Market Outlook & Investment Strategy 2021 - JF Apex Research 5 February 2021 By - Apex Equity

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Market Outlook & Investment Strategy 2021

By

JF Apex Research

5 February 2021 1

Contents

Market Review 2020

Malaysian Economy & Outlook

State of the World Economy

Equity Outlook 2021

Fundamental and Technical Perspectives

Downside risks

Investment Strategy 2021

2

Market Review 2020

• The FBMKLCI currently recovers back to the pre-pandemic level of 1500-600 points. The

benchmark index staged a ‘V-shaped’ recovery from mid-March low of 1219 points.

• This was mainly underpinned by the two glove counters in the index component stocks and now

on banking stocks.

• KLCI performance is in line with global stock markets rally, driven by ample liquidity (ultra-low

interest rate, loan repayment moratorium) and policy expectations (more stimulus, unlimited QE

and Fed acts as direct lenders to corporate in the US).

3

Market Review 2020

• Net buying interests from local institutions (RM10.5b) and retail investors (RM13.9b) amid selling

pressure from foreign investors.

• Third consecutive year of net outflow of foreign funds (2020: RM24.6b; 2019 & 2018: RM11-12b

each).

• Declining foreign interests in local bourse was mainly due to uninspiring corporate earnings, lack of

economic vibrancy, sluggish crude oil prices and political instability.

1,500.0

1,000.0

500.0

-

MAR 6

JAN 3

FEB 7

OCT 2

OCT 9

OCT 16

OCT 23

OCT 30

DEC 4

DEC 11

DEC 18

DEC 25

DEC 31

JAN 10

JAN 17

JAN 24

JAN 31

MAY 1

MAY 8

MAY 15

MAY 22

MAY 29

JULY 3

JULY 10

JULY 17

JULY 24

JULY 31

AUG 7

AUG 14

AUG 21

AUG 28

SEP 4

SEP 11

SEP 18

SEP 25

NOV 6

NOV 13

NOV 20

NOV 27

FEB 14

FEB 21

FEB 28

MAR 13

MAR 20

MAR 27

APR 3

APR 10

APR 17

APR 24

JUNE 5

JUN 12

JUN 19

JUN 26

(500.0)

(1,000.0)

(1,500.0)

(2,000.0)

Foreign Local Institution Local Retail

4

Market Review 2020

• Although foreign funds dislike Malaysian equity market, they still favoured our debt

market especially on MGS thanks to relatively higher yield than developed markets.

• Fitch downgraded Malaysia’s sovereign rating to ‘BBB+’ from ‘A+’ in early Dec 20, whilst

Moody’s maintained our rating at ‘A3’. How about S&P?

5

Market Review 2020

• Most of the sectors underperformed the benchmark index and delivered negative returns except

Healthcare, Technology, Industrial, and Logistics in 2020.

• The performance of the local bourse was ranked in the middle among its peers thanks to relatively

less foreign funds & well supported by domestic liquidity especially retail investors.

6

Malaysian Economic Outlook

Contraction in GDP growth in 9M20

9M20 – (-6.4%) vs. 9M19 – (+4.2%)

Massive contraction of GDP during 2Q20 due to MCO

Overall, we expect 2020 GDP to deplete 4.9% yoy

GDP is expected to grow at +5.0% in 2021 – Rebound in both expenditure and production

sides amid recovery in domestic demand as well as global economic growth upon successful massive

vaccination.

IMF projects better global economic prospects in 2021 with +5.1% growth amid pickup in economic

activity following lesser stringent containment measures as well as the low base effect.

7

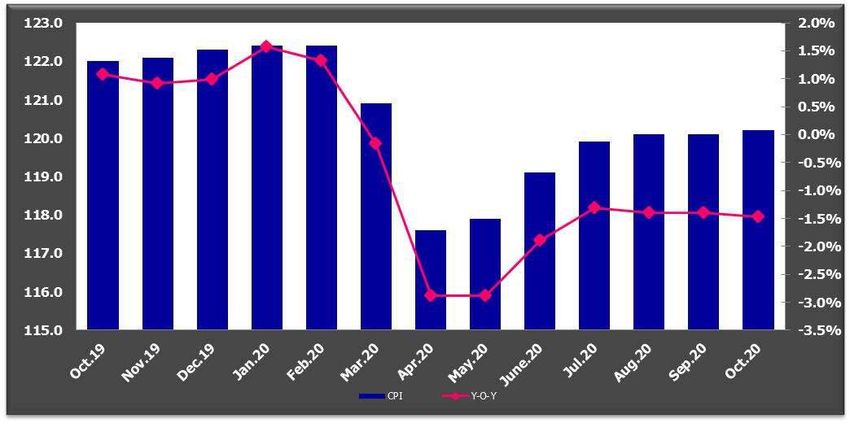

Malaysian Economic Outlook

10-month deflation

10M20 -1.0% vs. 10M19 : +0.6%

Due to lower cost of transport, housing and utilities prices

Overall, deflationary pressure for 2020 (-1.0% y-o-y)

