today’s 1.4 million Australians aged 65+ were supported

Millennial generation got 20 fewer years of life, on (indirectly via work and taxation) by 9.6 million people

average. The issue is that the extra years gifted to the aged 15-64. In broad terms this converts to a ratio of

lifecycle for today’s Australians aren’t added to youth almost seven ‘workers’ per ‘retiree’.

or even to middle age. No, the extra years of life are

added to the end of life creating, for the first time in Today the number of workers per retiree is closer to

history, an extensive retiree class. four and by 2040 it will be three. And the reason

is that Australians are living longer, the retirement

Australians have had access to an Age Pension for cohort is surging because Baby Boomers (born 1946-

more than a century. But when it was introduced (in 1964) are retiring. Indeed the first Baby Boomer

1911) access was set at age 65 for men and at age 60 turned 65 in 2011 as an initial step towards a so-

for women. Men typically died before getting access to called baby bust of the 2020s (see Section 5).

a retirement pension. And in many respects this was a

sensible arrangement given the modest pre-income-tax The use of terms like Baby Boomer, Generation X,

tax-base of the Australian economy. Millennial and others is somewhat controversial in

that it is illogical to ascribe common behaviours to

Fast forward to 2021 and Australians aged 65+ a cohort based solely on birthyear. However, the

comprise 4.2 million or 16 per cent of the national reason why “generations” is such a popular term

population. Just over 40 years ago in 1980 the number is that many in business (and the media) find these

of people aged 65+ (and largely eligible for an Age “handles” convenient ways of referring to different

Pension) was 1.4 million or barely 10 per cent of the markets defined by age or life stage.

population (see graphic 1).

Graphic 1: Increasing the burden: Australian population by life stage 1980-2040

Year 0-14 15-64 65+

1980 3,710,994 9,571,085 1,413,277

2000 3,943,342 12,721,200 2,364,260

2020 4,880,412 16,847,793 4,145,275

2040 6,070,021 21,186,984 6,346,371

Data source: ABS Population Estimates and Projections

4 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020S

The demographics of ageing

Plus, there is an element of truth to so-called Retirement in the 2020s for example will be shaped

generational traits in that consumer behaviour that by the coming of COVID-19, by the surge in Baby

is often learnt by common experience with, say, the Boomer numbers, by the pressures effected by the

Great Depression or with post-war austerity. The baby bust (that is, more workers leaving than entering

parents of Baby Boomers, for example, were necessarily the workforce) and perhaps by the rapid uptake in

frugal. When they retired in the 1980s many in this technology.

generation adapted to their straitened circumstances.

Retirement in the 2030s on the other hand will be

The opposite is sometimes said to apply to the shaped by an easing of demographic pressures,

Millennial generation (1984-1998) who matured perhaps by the diversion of public spending towards,

to adulthood in small, dual-income, families during say, defence, as opposed to, say, retiree support.

Australia’s long boom (1992-2020).

Retirement in the 2040s might be redefined entirely

The Baby Boomers first breached the retirement cohort as life expectancy by that time pushes well into the

during the 2010s and will come to dominate this later 90s.

stage of the lifecycle during the 2020s.

Generation-X (1965-1983) will trip across the 65-line

in 2030 and eventually this generation will come to

dominate the retirement cohorts during the 2030s and

2040s. (Note that there isn’t consensus agreement

on the precise years that relate to each generation;

definitions can vary by a few years.)

The issue is that the very foundations of the retirement

industry, accommodation, funding (including

superannuation) and consumer behaviour are set in

place by the values and the demographic weight of the

preceding generation. At any point in time it is up to

the newcomers, to the new retirement class, to impose

their values, to leverage their demographic and cultural

influence to create a new version of the retirement

lifestyle.

5 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020S

The rise of older workers

3

One of the responses to the ageing population has been the rise of older

workers.

