Leading the Future of Home

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

3/7/2022

Leading the Future of Home

The Affordable Ecosystem

Local Loan Real estate Builders &

It takes many hands to governments officers professionals developers

make home possible.

Partnership and

collaboration across the Mortgage &

Housing

banking

counselors

affordable ecosystem are executives

critical to drive both

business opportunities and

State

making the dream of home Appraisers

governments Housing

Non-profit

a reality for families. finance

organizations

agencies

2

1

3/7/2022

Challenges to Homeownership

Access to a down payment

for a mortgage remains one

of the most common hurdles

for today’s borrower.

13% 26% 24% 40% 42%

of All Buyers of Millennials of Millennials Don’t know down payment Don’t know of low down With housing prices rising,

28 and younger 29 to 38 requirements and… payment programs

incomes remaining stagnant

Saving for down payment most difficult Borrowers lack general down and limited housing stock, it

step in home buying process2 payment knowledge1 creates a highly competitive

market for very-low and low-

income borrowers who

Top Expenses that Delayed Saving for Down Payment2 increasingly struggle to save

for their initial down

50% 50% 37% 17% 13% 17%

payment.

Student Loans Credit Card Car Loan Child Care Health Care Other

Source: 1 2017 Urban Institute Report Barriers to Accessing Homeownership: Down Payment, Credit and Affordability

2 2019 National Association of Realtors Home Buyer and Seller Generational Trends Report

3

HFA Value Proposition

Housing Finance Agencies are easier to work with than ever before!

Competitive Production/Processing

Market Rates in average market

timing

(in most cases)

Down Payment

Assistance

4

2

3/7/2022

HFAs: An Opportunity for 1st Time Homebuyers

• Ideal for borrowers with limited funds for down payment and closing costs and those needing

extra flexibilities on credit and income sources

• Reach more potential homeowners through HFA programs that:

– Provide low down payment options

– Offer preferential pricing

• HFAs offers affordable downpayment and closing cost loans

• An alternative to FHA financing

5

Overview of HFA Advantage®

Mortgage

3

3/7/2022

HFA Advantage® Mortgage

One-unit primary residence High loan- to-value (LTV) Income limits established by the HFA

conventional offering

that’s an excellent

Purchase alternative to FHA Available to first-time homebuyers,

repeat buyers

lending requirements and

Maximum 97% LTV and 105% mortgage premiums.

total loan-to-value (TLTV ratios) Flexible funding options for down

Adopts the requirements payment and closing costs

Loan Product Advisor® of Home Possible® but

with added flexibilities for

HFAs. Flexible MI options available

No reserves required

7

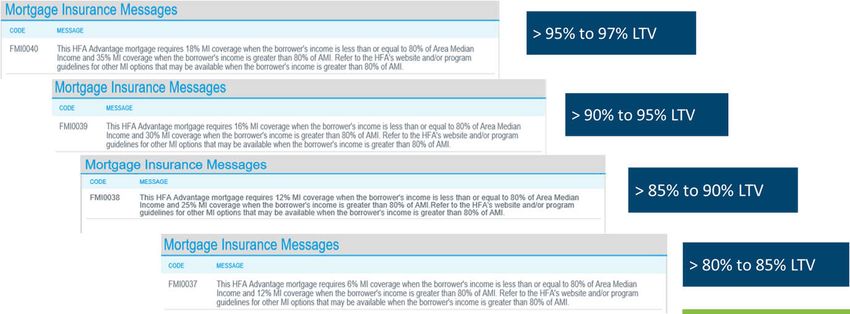

HFA Advantage® Mortgage –

Mortgage Insurance

HFA Advantage Mortgage Standard Mortgage

LTV Ratio Insurance Coverage Insurance Coverage

(Fixed rate only) (Fixed rate, term >20 years)

Greater than 80% up to 85% 6% 12%

Greater than 85% up to 90% 12% 25%

Greater than 90% up to 95% 16% 30%

Greater than 95% up to 97% 18% 35%

8

4

3/7/2022

Why Choose HFA Advantage ® Mortgage

over FHA?

HFA Advantage® FHA

MI ends when LTV < 80% OR MI stays for the life of the loan

Conventional MI: monthly premium OR FHA: Upfront AND monthly premiums

MI only required if the LTV is 80% or higher OR MI required regardless of the LTV

No upfront MIP OR Upfront MIP added to principal AND amortized

WHAT THIS With more funds applied toward the principal up front, an HFA

MEANS: Advantage mortgage with PMI lets the borrower build equity faster

Mortgage Insurance (MI)

9

Freddie Mac Loan Product AdvisorSM

5

3/7/2022

Loan Product Advisor

Select HFA Advantage in the

“Offering Identifier” field within

the “Mortgage Type and Loan

Terms” section of Loan Product

Advisor.

