Indian Association of Investment Professionals Indian Institute of Management, Bangalore - CFA Institute Research Challenge

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CFA Institute Research Challenge

Hosted by

Indian Association of Investment Professionals

Indian Institute of Management, Bangalore

Thyrocare Technologies (Thyrocare) is one of the

leading pan India diagnostic chains. It focusses

more on disorder rather than the disease. The

company currently offers 198 tests and 59

profiles of tests across 4 different segments. As

such, the company has a nation-wide

distribution network of 1041 authorized service

providers across 566 cities and 24 states.

Diagnostics industry in India is expected to grow

at ~14-16% to reach INR 650Bn by FY19.

Wellness and preventive healthcare sub-

segment posits even higher growth rate. Off-

late, Thyrocare has started offering these

wellness tests which is one of the highly

profitable segment.

Investment Thesis: The factors making

Thyrocare stock an investment buy include (1)

cost advantage offering unique differentiation,

Source: Bloomberg, NSE Website

(2) unique nation-wide distribution fueling more

growth, (3) asset-light model enables faster

revenue growth rate, and (4) high growth rate

opportunity in diagnostics and wellness and

preventive care segment, and (5) strong

operating and financial metrics with reasonable

valuation make it an attractive buy.

Valuation: We evaluate Thyrocare using the

intrinsic (DCF with two-stage model) and the

relative valuation (trading multiple approach)

Source: Bloomberg methods. The share price is expected to lie

between the INR 555 to INR 888 depending on

the three different scenarios (bear, base and

bull) and the trading multiples. Overall, we give

the buy recommendation with the target price of

INR 702 in the next 12 months.

Risks: can be categorized into business risk and

financial risk. Major risks include (1)

technological disruption, (2) concentration risk,

(3) extensive regulatory compliance, (4)

Source: Team Estimates, Annual Report vendors/suppliers risk, and (5) INR depreciation.

Investment Summary

Cost advantage offering unique differentiation: Comparing w.r.t to its main competitor, we estimate

Thyrocare to have significant cost advantage on its major consumables (chemicals, reagents, etc.) to the

tune of ~20% cheaper than that of Dr. Lal Path Lab. Additionally, with the high annual volume turnover of

61.5mn tests (vs. 21.8mn of Dr. Lal Path Lab), we believe this cost efficiency will remain sustainable and

offer superior margins (as reflected in higher EBITDA margins of ~40% vs ~26% for Dr. Lal Path Lab).

Unique nation-wide distribution fueling more growth: With the facility of 6 RPLs and 1 CPL, served by its

network of 1,041 ASPs across 566 cities and 24 states, Thyrocare has created its pan India presence.

Additionally, management intends to add 19 more RPLs and 1 CPL in the next 5 years to establish full-

fledged end-to-end distribution system, thereby making this network difficult to be replicated. This will

not only increase the customer base and thereby the higher sampling volumes, it will also help in creating

the trust for the long-term.

The efficient logistic capabilities and the IT infrastructure (barcoding process), in sync with the followed

hub-and-spoke model, will further increase the customer reach and improve the turnaround time. This

cost efficiency will enable Thyrocare to offer more affordable rates to the customers and hence will

further increase the number of samples and the revenue.

Asset-light model enables faster revenue growth rate: The high tests volume commitment and the strong

supplier relationship enables Thyrocare to pursue the asset-light model i.e. the leasing model for its

expensive equipment (from suppliers like Siemens). This reduces majority of their fixed costs (typical of

diagnostic equipment), align costs more closely with the actual demand and thereby offers higher revenue

growth rate (26% for Thyrocare vs. 20% for Dr. Lal Path). Overall, we believe, this business model will

enable management’s vision of expanding RPL and possibly CPL aggressively without much capital outlay

while keeping key financial metrics (such as ROA) at higher levels.

High growth rate opportunity in diagnostics and wellness and preventive care segment: Owing to the

increasing lifestyle-related diseases, rising urbanization, growing disposable income, and increasing

penetration of healthcare services and insurance packages, diagnostics industry posits a growth rate of

14-16% CAGR for the next 2 years to the market size of INR 650 billion.

A sub-sector, wellness and preventive care segment, presents a significant growth opportunity given it

contributed to ~46% of Thyrocare’s FY16 revenues with just ~20% of the total volumes. Given this segment

is merely 6-8% of the total FY16 diagnostics market, it has the potential to grow at 25-30% CAGR (over

next 3 years) to attain the penetration of 7-9% of the total FY18 diagnostics market especially when the

Wellness and Preventive segment will grow at a

higher rate than the diagnostics industry

INR 512 Bn INR 650 Bn

Source: Thyrocare RHP

Source: Thyrocare RHP

penetration is over 50% in the developed markets.