The idea of retiring with a pension at the age of 65 tertiary education, present to the post-65 stage of the

was regarded as a goal, as a reward for working hard, lifecycle from 2020 onwards.

by the generations that preceded the Baby Boomers

(that is, collectively ‘pre-boomers’). And especially The concept of retirement in the 2020s will be

for workers working in an economy dominated by shaped, in part at least, by a surge in university

manufacturing and agriculture: the bodies of working educated retirees and/or workers, the so-called Work-

men and women simply ‘wore out’ by their early 60s. on Baby Boomers. (I am tempted to extend this to

Working-on wasn’t an option. “Work-on Baby Boomers Looking for Extra Savings”

purely in order to create the acronym WOBBLES, but

But with the transition of the Australian economy maybe that’s a step too far.)

to skilled knowledge work a new kind of worker

emerged: the office worker or, more recently, the The number of Australians aged 65+ still in the

knowledge worker. The Baby Boomer generation was workforce in November 2020 was 616,000 or 4.8 per

the first cohort of Australians to have had wide access cent of the entire workforce. This number comprised

to a university education (literally from 1972 onwards). more men (369,000) than women (247,000).

Some 40 years earlier, in November 1980, the 65+

The back-half of the boomers (that is, those born 1954- workforce numbered 90,000 including 69,000 men

1964), including those who had access to fee-free (see graphic 2).

Graphic 2: Pandemic reshapes workforce: employment by age group February-November 2020

Male Female Total Change Feb-20 to Nov-20 Change Feb-20 to Nov-20 (%)

Age group

Feb-20 Nov-20 Feb-20 Nov-20 Feb-20 Nov-20 Male Female Total Male Female Total

15-19 326,644 313,497 348,658 340,213 675,301 653,710 -13,146 -8,445 -21,591 -4.0% -2.4% -3.2%

years

20-24 651,280 617,874 623,582 568,427 1,274,862 1,186,302 -33,406 -55,155 -88,560 -5.1% -8.8% -6.9%

years

25-29 795,545 805,718 739,283 701,705 1,534,828 1,507,423 10,173 -37,578 -27,405 1.3% -5.1% -1.8%

years

30-34 839,769 809,079 733,972 718,716 1,573,741 1,527,796 -30,690 -15,255 -45,945 -3.7% -2.1% -2.9%

years

35-39 811,171 808,552 685,527 708,229 1,496,697 1,516,782 -2,619 22,703 20,084 -0.3% 3.3% 1.3%

years

40-44 704,208 715,667 622,768 625,878 1,326,975 1,341,545 11,460 3,110 14,569 1.6% 0.5% 1.1%

years

45-49 721,504 709,363 671,357 657,026 1,392,861 1,366,389 -12,142 - 14,331 -26,473 -1.7% -2.1% -1.9%

years

50-54 647,295 645,798 603,116 612,643 1,250,411 1,258,441 -1,497 9,526 8,029 -0.2% 1.6% 0.6%

years

55-59 585,734 581,503 542,609 538,422 1,128,343 1,119,925 -4,231 - 4,187 -8,417 -0.7% -0.8% -0.7%

years

60-64 436,875 438,122 358,891 376,740 795,766 814,862 1,247 17,849 19,097 0.3% 5.0% 2.4%

years

65 years 354,749 368,618 243,694 247,256 598,443 615,873 13,869 3,562 17,431 3.9% 1.5% 2.9%

and over

Total 6,874,773 6,813,792 6,173,456 6,095,256 13,048,229 12,909,048 -60,981 -78,200 -139,181 -0.9% -1.3% -1.1%

Data source: ABS Labour Force

6 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020S

The rise of older workers

The rising contribution to the workforce made by remaining in, or returning to, the workforce (see

those who, theoretically, “could retire” seems to have again graphic 2).

reached an (upward) inflection point around 2006 (see

graphic 3). Job losses over the eight months to November applied

to all cohorts under the age of 35. Indeed, there was

And women do indeed seem to be closing the a net loss of 89,000 jobs alone in the 20-24 cohort

‘workforce participation gap’ in the 65-and-over and a further net loss of 46,000 in the 30-34 cohort

cohort. In November 1986 female workers aged 65+ between February and November. The pandemic has

comprised 0.8 per cent of the national workforce as taken the jobs of the young and appears to have

compared with 1.7 per cent for men. However by encouraged older workers to remain in the workforce.

