Peter Cashin on the "earth shattering" PEA for Imperial Lake

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Peter Cashin on the “earth shattering” PEA for Imperial Mining’s Crater Lake Scandium-REE deposit In this InvestorIntel interview with host Tracy Weslosky during PDAC 2022, Imperial Mining Group Ltd. (TSXV: IPG | OTCQB: IMPNF) President and CEO Peter Cashin talks about the company’s recent PEA announcement, which confirms that its Crater Lake TG Zone Scandium-Rare Earth Element (Sc-REE) deposit has “the potential to be a long-term provider of critical Scandium and magnet Rare Earths to world markets.” In the interview, which can also be viewed in full on the InvestorIntel YouTube channel (click here), Peter discusses how with the new PEA “people will look at the financial metrics of this project, and they they stand up against any project that’s out there currently.” He talks about the results of the new PEA, which include a pre-tax net present value (NPV) of $2.97 billion with a pre-tax internal rate of return (IRR) of 42.9%, with annual net revenues averaging $608 million from the sale of high-purity scandium oxide (Sc2O3), scandium-aluminum Master alloy (ScAl) and rare earth element (REE) hydroxide concentrate, and a pre-tax capital payback of 2.5 years from the start of production. Peter also talks about the importance of scandium, used in defense, aerospace and automotive industries where strong, lightweight metals are required, and when added to other metals in small amounts it makes them heat and corrosion resistant. Its lightness makes it an attractive “green” metal reducing vehicle weight for lower fuel consumption. “What we’ll ultimately end up doing is significantly reducing the carbon footprint of most manufactured platforms they have

right now.” To access the full InvestorIntel interview, click here Don’t miss other InvestorIntel interviews. Subscribe to the InvestorIntel YouTube channel by clicking here. About Imperial Mining Group Ltd. Imperial is a Canadian mineral exploration and development company focused on the advancement of its technology metals projects in Québec. Imperial is publicly listed on the TSX Venture Exchange as “IPG” and on the OTCQB Exchange as “IMPNF” and is led by an experienced team of mineral exploration and development professionals with a strong track record of mineral deposit discovery in numerous metal commodities. To learn more about Imperial Mining Group Ltd., click here Disclaimer: Imperial Mining Group Ltd. is an advertorial member of InvestorIntel Corp. This interview, which was produced by InvestorIntel Corp., (IIC), does not contain, nor does it purport to contain, a summary of all the material information concerning the “Company” being interviewed. IIC offers no representations or warranties that any of the information contained in this interview is accurate or complete. This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the

Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Prospective investors are urged to review the Company’s profile on Sedar.com and to carry out independent investigations in order to determine their interest in investing in the Company. If you have any questions surrounding the content of this interview, please contact us at +1 416 792 8228 and/or email us direct at info@investorintel.com. InvestorIntel Week in Review for June 13-20, 2022 Ever imagine what the world would look like if you closed your eyes and then saw the world 2 years later? Last week’s PDAC 2022 was like opening a musty cupboard that has been closed too long. Likewise, it felt like a bad case of Back to the Future in that it was post-PDAC 2020 when the world shut down, I recall when we were all abuzz over who had spread COVID during that event. Tired, and out of shape, there was an occasional dramatic betterment, as both George A. Brown and George Bauk of PVW Resources Limited (ASX: PVW) could attest to. Both confessed to substantial life changes and had left good solid poundage

aside for exercise and nutrition. They both looked younger.

With our new Publisher and Editor in Chief Stephen Lautens

onside this year, along with Byron W King, and Clint Adam

Smyth on Stage 1, Level 700 for 3 days at the Metro Convention

Centre: we completed 7 panels and we should have all these

live by end of the week this week.

This morning? Jack Lifton has a story he is working on an

opinion on the “USD$120 million by the U.S. Department of

Defense to Australia’s Lynas Rare Earths Limited (ASX: LYC) to

cover the costs of constructing what is referred to as a

‘heavy rare earths’ processing (separation) plant in the USA.”

And I am tracking down the 3 companies that are referenced in

Byron W King’s most recent piece on his highlights from PDAC.

My favorite participants? I need one more week to drill

through all the business cards, and do my research, and then,

am happy to share some interesting facts that I surmised from

my time during this event… including the resounding theme of

Copper, Gold and — uranium! Plus, when did Jamaica start

advertising rare earths?

We have the benefit of news flow, analysts and journalists

communicating with us endlessly. Starting this week and moving

forward, let me send you some of the highlights I review,

including re-reviewing this week’s upcoming InvestorTalk.com

schedule, which includes:

InvestorTalk.com Schedule for June 21-23 (Click Here to RSVP):

Tuesday, June 21 from 9-920 AM EST – InvestorTalk.com

with Brent Willis from Voyageur Pharmaceuticals Ltd.

