FY22 H1 PRE-CLOSE PRESENTATION - SEPTEMBER 2021 - Vukile ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FY22 H1 PRE-CLOSE PRESENTATION SEPTEMBER 2021

SOUTHERN AFRICAN PORTFOLIO

FY22 H1 PRE-CLOSE PRESENTATION

2

RETAIL PORTFOLIO PERFORMANCE AND TRADING ENVIRONMENT

PORTFOLIO HOLDING STEADY IN TOUGH OPERATING ENVIRONMENT

> Portfolio trading metrics back to pre-Covid levels

AUG 2021 MAR 2021 AUG 2021 MAR 2021

> FY22 turnover average 4% higher than comparable period in FY20

> Trading density growth up to 4.3% vs 1.7% at FY21

> Improvement in retention ratio (94% vs 90%) with strong Rent

Vacancies 3.4% GLA 3.2% GLA 98% 98%

collection rate (98%), indicating that tenants are paying rentals and are collection rate

trading

> Vacancies marginally up from 3.2% at FY21 to 3.4% Tenant Rent-to-sales

> SMME’s under pressure and account for c. 60% of all new vacancies 94% 90% 6.2% 6.3%

retention ratio

> Limited concern in the core of the portfolio. Strong retention of

nationals and second tier tenants, although negotiations more Annualised

-3.4% -3.3% COMMUTER

protracted Reversions growth in trading 4.3% 1.7%

Excl ERM +1.1% Excl ERM -1.8%

> Rental reversions holding steady and trending in line with FY21 results densities

> Pressure in the Urban regional portfolio

> Footfall trending 15% below pre-Covid levels, but with increased spend Average annual

Base Rentals R147.93/m² R146.40/m² R29 787/m2 R29 212/m²

trading density

per head – now starting to indicate changes in shopper behaviour more

pronounced in Commuter and Urban Portfolio

> Pending finalisation of outstanding renewals, base rentals show Contractual 84% vs 2019 87% vs 2019

6.6% 6.7% Footfall

marginal increase of 1.0% for the five months to August 2021 escalations 103% vs 2020 99% vs 2020

> The downward trend of contractual escalations continues as leases with

historical high escalations come to an end. Recent reversions were 3.3 years GLA

3.2 years GLA

concluded at average 6.5% in-contract escalations, with new leases at WALE

2.5 years Rent 2.7 years Rent

6.7%

3

RETAIL PORTFOLIO PERFORMANCE AND TRADING ENVIRONMENT

FOOTFALL AND SALES

Benchmark 2019

> Encouraging to note that current sales are trending ahead of Benchmark 2019 / 2020

(Pre-Covid)

pre-Covid levels (104%)

Average 104%

> Footfall trending below pre-Covid levels with notable 110%

109% 108%

shopper behaviour changes in commuter and urban malls 106%

103%

105%

101% 101% 99% 99% 101% 100%

98% 97% 99%

95%

> Rural and township centres show consistent growth in sales 93% 92%

90% 90% 88%

88% 88%

84% 86% 85%

> Value centres, with large exposure to grocers and essential 82% 84% 83%

81%

services, weathered the storm well during the COVID-19 72%

lockdowns with strong sustainable sales growth

59%

> Urban centres are showing improved sales, albeit at softer

growth rates

47%

> Commuter centres remain under pressure with reduced Sales

sales and footfall 33%

Footfall

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

2020 2021 2021

4

RETAIL PORTFOLIO PERFORMANCE AND TRADING ENVIRONMENT

SEGMENTAL FOOTFALL AND SALES

Sales Footfall

RURAL TOWNSHIP

> Sales recovered well with rural centres to 110%,

125%

116%

113%

113%

111%

111%

110%

108%

106%

106%

106%

106%

105%

105%

104%

104%

103%

103%

103%

102%

102%

101%

100%

100%

100%

99%

99%

98%

98%

97%

92%

township centres to 102%, urban centres to 92% and

87%

104%

104%

100%

98%

97%

96%

93%

93%

93%

92%

91%

90%

90%

55%

89%

89%

89%

89%

commuter centres to 89% relative to pre-Covid

89%

89%

88%

53%

87%

85%

85%

84%

84%

81%

79%

78%

76%

74%

72%

58%

Benchmark 2019 Benchmark 2019

trends

46%

(Pre-Covid) (Pre-Covid)