November 2020, older female workers accounted for

4.1 per cent of the workforce as compared with 5.4 This raises the question of the kind of jobs that

per cent for men. support older workers. The Australian Bureau of

Statistics provides estimates of the number of workers

The impact of COVID-19 on workforce participation by gender and age at quarterly intervals. The top

has been patchy although most job losses have applied ten jobs held by male and female workers aged

to the young and especially to young women. Between 65+ in November 2020 show that men and women

February and November 2020 (covering the first eight dominate roughly half these ‘big occupations’ and

months of the pandemic), there was an increase in that the other half is shared (see graphic 4).

the number of older Australians (regardless of gender)

Graphic 3: Inflection towards older workers: percentage total workforce aged 65+ by gender,

November 1978-November 2020

Data source: ABS Labour Force

7 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SThe rise of older workers

Older male workers for example dominate the Older women seem to find work in clerical and

occupations of Road and Rail Drivers (26,491 caring roles whereas older men find work in farming,

jobs), Design, Engineering, Science and Transport construction and management.

Professionals (14,180) and Other Labourers (13,649).

It seems logical that as more tertiary-educated Baby

Older women on the other hand dominate the Boomers reach the so-called retirement age of 65

occupations of Numerical Clerks (21,652 jobs), General later in the 2020s, there will be greater workforce

Clerical Workers (18,172) and Carers and Aides participation by this expansive age group. Indeed the

(12,915). Work-on Baby Boomer is likely to gather momentum

within the workforce and culturally in post-pandemic

Jobs that support older workers of both genders Australia.

include Farmers and Farm Managers (40,297 males,

16,750 females), Educational Professionals (22,071

females, 10,657 males) and Business, Human Resources

and Marketing Professionals (20,640 males, 10,701

females).

Graphic 4: Jobs for older workers: top 10 occupations (4-digit) for males and females, November 2020

65+, Male 65+, Female

Total persons Total persons

Rank Occupation Rank Occupation

employed employed

1 Farmers and Farm Managers 40,297 1 Education Professionals 22,071

2 Specialist Managers 29,446 2 Numerical Clerks 21,652

3 Road and Rail Drivers 26,491 3 General Clerical Workers 18,172

Business, Human Resource and

4 20,640 4 Farmers and Farm Managers 16,750

Marketing Professionals

Hospitality, Retail and Service

5 17,473 5 Health Professionals 15,642

Managers

Design, Engineering, Science and

6 14,180 6 Carers and Aides 12,915

Transport Professionals

Hospitality, Retail and Service

7 Health Professionals 13,681 7 12,299

Managers

Business, Human Resource and

8 Other Labourers 13,649 8 10,701

Marketing Professionals

Automotive and Engineering Trades

9 13,366 9 Sales Assistants and Salespersons 10,025

Workers

10 Sales Representatives and Agents 13,238 10 Inquiry Clerks and Receptionists 9,991

Data source: ABS Labour Force

8 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SAccommodating retirees and the frail

4 elderly

The number of Australians aged 65+ in 2021 is estimated to be 4.3 million, up

from 2.4 million at the turn of the 21st Century. This number has increased at

roughly 100,000 per year for the last decade (see graphic 5a).

The vast majority of this growth is shaped by cohort • 57,000 live in accommodation for the aged that

progression. In fact, in any single year over the age of is not self-contained which means that residents

65 the number of immigrants (mostly family reunion) share some facilities such as common living and

contributes less than one per cent to that cohort eating areas. This kind of facility accommodates 2

population (see graphic 5b). per cent of the 65+ population and appears to be

growing at a rate of 10,000 per year.

In other words, the demand for retiree accommodation

in any decade isn’t significantly affected by the rise or

fall in immigration in that year or even in that decade. The census suggests that just over one million

The impact of such change is more likely to be felt over (that is 1.009 million) Australians, or 27 per cent

the course of a generation. of all Australians aged 65+ at this time, lived in

some form of defined retirement accommodation.

The coming of COVID-19 may well negatively impact The vast majority lived in assisted living (640,000)

the demand for (young people’s) housing (that is, accommodation (requiring assistance with a core

fewer immigrants) in the 2020s, however within this activity), while a further 184,000 made the choice

timeframe it will only marginally impact demand for to live in self-contained accommodation within a

retirement accommodation. retirement village.