(TSXV: VM)

Wednesday, June 22 from 9-920 AM EST – Special Guest

Thursday, June 23 from 9-920 AM EST – InvestorTalk.com

with Terry Lynch from Power Nickel Inc. (TSXV: PNPN |

OTCQB: CMETF)

InvestorIntel Interview Highlights for the Week of June

13-20th, 2022:

June 20, 2022 – Hubert Lau talks about TrustBIX entering

a new growth phase with major agreements in place

https://bit.ly/3O6l3xN

June 17, 2022 – Byron W King says it is time for

investors to get back to “real things” like copper and

gold https://bit.ly/3xrXKr6

June 15, 2022 – Frederick Kozak of Appia Rare Earths &

Uranium talks about new REE discoveries at Alces Lake

https://bit.ly/3zpUaAr

th

InvestorIntel Column Highlights for the Week of June 13-20 ,

2022:

Stephen Lautens · June 17, 2022 – We’re Back – PDAC mood

positive in spite of sagging market

https://bit.ly/3O3L5BE

Dean Bristow · June 17, 2022 – Generation Mining looks

to knock Russia off its palladium pedestal

https://bit.ly/3xDdYOl

Byron W King · June 16, 2022 – Fresh from Toronto: Three

Mexican Beauties https://bit.ly/3xxOwJS

Stephen Lautens · June 14, 2022 – InvestorIntel is

digging for stories at PDAC 2022 https://bit.ly/39t2BjN

Bob Hanes · June 14, 2022 – Rare earths giant MP

Materials invests heavily to rebuild a U.S. magnetics

supply chain https://bit.ly/3xPTAuH

News Releases* InvestorIntel Published for the Week of June

13-20th, 2022:

June 20, 2022 – Romios Gold Begins Field Work On 3

Projects Near Newmont’s Musselwhite Gold Mine, NW

Ontario https://bit.ly/3beqVXg

June 17, 2022 – Awakn Life Sciences to Present in

Upcoming June 2022 Conferences https://bit.ly/3y9e6GR

June 17, 2022 – Nano One Announces Closing of Rio Tinto Strategic Investment and Collaboration Agreement https://bit.ly/3xZwwtu June 17, 2022 – Commissioning Commences at Vital’s Saskatoon Rare Earth Extraction Plant https://bit.ly/3tGEFAp June 16, 2022 – Voyageur Pharmaceuticals Ltd. Announces Closing of Over Subscribed $1Million Private Placement and Issuance of Shares for Debt https://bit.ly/3MWLLHH June 16, 2022 – TRU Signs Definitive Option Agreement for Consolidation of Final Contiguous Gold Property at Golden Rose Project https://bit.ly/3xUrDBD June 16, 2022 – ePlay Digital Announces the First Pet Store in the Metaverse https://bit.ly/3aY9mKR June 15, 2022 – NEO Battery Materials Signs a Collaboration Agreement with Applied Carbon Nano Technology Ltd. in South Korea https://bit.ly/3tDjyiq June 15, 2022 – Alphamin Operations Unaffected by Recent Closure of Bunagana Border Post with Uganda https://bit.ly/3tFrLCy June 15, 2022 – Nano One Appoints Lisa Skakun as Independent Director and Sets 2022 AGM Date https://bit.ly/3xRWTS1 June 14, 2022 – Kalo Gold Provides Vatu Aurum Gold Project Exploration and Geological Update https://bit.ly/3aZtfkG June 14, 2022 – Valeo Pharma Reports Its Second Quarter 2022 Results and Highlights https://bit.ly/3Qr3PfZ June 14, 2022 – Awakn Life Sciences Reports Results for Quarter Ended April 30, 2022 https://bit.ly/3b0L0Aj June 14, 2022 – Appia Begins Trading on The OTCQX https://bit.ly/3xTc39E June 14, 2022 – Romios Gold Reports High-Grade Assays Up to 17.9 g/t Au from Previously Undocumented Prospects on the Kinkaid Project, Nevada https://bit.ly/3MQdtFZ June 14, 2022 – TRUSTBIX INC. Announces Release of BIX Origin https://bit.ly/3HjY7se

June 14, 2022 – Hemostemix Announces the Incorporation

of PreCerv Inc. And a Global Field of Use License to

NCP-01 https://bit.ly/3zzjTGH

June 14, 2022 – Appia Provides 2022 Drilling Update for

WRCB and Augier and Confirms Continuity of Very

Significant Augier Discovery at Alces Lake Rare Earth

Property, Northern Saskatchewan https://bit.ly/3Oji05b

June 14, 2022 – Drill Assay Results Demonstrate

Significant Expansion Potential of the 170 MT La Paz

JORC Resource https://bit.ly/3O6Ojoh

June 14, 2022 – Metallum signs Negotiation Agreement

with the Pays Plat First Nation https://bit.ly/39lji0B

June 14, 2022 – Fission 3.0 and Traction Drilling

Intersects Additional Anomalous Radioactivity at Lazy

Edward Bay https://bit.ly/3NSGwKz

June 13, 2022 – CBLT Options Chilton Cobalt

https://bit.ly/3Hkp8vD

June 13, 2022 – Bald Eagle Unveils New Porphyry-Style

Copper Anomaly on Consolidated Hercules Land Package

https://bit.ly/3OgcAYB

June 13, 2022 – Kalo Gold Provides Vatu Aurum Gold

Project Exploration and Geological Update

https://bit.ly/3zF9ppn

June 13, 2022 – Ucore Hosts ‘Secure Supply Chains’ Panel

at PDAC 2022 – Rare Earths and other Critical Metals

https://bit.ly/3Odiolq

June 13, 2022 – Imperial Mining Receives Positive

Results for the Preliminary Economic Assessment (PEA)