2021’s CPI to grow at +1.8% y-o-y

Expect marginal inflation of +1.8% y-o-y anticipating greater economic activity as well as higher

crude oil prices

Overnight policy rate (OPR) to be maintained in 2021

Reckon that BNM to maintain an accommodative monetary policy by keeping its OPR unchanged

at 1.75% for 2021 to spur domestic demand

8

Malaysian Economic Outlook

Another contraction year for both export and import

Exports: -2.1% (10M20) vs -1.5% (11M19) – Contraction of Mining outputs (-21% yoy)

Imports:-6.3% (10M20) vs -3.8% (11M19) – Contraction in intermediate and capital goods

Expect recovery growth for 2021 albeit uncertainty persist

Expect trade performance to rebound amid easing pandemic impact as exports will be spurred by

sustainable pick-up in external demand

30.00 200.0%

25.00 150.0%

20.00 100.0%

15.00 50.0%

10.00 0.0%

5.00 -50.0%

0.00 -100.0%

Oct-19

Nov-19

Dec-19

Jan-20

Feb-20

Mar-20

Apr-20

May-20

Jun-20

Jul-20

Aug-20

Sep-20

Oct-20

(5.00) -150.0%

Trade Surplus (RM bil) Y-O-Y

9

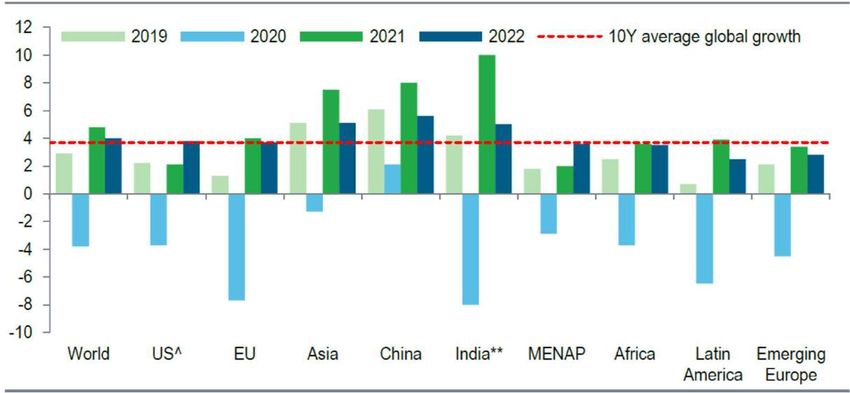

Global Economy

• Expecting better 2H21 pinning hopes on vaccine rollout.

• Asia will lead the global growth (especially China and India).

• Stanchart predicts global economic growth of 4.8% in 2021 vs 3.8% in 2020.

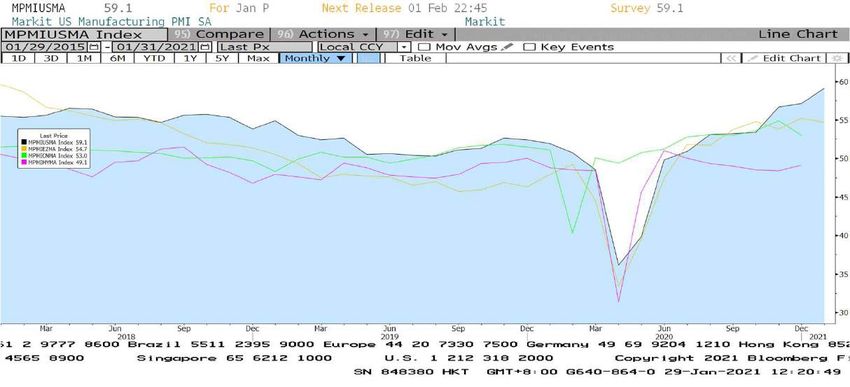

10Global Economy

• All major economies have exhibited ‘V’ shaped recoveries for their Manufacturing PMI

since March 20. Heading back to pre-pandemic levels or even higher.