Increased diversification via developing NHL’s network and expanding service platform: Besides

diagnostics, Thyrocare is increasing the breadth of its services that leverage its network and the

established brand by offering molecular imaging services and establishing Thyrocare Metabolic Clinic

(TMC). Nueclear (NHL) intends to expand its services via the franchisee model and the affordable

competitive pricing. Similarly, a new stream of revenues is envisioned with TMC while providing doctors

and chronic-illness patients a metabolic clinic platform. These new services are likely to augur well for the

company’s growth plan and offer revenue stability/diversification.

Strong operating and financial metrics with reasonable valuation make it an attractive buy: Thyrocare

has achieved income from operations growth of 21.2% CAGR over FY12-16 with significantly high EBITDA

margins of ~40% during this period. Even the net profit has grown at a CAGR of 13.2% during the same

period. From stakeholders’ perspective, Thyrocare has achieved higher asset utilization (ROA of 20%) and

ROE of more than 20% for the last 5 years and more importantly, has the financial leverage for future

growth as it is a debt free company with a cash balance of ~INR 750mn.

Business Description

Established in 1996 by Mr. A Velumani, Thyrocare was initially focused on thyroid testing. The company

later shifted to offer a variety of tests and now it offers 198 tests and 59 profiles of tests. Thyrocare

focusses more on disorder which involve repetitive tests rather than disease which involve one-time tests.

It is one of the leading pan India diagnostic chain and has 4 brands [Exhibit 1]:

Thyrocare - offers diagnostic testing for metabolic disorders and thyroid, which accounts for 70%

volume of samples and 20% of revenue

Aarogyam - offers services catering to wellness & preventive healthcare, contributing ~46% to

company’s revenue. It offers seven test profile covering tests for chronic disorders. [Exhibit 2]

Nueclear, as wholly owned subsidiary Nueclear Healthcare (NHL), provides imaging services for

early and effective cancer monitoring. It has 5 operating PET-CT scanners in 3 imaging centers- 2

in Navi Mumbai, 2 in New Delhi and 1 in Hyderabad.

Whaters - offers services including testing of varied parameters in water.

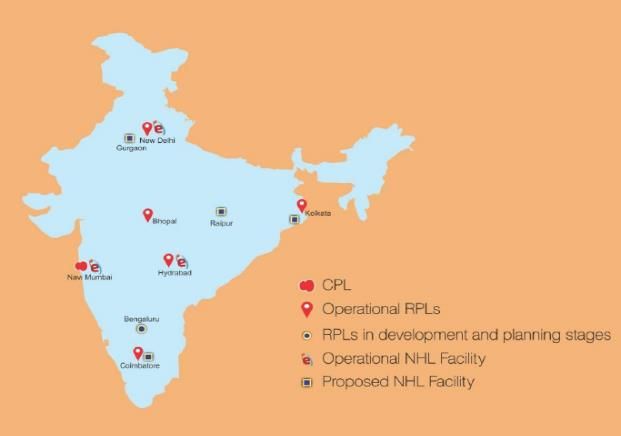

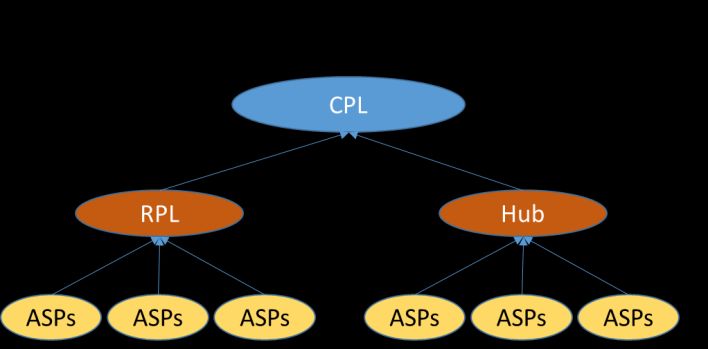

The company operates on hub and spoke

model with a fully automated CPL (Central

processing lab - bar coding and bi-directional

laboratory information system) located in

Navi-Mumbai which has capacity to process

180mn samples per year. It also has 6 RPLs

(Regional processing lab) located in New

Delhi, Bhopal, Kolkata, Hyderabad,

Coimbatore and Bengaluru [Exhibit 3]. RPLs

primarily offer routine tests conducive to high

Source: Team Research

volume testing while CPL offers entire range

of tests. The strategic locations of RPLs help in

processing specimen from remote location thereby increasing sample volumes.