The 2016 Census shows the accommodation choices However, this still leaves 2.7 million or 73 per cent

made by older Australians (see graphic 6). Other who lived in private accommodation of some sort at

than private dwellings the most popular forms of this time.

accommodation for Australians aged 65+ at this time

were as follows: It may be said that up to the coming of COVID-19

three out of four Australians aged 65+ had chosen to

• 640,000 lived in assisted living accommodation remain in the family home or some kind of equivalent.

which equates to 17 per cent of the 65+ population.

However I suspect this reflects the young skew of 65+

This market appears to be growing at a rate of

population at the time of the last census. In 2016

20,000 per year based on intercensal calculations

Baby Boomers largely clustered in the 65-69 cohort

• 184,000 lived in a self-contained retirement village. and so were more likely to have been “in work” and

This equated to 5 per cent of the 65+ population. indeed “at home”, whereas progressively throughout

This market seems to be growing at a rate of about the 2020s as this cohort ages further into their 70s

10,000 per year other accommodation (and care) options are sure to

emerge.

• 128,000 live in nursing homes. This is about 4 per

cent of the 65+ population. There was very little

growth in the nursing home population between

the last two censuses. (Generally the modern

preference is for extended in-home care.)

9 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SAccommodating retirees and the frail elderly

Graphic 5(a): Predictable increases: annual growth in 65+ population 2000-2030

Year 65+ Annual change (#) Annual change (%)

2000 2,364,260 42,634 1.8%

2001 2,419,070 54,810 2.3%

2002 2,465,669 46,599 1.9%

2003 2,511,327 45,658 1.9%

2004 2,558,857 47,530 1.9%

2005 2,611,879 53,022 2.1%

2006 2,664,064 52,185 2.0%

2007 2,736,610 72,546 2.7%

2008 2,805,167 68,557 2.5%

2009 2,890,566 85,399 3.0%

2010 2,986,675 96,109 3.3%

2011 3,087,911 101,236 3.4%

2012 3,213,853 125,942 4.1%

2013 3,330,378 116,525 3.6%

2014 3,442,148 111,770 3.4%

2015 3,554,304 112,156 3.3%

2016 3,672,251 117,947 3.3%

2017 3,790,842 118,591 3.2%

2018 3,912,975 122,133 3.2%

2019 4,038,131 125,156 3.2%

2020 4,145,275 107,144 2.7%

2021 4,271,505 126,230 3.0%

2022 4,397,463 125,958 2.9%

2023 4,526,677 129,214 2.9%

2024 4,656,293 129,616 2.9%

2025 4,788,483 132,190 2.8%

2026 4,925,741 137,258 2.9%

2027 5,059,231 133,490 2.7%

2028 5,188,776 129,545 2.6%

2029 5,310,524 121,748 2.3%

2030 5,415,563 105,039 2.0%

Data source: ABS Population Estimates and Projections

10 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SAccommodating retirees and the frail elderly

Graphic 5(b): Recent older arrivals: Percentage population recent (last 12 months) immigrants by single

year of age over 65, 2016 Census

Data source: ABS Census, 2016

Graphic 6: Accommodating older Australians: 65+ population in retirement accommodation, 2011 & 2016

Accommodation Accommodation

Retirement Retirement

for the retired or for the retired or Nursing home Assisted living

Year 65+ population Nursing home Assisted living village (self- village (self-

aged (not self- aged (not self- (%) (%)

contained) contained) (%)

contained) contained) (%)

2011 3,012,281 46,763 1.6% 123,024 4.1% 537,281 17.8% 137,470 4.6%

2016 3,676,762 57,282 1.6% 127,896 3.5% 640,291 17.4% 184,236 5.0%

Change

664,481 10,519 0.0% 4,872 -0.6% 103,010 -0.4% 46,766 0.4%

2011-16

Data source: ABS Census, 2016

11 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SImpact of the baby bust

5

The baby bust of the 2020s will be one of the three biggest demographic

issues impacting Australia in 80 years. The other two were women ‘returning to

the workforce’ in the 1970s and the baby boom of the 1950s. A baby bust is

said to follow a baby boom by 70 years: it occurs when more workers exit the

workforce at age 65 than enter the workforce at age 15. Australia has been on

a baby bust trajectory for decades.