• Strong rebound was due to pent-up demand, stock-up activities and policy aids.

• However, PMI in Malaysia eased in 2H20 (Equity Outlook 2021

Signs of bubble forming?

• Liquidity is ‘chasing’ risky assets as a result of low cost of money (interest rate).

• ‘Retail frenzy’ globally – Higher retail participation in stock market globally.

• GameStop, AMC, Blackberry, Express, Nokia under Reddit traders’ playgrounds. >>>

Spillover to glove counters in Malaysia.

• Even US junk bond yield hit record low.

• Record high of negative yielding debts.

• Hot money even pushing up property prices in some countries.

• ‘Mother of all bubbles’ - Bitcoin price hit record high. How to value Bitcoin?!

12Equity Outlook 2021

• Prevailing market - Rising risk-on appetite of investors; thematic/rotational plays;

sentiment or news flow driven, and fundamental takes a back seat.

• Rising cash call, bonus issue, stock split and IPO, SPAC frenzy globally – more shares

to the markets.

• Reality check - Why corporate are more willing to borrow from markets (equity and

bond) rather than from banks even low rate atmosphere?

a) capitalizing on current steep share price;

b) banks are still stringent on loan approval, and

c) aided by FED’s asset purchase programme.

13Equity Outlook 2021

• Widening gap between price discovery and valuation – 1) market is ‘very, very forward

looking’ this time; and 2) market is driven by high retail participation nowadays, i.e.

sentiment driven (euphoria, herd mentality, leverage).

• Investors look beyond gloomy FY20 results, i.e. market has priced in the negative

impact from coronavirus. Surprisingly, better-than-expected 3QFY20 results signaled

earnings recoveries are well on track moving into 2021?

• Unfortunately, second/third wave hit the world on the back of partial lockdown. Risk of

double-dip on economic growth?

• We reckon that the global economy is having ‘K-shape’ recovery (Tech, Healthcare,

Logistics, selected Manufacturing doing well; whilst Services, Retail, Aviation,

Hospitality, Commercial Real Estate having tough times).

• Earnings play catch-up with run-up in stock prices (especially Tech, Healthcare,

Logistics and export-oriented industries such as EMS, Furniture, Plastic packaging etc).

14Equity Outlook 2021

• How to quantify investor sentiment? Prices easily overshoot or undershoot nowadays

especially with short selling allowed.

• Is market rally sustainable? – We are currently under asset price inflation and this might

go on for a while before bubble is pricked.

• We reckon that 2021 market performance won’t be as strong as last year.

• Bullish consensus on 2021 outlook raises the odds of near-term pullback or major

correction.

15Equity Outlook 2021

• Reflation theme underway – as witnessed by rising commodity prices (Copper, Crude oil).

• But global inflation (US, China and EU) remains subdued and hence good for asset prices.

• Cyclical plays shall be in focus – Commodity, Banking, Industrials, Energy, Property, Construction

16Equity Outlook 2021

Our house view:

• Year-end 2021 FBM KLCI target: 1680 (17.4x 2021 PE, which is at its +1 SD

above mean) vs consensus of 1700-1800 points

• Market EPS growth: +13.5%

• Average Crude Oil (Brent) price: US$50/barrel

• Average USD/MYR: 4.05

• Average CPO price: RM2600/MT

• GDP growth: 5%

• Inflation: 1.8%

• OPR: 1.75%

17Equity Outlook 2021

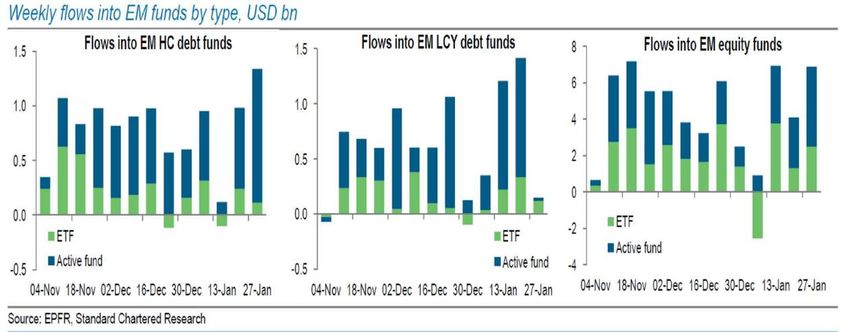

Global Fund flows & asset allocations in Emerging Markets (EM)

• Rising interests in EM – both for debt and equity especially on Hard Currency Debt.