The samples to be processed are collected by a network of 1041 authorized service providers (ASPs)

spread across 566 cities. These ASPs collect samples from local hospitals, laboratories, doctors and also

from patients procured by direct sales associate or referred to them by doctors. ASPs either deliver

samples directly to one of the RPLs or, if the sample is to be processed at the CPL, to one of 22 hub

locations [Exhibit 3], where samples are aggregated and transported directly to the CPL. The

transportation is mainly done by air cargo. Based on the bar code on the sample, it is automatically

processed for the respective tests at the CPL and the reports are thereby generated automatically and

uploaded on the website or posted to the users as required.

Industry Overview and Competitive Positioning

The Indian diagnostic industry is valued at INR 512 billion as of 2016-17 with the growth drivers being

increase in evidence-based treatment, high literacy rates, increasing health awareness and disposable

incomes rise, expanding health insurance coverage, rising urbanization, changing demographics and the

increase in life-related diseases [Exhibit 4]. The industry is expected to grow at a CAGR of 14-16% over the

next two years to over ~ INR 650 billion by FY19.

Increasing disposable incomes (INR tn) coupled Expected increase in death due to chronic diseases

with... will lead to increase in the diagnostics tests

81 32%

72 29% 29% 29% 29% 29%

24% 25%

60 19%

52

45 8%

37 5% 6%

33

26 29

21 24

Communicable Other Cancer Cardiovascular

diseases Non-communicable diseases

diseases

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2012 2015 2030

Source: Team Research

The industry comprises of two parts [Exhibit 5] – Pathology and Imaging. Pathology testing involves

diagnostics on collected samples (in the form of blood, urine) and imaging/radiology involves procedures

such as taking X-ray, CT-scan and ultrasound reports. Pathology testing being volume driven commands

57% market share while Imaging business commands 43%. Biochemistry driven by pathology chronic

disease like diabetes/sugar, cardiovascular forms a major part of Pathology testing.

Characteristics of the Diagnostics industry:

Highly fragmented and unorganized – The

diagnostic market consists of 3 types of players -

unorganized standalone centers, unorganized

hospital based centers and organized diagnostic

chains with relative size as depicted in figure.

Out of the diagnostic chains, 35-40% are pan

India chains and rest are smaller regional chains.

The share of diagnostic chains is expected to

increase to 20% by 2018-19 at a robust CAGR of

30-32% over the next three years.

Lack of comprehensive and stringent regulatory

framework- With only 3 to 4 major regulations

governing the industry, it is far under-regulated

as compared to the pharmaceuticals and

Source: Thyrocare RHP

hospitals industry [Exhibit 6].

Intensely competitive - Diagnostic chains face stiff competition in two forms - the captive patients catered

to by hospital-based diagnostic centers and local brand name/commission tie-ups of standalone centers.

Since the nature of the tests is the same, the key differentiator across major diagnostic players lies with

strong doctor referral network, expanded customer reach and enhanced service offerings. These offerings

are in the form of reduced turnaround time by robust logistics network, consistently high quality and

accuracy of tests produced and automated IT systems facilitating easy availability of reports.

Porter’s five forces analysis – signifying diagnostics industry is extremely competitive

The five forces Score Rationale

Bargaining power Medium Large chains have higher bargaining power, allowing them to

of suppliers keep their input costs (bulk purchase of reagents) lower than

standalone centers

Threat of Low Substitutes like point of care testing are too far-fetched in future,

substitutes thus low immediate threat from substitutes

Bargaining power High Extremely fragmented and competitive market leading to higher

of customers price sensitivity among customer

Threat of new High Lack of regulatory framework and lease-based asset light model

entrants make industry more attractive new players

Industry Rivalry Medium Due to undifferentiated offerings but smaller size of fragmented

players, industry rivalry exists among pan India chains

1Source: Team Research

Brand based commission structure - Revenue in this industry is largely dependent on doctor referrals (50-

60%) and walk-ins (30-35%). Standalone centers and smaller regional chains offer much higher

commission margin towards doctor referrals (as high as 30-40%) while the diagnostic chains can afford to

offer lower commissions (15-20%) owing to a strong brand name.

Large proportion of the costs are fixed- About 55-60% of total costs (including lease rentals- 20-25%,

employee- 20-25%, power fuel and maintenance costs- 1-3%) are largely fixed. Consumables (25-30%)

include cost of reagents while selling expenses (4-8%) include the costs of advertisement, publicity and

commission given to the franchise.

Cash rich business- Revenue model works on the concept of advance payment collection resulting in a

significant fund flow, zero debt and cash profit generation.