for Crater Lake https://bit.ly/3xMMWFw

(*) The company news releases that are published are from ii8

System members. For more information, email me direct and

special thanks to Assistant Publisher Raj Shah.We’re Back – PDAC mood positive in spite of sagging market After an absence of more than two years, PDAC was back this week. Even lingering Covid concerns and soft markets couldn’t dull the enthusiasm at the world’s largest mining and investor trade show back in person for the first time since 2020. Attendance was down from pre-pandemic highs with the official count placing this year at almost 17,500 visitors (compared to in-person 23,000 attendees in 2020), but you wouldn’t have known it from the first day’s crush at registration. Either surprised or out of practice, PDAC officials struggled to sign in thousands of people who showed up on the opening day. At one point police shut the outer doors to the Metro Convention Centre because the registration floor was over the safe capacity. Once inside there was still an over half hour wait for pre-registered attendees to get their badges. But miners and investors are by necessity a patient lot, and none of the first day’s initial delays dampened the enthusiasm of being back in person. For years the industry and investors have tried to judge market sentiment for the coming year by the “mood on the floor”. The mood at PDAC 2022 was decidedly upbeat and enthusiastic, even as the S&P/TSX and the Venture Composite Indexes dropped between Monday and Wednesday as people were packing up their booths. The buoyant mood might have been the result of the joy of seeing people again, but there was a genuine feeling of optimism for the gold, nickel, silver and critical materials sectors, especially among the large number of companies who had secured financing this spring for continued exploration and development in 2022.

As a PDAC media sponsor, InvestorIntel found a number of old favorites and hidden gems on the trade show floor, some of which we will be bringing to the attention of our readers in the next few weeks. Some companies have been quietly expanding and developing their projects during Covid and now deserve a wider audience. The InvestorIntel PDAC Panel Series: “The Uranium Bull in the Room” with moderator Tracy Weslosky and panelists Dr. Richard Spencer from U3O8 Corp., Tom Drivas from Appia Rare Earths and Uranium, Curtis Moore from Energy Fuels, and Jon Bey from Standard Uranium. We also took the opportunity to catch up with some leading CEOs and industry experts for an update and analysis on markets, commodities and progress on properties. These informative panel discussions will be available as videos next

week on InvestorIntel.com and our YouTube channel. If the energy and enthusiasm (not to mention the packed hospitality suites) of PDAC 2022 is any indicator, market sentiment is extremely high for a good second half of this year. It’s not a very scientific measurement, but at this point, we’ll take it. InvestorIntel is digging for stories at PDAC 2022 PDAC 2022 is underway, and InvestorIntel is one of the media sponsors at the world’s largest mining and exploration convention. We are busy looking for new stories and meeting old friends at the first in-person PDAC since 2020. Monday through Wednesday (June 13-15), InvestorIntel is conducting exclusive interviews with industry leaders, presidents and CEOs of some of the most interesting silver, gold, rare earths, uranium and other critical materials companies. On Monday our first panel was Rare Earths, Sustainability & Meeting the EV Market Demand hosted by InvestorIntel CEO and Founder Tracy Weslosky with panelists Mark Chalmers, President and CEO of Energy Fuels Inc. (NYSE American: UUUU | TSX: EFR) and Constantine Karayannopoulos, President, CEO and Director of Neo Performance Materials Inc. (TSX: NEO).

Our next panel discussion was hosted by Chris Thompson of eResearch on Silver, The Technology Metal & Market with Byron W. King, InvestorIntel columnist, Bald Eagle Gold Corp.‘s (TSXV: BIG) CEO Chris Paul, Silver Bullet Mines Corp.‘s (TSXV: SBMI) VP Capital Markets and Director Peter Clausi, and Simon Ridgway, Founder, Director, President and CEO of Volcanic Gold Mines Inc. (TSXV: VG).

To finish off Monday’s schedule, InvestorIntel columnist and renowned critical materials expert Byron W. King, led a panel discussion on Building the EV Material Supply Chain with Appia Rare Earths & Uranium Corp.‘s (CSE: API | OTCQB: APAAF) President Frederick Kozak, Search Minerals Inc.‘s (TSXV: SMY | OTCQB: SHCMF) President, CEO, and Director Greg Andrews, Avalon Advanced Materials Inc.’s (TSX: AVL | OTCQB: AVLNF) President, CEO and Director, Don Bubar, and Vital Metals Limited‘s (ASX: VML | OTCQB: VTMXF) Managing Director, Geoff Atkins.

If you are at PDAC, be sure to visit the InvestorIntel media studio on Level 700. Lynas Continues Its Reign Under Amanda The Great Look online, and you will discover that while Lynas Rare Earths Ltd. (ASX: LYC) is covered by 9 research companies, it is impossible to find one PDF Equity Research Report online. For Australian-listed companies, sometimes they publish the reports on their website; unfortunately, not for Lynas. Dig deeper online and you may see a headline about whether

Lynas has too much debt… these conclusions are in my humble

opinion quite wrong, and underestimate this rare earths’ ruler

outside of China, Amanda Lacaze.

I ran my conclusions by a semi-retired analyst, who requested

anonymity and wrote me back promptly in agreement: “Saw their

balance sheet and they are running just over 1x debt: cash

flow and their cash flow is strong based on growing sales and

commodity prices.”

The media loves to tout Chinese control of rare earths, but it

is a woman with an iron fist that rules the rare earths world.

Proud of how she likes to watch the pennies, it is

unquestionably the reason why she has held the role as a Non-

Executive Director for ING Bank Australia Ltd. for over 11

years.

Now let’s start with some prenuptial notes on Lynas, before

you decide to make a commitment to this industry giant.