• For equity, inflows mainly into Northeast Asia and India for Asia Pacific.

18Fundamental Outlook

• We deem the FBM KLCI is fairly valued based on consensus earnings estimates (at

1575-point level).

• The FBM KLCI currently trades ~ 14x 2021/2022 PE, which is below its historical

mean PE of 15-16x. (all-time high of 1896 points in 2018).

• Lower PE multiple is partly due to recent index reshuffle, with strong earnings

growths posted by the glove stocks.

• The FBM Small Cap Index is currently trading at 13.5x/10x 2021/2022 PE (at 15170-

point level), which is slightly above its historical average of 10-13x. (all-time high of

19330 points in 2014).

• Higher PE multiple due to higher participation rate of retail investors. 19Fundamental Outlook

Are small cap stocks still cheap?

• Historically, small cap stocks have been trading at 35% PE multiple discount to

large cap counters.

• Small cap stocks have experienced correction since Oct 20 once it had traded at

10-20% premium to the large cap.

• Currently trading at 28% PE multiple discount to large cap. Still room for correction.

20Fundamental Outlook

PER (X) Dividend yield (%)

2021 2022 2021 2022

FBMKLCI Index 13.9 14.2 4.0 3.9

HSI Index 12.9 11.3 2.9 3.2

FSSTI Index 15.5 12.6 3.9 4.4

JCI Index 11.1 8.8 1.9 2.4

SET Index 19.1 16.2 2.6 3.0

PCOMP Index 18.4 14.2 1.6 1.9

KOSPI Index 14.6 12.0 1.6 1.8

TWSE index 17.6 16.0 3.1 3.4

Average (ex-KLCI) 15.6 13.0 2.5 2.9

KLCI's premium

over region (%) -11.2 8.8 60.2 37.6

How foreign investors view Malaysia in respect of valuation?

• At current level of 1575 points, the FBM KLCI current valuation is considered cheaper

than other Asian peers.

• The local bourse now trades at ~ 14x forward PE, which is the third expensive bourse in

the region (after India, Taiwan and on par with the Philippines).

• Dividend yield wise, the local bourse looks attractive, higher than others.

21Technical Outlook

FBM KLCI Technical Chart

22Technical Outlook

• The FBM KLCI declined from an all-time high near 1900 points

in April 2018 to low of almost 1200 points in March 2020 before

rebounding to near-1700 points in December 2020.

• Immediate term: Negative view as technical indicators are

bearish with the RSI falling towards the oversold zone while the

MACD is declining below the signal line. Immediate support at

1550 points.

• Longer term: Positive as the uptrend channel since March 2020

is still intact. Downward reversal may occur if the 200-day

moving average (orange line) at 1535 points is breached.

23Downside risks

Major events or black swam which could derail local stock market in 2021: -

• Mean reversion and hence major correction in the US market - Steep valuations of current

US markets as S&P 500 now trades >20x forward P/E which is higher its historical average

of 15-16x.

• Rising inflation which triggers monetary tightening although FED promises zero rate till

2023 >>>>Rising yield leads to lower asset values.

• Full control of houses by left-wing politics in the US – Democrat could pass its bills on

increases in corporate tax rate, capital gains tax, tax hike on high-income households as

well as more regulations on tech giants.

• Capital flight from EM pursuant to twin deficits following depreciation of USD against EM

currencies.

• Domestic political instability - Snap polls after the pandemic?

• Downgrade of Malaysian sovereign ratings by S&P following Fitch’s rating cut?

• Removal of Malaysia from FTSE Russell WGBI (next review in March 21)?

24Downside risks

• Steep valuations of current US markets as S&P 500 now trades 22-23x forward P/E vs

dotcom bubble in 2000 of 24-26x. Rally is underpinned by FAANG stocks which

command premium valuations.