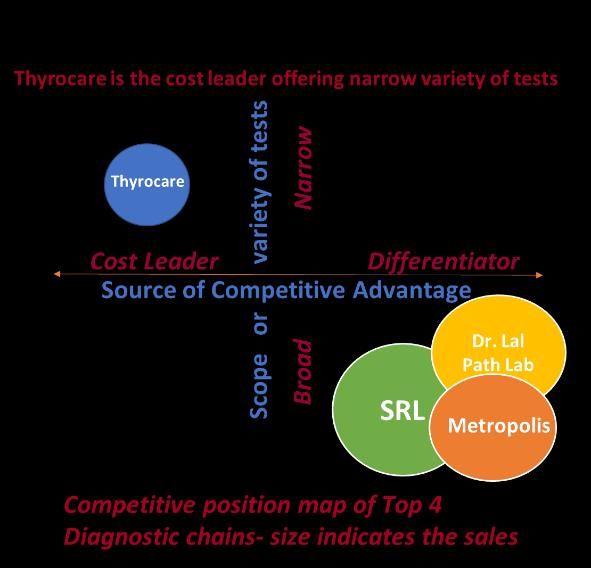

Amongst these characteristics, Thyrocare stands out

amongst its competitors as follows:

Cost leader- Thyrocare as a unique organization, serves its

clients at the lowest rates in the industry. Thyrocare’ s B2B

focus coupled with a central laboratory for regional labs and

price disruption helped Thyrocare in getting high volumes.

High volumes coupled with automated large scale labs make

the company a cost leader.

Unique business model & CPL focused operations – CPL

processes 0.2mn tests a day-highest by any lab in India and

hence bring in operational efficiencies. Complete

automated process leads to faster turnaround time of

Omni Chanel presence - Online client system, branded Thyroid metabolic clinic- Company has

introduced online client system where persons or organizations with ability to collect samples can

outsource the testing to Thyrocare. Further, company is planning to introduce Thyroid metabolic clinic

(TMC) which will be a nation-wide chain of branded metabolic clinics for individuals with chronic illness

or who plan to undergo healthcare procedure. These clinics will provide platform for doctors to deliver

their expertise to potential patients.

Well-knit network driving volumes which can’t be easily replicated- The only moat which can’t be

replicated is volume of samples. Pan India deep network of ASPs with large scale labs is a model which

drives volumes. Further, Thyrocare’ s RPL strategy is in right direction which will help in cutting logistics

costs and thus help keeping up with pricing pressure in future. This will lead to sustained revenue growth

though margins may be sacrificed in future.

Asset Light Model - Due to the leasing of equipment and analyzers from vendors, the company follows an

asset light model. As a result of this, the company does not have any long and short-term borrowings. The

company generates enough cash for funding its expansion plans in the near future. This leaves a lot of

room for Thyrocare to leverage its balance sheet for future expansion.

Valuation

The valuation has been evaluated using a combination of intrinsic and relative valuation methods namely

– DCF with a two stage model, and the trading multiple approach of comparable companies. We also

looked for the past transaction multiples, but with hardly one deal in the recent past, that valuation

method is not reliable. To get a better visibility, we have analyzed 3 different scenarios in the DCF model

– downside case, base case and the management case. Shown below are the share prices varying from

INR 555 to INR 888 as calculated using the different methodologies. But overall, we believe the base case

is more likely and hence the stock price of INR 702 is our recommendable target for the next 12 months.

FY17 P/E 695 772

FY17 EV/EBITDA 801 888

DCF 555 866

Source: Team Estimates, Bloomberg, Company Reports, Broker Research

Discounted Cash Flow (DCF) Method: In order to assess the different market conditions, we developed

the detailed financial model and simulated 3 different scenarios namely – downside, base and

management cases. These 3 scenarios differ in the growth rates [Exhibit 7] in the two-stage discounted

cash flow model with management case as the most bullish and the downside case as the bearish. With

the below mentioned assumptions, we get the following target stock price: INR 555 (downside case), INR

702 (base case) and INR 866 (management case). For detailed valuation model, please refer [Exhibit 9].

However, we believe base case of INR 702 is the most likely achievable target in the next 12 months.

Assumptions

Revenue Growth Rate: Since the firm witnessed a high revenue growth rate of 32% in FY16, a two stage

model wherein this rate is expected to fall down marginally is justified. In this model, for the first five

years (FY17-FY21), Thyrocare is expected to experience high growth stage, growing at a rate of 27% YoY

followed by the second stage of medium growth phase with 24% revenue growth during FY22-FY26. Post

the horizon period, Thyrocare is assumed to grow at a perpetual growth rate of 5%.

