KIMs IPO - Everything you need to know! - JST Investments

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

KIMs IPO – Everything you need to know!

Krishna Medical Institute of Medical Sciences or KIMS Ltd is a multidisciplinary integrated healthcare

services company in Tier 1, 2 and 3 cities, operating nine multi-specialty hospitals under the “KIMS

Hospitals” brand, with an aggregate bed capacity of 3,064 beds including over 2,500 operational beds with

utmost financial prudence. Their key specialities include cardiac sciences, oncology, neurosciences, gastric

sciences, orthopaedics, organ transplantation, renal sciences and mother and child care.

They enjoy a dominant position in AP and Telangana in terms of number of patients treated and treatments

offered, which are 2.2 times more beds than the 2nd largest provider in AP and Telangana.

About Offer:

Issue Size- 2145crs

New Issue- 200crs (will be used to pay off debt)

Offer for sale (Promoters selling out)- 1945crs

Price Band- 815-825 /share

Market lots- 18 shares

Market Capitalisation- 6600crs at upper band.

IPO dates- 16 to 18th June, 2021

Business Overview:

External growth drivers:

1. Increasing Population: 1.5B by 2030

2. Increasing Urbanisation: From 35% in 2020 to 40% in 2030

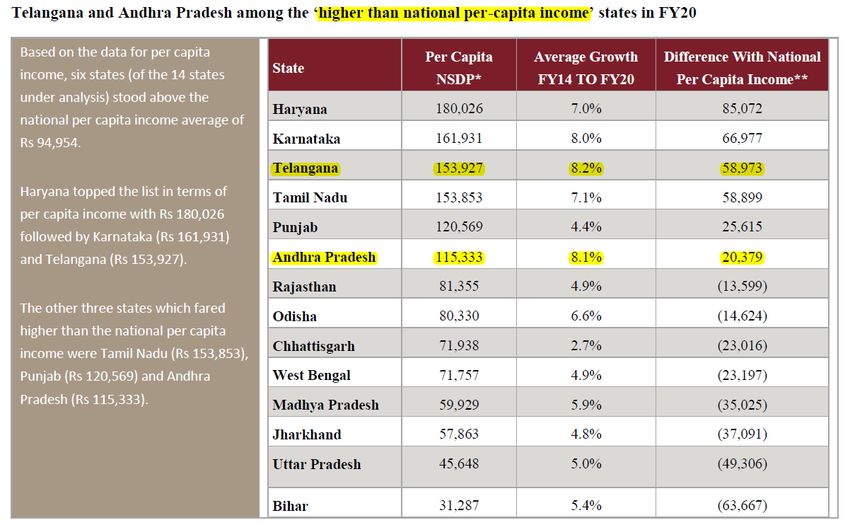

3. Telangana & AP having higher than national GDP per capita, also being the states with the fastest

growth (2x the GDP of India)

www.jstinvestments.com

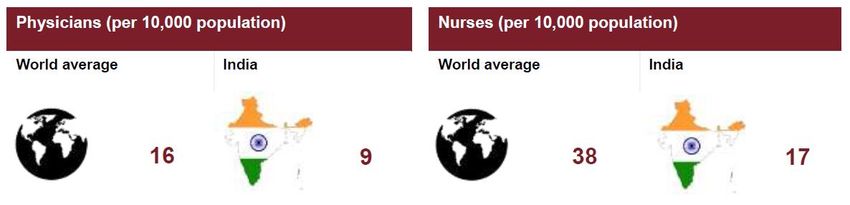

4. No. of beds, physicians & nurses per 10,000 people lag the global median; there’s much room for

improvement.

5. Conducive government policies leading to greater affordability & better quality of services.

6. Increased Health Insurance coverage.

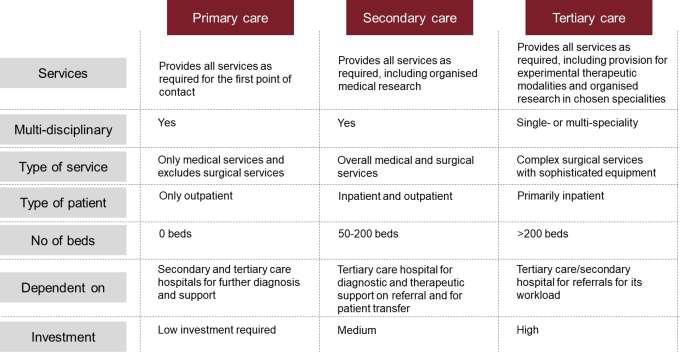

Hospitals are of 3 types & complexity of what they can deal with increases from Primary to Tertiary. All

Hospitals of KIMs are Tertiary care.