41%

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

2020 2021 2021 2020 2021 2021

> Footfall still lagging with rural centres to 92%,

URBAN COMMUTER

township centres to 89%, commuter centres to 79%

112%

110%

102%

100%

99%

96%

and urban centres to 70% relative to pre-Covid trends

96%

94%

94%

94%

92%

91%

91%

91%

91%

90%

89%

89%

89%

88%

88%

88%

88%

87%

87%

84%

84%

83%

83%

83%

81%

75%

100%

92%

92%

91%

89%

87%

86%

85%

84%

84%

84%

82%

81%

79%

79%

78%

> Shopping patterns are returning to pre-Covid trends

78%

77%

77%

77%

76%

76%

75%

74%

73%

72%

72%

70%

69%

26%

62%

61%

16%

Benchmark 2019 Benchmark 2019

41%

with increased weekend trade

13%

(Pre-Covid) (Pre-Covid)

26%

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

2020 2021 2021 2020 2021 2021

5

RETAIL PORTFOLIO PERFORMANCE AND TRADING ENVIRONMENT

RETAIL CATEGORY PERFORMANCE

Home Grocery/

Furnishings/ Art/ Supermarket Pharmacies

Antiques/ Décor Density 12,7% Density 19,0%

Density 9,8% Turnover 12,4% Turnover 20,1%

Turnover 15,0%

Sports

Fashion

Year-on-year turnover growth

Utilities/Gyms/Outdoor Cell Phones

Density (2,5%) Goods & Wear

Turnover (2,8%) Density 15,8%

Density 0,4% Turnover 15,4%

Turnover 1,6%

Other

Health & Beauty Density (3,9%)

Density (12,9%) Turnover (3,1%) Food

Electronics

Turnover (8,4%) Density 13,6%

Density 5,9%

Turnover 14,1%

Turnover 2,8%

Bottle Stores

Density (8,0%)

Department Stores Restaurants &

Turnover (8,3%)

Density (15,8%) Coffee Shops

Turnover (15,5%) Density (14,3%)

Turnover (14,7%)

Average annual trading density growth

6

RETAIL PORTFOLIO PERFORMANCE AND TRADING ENVIRONMENT

COLLECTIONS

R937M OF R955M COLLECTED

66% of 13% of 19% of 2% of

billings billings billings billings

National Mid-tier SMME's Government *

tenants tenants 97% 71%

99% 97%

Total portfolio

98%

35% of 16% of 49% of

billings billings billings

Fashion,

Groceries Other

Department

100% 96%

and Home

100%

* Government of Namibia and SA Post Office biggest contributors to irregular collections in Government tenancy, but limited to 1.7% of portfolio billings