Indeed, demographers have been warning of a baby Net annual growth in the retirement (65+) population

bust for many years including Australian educated lifted from an average of 40,000 over the 40 years to

Canadian academic David K Foot who wrote a best- 2010 and rises to an average of 120,000 during the

selling book on the topic Boom, Bust & Echo (1996). early 2020s. Indeed, peak growth in the ‘retirement

The argument being that a post-war baby boom cohort’ is expected in 2026. The federal budget will

inevitably will lead to a baby bust in the 2020s. be stretched for another two election cycles before

pressure eases on the demand for retirement funding

The baby bust thesis is that the tax base of countries and services.

like Canada, the United States, Australia and others

expanded as a generation of Baby Boomers entered The problem is that the strong growth during the

the workforce in their early 20s (over 1966-1984) at a productive years (say, 1980-2020), when more

faster rate than 60-somethings exited the workforce. Baby Boomers poured into the productive taxpaying

stage of the lifecycle, is now being replaced by

The net effect of the baby boom was an increase in the weaker growth (say, 2020-2040) as boomers exit the

tax base in the late-20th and early-21st centuries as workforce and transition into their long retirement.

developed-world workforces swelled.

In simple terms the baby boom of the 1950s is being

The baby bust issue (in Australia at least) officially followed by a baby bust (and a pandemic) of the

starts from 2011 when the first Baby Boomer (born 2020s.

1946) turned 65. The so-called bust has continued as

boomers (born late 1940s) exited the workforce at a This demographic trajectory is partially offset

faster rate than Millennials (born mid-1980s to late- in Australia by a relatively high birth rate (for a

1990s) could enter the workforce in their early 20s. developed nation), by strong levels of overseas

immigration aimed at skilled youth, and by a program

As a consequence of the baby bust the rate of growth of importing guest workers.

in the workforce decelerates during the 2020s (see

graphic 7). The coming of COVID-19 is expected to block the

traditional avenues by which the effects of the baby

However, the baby bust in Australia was moderated bust are moderated.

by an uptick in international migration from the mid-

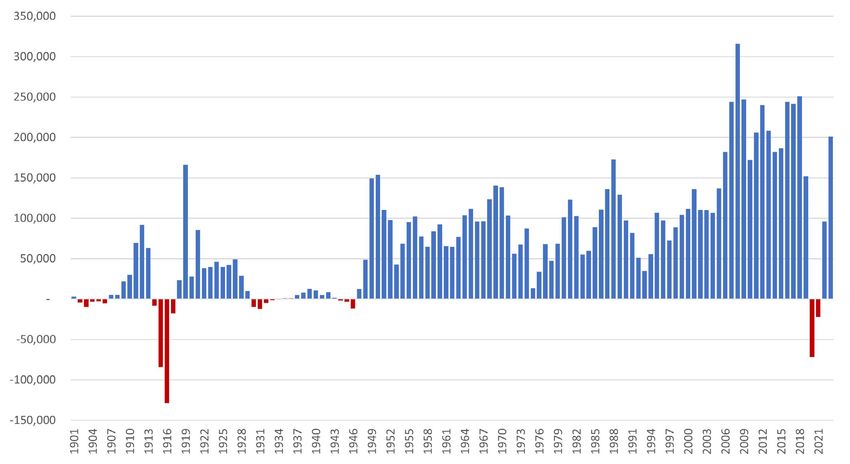

2000s onwards and which was largely focused on The great challenge for Australia, and for other

skilled migration and foreign student programs (see nations shaped by the post-war baby boom, is to

graphic 8). maintain service delivery to retirees including the Age

Pension and healthcare support despite a slowdown

Indeed, net annual growth in the working age (15-64) in workforce growth.

population had hovered around the 150,000-mark for

40 years prior to 2020, but over the following 40 years The alternative is to redefine community expectations

(based on pre-Covid projections) net annual growth in about the lifestyle that can be expected in retirement.

this cohort reduces to 100,000 or less (see graphic 9).

