ESTADÍSTICAS TRIBUTARIAS REVENUE STATISTICS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ESTADÍSTICAS TRIBUTARIAS REVENUE STATISTICS 55 Asamblea General/General Assembly GUATEMALA Santiago Díaz de Sarralde Miguez Director de Estudios Tributarios /Centro Interamericano de Administraciones Tributarias (CIAT) Tax Studies Director/Inter-American Center of Tax Administrations (CIAT)

VARIACIONES MENSUALES Y ACUMULADAS RECAUDACIÓN CIAT (23)

MONTHLY AND CUMULATIVE COLLECTION VARIATIONS CIAT (23)

Promedio Mensual Promedio Acumulado

10.0

5.6

4.8

5.0

4.8 5.2

1.1

0.0

0.3

-2.1

-5.0

-4.8 -4.4

-6.4

-7.4

-10.0

-8.7 -10.0

-9.4 -9.3

-10.8

-12.0 -11.5

-12.1

-15.0 -12.7

-13.9

-20.0

-22.6

-25.0

-26.9

-30.0 -28.7

-35.0

Ene 20/19 Feb 20/19 Mar 20/19 Abr 20/19 May 20/19 Jun 20/19 Jul 20/19 Ago 20/19 Set 20/19 Oct 20/19 Nov 20/19 Dic 20/19

VARIACIONES ACUMULADAS RECAUDACIÓN/CUMULATIVE COLLECTION VARIATIONS

AMÉRICA LATINA Y EL CARIBE CENTROAMÉRICA + Rep.Dom. CARIBE ANDINOS + Chile MERCOSUR + México OTROS

15.0

10.0

5.0

0.0

-2.3

-5 .0 -3.2

-1 0.0 -10.9

-11.7

-12.0

-1 5.0

-14.4

-2 0.0

ENE 20/19 FEB 20/19 MAR 20/19 ABR 20/19 MAY 20/19 JUN 20/19 JUL 20/19 AGO 20/19 SET 20/19 OCT 20/19 NOV 20/19 DIC 20/19

ALC VARIACIÓN ACUMULADA POR IMPUESTOS

LAC CUMULATIVE COLLECTION VARIATIONS BY TAX

TOTAL OTROS ISC ISR IVA

15.0

10.0

5.0

0.0

-5 .0

-7.8

-9.3

-1 0.0

-10.9

-13.4

-14.2

-1 5.0

-2 0.0

ENE 20/19 FEB 20/19 MAR 20/19 ABR 20/19 MAY 20/19 JUN 20/19 JUL 20/19 AGO 20/19 SET 20/19 OCT 20/19 NOV 20/19 DIC 20/19

• ISC (IMPUESTOS SELECTIVOS CONSUMO) = EXCISES

• ISR (IMPUESTO SOBRE LA RENTA) =INCOME TAXES

• IVA = VAT

• OTROS = OTHER

VARIACIONES ACUMULADAS RECAUDACIÓN POR PAÍS

CUMULATIVE COLLECTION VARIATIONS BY COUNTRY

Marruecos 8.2

México 0.8

Paraguay -1.3

Uruguay -2.7

Nicaragua (Nov) -2.7

EE.UU. -3.5

Italia -5.3

El Salvador -5.5

Brasil -5.5

Guatemala -6.7

Argentina -7.4

España -8.5

Promedio Acumul ado -9.3

Colombia -9.4

Chile -9.5

Costa Rica -11.9

Ecuador -12.9

República Dominicana -13.0

Jamaica -14.5

Perú -15.1

Trinidad y Tobago -21.4

Honduras -22.5

Panamá -26.9

-30.0 -25.0 -20.0 -15.0 -10.0 -5.0 0.0 5.0 10.0

Movilidad Tiendas y Ocio

-70.0 -60.0 -50.0 -40.0 -30.0 -20.0 -10.0 0.0

10.0

Feb

5.0

Nov

0.0

Oct Dic

Recaudación Total

Set

-5.0

Mar

Jul

Ago

-10.0

-15.0

y = 0.6042x + 12.206

R² = 0.8662

-20.0

Jun

-25.0

Mayo

Abril

-30.02021 1er Cuatrimestre/1st Quarter

• LA RECUPERACIÓN ESTÁ EN MARCHA / RECOVERY IS UNDERWAY • TODAVÍA EXISTE GRAN INCERTIDUMBRE / STILL GREAT UNCERTAINTY • DATOS PROVISIONALES/PROVISIONAL DATA • EL ANÁLISIS ES COMPLEJO (POR PERIODO, IMPUESTO, PAÍS) / ANALYSIS IS COMPLEX (BY TIME PERIOD, TAX, COUNTRY)

ESTADÍSTICAS TRIBUTARIAS REVENUE STATISTICS MUCHAS GRACIAS A TODOS LOS PAÍSES Y SUS FUNCIONARIOS POR SU COLABORACIÓN THANK YOU VERY MUCH TO ALL COUNTRIES AND THEIR PUBLIC SERVANTS FOR THEIR SUPPORT

IMPLEMENTATION OF VAT ON DIGITAL SERVICES

CHILEAN EXPERIENCE IN THE

IMPLEMENTATION OF VAT ON DIGITAL

SERVICES (VAT DS)

CIAT - Guatemala 2021VAT on Digital Services

INDEX REGULATORY ASPECTS REGISTRATION– DECLARATION – PAYMENT LEGAL CONTROL MECHANISMS RESULTS

REGULATORY ASPECTS

REGULATORY ASPECTS

§ Law 21.210 established

new VAT taxable events

New letter n) of

starting June 1° 2020.

article 8th of the VAT

Law

§ The new letter n) of article

8th of the VAT Law

included four taxable

Law 21.210 which services rendered by non

modernizes tax resident service suppliers.

legislation,

enacted as of

February 2020

§ A Simplified Registration and

Compliance Regime

New paragraph 7° exclusively for nonresident

bis, of the VAT Law service suppliers is createdREGULATORY ASPECTS

1. Platforms that intermediate

underlying services rendered in

Chile - any kind of service - or sales

of Chilean or imported goods.