7

COVID -19 RENTAL CONCESSIONS

R6.4M VS. R133M IN FY21 H1

R0,1m R0,0m

R0,2m

SMME's

16 tenants

R0,4m R0,4m TOWNSHIP

6%

R1,9m

National R0,1m

tenants

R0,8m

National tenants Mid-tier tenants

85 tenants 37 tenants R0,1m R0,0m

R0,2m

R2,4m R3,6m R0,3m

37% 57%

R0,1m

Mid-tier R0,6m COMMUTER

tenants

R0,3m R0,2m

4% R0,5m

5% Hospitality

R0,5m

8% R2,1m Sports Utilities/ Gyms

33% R0,6m

Bottle Stores R 0,041m

R0,5m

9% Restaurants & Coffee Shops R 0,026m

R0,6m Fashion

R 0,032m

9%

Home Furnishings/ Décor SMME’s

R0,2m

Gambling

R0,7m

R1,4m

11% Other R0,1m

21% 8

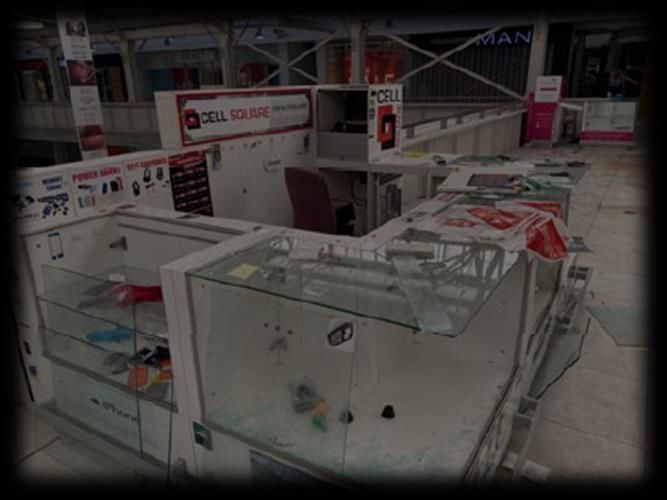

UPDATE ON CIVIL UNREST

6 PROPERTIES AFFECTED BY UNREST

Expected reinstatement costs Expected loss of rental

SASRIA claim SASRIA claim

R125m R57m

Number of shops damaged GLA Impacted

473 139 000m²

43% national 14% mid-tier 43% SMME 73 000m² (55%) exposure to Top 10 tenants

20 000m² (15%) exposure to SMME’s

9

UPDATE ON CIVIL UNREST

REINSTATEMENT AND TRADE

Expected Expected Number of

Number of % of GLA

completion cost to stores

stores trading

date repair trading

57 57

Perimete r fen ce, main en tran ce d oors an d National 24 National 24

16 Aug 21 R2.6m Mid-tier 11

100%

sh op fron ts Mid-tier 11

SMME 22 SMME 22

90 90

E n tran ce d oors, sh op fron ts, CCTV, gates an d National 39 National 39

16 Aug 21 R1.6m Mid-tier 16

100%

p erimete r fen ce Mid-tier 16

SMME 35 SMME 35

E n tran ce d oors, sh op fron ts, CCTV, vertical 116 84

National 58 National 46

tran sp ort, electrical, fire eq u ip men t, fire d amage 28 Sep 21 R13.8m Mid-tier 14

79%

Mid-tier 21

to 1 sh op SMME 37 SMME 24

E n tran ce d oors, sh op fron ts, CCTV, WiFi, vertical 93 36

National 34 National 18

tran sp ort, electrical, p arkin g eq u ip men t, fire 17 Sep 21 R9.5m Mid-tier 4

55%

Mid-tier 11

eq u ip men t, fire d amage to 3 sh op s SMME 48 SMME 14

E n tran ce d oors, sh op fron ts, ab lu tion s, 90 20

National 33 National 10

man agemen t offices, CCTV, WiFi, electrical, fire 13 Sep 21 R5.5m 46%

Mid-tier 5 Mid-tier 1

eq u ip men t, fire d amage to 3 sh op s SMME 52 SMME 9

27 2

Roof an d section s of b u ild in gs fire d amaged , National 16 National 2

sh op fron ts, ab lu tion s, man agemen t offices, 30 Mar 22 R91.5m Mid-tier 0

36%

Mid-tier 2

electrical, fire eq u ip men t, fire d amage to 3 sh op s SMME 9 SMME 0

10UPDATE ON CIVIL UNREST

Pine Crest 16 July 2021 Pine Crest 10 September2021

11UPDATE ON CIVIL UNREST

Durban Workshop 17 July 2021 Durban Workshop 9 September 2021

12UPDATE ON CIVIL UNREST

Hammarsdale 19 July 2021 Hammarsdale 9 September 2021

13DISPOSALS UPDATE

Sales Expected

Sector price Yield transfer

[R’m] date

Total 1 511.7 10.4%

357.5 9.9%

Ulundi King Senzangakona Shopping Centre Retail 308.7 9.4% Transferred 19 August 2021

Transferred Kempton Park Spartan Warehouse Industrial 23.8 14.8% Transferred 12 April 2021

Pretoria Rosslyn Warehouse Industrial 25.0 11.4% Transferred 14 April 2021

367.2 9.7%

Letlhabile Mall Retail 161.0 10.0% Sep-21 Obtaining clearance certificates

Unconditional Soshanguve Batho Plaza Retail 160.0 9.8% Nov-21 Obtaining clearance certificates

Centurion Samrand N1 Industrial 46.2 8.0% Sep-21 Obtaining clearance certificates

787.0 11.0%

Namibia Portfolio (sale of 64% stake) Retail 717.0 11.0% Nov-21 Due diligence complete. Formal agreements to be

Conditional signed shortly

Makhado Nzhelele Valley Retail 70.0 10.7% Nov-21 Formal agreements have been signed. Purchaser

obtaining funding

14FY22 H1

PRE-CLOSE

PRESENTATION

15ECONOMIC UPDATE: SPAIN

> In Q2 2021, Spanish GDP increased by 2.8% vs. Q1 2021 and increased by 19.8% vs. Q2 2020.

> The Spain GDP growth outlook for 2021 has recently been revised upwards from 5.5% to 6.5%.