Lynas Rare Earths Ltd. is listed on the Australian Securities

Exchange (ASX: LYC). The company also has a sponsored Level 1

American Depository Receipt (ADR) program through the Bank of

New York Mellon (Code: LYSDY). On June 6 (Australia), the

shares closed at AUD$ 9.35. There 902.4 million shares

outstanding, giving the company a market capitalization of

approximately AUD$8.4 billion (US$6.1 billion. At December 31,

2021, Lynas reported six month results including AUD$741.7

million positive working capital (including AUD$674 of cash

and short term deposits) and AUD$156 million long term debt.

Cash and short term deposits increased to AUD$768.4 at March

31, 2022.

Lynas’ quarter ended March 31, 2022, had the following

highlights:

All necessary approvals received for the Kalgoorlie Rare

Earth Processing Facility (Australia based processing

facility)Site clearing of the Kalgoorlie facility location is

complete

Delivery of major equipment to Kalgoorlie site with

foundation and building work underway

Kalgoorlie should be on track as part of the company’s

2025 Foundation Project program

Planning is underway for the US Rare Earths Processing

Facility including contracts signed with the US

Department of Defense

Record quarter for operations including:

Sales revenue of AUD$ 327.2 million (AUD$ 202.7

million previous quarter)

Sales receipts of AUD$ 262 million (AUD$151

million previous quarter)

Total REO production of 4,945 tonnes (4,209 tonnes

previous quarter)

NdPr production of 1,687 tonnes (1,359 tonnes

previous quarter)

Lynas noted quarterly price strength for NdPr

contributed to record financial results

Automotive demand for rare earths “remains strong”

Exploration drilling under the existing Mt. Weld

extraction pit revealed continuous rare earth element

mineralization along 1,020 metres of drill core. Further

targeted exploration is to be conducted “with the goal

of meeting accelerating customer demand”.

The company targets to be operating four sites in three

countries with global sales in 2025

Having heard Amanda speak on several occasions in her early

role as Managing Director nearly eight years ago, I recall

believing that her reign would be short-lived. Her valiant

commitment to the bottom line above all else seemed

conservative and backward compared to the charismatic

marketing styles of other leaders I quite like in the market.

Commenting that weekly meetings would necessitate

accountability for every dime spent, seemed dismal and drollto me, it seems, however, she was quite right. As down winds from the recession are upon us, or gales of a correction are indeed in full force, I look to the critical materials sector for which many experts harbor no fears. And with the demand for rare earths continuing to exceed supply, it seems that the noble Australian woman whose fearless tactics took me by surprise is now the one championing it all. American OEM automotive industry’s big problem with lithium … and why Elon Musk is wrong. There isn’t enough lithium mined, and there can never be enough lithium mined and processed into end-user forms economically, to replace the use of fossil-fueled internal combustion engines in the powertrain systems of the current one and one-half billion personal and mass transportation vehicles with electric motors powered by rechargeable lithium- ion type storage batteries. I think that most of the managers of the global OEM automotive, aerospace, and shipbuilding industries know this, but they are powerless in the face of the demands of politicians who have given in to the greens who are unaware of the limitations of physical natural resource production and processing for non fuel minerals, and who rely on the advice

of narrowly and poorly educated and just plain dumb “experts” who have credentials but no experience of business operations, real-world economics or even rudimentary geology. The more often these experts repeat such mantras as “settled science” (to prove that climate change is caused by or can be remedied by human activity) or proclaim the unlimited resources of “earth abundant minerals” (to prove that non-fuel natural resources are unlimited) the more destructive their ignorance impacts our cheap energy based (which they neither see nor understand) standard of living and quality of life. In order to preserve their industry and their high paying jobs long enough until they can safely retire, the current top managers of the global OEM automotive industry have accepted the economic power and poison of the green energy “transition” in making their decisions rather than the free marketplace. It is typically stated that a modern internal combustion engine powered vehicle has over 6,000 components and that an EV, an electric powered vehicle, is “much” simpler. In fact, the much simpler vehicle still has some 4,000 parts. Henry Ford pioneered the vertical integration of his eponymous car company in the teens of the last century to avoid being controlled by the natural resource “trusts” (monopolies) of his time. By the early 1920’s the Ford Motor Company manufactured internally all of its necessary component parts except for tires (Ford was a personal and lifelong friend of Harvey Firestone) and produced all of its own needs for electricity. As the decline of the auto-industrial age proceeded after the oil price shocks of the 1970s the OEMs shed their then advanced vertical integration (almost always in order to raise money to cover losses and declining margins) and adopted just- in-time delivery of necessary parts from the then reborn and expanding external supply base. Rising American labor costs in the 1980s created a mass exodus of OEM automotive suppliers to

Mexico and Asia. Shortly thereafter that Asian vehicle makers entered the US markets and rapidly learned enough to destroy the postwar global dominance of the OEM American car industry. Chrysler needed rescuing first, then GM. Ford survived the downsizing better than the others, but like them had to withdraw from the global markets of the heyday of the globalization of the pre-war (WW2) era. Now, in 2022, the OEM American car and truck assemblers – for that is the correct term for a company that imports all of its components and assembles them into a vehicle – are being told that they must reduce and eliminate the use of imported components and find or develop domestic or friendly nation sources to redevelop domestic vertically integrated manufacturing. At the same time, they are being told by the government that they must convert all power trains to electric drive fueled by rechargeable storage batteries. The answer, of course, is to rebuild domestic factories to once again produce the 4000 components per vehicle they will need for EVs. There will be components which are common to both fossil-fueled and electric powertrains and vehicles, but such electromechanical marvels as modern multi-speed transmissions as well as efficient gasoline and diesel fueled internal combustion engines will cease to receive attention and the skills to build them will wither away. The key component to be researched and manufactured domestically now has become the lithium-ion battery to be used to power the battery electric vehicles to be built. No such mass production industry for this type of component has ever been successfully built or operated by a domestic American company. The supply chain for manufacturing lithium ion batteries for vehicle powertrains does not exist today in the USA.

