RBC Emerging Markets Equity Outlook 2021 - Themes, Sectors, Countries & Style

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

RBC Emerging Markets Equity Outlook 2021 Themes, Sectors, Countries & Style

RBC Emerging Markets Equity Outlook – 2021

Announcing the fifth annual RBC Emerging Markets Equity

Outlook 2021

This report explores the RBC Emerging Markets team’s 5.8%, before recovering by 3.9%. Consensus expectations

areas of research throughout the year and displays the are for China to grow in 2020 and to accelerate to 8.0%

team’s active engagement with companies and their growth in 2021 which is quite a dramatic recovery for an

analytical rigor. We hope you enjoy the team’s insights for economy so large. (Exhibit 1)

2021.

In terms of currency, we expect EM currencies to

The full report covers a vast scope of topics including appreciate against the U.S. dollar in 2021. EM currencies as

macro-economics, global policy response, portfolio a whole remain very cheap relative to the U.S. dollar, and

themes, ESG reforms, sector analysis, and style analysis, the three largest EM countries – China, Taiwan and South

with separate segments focusing on China, India, and Latin Korea – have positive current account balances and fiscal

America. deficits significantly lower than the U.S.

Below you will see the report highlights. For the full RBC The extraordinary market conditions in 2020 have made

Emerging Markets Equity Outlook 2021, which provides a our thematic, long-term approach more relevant than ever.

much more detailed analysis of the topics outlined below, Overall, most trends will likely revert to normal once the

please contact your local representative or reach us at: coronavirus pandemic has ended, however history has

rbcgamukmarketing@rbc.com shown that crises can leave enduring effects; we expect to

see some permanent shifts as a result of the current crisis.

At the beginning of 2020 there was an optimistic outlook for The most notable probable changes include: accelerated

the year’s global growth, however the COVID-19 pandemic technological adoption across a broad range of

changed everything. Strict lockdown restrictions and applications, de-globalisation driven by the re-localisation

business closures imposed by governments worldwide of supply chains, particularly within food production and

have caused the sharpest global economic downturn technology, and increased automation as a solution to the

seen in the last half a century. The government support costs and risks associated with local manufacturing and

packages in emerging economies have averaged 5% of manual labour.

GDP, compared with 30% of GDP in developed countries. In

terms of structure, there has been virtually no quantitative Sector analysis shows that Consumer sectors remain

easing in emerging nations, and only a fraction of the fiscal attractive as we look ahead to 2021 and we are selectively

spending seen in the developed world. positive on the Information Technology and Healthcare

sectors due to valuations. Over the last 12 months we have

The International Monetary Fund expects emerging seen an unprecedented level of divergence within sectors,

markets’ economic output to fall by 3.3% in 2020, then led by those that are benefitting from COVID-19. Technology

increase by 6.0% in 2021; this compares favourably to has been a key investment area with strong structural

developed markets, where output is expected to drop by tailwinds for some time now, however the effects of

Exhibit 1: Bloomberg Consensus GDP growth forecasts by EM country

Source: Bloomberg Consensus. Data as at 8 November, 2020.

2RBC Emerging Markets Equity Outlook – 2021

COVID-19 have further accelerated the migration towards The pandemic has had a severe impact on the Latin

digital services. American region and its equity markets in 2020 with

its two largest equity markets - Brazil and Mexico -

Style analysis indicates that the Growth style is outpacing underperforming EM equities by 43% and 24% respectively

Value by more than 30%, and is delivering the best (year-to-date as at 4 November 2020).2 Interestingly, both

outperformance ever, justified by much better earnings countries’ economic paths and fiscal responses to the

growth. Quality, in a risk-off environment, has also pandemic have been quite different: Mexico’s limited

outperformed but by a lesser margin. Small Cap stocks support package of 1.2% of GDP was the lowest in Latin

have been lagging but have started to perform better as America, whereas Brazil’s government stimulus at 12% of

the market rebounded from its March lows. As investors GDP was one of the highest. Mexico witnessed a significant

start to look ahead to 2021 there have been some signs reduction in economic activity followed by a mild recovery

that they are interested in quality Value names with a while Brazil witnessed a more contained decline in

good growth outlook in selected segments such as Banks, economic activity followed by a more rapid normalisation.

Autos or Industrials. However if the pandemic is not Looking ahead to 2021 there is continued concern over the

controlled, the global economic growth expected for 2021 economic outlook, fiscal risks and the uncertain political

would have to be downgraded and it is likely that a market backdrop.

sell-off would take place as currently a strong recovery is

priced in. In that risk-off environment, high Growth stocks China appears to have handled the coronavirus crisis

and those benefitting from COVID-19 would resume their successfully by marshalling early and aggressive

outperformance whilst Value and Small Cap stocks could lockdowns supported by a timely policy mix of tax cuts,

underperform. government spending stimulus and cheaper credit. After

suffering its worst quarterly drop in output since the 1960s

In terms of countries, this year’s report concentrates on from January through to March, the Chinese economy has

India, China, Mexico and Brazil. We expect India to remain started to recover without monetising debt. Looking into

the fastest-growing major EM economy, with growth driven 2021 and beyond, the key strategic focus of China’s current

by economic reforms and supportive demographics. ‘Five-Year Plan’ offers a glimpse of how the country will

Although there are still significant structural challenges, tackle two key challenges: declining potential growth and

the Indian economy is making progress under Prime a deteriorating external environment. More importantly,