12 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SImpact of the baby bust

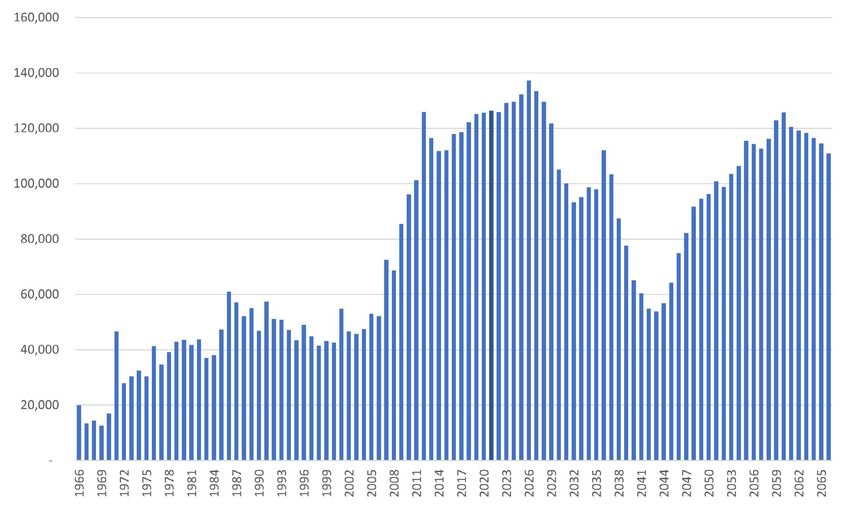

Graphic 7: Step change in workforce: net annual growth in Australian population 15-64, 1966-2066

Data source: ABS Historic, Estimated and Projected population

Graphic 8. The longest boom: net overseas immigration to Australia, 1901-2024

Data source: ABS; Australian Federal Budget 2020; The Demographics Group

13 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SImpact of the baby bust

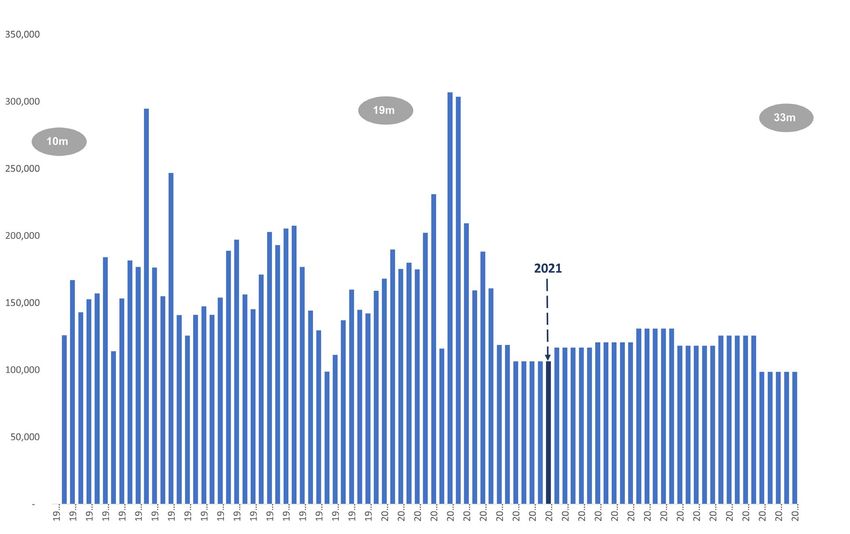

Graphic 9. Boomer’s retirement mountain: net annual change in Australian population 65+, 1966-2066

Data source: ABS Historic, Estimated and Projected population

14 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SOutlook for retiree personas

6

There are structural factors that shape planning for retirement including

the capacity of the nation to support a retirement cohort and community

expectations about the quality of life expected in retirement.