The revenue for the imaging business and the other businesses are estimated separately as they have a

different growth profile compared to the diagnostics segment. And this growth rate is assumed to be

different in different scenarios. For the imaging business, the revenue is estimated to grow at 30% YoY in

our base case scenario.

EBITDA Margin: For the diagnostics business, it is assumed to decline slowly as the competition kicks in,

leading to decrease in prices for the various tests. At the same time, EBITDA margins for the imaging

business is expected to improve with better utilization of the existing machines. Overall, the firm wide

EBITDA margin is at 40% and is assumed to stabilize at 37% by the end of 10-year horizon period.

Fixed Assets: The assets are estimated assuming that the fixed asset turnover ratio will be stable as the

firm would require to increase the asset base at a similar pace as the revenue is growing. At the same

time, we have used the management’s capital expenditure estimates for the next 5 years. They expect to

operate around 25 RPLs by end of 2020, along with imaging centers deploying 5 PET-CT scan machines

and 1 cyclotron. Since the company is expected to operate on a franchisee model for the PET-CT scan

machines, we assume a lesser capital cost and consequently lower revenue due to the revenue sharing

model with the franchisees. For the next 5 years, we have assumed creation of 3 RPLs every year at a per

unit cost of INR35mn, an INR300mn investment in FY19 for establishing a CPL in Delhi, INR60mn each for

PET-CT scan in FY18, FY20 and FY22.

Cost of Equity: With limited trading history of Thyrocare stock, we have assumed the beta of 1. As such,

its peer, Dr. Lal Path Lab trades at a beta of 0.55. Overall, we estimate the cost of equity for the company

to be 13%.

Sensitivity Analysis- To understand more about the stock price variance, we have performed the

sensitivity analysis by varying the terminal growth rate (from 4% to 5%) and the WACC (from 12% to 14%).

The detailed results can be seen below:

Downside Case: Base Case: Management Case:

Stock Price (INR) Stock Price (INR) Stock Price (INR)

Terminal Growth Rate Terminal Growth Rate Terminal Growth Rate

28,587 4.0% 4.5% 5.0% 5.5% 6.0% 36,166 4.0% 4.5% 5.0% 5.5% 6.0% 44,629 4.0% 4.5% 5.0% 5.5% 6.0%

12.0% 594 621 652 688 730 12.0% 753 789 830 876 931 12.0% 931 976 1,028 1,087 1,157

12.5% 551 574 600 630 664 12.5% 697 727 761 800 846 12.5% 859 898 941 991 1,049

WACC

WACC

WACC

13.0% 513 533 555 580 608 13.0% 647 673 702 735 773 13.0% 797 830 866 908 956

13.5% 480 497 515 536 560 13.5% 603 626 650 678 710 13.5% 741 769 801 836 877

14.0% 450 464 480 498 519 14.0% 564 583 605 628 655 14.0% 692 716 743 773 807

Comparable Company Analysis - In the organized diagnostics space in India, there are hardly few major

players namely - Dr. Lal Path Lab, SRL Diagnostics, Metropolis Healthcare, Thyrocare Technologies.

However, only Dr. Lal Path Lab is the other listed entity besides the recent listing of Thyrocare. For

comparison, we have shown below the key financial and operating metrics comparing Thyrocare with Dr.

Lal Path Lab.

2017E

Mcap Revenue Revenue EBITDA Net Net D/ EV/

Company ROE P/E

(INR mn) (INR mn) Growth Margin D/E EBITDA EBITDA

Thyrocare 34,015 2,312 26.4% 39.3% 16.0% (0.3x) (1.2x) 28.7x 48.3x

Dr Lal Path 98,787 7,913 20.0% 26.5% 31.2% (0.6x) (1.4x) 37.7x 61.0x

Source: Bloomberg, Company Reports, Broker Research

Based on the 2017 EV/EBITDA and P/E trading multiple of Dr. Lal Path Lab, Thyrocare technologies can be

valued at share price of INR 865 and INR 754 respectively. Despite giving a market discount of 10%, share

price comes out to be INR 781 and INR 678 by the comparable EV/EBITDA and P/E multiples respectively.Financial Analysis