Let me explain how the contemporary (legacy) global OEM

automotive industry finds and chooses among its parts

suppliers, so you can understand the dilemma that the

contemporary geopolitics of globalization has caused, in

particular, in the United States and Europe.

The outside OEM automotive suppliers, of course, must have

experience in building and successfully selling the components

for the same or same type of use. This is not taken for

granted just because of the size or reputation of the seller.

All production parts accepted for use by the domestic American

OEM automotive industry must undergo the PPAP (production part

approval process) and the suppliers must pass a financial due

diligence.

PPAP involves real time passing of the test of operating under

real-world conditions for at least three years in general and

for the life of the part’s warranty. For a lithium-ion

powertrain battery, this means today’s operation with no more

than the stated degradation of capacity for up to 8 years.

Upon passing the PPAP, the due diligence requires that the

component meet the following requirements:

On-time delivery, to specification, in the volumes

agreed, and at the agreed price,

Just-in-time delivery to agreed locations, no matter the

weather conditions,

All parts must meet agreed customer specifications

within a narrow quality range, and

Prices are agreed for the life of a vehicle model

It has been the practice of the OEM automotive industry to

make the direct supplier of the component or subassembly, the

Tier One supplier, responsible for the all of its (sub)

suppliers to meet their PPAP requirements, even if it is the

assembler who PPAPs the mechanical and electrical quality of

the sub-tier supplier.Very recently, for the first time in 25 years, the OEM domestic American automotive assemblers have begun to look at the entire supply chains for critical (without them the vehicle cannot be sold) components. In the last year, General Motors and Ford have announced “agreements” with domestic, non producing, semi-finished raw material suppliers, of lithium and the rare earths, to provide them with raw materials (lithium) and critical component parts (rare earth permanent magnets), which the companies will somehow get processed into the forms necessary to produce rechargeable storage batteries and electric motors from a currently non-existent domestic American manufacturing base. Tens of billions of dollars have already been allocated by the domestic American OEM automotive industry to build 7 battery “gigafactories” and several EV platform ( the battery plus the electric motor) factories. Among the domestic OEM assemblers nearly 100 billion dollars has also been allocated to the construction of dedicated and multi-functional BEV plants. The OEM automotive assemblers have bet the farm that they can become domestic vertically integrated manufacturers of battery powered electric cars and trucks. Yet, as of today, not one gram of ESG lithium or rare earths is produced in the United States or Canada. Look at the following chart:

This chart from the IEAE tells you that there is no possibility of producing enough lithium to manufacture the batteries that would be required by the currently planned demand after this year. I think that the ignorance, by politicians and journalists, of the steps universally and necessarily required in the operations of any and all global original equipment manufacturing business is due to intellectual laziness, intelligence limitations and the rapidly declining coverage and quality of American “education” at all levels. The attempt to eliminate selection by merit, rather than expand it, and replace it with superficial characteristics as the criteria for education has rapidly eroded the ability to select those best qualified for specialized education and training and given over world leadership in science and engineering to Asian nations.

I repeat that the success of a transformation of the fuel for vehicular transportation from liquid fossil fuels to electricity stored on board in rechargeable batteries depends entirely on the supply of the element lithium. And that energy and resource illiteracy and innumeracy among our managerial and credentialed classes are the only reason that the domestic American OEM automotive assembly industry has blindly bet the farm on a green fetish pursued by some of the dumbest (or most corrupt, or both) politicians in the history of our Republic. The BEV revolution will not engender a second Auto-Industrial age in America. It will, in fact, end the dominance of that industry, and ensure that BEVs survive only as luxury vehicles to be driven between enclaves with charging facilities. Elon Musk tweeted two weeks ago that Tesla may have to get into the lithium mining business. He said that although there is lithium everywhere and lots of it, the mining industry is very slow to bring it to market. Elon Musk is a brilliant businessman and an even more brilliant financier, but he is a mineral economics moron. I invite readers to please challenge my assumptions and conclusions with data, logic, experience, and educationally based counterarguments. Geoff Atkins talks about Vital Metals’ transitional

year from developer to producer in 2022 In this InvestorIntel interview with host Tracy Weslosky, Vital Metals Limited‘s (ASX: VML | OTCQB: VTMXF) Managing Director Geoff Atkins talks about the company moving from rare earths miner to producer in the coming months. In the interview, which can also be viewed in full on the InvestorIntel YouTube channel (click here), Geoff talks about production from Vital’s Nechalacho rare earths project in the Northwest Territories going to its Saskatoon extraction plant, with production of high purity rare earth carbonate forecast to commence in June 2022, and its rare earths product to be sold to Vital’s take off partner in Norway later this year. Geoff goes in to explain, for Vital “this year is that transformational process from developer through to operator.” Being an Australian company with both its cornerstone project and processing facility in North America, Geoff also discusses increasing the company’s presence in the North American markets in the coming months as it moves to producer. Don’t miss other InvestorIntel interviews. Subscribe to the InvestorIntel YouTube channel by clicking here. About Vital Metals Limited Vital Metals Limited (ASX: VML) is Canada’s first rare earths producer following commencement of production at its Nechalacho rare earths project in Canada in June 2021. It holds a portfolio of rare earths, technology metals and gold projects located in Canada, Africa and Germany. To know more about Vital Metals Limited, click here Disclaimer: Vital Metals Limited is an advertorial member of