> This is mainly due to increased consumption attributed to faster than expected vaccination roll-out, pent-up

demand from a high level of household savings, expected to be c.€60bn by Q42021, and the

GDP NextGenerationEU Plan which aims to distribute 70% of total available funds by the end of 2022 and the

OUTLOOK remaining 30% by 2023

> GDP is expected to recover to 2019 levels by 2022

> Inflation reached 3.3% in August (YoY) due to increased consumption levels and significant increases in

energy-related price levels and commodities. Analyst consensus estimates that 2021 will close with an annual

inflation rate of 3.4%

> Unemployment is expected to stabilise back to 2019 levels of just over 14.2% by 2022. As at July 2021,

unemployment rate reached c. 14% vs. 16% in July 2020

LABOR > In Q2 2021, total unemployment dropped by c. 100k workers to 3.5 million people

MARKET > There was a reduction in furloughed workers (ERTE) in Q2 2021 from 4% of enrolled workers to c. 3%

> ERTE program has been extended to the end of September 2021

> Spain received 4.4 million international tourists in July 2021, up 78% from 2020, and 9.8 million for the year

to the end of July 2021, however this is still only c. 55% of the levels seen in 2019

> Spain regional governments and the tourism sector are attempting to extend its high season into September

TOURISM

and October to increase visitor levels

Source: BBVA, EL PAIS, European Commission, Funcas

16UPDATE ON COVID-19 IN SPAIN

SPAIN ACHIEVED THE TARGET OF VACCINATING AT LEAST 70% OF THE POPULATION BY THE END OF AUGUST 2021

VACCINATION PROGRAMME FOLLOWING THE WAVES

Fully Vaccinated At least 1 shot

State of Alarm

73% 78% declared

Start of

vaccination

– hard national

of population of population programme 34.3 million people

lockdown

with vaccination

completed

> Vaccination campaign enjoys a high acceptance rate by the Spanish Announcement of

(c. 73% of

population, ranking 3rd in Europe in the level of population fully vaccinated. de-escalation plan

population)

According to the Spanish Ministry of Health, c. 90% of the population trusts the

positive effects of being vaccinated Spain

under curfew

> Elderly and other vulnerable people have already been vaccinated, Main restrictions:

significantly reducing deaths and pressure in ICU beds. 100% of people >80 “New normal” trading hours,

years of age, 99% between 70-79 and 98% of people between 60-69 years of capacity limits and

age have been fully vaccinated non-essential

> At the current vaccination rate, 90% of the population will be vaccinated by closures

October 2021

KEY INDICATORS

> Accumulated incidence in last 14 days reached 160 cases per 100,000 people

yet deaths remain low compared to previous waves

> Pressure on ICU beds remains at c. 15%, which is considered a medium risk.

Currently, there are c. 1,300 COVID-related patients at hospitals

> Total number of accumulated cases: c. 5 million confirmed

> Total deaths: c. 85k confirmed by Ministry of Health

Source: Ministry of Health, Government of Spain. https://www.rtve.es/noticias/coronavirus-graficos-mapas-datos-covid-19-espana-mundo/ 17FOOTFALL & SALES

2020 2021

18 120,0%

1ST WAVE 2ND WAVE (3) 3RD WAVE (3) > Sales continue to strengthen and have

16 surpassed 100% of 2019 levels in June

100,0% 2021. Larger basket sizes and higher

14 conversion rates continue to drive

sales

12 80,0%

> Retail park sales are already above

10 2019 levels. Retail parks comprise

60,0%

45.1% of Castellana’s portfolio by GLA

8

> Footfall recovered up to 85.7% of 2019

6 40,0%

levels in August 2021, the highest level

4

since March 2020. Over the past 18

20,0% months the pandemic waves have

2 affected the performance of the

Partial restrictions and portfolio, however strong growth was

Essential services only trading hour limitations

0 0,0% evident once restrictions were relaxed

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dic Jan Feb Mar Apr May Jun Jul Aug

Nº of Assets open and without highly restricted mobility Footfall Recovery

Sales Recovery Footfall Recovery Benchmark

Sales Recovery Benchmark

(1) Footfall Data includes the following shopping centres: El Faro, Bahía Sur, Los Arcos, Vallsur, Habaneras, Puerta Europa and Granaíta Leisure & Retail Park. There are no counters in the rest of the retail park assets Granaita

only counts cars, so we have estimated an average of 2 people per car. Monthly information: evolution of month in 2020 and 2021 vs the same month in 2019

(2) Sales Data includes all retail assets. Monthly information: evolution of month in 2020 and 2021 vs the same month in 2019

(3) Regional restrictions during 2º and 3º wave: town perimeter closures, trading hours capped, curfews, non-essentials retails closures…). Regional restrictions during 4th and 5th waves: Trading hours and capacity capped

18OPERATING ACTIVITY

(2)