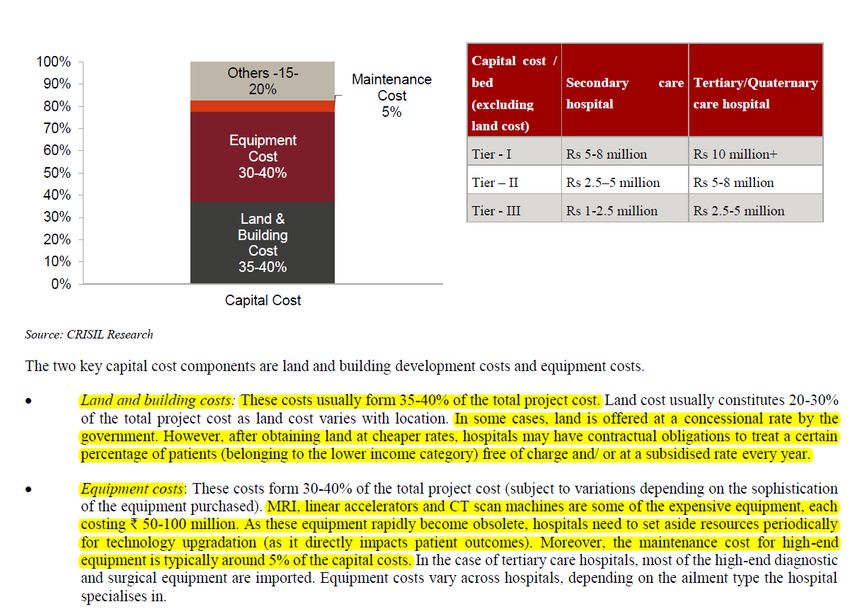

Did you know: Why is a hospital bed more expensive than a 5-star hotel? Capital cost for opening a

hospital can be more than 1cr/bed.

www.jstinvestments.com

Strengths:

1. Volume driven model of healthcare like that of KIMs stand to relatively weather the COVID crisis

better.

2. Key advantages of having a strong regional presence.

www.jstinvestments.com

3. Among the Top 1% of hospitals in terms of financial prudence: rated ‘AA’ by CRISIL.

4. Scale up from 250 beds in 2000 to 3000 beds currently has been phenomenal, acquiring 4 hospitals

in the last 5 years & turning them around. The management wishes to grow at the 20%+ cagr for the

decade to come.

5. Demand looks to be higher than supply & the management is capitalising on that.

1. Approximately one-third of the 3,064 beds were launched in the last four years. They have

added over 940 beds, in aggregate, in their hospitals in Visakhapatnam (Vizag) (AP),

Anantapur (AP), Rajahmundry (AP) and Kurnool (AP) in Fiscal Years 2019 and 2021, and

improved the overall bed occupancy rate in these hospitals from 71.83% to 78.60% in

the same period.

www.jstinvestments.com

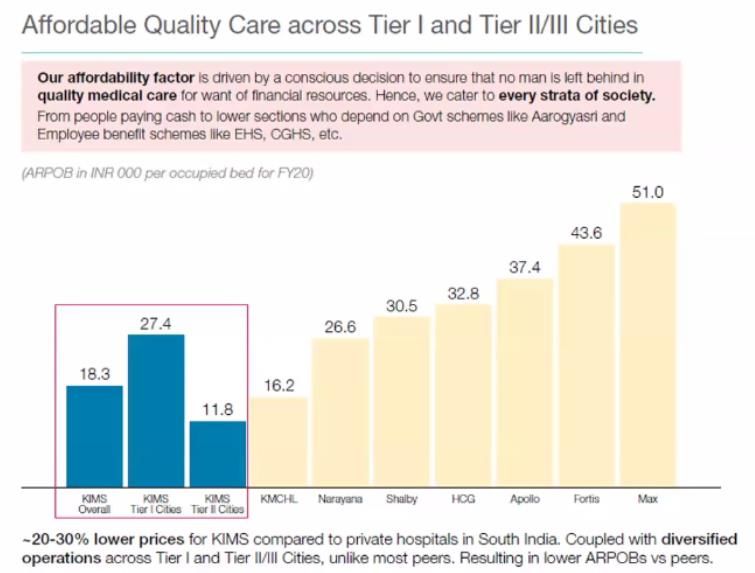

6. Disciplined with capital allocation which in turn drives affordable pricing.

1. Capex per bed was ₹ 6.35 million for hospitals in Tier 1 cities and ₹ 2.21 million for

hospitals in Tier 2-3 cities, compared to the industry average of ₹ 5-8 million in Tier 1

cities and ₹ 1-5 million in Tier 2-3 cities.