InvestorIntel Corp. This interview, which was produced by InvestorIntel Corp., (IIC), does not contain, nor does it purport to contain, a summary of all the material information concerning the “Company” being interviewed. IIC offers no representations or warranties that any of the information contained in this interview is accurate or complete. This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Prospective investors are urged to review the Company’s profile on Sedar.com and to carry out independent investigations in order to determine their interest in investing in the Company. If you have any questions surrounding the content of this interview, please contact us at +1 416 792 8228 and/or email us direct at info@investorintel.com.

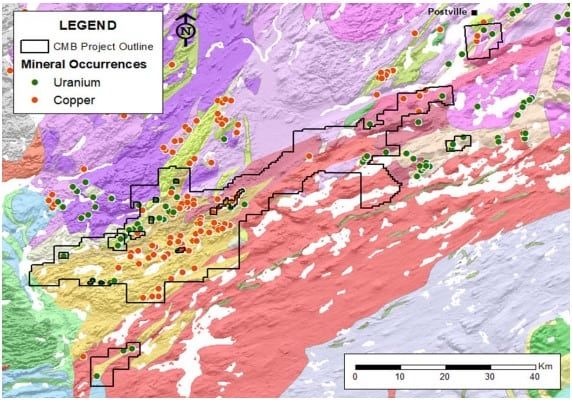

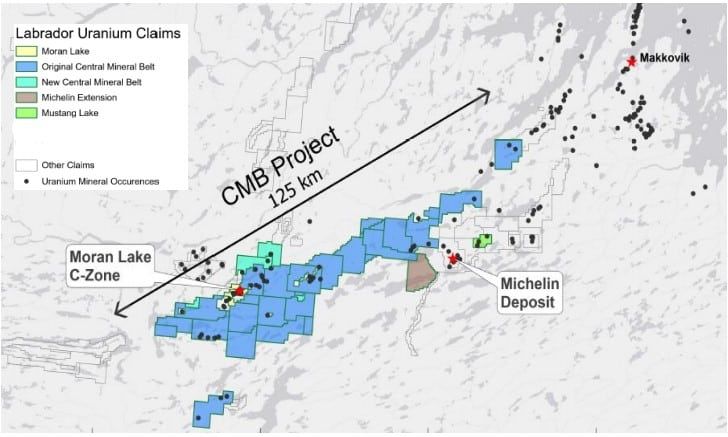

Cash-rich Labrador Uranium continues to expand and explore Canada’s mineral superstore I promise this is the last article I write about a junior miner in Newfoundland & Labrador… this week. As I’ve noted in the past, this region of Canada is blessed with an abundance of resources of all kinds – gold, silver, copper, nickel, cobalt, iron, zinc, molybdenum, rare earths and uranium to name a few. I recently discussed a gold explorer that has also stumbled across some hard rock lithium (pegmatite) in the area. It would seem we’ve found our green revolution superstore, all in a mining friendly and politically stable jurisdiction, occupied by some of the most friendly people on the planet. What more could you ask for? That’s why I continue to be fascinated by, and write about this important mining region. So what commodity to focus on today? How about uranium. That’s right, Saskatchewan’s Athabasca Basin doesn’t host all of Canada’s uranium resources. There’s plenty to be found in the Central Mineral Belt (CMB) in Labrador. And a key new explorer in the region is Labrador Uranium Inc. (CSE: LUR | OTCQB: LURAF) recently spun out of Consolidated Uranium Inc. (TSXV: CUR | OTCQB: CURUF), by transferring ownership of the Moran Lake Project to LUR in exchange for 16 million common shares of LUR. Shortly after the spin-out was announced LUR then agreed to acquire from Altius Minerals Corporation (TSX: ALS) a 100% interest in the 125,000 hectare Central Mineral Belt

(CMB) Uranium-Copper Project, located adjacent to the Moran Lake Project, and the Notakwanon project, both located in Labrador. Lastly, LUR rounded out its Labrador portfolio with an agreement to acquire Mega Uranium Ltd.’s 66% participating interest in the joint venture that holds a 100% interest in the Mustang Lake project, approximately 9.5 kilometres northeast of Paladin Energy’s Michelin deposit with its 128 million lb uranium resource. That’s a pretty impressive land grab in a span of 7 months since Consolidated Uranium first announced the spin out. The financial team was also busy for Labrador Uranium during that time amassing roughly C$18 million in two capital raises, with the latest one closing April 28th. All of this has created a well funded exploration and development company focused on uranium projects, with over 139,000 ha in the prolific CMB in central Labrador. Both the Moran Lake Project, which hosts historical uranium mineral resources, and the CMB Project, have had substantial past exploration work completed with numerous targets with uranium, copper and IOCG (iron oxide, copper, gold) style mineralization. The Notakwanon Project is underexplored but drill ready. All three projects are expected to be the focus of an aggressive exploration program in 2022.