Add to this the effects of the pandemic (including always managed and they’ll “get by” in retirement

the drawdown on superannuation), the prospects with a bit of super and the pension.

of diminished immigration, the changing ethnicity • Meet first-wave Baby Boomers David & Linda both

and culture of Australian society, and the outlook for in their late 60s who sold their family home and

retirement can vary from different perspectives. business in Queensland’s Roma and “did a bit of

a seachange” by retiring to Brisbane’s Cleveland

We have developed five “personas” to consider

a few years ago. They shuttle between Cleveland

how retirement might be reimagined from different

and their kids interstate, visiting grandkids, and

perspectives in 2021 (see graphic 10). pursuing their hobbies and interests. They are

concerned that the value of their nest egg, and the

• Meet young professional couple Matt & Natasha,

quality of their retirement, could be whittled away

Millennials in their mid-30s currently renting in

by constant changes to benefits and concessions.

the inner suburbs of Sydney. They have one child

and would like another. They need a family home • Meet Franco & Maria, both in their early 70s living

not too far from their city workplaces. They have in the family home in Adelaide. Franco is a semi-

drawn down on their super balances and are retired accountant. Maria says he’ll never stop

looking to buy a family home. They argue they need working. Franco is determined that his kids and

a house now not superannuation later. They see grandkids will be left a legacy. He is concerned

“home ownership” as a more important part of that the rules around which he has developed his

achieving financial independence than investing in retirement plan could be changed. Franco wants

superannuation that may benefit their lifestyle in 30 everything to remain just as it is today.

years.

• Meet middle-aged Michelle a recently divorced The five personas must plan for retirement lifestyles

mother of two (aged 17 & 19) living in Melbourne’s that range from the here and now and 30 years into

Burwood. Michelle is a contractor with the Victorian the future.

Government and is concerned about job security

Those currently in retirement (David & Linda and

going forward. She still has a mortgage and

Franco & Maria) are concerned about sovereign

doesn’t feel she has enough in superannuation. The

risk, about the possibility of change to existing

pandemic has shaken her self-confidence; she is

arrangements.

concerned that if she loses her job she may not get

another job at the same level (she’s thinks the world

Michelle is fearful about the uncertainty of the future

has “moved on”); she wants reassurance about the

and about the demand for her skillset. The pandemic

quality of life that awaits her in retirement (in 2035).

has unsettled her sense of security.

• Meet Aussie battlers Justin & Jennifer both in

their mid-50s with three adult kids living nearby Like Michelle, Justin & Jennifer are also looking at

in Melbourne’s western suburbs. Justin works at a retirement next decade, but they have a much more

warehouse while Jennifer works at a supermarket. relaxed attitude towards the future. Maybe they’re

They still have a mortgage on their family home. too relaxed?

They want to retire at 65, which means 2030. They

have a modest super balance, but they also have a Young Matt & Natasha have relegated retirement

strong “she’ll be right” attitude. They say they have planning to a low priority in their lives.

15 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SOutlook for retiree personas

Graphic 10: Five personas rethinking retirement during 2021

Five personas showcase the super realities of Middle Australia

Matt (37) & Michelle (52) Justin (56) & David (69) & Franco (72) &

Natasha (33) Jennifer (55) Linda (66) Maria (70)

Both engineers by Divorced, two kids Their three adult kids Born in 1951 & 1954 Franco is a semi-

training (17 & 19) at home live nearby Sold their business retired accountant

Born 1983 & 1987 Contractor at VIC He works at a and sea-changed Maria was a

Retirement planned State Government warehouse, she at Retired from farming homemaker

for early 2050s Born 1968 the local supermarket a few years ago 2 adult children and 4

Likely retirement at Born 1964 & 1965 Bought a 3 BR house grandkids

Renting 2 BR 67 in 2035 Plan to retire as early in Cleveland Qld Norwood, Adelaide,

apartment in Surry as possible Adult kids live in SA

Hills NSW but are 3 BR house with Renters in 3 BR Brisbane, Melbourne Still live in the 4 BR

looking to buy a mortgage in Burwood house in Hoppers & Sydney family home

family home Covid has prompted Crossing David fishes, Linda Maria active in church

her to rethink her Proud first-time volunteers community

situation including grandparents

super arrangements Care for parents

She’s more engaged

in the process

Data source: The Demographics Group

16 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SSummary points

7

This report considers how retirement planning might be reimagined during the

2020s from the perspective of 2021 following the coming of COVID-19 and as

Baby Boomers press more fully into the retirement years. The main findings are

as follows:

1. Life expectancy rising: Life expectancy is extending 4. 84,000+ additional ‘older workers’ by 2030: The

the post work stage of the lifecycle otherwise proportion of the workforce comprised of workers

known as ‘retirement’. It is only in the post-war era aged 65+ was 4.8 per cent or 616,000 workers

that the Australian life expectancy has exceeded 65 in November 2020. The number of Australians

(the year at which men have been eligible for the aged 65+ will lift from 4.1 million in 2020 to 5.4

Age Pension since it was introduced in 1911). Prior million in 2030. It is possible if not likely that the

to WWII most Australians died in their early 60s. proportion of the workforce comprised by the 65+

Retirement planning let alone retirement funding cohort will lift over the coming decade to, say,

is an issue that has gathered momentum as the five per cent (if not more). This share of a 2030

Australian lifespan has expanded. workforce of, say, 14 million equates to 700,000

workers aged 65+ which is an extra 84,000 ‘older

workers’ than was the measured in November

2. Retiree population rising: The 2020s was always

2020.

going to be a period of intense pressure on

retirement funding due to the effects of the

so-called baby bust. The baby boom of the 5. More retirement accommodation required: The

1950s converts into a baby bust in the 2020s as 2016 census shows that 73 per cent of the

Baby Boomers exit the workforce. Without an population aged 65+ lives in some form of private

offsetting boost to births or a program of youthful accommodation. The remaining 27 per cent live in

immigration, the rate of growth in the tax base various forms of retirement housing or in assisted

subsides (with the baby bust) placing pressure care or assisted living arrangements. The most

on the national capacity to maintain retirement common non-private accommodation is assisted

concessions and support. The number of Australians living (17 percentage points) followed by those

aged 65+ will continue to rise every year to 2026 who live independently within a retirement village

before subsiding. (5 percentage points) and the remainder being

cared for in a nursing home (4 percentage points).

A 27-per-cent share of the 2020 population aged

3. Work-on Baby-Boomers rising: The coming of

65+ equates to 1.1 million; the same share applied

COVID-19 has increased the national debt, reduced

to the 2030 population aged 65+ equates to 1.5

the superannuation savings of many, threatened (if

million. During the 2020s underlying demographic

not eliminated) businesses in hospitality and tourism,

change can be expected to lift demand for

and changed many aspects of consumer behaviour

‘retirement accommodation’ (as defined in the

(such as greater focus on security; more comfortable

census) by an average of 40,000 residents per year.

with technology). The pandemic has also changed

the way we work and triggered a realignment of

trade arrangements and alliances. It has stopped

overseas immigration and has severely dented the

international education industry. It is likely that

skilled labour will be in even greater demand in the

2020s prompting many Baby Boomers to remain in

the workforce.

17 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SSummary points

6. Retirement planning must navigate priorities and 7. Forget the Fokkers, meet the WOBBLES: Finally,

risk: Consideration of how retirement planning this work has thrown up a new lifeform that is

might be reimagined during the 2020s from the sure to gather momentum during the 2020s: this

perspective of five “personas” shows a number of refers to the rise of the Work-on Baby Boomer

consistent themes. Those within retirement are likely Looking for Extra Savings otherwise known as

to be most concerned about retaining existing rules the WOBBLES. There are two factors driving the

and concessions. Those approaching retirement are WOBBLES: (a) the rise of tertiary-educated Baby

likely to be concerned about job security and having Boomers from the mid-1970s now pushing into

sufficient funds although others can be disengaged retirement and keen to boost super balances by

taking a “she’ll be right” approach. Young working on; and (b) the impact of COVID-19 in

Australians not looking to retire for three decades stymieing the inflow of skilled workers (including

or more could well question the rationale of the foreign students) from 2020 onwards leading to

entire superannuation system. Indeed, rethinking heightened demand for older knowledge workers

retirement in the 2020s very much depends on the to ‘work on’. The 2020s could well be the decade

vantage point of those doing the rethinking. of the WOBBLES.

18 | RETHINKING RETIREMENT: THE IMPACT OF DEMOGRAPHIC CHANGE AND THE PANDEMIC ON RETIREMENT PLANNING IN THE 2020SYou can also read