2. ARPP (Average rev per patient) is ₹ 79,526, which is 41% lower than the industry

average of ₹ 112,000

7. Revenue is diversified across the specialities.

1. In Fiscal Year 2021, total income mix was 17.82% from cardiac sciences, 12.55%

from neuro sciences, 9.30% from renal sciences, 4.64% from orthopaedics, 5.25%

from gastric sciences, 5.71% from oncology, 6.11% from mother & child care, 1.86%

from organ transplant, 35.28% from other specialties and 1.48% from other income.

8. Collaboration with medical institutions.

1. It allows them access to a talent pool of doctors from their DNB student programs

and nursing staff through affiliations with in-house nursing schools and colleges.

2. The employees' growth (including doctors) have been consistent.

www.jstinvestments.com

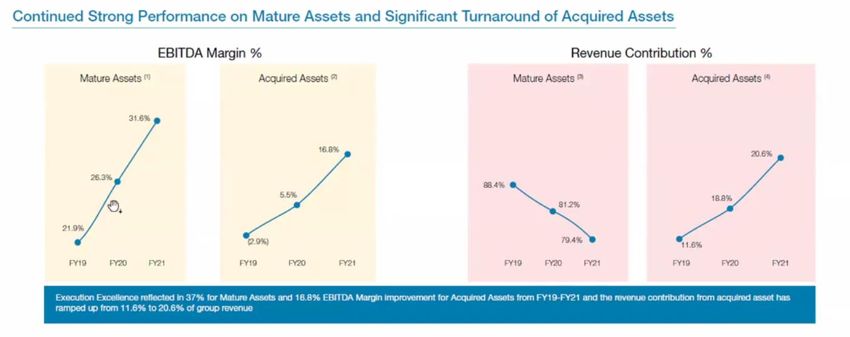

9. Ability to turn around loss making hospitals has been commendable, as of 2021, each & every one

of their hospitals is making EBITDA breakeven with superb occupancy rates; the sustainability of this must

be tracked.

10. Doctors have equity participation in the company; owning 7% of the company that’s going to be

listed & various other percentages in the subsidiaries.

www.jstinvestments.com

Where does the rev come from?

Still 55-60% of the total revenues is out of pocket & only 16% through insurance.

Government scheme proportion varies between 20-30%. The government dues can take a bit

longer to come, however, the payment is made in full.

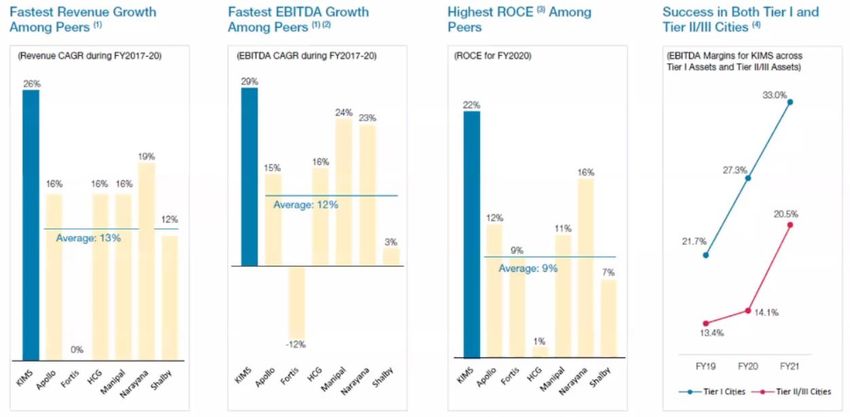

Competitive Scenario: Among the fastest growing & most efficient users of capital.

www.jstinvestments.com

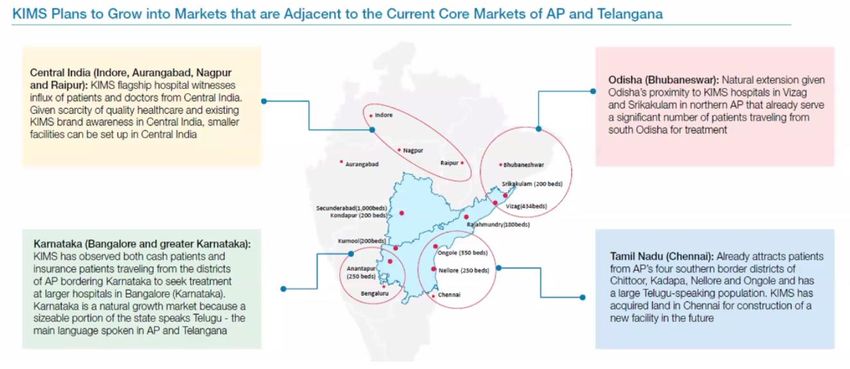

Growth Strategy: In the short to medium term, additional capacities in AP & Telangana will drive growth.