Source: Labrador Uranium Corporate Presentation One of the unique things about Labrador Uranium, as they move forward to start drilling this massive portfolio that they’ve put together, is their use of technology. The CMB region has seen significant historical exploration work by multiple private and public groups resulting in a large database of geological data available. The Company is reviewing several terabytes of data including, geological, geochemical, mineral occurrence and geophysical (magnetics and radiometrics) to seek overlooked, potentially large mineral systems that may not be easily identifiable through standard field and remote exploration techniques for various reasons including extensive cover or lack of drill coverage. LUR is utilizing its internal expert knowledge to review the existing datasets to map geological framework elements such as stratigraphy, alteration, fault and fracture systems, folding and intrusive contact. Then utilizing technology, the team is assembling training datasets upon which to train Machine Learning algorithms to identify yet unknown or poorly expressed mineral systems in the belt together with geomechanical modeling

approaches to identify and prioritize mineral targets. Regardless of whether I’ve explained this in a coherent enough way for people to understand, or if I made a complete mess of the explanation, suffice it to say that their process has already identified >140 targets. Many of which are copper, which isn’t necessarily a bad thing. Source: Labrador Uranium Corporate Presentation The next weeks and months will be interesting to see where Labrador Uranium focuses their activity. As noted, they are well funded for a large and aggressive exploration program in 2022. Over half of their current C$37 million market cap is in the form of cash to go out and generate plenty of news. Combine that with another potential rally in the uranium sector and investors could see a handsome return if the drill bit hits its mark. Paladin Energy’s Michelin deposit has proven there are elephants roaming the plains of central Labrador.

Greg Andrews of Search Minerals on the positive impact of their updated resource estimate on its coming PEA In this InvestorIntel interview with host Tracy Weslosky, Search Minerals Inc.’s (TSXV: SMY | OTCQB: SHCMF) President, CEO, and Director, Greg Andrews, discusses the positive impact on its upcoming PEA of the recently increased mineral resource estimates for Search Minerals’ Deep Fox and Foxtrot Critical Rare Earth Element properties in South-East Labrador. In the interview, which can also be viewed in full on the InvestorIntel YouTube channel (click here), Greg Andrews tells InvestorIntel that its updated resource estimates will form the basis of Search’s upcoming Preliminary Economic Assessment (PEA). He goes on to explain how the PEA will take into account the significance of both the Deep Fox and Foxtrot properties. With Search Minerals positioned to become a reliable source of rare earths in North America, Greg also comments on how the 2022 Canadian Federal Budget is likely “to spur investment into all critical minerals, and the rare earths in particular.” Don’t miss other InvestorIntel interviews. Subscribe to the InvestorIntel YouTube channel by clicking here. About Search Minerals Inc. Led by a proven management team and board of directors, Search

is focused on finding and developing Critical Rare Earths Elements (CREE), Zirconium (Zr) and Hafnium (Hf) resources within the emerging Port Hope Simpson – St. Lewis CREE District of South East Labrador. The Company controls a belt 63 km long and 2 km wide and is road accessible, on tidewater, and located within 3 local communities. Search has completed a preliminary economic assessment report for FOXTROT, and a resource estimate for DEEP FOX. Search is also working on three exploration prospects along the belt which include: FOX MEADOW, SILVER FOX and AWESOME FOX. Search has continued to optimize our patented Direct Extraction Process technology with the support from the Department of Industry, Energy and Technology, Government of Newfoundland and Labrador, and from the Atlantic Canada Opportunity Agency. We have completed two pilot plant operations and produced highly purified mixed rare earth carbonate concentrate and mixed REO concentrate for separation and refining. We also recognize the continued support by the Government of Newfoundland and Labrador for its Junior Exploration Program. Search Minerals was selected to participate in the Government of Canada Accelerated Growth Service (“AGS”) initiative, which supports high growth companies. AGS, as a ‘one-stop shop’ model, provides Search with coordinated access to Government of Canada resources as Search continues to move quickly to production and contribute to the establishment of a stable and secure rare earth element North American and European supply chain. To learn more about Search Minerals Inc., click here Disclaimer: Search Minerals Inc. is an advertorial member of InvestorIntel Corp. This interview, which was produced by InvestorIntel Corp., (IIC), does not contain, nor does it purport to contain, a

summary of all the material information concerning the “Company” being interviewed. IIC offers no representations or warranties that any of the information contained in this interview is accurate or complete. This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Prospective investors are urged to review the Company’s profile on Sedar.com and to carry out independent investigations in order to determine their interest in investing in the Company. If you have any questions surrounding the content of this interview, please contact us at +1 416 792 8228 and/or email us direct at info@investorintel.com.