Source: Alpine Macro

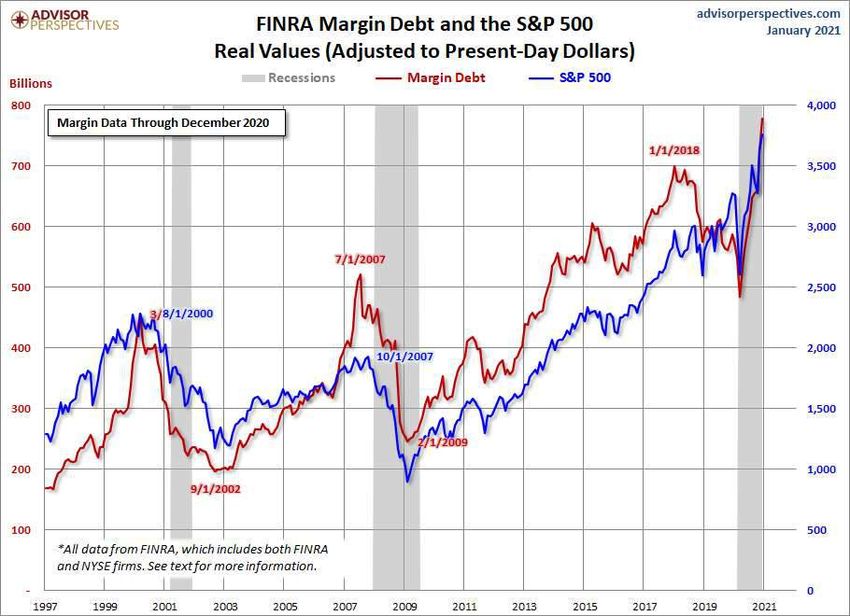

25Downside risks

• Record high of margin debt in the US currently.

• Margin lenders tightening loan, causing liquidity squeeze.

26

Source: Advisorperspectives.comDownside risks

Inflation rising faster-than-expected –

1) Supply-demand mismatch upon economy back to normalcy, e.g. rising freight charges;

rising commodity prices such as crude oil etc;

2) Low base effect resulting in higher Y-o-Y inflation (especially starting Mar/Apr 21);

3) Policy lag as FED has high tolerance on uptick of inflation since it sets average target of

2% over the longer run;

4) Minutes in Dec 20 of FED policy meeting showed that committee members were divided

on timeline of rate hike and it started to mention ‘tapering’.

5) US$900b fiscal stimulus to be rolled out in the US soon;

6) Highly indebted nations like inflation!

7) Market says so and this is real money - rising inflation expectation as indicated by the

10-year US Breakeven (UST nominal yield minus TIPS) .

27Downside risks

• 10-year US Breakeven exceeds pre-pandemic level.

• Subsequently followed by spike in 10-year US Treasury from 0.7% to 1%.

• FED seems like losing control of long-term bond yield (as true reflection of inflation as compared to

short term yield).

• Rising yield leads to lower asset values as price and rate have inverse relationship.

28Downside risks

• Democrat comes into full control for Senate and House.

• Biden’s team will concentrate on wealth distribution rather than wealth creation.

• Democrat is ‘big government’ as opposed to Republican which is advocacy of free

market and pro-business.

• Knee-jerk reaction on the Wall Street if capital gains tax and corporate tax rate hike?

Biden gets tough on tech giants – more regulations and break-up?

• Fiscal policy will take major role in stimulating economy whilst monetary policy could

take a back seat moving forward. Bigger fiscal stimulus or welfare policies to ‘kick start’

inflation?

29Downside risks

• EM crisis? Twin deficits? As sudden appreciation of EM currencies during 4Q20 could

dampen their export competitiveness.

• Besides, EM already bogged down by higher budget deficit as to fight the economy

which is being affected by the coronavirus pandemic.

• Sudden surge of USD, if any, could trigger capital flight from EM as Yellen advocates

strong dollar?

30Investment Strategy

• We advise investors to relook at: 1) reopening laggard, 2) dividend stocks and

3) relatively cheap valuation with good prospects instead of growth stocks.

• Favour: O&G, Consumer, REIT (Industrial & Retail), Utilities, Concessionaire,

Telco, Automotive, Finance, Property, Construction, Building Material sectors.

• Mixed outlook (selectively or buy on weakness): Healthcare, Technology,

Logistics, Industrials (EMS, Furniture, Plastic packaging etc), Plantation

sectors.

• Dislike: Aviation, Gaming, hospitality & tourism.

• Our top picks under coverage: Axiata, Bumi Armada, AME Elite, CCK, Wellcall,

31

FoundPac, LBS.Investment Strategy

• Although we envisage recovery is in store for 2021, we also anticipate an

uneven turf beckons for the market. Thus, investors shall construct a

portfolio consisting of value, defensive, dividend yielding stocks besides

focusing on cyclical and growth stocks.