Minister Mod and has managed to attract more foreign it also sets out the roadmap to become a high income

direct investment and has increased its manufacturing economy. With a broad objective of ‘sustained and sound

base through the government’s ‘Make in India’ initiative, economic growth’ in mind, the Chinese government has

launched in 2014, and the more recent ‘Production-Linked targeted self-sufficiency particularly in key technological

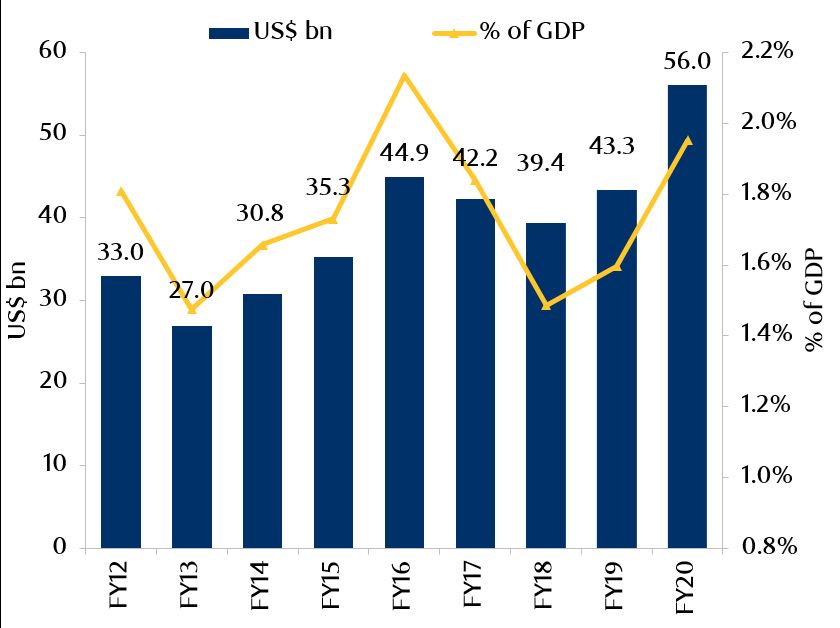

Incentive’ scheme for the electronics industry.1 (Exhibit 2) areas, innovation, domestic demand, environmental

protection, and new urbanisation.

Exhibit 2: India has been attracting FDI This year’s report also focuses on ESG reforms at a country

level with particular attention on China’s evolving climate

change policies, South Africa’s development in terms of

gender diversity, and India’s improvement in ‘ease of doing

business’. Reforms continue to be a key long-term driver

of growth and of differentiation among EM countries and

those that specifically relate to ESG and sustainability will

become increasingly important.

Source: CEIC, UBS. Data as at October, 2020.

1

CEIC, UBS. Data as at October, 2020. 2 Bloomberg. Data as at October, 2020.

3This document is provided by RBC Global Asset Management (RBC GAM) for informational purposes only and may not be reproduced, distributed or published without the written consent of RBC GAM or its affiliated entities listed herein. This document does not constitute an offer or a solicitation to buy or to sell any security, product or service in any jurisdiction. This document is not available for distribution to people in jurisdictions where such distribution would be prohibited. RBC GAM is the asset management division of Royal Bank of Canada (RBC) which includes RBC Global Asset Management Inc., RBC Global Asset Management (U.S.) Inc., RBC Global Asset Management (UK) Limited, RBC Global Asset Management (Asia) Limited, and BlueBay Asset Management LLP, which are separate, but affiliated subsidiaries of RBC. In Canada, this document is provided by RBC Global Asset Management Inc. (including PH&N Institutional) which is regulated by each provincial and territorial securities commission with which it is registered. In the United States, this document is provided by RBC Global Asset Management (U.S.) Inc., a federally registered investment adviser. In Europe this document is provided by RBC Global Asset Management (UK) Limited, which is authorised and regulated by the UK Financial Conduct Authority. In Asia, this document is provided by RBC Global Asset Management (Asia) Limited, which is registered with the Securities and Futures Commission (SFC) in Hong Kong. This document has not been reviewed by, and is not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the above-listed entities in their respective jurisdictions. Additional information about RBC GAM may be found at www.rbcgam.com. This document is not intended to provide legal, accounting, tax, investment, financial or other advice and such information should not be relied upon for providing such advice. RBC GAM takes reasonable steps to provide up-to-date, accurate and reliable information, and believes the information to be so when printed. RBC GAM reserves the right at any time and without notice to change, amend or cease publication of the information. Any investment and economic outlook information contained in this document has been compiled by RBC GAM from various sources. Information obtained from third parties is believed to be reliable, but no representation or warranty, express or implied, is made by RBC GAM, its affiliates or any other person as to its accuracy, completeness or correctness. RBC GAM and its affiliates assume no responsibility for any errors or omissions. Past performance is not indicative of future results. With all investments there is a risk of loss of all or a portion of the amount invested. Where return estimates are shown, these are provided for illustrative purposes only and should not be construed as a prediction of returns; actual returns may be higher or lower than those shown and may vary substantially, especially over shorter time periods. It is not possible to invest directly in an index. Some of the statements contained in this document may be considered forward-looking statements which provide current expectations or forecasts of future results or events. Forward-looking statements are not guarantees of future performance or events and involve risks and uncertainties. Do not place undue reliance on these statements because actual results or events may differ materially from those described in such forward-looking statements as a result of various factors. Before making any investment decisions, we encourage you to consider all relevant factors carefully. Publication date: June, 2020 ® / TM Trademark(s) of Royal Bank of Canada. Used under licence. © RBC Global Asset Management Inc., 2020 GUKM/20/381/FEB22/A

You can also read