Betting the farm on lithium in the short term and the long term. Politics Before Economics: The Coming Train Wreck of Peak Lithium, Mandated EVs, and Alternate Electricity Generation This is the best time ever to invest in lithium mining and processing because the legacy global OEM automotive industry as well as dozens of newcomers, including TESLA, have bet their continued and future existence not on the market but on the politically mandated ultimate replacement of internal combustion engine power trains by rechargeable battery fueled electric ones. This powertrain replacement is to be 100% dependent on lithium-ion batteries to store the electricity (i.e., fuel) to supply the electric motors that will replace fossil fuel using internal combustion engines. These EV batteries are, for their operation, 100% dependent on the chemical element, lithium. At the same time, the politicians have also decreed that the generation of relatively inexpensive electricity, which today is mostly done by the use of the fossil fuels, coal, oil, and natural gas (with the balance, more than 20%, coming from nuclear) shall be completely replaced by alternate forms of electricity generation dependent upon the wind and the sun with their excess outputs stored until needed in lithium ion batteries. Wind and solar are, at best, intermittent, and they are therefore not remotely reliable or dependable. They exist only because of government subsidies and, worse, mandates. Alternate energy generation being intermittent must be smoothed out (continuously maintained) ideally (in the Green

Dream) by backup batteries. This would ultimately require enormous quantities of lithium, more than for EVs, for the gigantic smoothing and backup systems that would be necessary. From the perspective of the supply of the key critical battery metal, lithium, these two goals, electrification of mobility and stationary storage of electric power for grid smoothing are competitive with each other for lithium, and this competition shows the complete ignorance of politicians and manufacturers of the fact that the overall demand for lithium from the two mandated uses cannot possibly be supplied from currently existing, planned, or known accessible sources. A recent article in the Wall Street Journal states that “mining is like anything else. Eventually high prices stimulate more production. But the slow real-world expansion capabilities of mining explain the IMF’s forecast that mineral inflation would last “roughly a decade” until supply catches up.” This is utter nonsense. Mining any natural resource is entirely dependent on the physical accessibility of the resource, the grade (concentration) of the desired mineral, the ability of deployable technology to extract the desired mineral, the economics of the processing of the mineral concentrate to a usable form, and that the total costs incurred by the entire supply chain can be borne by the selling price for the end user products enabled or manufactured from that resource. Supply of anything cannot “catch up” to demand if that supply is limited by a maximum price limit for the demanded form and for the accessibility, grade, and applicable process technology for the “deposit.” The highest grade accessible and processable deposits of lithium from brine and from hard rock minerals are, respectively, in Chile, Argentina, and Australia. These

deposits are already mined at scale and represent the lowest cost of production today. So, since the highest grade, accessible, physically and technologically, deposits are in production why can’t they just ramp up and supply any amounts of lithium needed? Those writers who are ignorant of geology, mineral economics, and geopolitics, and who are not aware of the limitations of contemporary known deposits of natural resources, think that lithium production is organic, i.e., that to get more lithium you simply do more mining. But, in fact, all mineral deposits decline in grade and fall below economic grades after a time. The period during which the mine is projected to be profitable is called, for that reason, the life of the mine. In 2007 the global production of lithium, measured as metal, was 16,000 tons. In 2021 that figure was 86,000 tons, a 5.5X increase. Yet at the beginning of 2022, the price of metallic lithium, $60,000 a ton in January 2021 had reached $360,000 a ton! I note that lithium metal is now more expensive than silver. Why? The demand for lithium today just for batteries is 60% of global lithium production, and new battery factories are coming online and being planned and under construction daily. The total demand for lithium for all of these factories by 2025 is calculated to be 2.5 times total global lithium production in 2021. By 2030 that figure would be 5 to 10 times the total global 2021 output of lithium. It is likely that the lithium supply is already in deficit due to existing battery factories buying for inventory and traders buying for speculation. The legacy OEM car/truck makers have almost all allocated essentially all of their R&D capital and their new manufacturing construction to EVs. The better managed ones

realizing that the total conversion of their outputs solely to EVs cannot be supported anytime soon, if ever, by the lithium supply chain and that the cost of such vehicles is already prohibitive in the mass market are hedging their bets by continuing to plan for a mixed output of EV and fossil fueled powertrains indefinitely. Mis-allocations of capital in the most capital intensive industry on earth, the OEM automotive industry, cannot be reversed rapidly, and the damage to competitive advantage from losing the lead in internal combustion engine and transmission development could be fatal. This misallocation is not confined to the assembly operations of the global legacy OEMs. It could also be fatal to suppliers of ICE specific components. There are today some 1.5 billion ICEs in use globally, and the number is growing. Imagine that each of them will use on average 4 kg of lithium, measured as metal, for a 50 kWh lithium-ion battery. A Tesla Model 3 uses 6-8 kg for a 100 kWh battery. So to replace just today’s powertrains would require 6 billion kg of lithium, or 6 million tons of lithium, or 36 million tons of LCE (lithium carbonate equivalent). This is more than 70 years total global 2021 lithium production with nothing left over for the stationary storage market for grid smoothing of wind and solar generation. Neither conversion will ever happen, because it is beyond the capability and capacity of our current know-how in mining, refining, and fabricating the end-use raw materials. The looming and fatal to the green revolution lithium supply deficit has spawned an enormous price increase for the metal and its compounds, which has reversed the steady decline in the costs of lithium-ion batteries. But is it too late to stop the attempted suicide of the global OEM automotive and electric energy generating industries? Cars and trucks running on high priced electricity generated

by increasingly expensive wind and solar systems backed up by hugely expensive stationary storage battery parks will not have large enough markets to be self sustainable or reasonably priced. Lithium mining and processing will boom until no one can afford the vehicles or the electricity. At some point before that occurs the decarbonization of Western society will reverse and steel, aluminum, oil and gas will return to their central place in our world of cheap energy. Until then look for lithium, the rare earths, copper, and uranium to enter a long Super Cycle. Betting the farm on lithium in the short term and the long term.

You can also read