If using a Loan Origination

Software (LOS) system, please

contact them to verify what

field and value to enter. Some

LOS systems may have you

enter “251”.

11

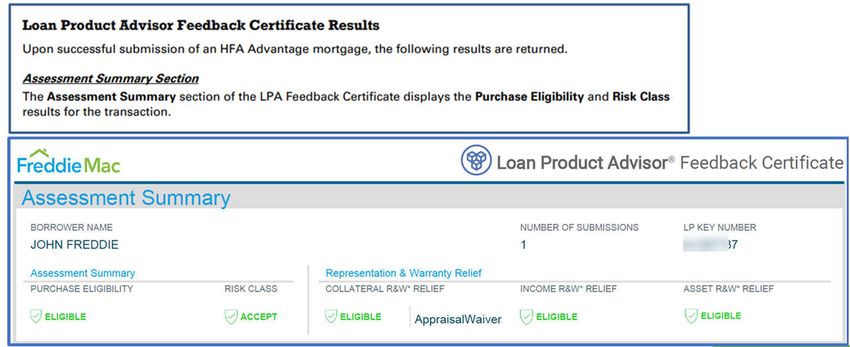

Loan Product Advisor Feedback

Certificate

Verify the loan was

submitted correctly by

ensuring the value entered

in the “Offering Identifier”

field is showing HFA

Advantage. This is found

in the “Mortgage

Information” section of the

Loan Product Advisor

feedback.

12

6

3/7/2022

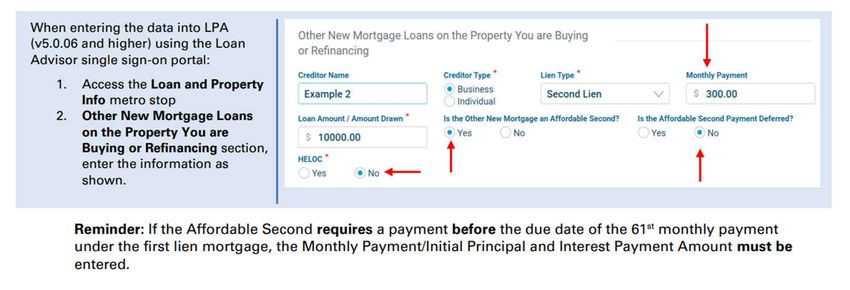

Down Payment Assistance:

Non-Amortizing Subordinate Financing

13

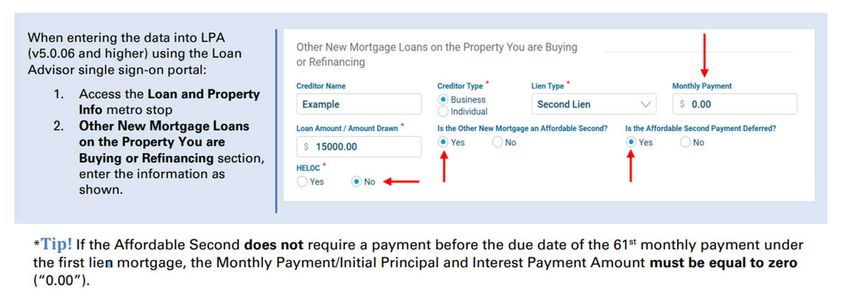

Down Payment Assistance:

Amortizing Subordinate Financing

14

7

3/7/2022

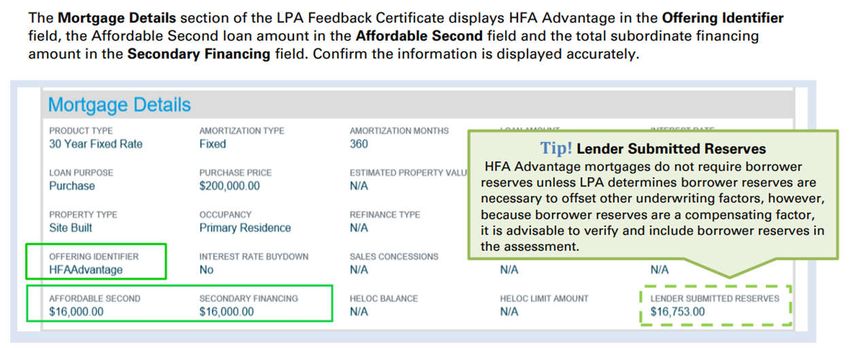

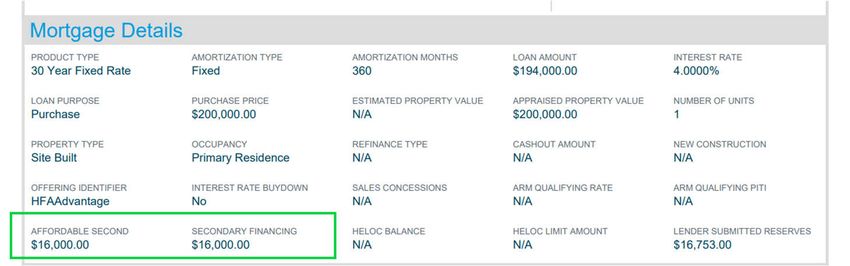

Mortgage Details

15

Purchase eligibility and AUS Risk Class

16

8

3/7/2022

Purchase Restriction Messaging

• Purchase eligibility must be

“Eligible”.

• Ineligible reason messages

will be clearly displayed on

the feedback certificate

17

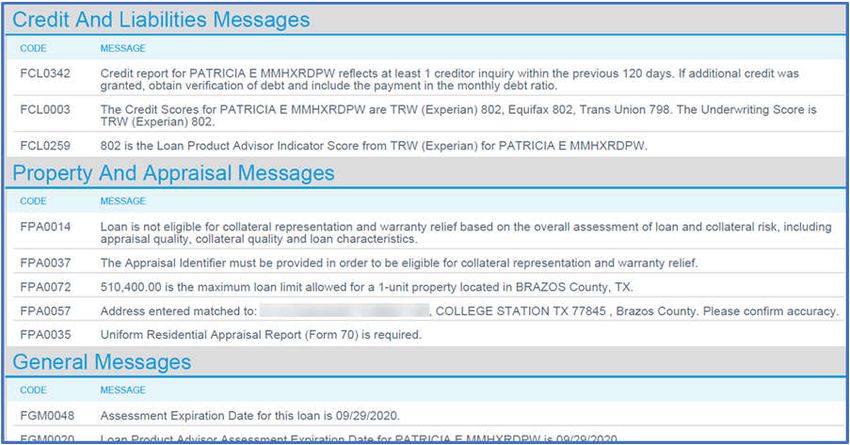

Caution Related Feedback Messaging

18

9

3/7/2022

Qualifying Ratios

19

Loan Product Advisor- Mortgage Details

20

103/7/2022

Loan Product Advisor Feedback

Certificate

21

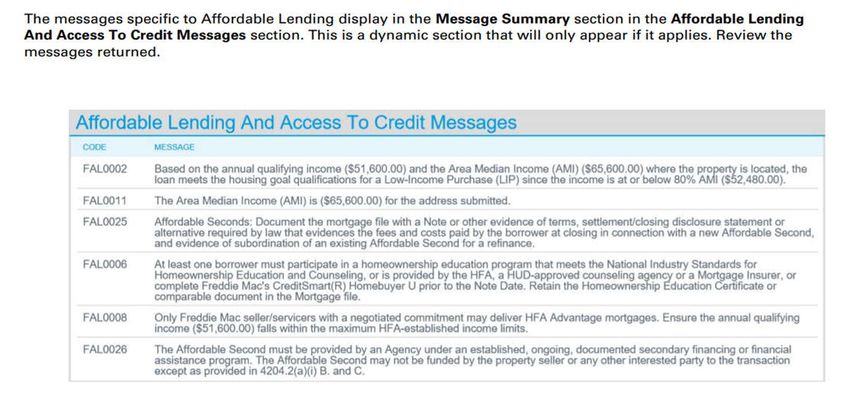

Message Summary

22

113/7/2022

MI Specific Messaging

23

800-FREDDIE

Specialists trained in HFA Advantage

Review individual loan scenarios

Assist with LPA Feedback

24

123/7/2022

YOU Are the Critical Link

• YOU are the critical link to helping well • Homebuyer dream realized—and more

qualified homebuyers achieve their business for you—if you know your market

homeownership objectives: and where to find those affordability gap

– Provide access to credit; originate loans to the full solutions

extent of Freddie Mac’s credit box

– Utilize your mortgage finance expertise

– Explain the process and dispel the 20% down

payment myth

– Identify and match available financial resources in

your area (government, nonprofit, private

sources) with a sustainable mortgage solution

– Take advantage of Freddie Mac training and

resources for yourself and your borrower Freddie Mac is here to help!

25

13You can also read