Much later into the future (5+ years), capex from other states (Chennai & Bengaluru) should start yielding

dividends.

www.jstinvestments.com

Custodians of your capital aka. Management: Spearheaded by Dr. Bhaskara Rao Bollineni is a

renowned cardiothoracic surgeon in India. He has over 27 years of experience in cardiothoracic surgery

and has worked in several other leading medical institutions in the country.

Under his leadership, and that of Dr. Abhinay Bollineni, who joined KIMS in 2014, they have expanded into

nine cities across AP and Telangana through a combination of greenfield, brownfield and acquisition-led

expansion with a high rate of success. (No succession issues)

Shareholding before & after the IPO:

Promoters stake decreases from 47% to 39%

The largest shareholder PE investor General Atlantic halves its stake from 40% to 20%.

www.jstinvestments.com

Risks:

1. They are highly dependent on their healthcare professionals, including doctors that we engage on a

consultancy basis. Wages increases could lead to a hit in the margins.

1. The attrition rate for their healthcare professionals, which includes resident doctors

(including DNB students), consultant doctors, nursing staff (including interns) and

paramedical personnel, for Fiscal Years 2019, 2020 and 2021 was 39.7%, 39.0%

and 51.6%, respectively. [Need to be tracked going forward.]

1. The higher attrition rate is attributed to the huge proportion of nursing staff &

temporary hires in CY20 to cater to COVID.

2. Interesting caveat: Since inception in 2000, they have retained over 80% of

their doctors.

3. The ability to attract medical personnel & retain them is the key.

2. COVID related disruptions: Delay in elective surgeries, increased cost to provide for the continuity of

operations & subdued medical tourism.

1. The COVID waves have been under control in the states the company operates in.

www.jstinvestments.com3. High dependence (~65% of rev) to the hospitals in Hyderabad, Telangana: Any political unrest could

be a risk to watch out for.

4. Hospitals at Vizag (AP), Kondapur (Telangana) and Nellore (AP) (partially leased) are situated on

land that is leased on a non-perpetual basis with terms ranging from 2yrs- 30yrs: Any adverse impact on

the title or ownership rights of the owner or breach of the terms or nonrenewal of the license agreement

may lead to disruptions.

5. Commodity business for the most part: They face intense competition from other healthcare service

providers like Apollo, Fortis, Healthcare Global, etc.

6. Keeping pace with technological changes, new equipment and service introductions, changes in

patients' needs and evolving industry standards is a must.

1. Repairs and maintenance of medical equipment is a substantial cost every year

ranging from 20-25crs.

7. M&A activity has been high since the last 5 years: Acquired 4 hospitals since FY2016.

8. Litigations & contingent liabilities are not very high even though we need to track their progress.

www.jstinvestments.com9. Any unexpected price increases in key Raw material which is medical consumables: For Fiscal

Years 2021, 2020 and 2019, purchase of medical consumables, drugs and surgical instruments (net of

(increase)/decrease in inventories of medical consumables, drugs and surgical instruments) represented

21.56%, 22.52% and 22.75% of their total income, respectively.

10. Health Insurance penetration does not catch up in India.

www.jstinvestments.comFinancials:

Balance Sheet:

Goodwill, Intangibles & Trade receivables are under control.

Approximately 200crs of debt which will be paid off using IPO proceeds.

www.jstinvestments.comProfit & Loss:

Growing revenues & margins: According to management, the margins will remain stable due to

higher growth in high value surgeries like Heart & Lung Transplant. [Needs to be tracked]

FY19 was an anomaly due to 87.1cr non cash Loss on fair value changes in financial instruments.

EPS before the Issue: After the issue, the PE would be nearly 30.

www.jstinvestments.comCash Flow Statement:

Strong Cash Flows with Positive FCF of 250+crs in FY21.

Efficient Working capital days of less than 10.

Dividend Policy: So far FCF has been reinvested for growth capex, going forward dividends will be

issued as per the future growth plans.

www.jstinvestments.comValuations:

Most of the other competitors took a hit on the EBITDA margins this year due to lower sales.

Valuations seem reasonable given the financial metrics & return ratios.

Conclusion:

With planned capex of 1000 beds, Industry leading occupancy rates of 80%, growth in revenues & margins,

spearheaded by Dr. Bhaskara Rao Bollineni, a renowned cardiothoracic surgeon & finally being available at

reasonable valuations makes us interested in the company for the long term. However, we would like to

monitor a few deliverables before taking up a position in this company.

Thanks for reading till the end! If you would like to add anything or give any feedback or would like to

appreciate the article, reach out to me on twitter – @AnishA_Moonka or email me at

anish.moonka@jstinvestments.com!

www.jstinvestments.comYou can also read