Revenue - Thyrocare witnessed a healthy growth of 31.7% in revenue with INR 2409.65 million in FY 16

as compared to INR 1829.58 million in FY 15. The increase in the revenue is mainly on account of the

increased focus on preventive care offerings, increase in turnaround time due to setting up of more

regional processing laboratories and also increase in the number of CT scans conducted by the imaging

business. The growth in the industry is mainly volume growth as Thyrocare conducted 61.5mn

investigations and 11.5mn tests in FY 16. A snapshot of the financial performance on a standalone basis

is shown in the table below

Financial Performance

2,500 45% 47% 46% 2,351 50%

42% 41%

2,000 1,801 40% 40%

32% 31%

1,500 1,343 1,500 27% 30%

1,091 25%

1,000 946 20%

636 690 735

491 566 588

458 487

500 350 10%

0 0%

FY 12 FY 13 FY 14 FY 15 FY 16

Revenue from ops (INR mn) EBITDA (INR mn) PAT (INR mn)

EBITDA Margin (%) PAT Margin (%)

Source: Company Annual Report

Consistent margins of > 40% EBITDA, >25% PAT for the last 5 years. This growth was volume driven as is

evident from the 20.6% CAGR growth in samples processed from FY 12 to FY 16.

EXPENSES (% OF REVENUE) Expense Analysis

1. Cost of materials consumed – This has shown

mostly a stable trend as percentage of revenue, except

21% 22% in FY 15 where the rupee depreciation increased the cost

22% 20% 18%

10% to a greater extent.

7% 7% 8% 11%

2. Employee benefit Expense – This has increased

27% 27% 28% 31% 27% in FY 16 primarily due to introduction of employee stock

options and increase in the number of employees

FY 12 FY 13 FY 14 FY 15 FY 16

Cost of material Employee benefit expense Other expense 3. Other Expense – This has increased more in

recent years due to the increasing service charges to the

authorized service providers.

Lesser Capital Costs- The business model of Thyrocare involves leasing of diagnostic equipment and

instrument from vendors like Siemens, Trans Asia Bio Medicals Limited with a contractual agreement to

purchase reagents and consumables from them for periods ranging from 2 to 6 years. While this reduces

the capital costs associated with the equipment but at the same time it increases the liability for Thyrocare

as it has to purchase reagents from the same vendors as per the contract.

Employee Costs-Thyrocare has state-of-the-art automation system, consisting of an IT system comprising

of bar coding and bi directional laboratory Information System. Due to this, the operations require

minimal human intervention. Hence, the employee costs as % of total income for Thyrocare is 10% as

compared to 17.4% for its competitor Dr. Lal Path labs.Segment wise Revenue Breakup

DIAGNOSTIC-SEGMENT WISE

REVENUES Thyrocare recognizes its diagnostics testing

services and imaging services as the primary

business segments. The company focusses on

59% 53% 49% 54% wellness and preventive health care offering

through its brand Aarogyam. The distribution

41% 47% 51% 46% of revenue amongst Aarogyam and others is as

shown in adjacent figure

FY 13 FY 14 FY 15 FY 16

Test Profile based revenue and volume

Wellness & preventive healthcare Others breakup-From the adjacent figure, we can see

SEGMENT WISE - VOLUME, VALUE,

that the Aarogyam brand is of increasing value

MARGINS

for Thyrocare as it generates the maximum

20% 30% 20% revenue with minimum number of processed

20% tests.

20% Dividend policy

70%

The Company has decided on dividend policy

50% 60%

based on the standalone financials. 2 interim

10% dividends totaling to INR 7.5 per equity share

and another dividend of INR 2.5 totaling to INR

VOLUME VALUE MARGIN 10 per equity share.

Wellness & Preventive Thyroid Others

Du Pont Analysis (FY 16)-The only place

Thyrocare lags is the Asset turnover ratio. This implies that Thyrocare is not able to utilize its assets to

the same potential as its peers. Here, we also have to consider the impact of newly started RPLs in Bhopal

and Hyderabad. Though the assets i.e. RPLs and the Imaging centers have been set up, but they weren’t

yet operating at their full potential capacity.

Balance Sheet-The balance sheet size for Thyrocare grew

Du pont Comparison - Thyrocare

vs Dr. Lal from INR 3292.18 million to INR 4096.74 million at 24.44%.

127% The diagnostic testing services accounted for 66% of total

89%

81%

allocable assets and imaging accounted for 33.3%.

60% However, the revenue contributions from the two

25% 17% segments were 88.9% and 6.4% respectively. Thus, we see

13% 17%

that the imaging business contributes very less to the top

Net Asset Financial RoE line of the company as compared to the contribution in

profit turnover leverage total assets. While this is partly due to lesser number of CT

Margin

Thyrocare Dr Lal scans (60 scans per day) on account of lesser awareness and

availability of PET-CT scans in the country.