Our stock picks by sectors are as follows: -

• O&G (Dayang, Bumi Armada, Yinson, Dialog, Alam Maritim, Coastal, Icon)

• Finance (HL Bank, RHB, Maybank, RCE cap, Takaful);

• Plantation (Kim Loong, Ta Ann, Sarawak Plantations, Sarawak Oil Palms, KLK)

• Property (SP Setia, Sime Darby Property, Lagenda Properties, Matrix Concepts, LBS,

Tambun Indah);

• Consumer (F&N, Nestle, Ajinomoto, Carlsberg, Heineken, QL, CCK, Cocoland, GCB,

Kawan Food, Amway, BJ Food, Hup Seng, Power Root, Spritzer, Hai-O);

• Telco (Axiata, TM)

• REIT (Retail & industrial such as IGB, Sunway, Axis REIT);

• Utilities (Tenaga, Malakoff, MFCB, Cypark, Pestech);

• Concessionaire (Litrak, Perak Transit, Taliworks, UEM Edgenta, Gas Malaysia,

Astro, Westport)

• Industrial (Press Metal, Wellcall, Scientex, Pecca, BP Plastic, OCK, Poh Huat);

• Building material (OKA, Malayan Cement)

• Automotive (UMW, DRB Hicom, MBM Resources)

• Construction (MGB, AME, Gamuda, IJM, Gadang, Kerjaya, Advcon, Suncon)

32

* Bold represents high dividend-yielding stocks (>4%) based on consensus forward earningsInvestment Strategy Potential thematic plays • Fourth cycle of the large-scale solar (LSS4) scheme award and renewable energy plays as Biden to be sworn in as the US President – Cypark, Pestech, Solarvest, Samaiden, Kpower, Boilermech, Greatech, Vsolar. • Rising hard commodity prices and US consumption of precious metal for infra development pursuant to massive fiscal policy – Annjoo, Southern Steel, CSC Steel, Press Metal, Wellcall, Chin Well, Tong Herr. • Water tariffs hike prelude cutting of NRW and pipe replacement, and constructing of water treatment plant in Selangor – Engtex, Hiap Teck, Fitters, HSS Engineering, Salcon, Ranhill, George Kent, Taliworks, KPS. • Potential beneficiaries of the lingering US-China trade war, i.e. EMS, Fastener, Tech, Furniture, palm oil, industrial parks – VS, SKP Resources, ATAIMS, Chin Well, Tong Herr, MPI, Globetronics, Inari, Pentamaster, Vitrox, Poh Huat, Latitude Tree, Lii Hien, Sern Kou, Homeritz, HeveaBoard, Evergreen, Mieco, KLK, IOI, Sime Darby Plantations. • Massive adoptions of E-payment in community & usage of E-solution by the govt. – Iris, Awantec, Revenue, GHL, Datasonic, Censof, HeiTech Padu, DNex, MyEG. • Capitalizing on strong Vietnam growth – Berjaya, HL Industries, Gamuda, SP Setia, Poh Huat, OCK. 33

Thank You

JF APEX SECURITIES BERHAD - DISCLAIMER

Disclaimer: The report is for internal and private circulation only and shall not be reproduced either in part or

otherwise without the prior written consent of JF Apex Securities Berhad. The opinions and information contained

herein are based on available data believed to be reliable. It is not to be construed as an offer, invitation or

solicitation to buy or sell the securities covered by this report.

Opinions, estimates and projections in this report constitute the current judgment of the author. They do not

necessarily reflect the opinion of JF Apex Securities Berhad and are subject to change without notice. JF Apex

Securities Berhad has no obligation to update, modify or amend this report or to otherwise notify a reader thereof in

the event that any matter stated herein, or any opinion, projection, forecast or estimate set forth herein, changes or

subsequently becomes inaccurate.

JF Apex Securities Berhad does not warrant the accuracy of anything stated herein in any manner whatsoever and

no reliance upon such statement by anyone shall give rise to any claim whatsoever against JF Apex Securities

Berhad. JF Apex Securities Berhad may from time to time have an interest in the company mentioned by this report.

This report may not be reproduced, copied or circulated without the prior written approval of JF Apex Securities

Berhad.

34

Equity Market OutlookYou can also read