OCCUPANCY RATE 97% CONTINUOUSLY CLOSING AGREEMENTS AND OPENING

NEW STORES DURING THE PANDEMIC DUE TO THE STRENGH OF OUR TENANT

KEY KPI´S YTD 31st August 2021

RELATIONSHIPS AND RETAIL EXPERTISE

86 €4.3m PORTFOLIO ALMOST FULLY LET

31 AUGUST

LEASES SIGNED NEW RENT SIGNED 2021 97.0%

31 MARCH

2021 98.3%

28 58 €1.2m €3.1m

RENEWALS NEW CONTRACTS RENEWALS NEW CONTRACTS

RENT ARREARS UNDER 5% DESPITE PANDEMIC

31 AUGUST

2021

4.9%

31 MARCH

2021

4.8%

18,170 sqm 1.76%

GLA SIGNED AV. RENT INCREASE(1)

RENT COLLECTION ABOVE 95%

31 AUGUST

1.38% 95.1%

2,824 sqm 15,346 sqm 2.34% 2021

RENEWALS NEW CONTRACTS RENEWALS NEW CONTRACTS 31 MARCH

2021 95.2%

(1) Considering operations with passing rent as renewals, relocations and replacements

(2) Period reported from 1st April 2021 to 31st August 2021

19TRADING ENVIROMENT

> Sales & Footfall continue to improve with portfolio effort rates

in line with industry benchmarks

> Larger retailers like Inditex, JYSK, Primark, Kiwoko, Pepco, IKEA

(with a 3,000sqm concept), Kiabi, Media Markt (500-700sqm

“Smart” format), are currently expanding their portfolios and

continue to demand new space, opening new stores across the

country

> Restaurants and Leisure, two of the most affected sectors

during the pandemic, are recovering sales levels. Some

retailers like Popeye’s, Fitzgerald, KFC, Papa John’s, are

resuming their expansion projects

> Castellana has continued to create interesting and exciting

events in our Shopping Centres over summer which has

improved awareness and grown footfall

20RETAIL CATEGORY PERFORMANCE

+2.5% OVERALL PORTFOLIO SALES GROWTH FOR THE PERIOD 1 AUGUST 2020 TO 31 JULY 2021

Turnover growth by retail category

> 2021 sales are approaching 2019

120 000 000,00 40,0%

23,2% -6,3%

28,4% levels month by month. We have

19,9%

100 000 000,00 14,6% 20,0% been above 90% of 2019 sales in

0,4% 2,7% 0,4% 0,5%

the last three months, exceeding it

-2,8%

80 000 000,00 0,0% in June

-14,3%

60 000 000,00 -20,0%

> DIY, Electronics and Pets continue to

40 000 000,00 -40,0%

be the best performing categories

-62,6%

20 000 000,00 -60,0% > Leisure and Food & Beverage

continue to be the most affected by

- -80,0%

restrictions

Sales L12M 2020 Sales L12M 2021 Var %

21FINANCE AND TREASURY FY22 H1 PRE-CLOSE PRESENTATION

DEBT AND TREASURY UPDATE

IMPROVED BALANCE SHEET METRICS RECOGNISED BY DEBT CAPITAL MARKETS AND CREDIT RATING AGENCY

> Balance sheet metrics remain positive:

> Group LTV and ICR ratios are expected to be largely in line with 31 March 2021

> c. R300 million of Vukile bank debt maturing in FY2022 is currently being negotiated and a further c. R1.6 billion of Vukile bank

debt maturing in FY2023 is currently under consideration for early re-finance

> In advanced stages of finalising the re-finance of Castellana’s Syndicate Loan (c. €140m, which matures over three tiers across

FY2023, FY2024 and FY2025), into a new 5-year loan

> c. R2.7 billion of undrawn facilities

> GCR reaffirmed national scale Issuer rating of AA-(ZA) and A1+(ZA) for the long- and short-term respectively, with a stable outlook

> Successful oversubscribed R500 million unsecured bond auction held in August:

> Auction 4.4 times oversubscribed, attracting bids of more than R2.2 billion and drew orders from 13 investors

> R342 million 3-year note issued below guidance at a margin of 185bps and R158 million 1-year note issued at a margin of 135bps

> R535 million note maturing in August was repaid with the proceeds of the auction. The issuances were LTV neutral

> Good progress on the sale of non-core assets:

> R357 million property sales transferred in FY2022

> R367 million property sales unconditional and expected to transfer in Q3 and Q4 2021

> Good progress with potential sale of Namibian Portfolio 23QUESTIONS

24You can also read