Peer Comparison -We consider SRL, Metropolis Healthcare and Dr Lal as the major competitors for

Thyrocare and accordingly compare them on key financial parameters (FY 16 only) [Exhibit 8]

Investment Risks

Business Risks/ Strategic Risks

Technological Disruption and Point of care testing (POCT)- POCT involves an instrument which

can do testing at home and will bring diagnostic lab at counter. There are instances like Delhi

Government using such instrument to deliver diagnostic services. Once this technology becomes

cost effective and provide a much variety of tests with single instrument it can significantly affect

the diagnostic industry. Further technologies like Digital pathology, whole-slide testing, molecular

diagnostics, wearable bio-sensors, mobile health solutions may pose a threat. Concentration risk- Thyrocare model is different from other players. Main competitor chains

have 100-200 labs spread across India but Thyrocare has a large dependence on CPL and the 6

RPLs. CPL performs all the tests offered while RPLs do tests that are more routine in nature and

conducive to high volume testing. Any disruption in transportation of samples to CPL /RPL or any

disruption in the CPL/RPL itself will lead to significant loss of business. Further, limited number of

test profiles offered lead to risk of losing out to a business segment that may grow abruptly in

future.

Extensive regulatory compliance- Diagnostic business is not subjected to much regulations but a

stricter regulatory environment in future dealing with handling of medical specimens, human

health and safety laws may pose a significant operational risks. Further, Nueclear business is

exposed to much more regulations than the diagnostics.

High dependence of ASPs- The pan India network of 1041 authorized service providers give ability

to grow customer base, enhance brand recognition and execution of business model. Heavy

dependence on these franchise based ASPs which are not in the direct control is a significant risk.

Further these ASPs can easily switch to other chains as they are allowed to give samples to other

chains also. The 687 TAGs (Thyrocare aggregators) and 354 TSPs (Thyrocare service providers)

form the crucial link between the company and the customers and hence extensive reliance on

them rather than having company owned network is a risk.

Vendor/ Supplier’s risk- The testing equipment like analyzers are acquired from vendors at

extremely low or no costs but with a contractual commitment to purchase a minimum amount of

reagents or consumables for a specified period. The ownership of equipment lies with the vendors

and may pass on to company only after the contractual period at a pre-decided price. This would

mean the if company doesn’t purchase the equipment as per the price set by the arrangement,

the vendor (Siemens, TransAsia, Roche) may withdraw and retake the possession of the

equipment.

Competition risk- Being a highly competitive and fragmented industry the only moat that

Thyrocare have is its pricing and volumes. There is a risk of a competitor drastically reducing its

pricing and cannibalizing the Thyrocare sales. Further any impairment in the ability to conduct any

test will dampen the operations and sales.

Financial risks/Macro Risk

INR depreciation- The purchase of raw material is linked to US Dollar. Hence any depreciation in

INR/USD will adversely Impact the cost of materials or reagents.

Non-sustainability of high margins- Because of huge competition risk, the company will face this

risk unless it spends on marketing costs.

Corporate Governance

Thyrocare Dr. Lal

Path Labs

Independence of the Board of Directors 50% 55%

Independent Committees Available Available

Transparency and Accountability Available Available

Vigilance Policy Available Available

Compensation Structure Available Available

Results communication: Half yearly NA NA

Quarterly reports Available Available

Annual report Available Available

Source: Company Annual Reports

The company has 5 committees – Audit, corporate social responsibility (CSR), nomination and

remuneration, stakeholder relationship and risk management – all headed by independent directors. In

the recent financial year, the company did not spend the required amount on CSR due to pending

identification of suitable projects. 50% of the directors do not have any other directorship or committee

membership in any other public companies. Except one director, every other director has attended more

than 75% of 12 general body meetings held last year, which shows the commitment towards the company.Appendix

Exhibit 1 – Thyrocare Brands and their offerings

Brand Services Offered

Thyrocare Metabolic Disorders and Thyroid Testing

Aarogyam Wellness and Preventive offering including liver, cholesterol,

kidney, thyroid, pancreas and other chronic disorders

Nueclear Cancer Monitoring- Full Body and Brain Scans

Whaters Water Testing- physical and chemical compounds testing

Source: Company Annual Report

Exhibit 2 – Type of Tests offered at CPL and RPL

Types of Thyroid Tests CPL RPL

Thyroid Stimulating Hormone Yes Yes

Total Triiodothyronine Yes Yes

Total Thyroxine Yes Yes

Non thyroid tests

CLIA Yes Yes

ELISA Yes

HPLC Yes Yes

Electrophoresis Yes

Flow cytometry Yes

Fluorescence Flowcytometry Yes Yes

Nephelometry Yes

Photometry Yes Yes

Liquid Chromatography Mass Spectrometry Yes

ICP-MS Yes

Wellness and Preventive Tests

Aarogyam 1.1 Yes Yes

Aarogyam 1.2 Yes Yes

Aarogyam 1.3 Yes Yes

Aarogyam 1.4 Yes

Aarogyam 1.5 Yes

Aarogyam 1.6 Yes

Aarogyam 1.7 Yes

Source: Thyrocare RHPExhibit 3 – Nationwide Location of CPL, RPL, Hubs and NHL PET-CT scan centers

Source: Thyrocare RHPExhibit 4 – Demand Drivers for Diagnostics Industry In India

Health insurance coverage in India

INR

Mn Increasing health insurance coverage ...

300

250

200

150

100

50

0

1 2 3 4 5

Total Non-Life Industry # of persons covered

...alongwith high population ...with more people in higher age groups will fuel demand

for diagnostic industry

growth...

1.36 1.42 6.9 8.2 9.2 10.7 12.5

1.29 11.1 13.6

1.21 14.8 15.5 16.3

1.03 19.6 20.5 21.1 22.5 23.7

27

28.6 28 26 24.3

35.4 29 26.8 25.1 23.4

FY2001 FY2011 FY2016 FY2021 FY2026 FY2001 FY2011 FY2016 FY2021 FY2026

0-14 years 15-29 years 30-44 years 45-59 years 60+ years

Source: Team Research

Exhibit 5 - Industry structureExhibit 6 - Mandatory licences and regulations for Diagnostics industry in India

Shop establishment licence

Pre-natal diagnostic technique act

Bhabha atomic research center guidelines

Pollution control board

Clinical establishment Act, 2010

Source: Team research

Exhibit 7 – Assumption of different growth rates for 3 scenarios

3 Different Scenarios FY17-21 FY22-26

Management case

Diagnostic Testing Services 30% 27%

Imaging Services 30% 30%

Others 30% 30%

Base case

Diagnostic Testing Services 27% 24%

Imaging Services 30% 30%

Others 20% 20%

Downside case

Diagnostic Testing Services 24% 21%

Imaging Services 20% 20%

Others 20% 20%

Source: Team Estimates, Bloomberg, Company Reports, Management Con-call

Exhibit 8 – Peer Comparison

Thyrocare Dr Lal SRL (FY 15) Metropolis

Revenue (In INR 2,410 7,910 8,980 6,500

mn.)

EBITDA Margin 38.8% 27.14% 18.68% 30%

PAT margin 21.50% 16.81% 10-11% 20%

RoE 14.17% 26.29% - -

Dividend 100% 24.5% - -

Revenue Mix 46.4% wellness 95% Pathology - -

and preventive and 5%

and 53.6% others radiology

Geography Mix Balanced ~72% revenue Balanced More focused on

Geographic Mix comes from Geographic Mix of west & south,

of revenues North India revenues

Variety of tests 193 tests 3495 tests 3800 tests 4500 tests

Infrastructure 1 CPL in Navi 172 clinical labs 325 labs in India, 4 130 labs and

Mumbai, 6 RPLs, 1,559 Patient international labs 1,000 collection

22 hubs Service Centers ,7500 collection centers spread

(PSCs) & 4,967 across India,

points

Pickup Points Africa, Sri Lanka

(PUPs) and Mauritius

Source: Annual Reports, Brokerage ResearchExhibit 9 – Valuation Summary Management case Base Case

Downside Case

Disclosures:

Ownership and material conflicts of interest:

The author(s), or a member of their household, of this report does not hold a financial interest in the securities of this company. The

author(s), or a member of their household, of this report does not know of the existence of any conflicts of interest that might bias the

content or publication of this report.

Receipt of compensation:

Compensation of the author(s) of this report is not based on investment banking revenue.

Position as a officer or director:

The author(s), or a member of their household, does not serve as an officer, director or advisory board member of the subject

company.

Market making:

The author(s) does not act as a market maker in the subject company’s securities.

Disclaimer:

The information set forth herein has been obtained or derived from sources generally available to the public and believed by the

author(s) to be reliable, but the author(s) does not make any representation or warranty, express or implied, as to its accuracy or

completeness. The information is not intended to be used as the basis of any investment decisions by any person or entity. This

information does not constitute investment advice, nor is it an offer or a solicitation of an offer to buy or sell any security. This report

should not be considered to be a recommendation by any individual affiliated with Indian Association of Investment Professionals,

CFA Institute or the CFA Institute Research Challenge with regard to this company’s stock.

CFA Institute Research ChallengeYou can also read