2. Download or streaming of digital

entertainment content (movies,

New letter n) of New videos, music, games, texts, books,

article 8th of the Taxable newspapers, magazines, etc.).

VAT Law Services

3. Download of software, SaaS, PaaS,

IaaS (storage, platforms, or

computing infrastructure).

4. Advertising regardless of how it is

executed (digitally or by other

means)REGULATORY ASPECTS

Non resident suppliers of

Liable Taxpayers services of the new letter n) of

article 8th of the VAT Law.

Taxpayers and

tax rate

VAT, with a 19% rate, is applied

on price paid for services of

Tax Rate the new letter n) of article 8th

of the VAT Law.REGULATORY ASPECTS

It is a simplified tax regime

established in article 35 A of

paragraph 7 bis of the VAT Law,

¿What is it? which can be used instead of the

ordinary tax regime, by nonresident

Simplified suppliers who meet certain

Registration and requirements.

Compliance Regime

of paragraph 7° bis 1. Non resident suppliers.

of the VAT Law 2. That render services levied in

¿Which

the new letter n) of article 8th

taxpayers can

use this of the VAT Law.

3. Services must be used in Chile

regime?

by individuals or legal entities

that are not VAT taxpayers.

Nonresident suppliers that provide

services, other than those indicated

in the new letter n), of article 8th of

the VAT Law, may also apply this

regime if the they request it.REGULATORY ASPECTS

Tax period in 1 month or 3 consecutive

which VAT must months, payable until the 20th

be declared and

paid of the first following month. VAT

can be paid in USD, Euros or

Chilean $.

Simplified

Registration and

Compliance Regime

The nonresident supplier cannot

Deduction of deduct input VAT and is released

input VAT? from issuing invoices and other

tax documentation.REGULATORY ASPECTS

Provides instructions on VAT

Circular 42 taxation and administration

(11.06.2020) of digital services

Regulates registration in the

Res. Exta. SII N° 55 Simplified Registration and

(20.05.2020) Compliance Regime

Regulations

Regulates the procedure for

non resident suppliers to

Res. Exta. SII N° 67 declare and pay VAT.

(25.06.2020)

Reporting obligations on

Res. Exta. SII N° 91 offshore payments with

(21.08.2020) y N° 167 credit cards and other

(20.12.2020) online payment meansREGISTRATION – DECLARATION –

PAYMENTREGISTRATION – DECLARATION – PAYMENT

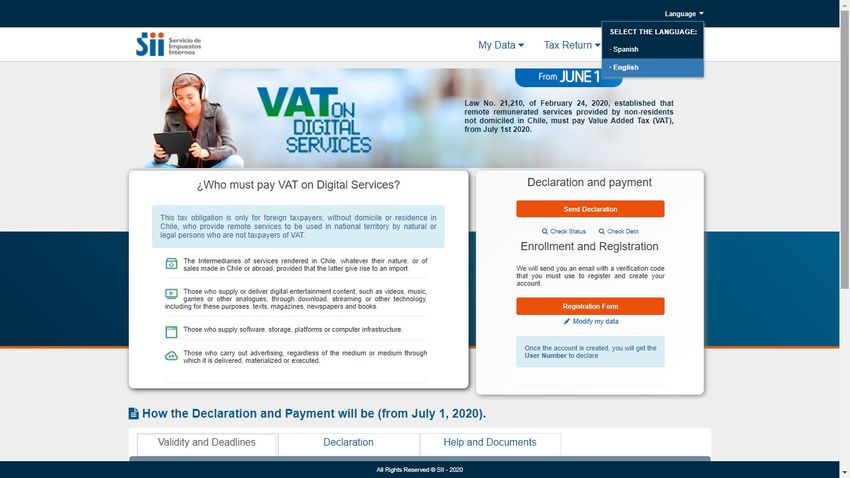

VAT Portal on Digital Services is

VAT Portal on

available on the web site sii.cl.

Digital Services

VAT Portal -

Available The platform contains relevant

Available

Information information regarding VAT on digital

information - services, both in English and Spanish.

Relevant dates

1. VAT surcharged on services

rendered since June 1rst 2020

Relevant Dates 2. Declaration and payment since:

§ July 1rst 2020 (monthly tax period)

§ Octobre 1rst 2020 (quarterly tax

period)

(January-March / April-June / July-

September / October - December)REGISTRATION – DECLARATION – PAYMENT

REGISTRATION– DECLARATION – PAYMENT

REGISTRATION – DECLARATION – PAYMENT

Nonresident suppliers can file online

the registration form for the

Registration Form

Simplified Registration and

Compliance Regime.

§ Have a valid email

Requirements § Confirm email (verification code)

§ Create a password

After the email is confirmed, a User

User Number Number that identifies the taxpayer

and allows browsing through the site

is generated.REGISTRATION– DECLARATION – PAYMENT

REGISTRATION– DECLARATION – PAYMENT

REGISTRATION– DECLARATION – PAYMENT

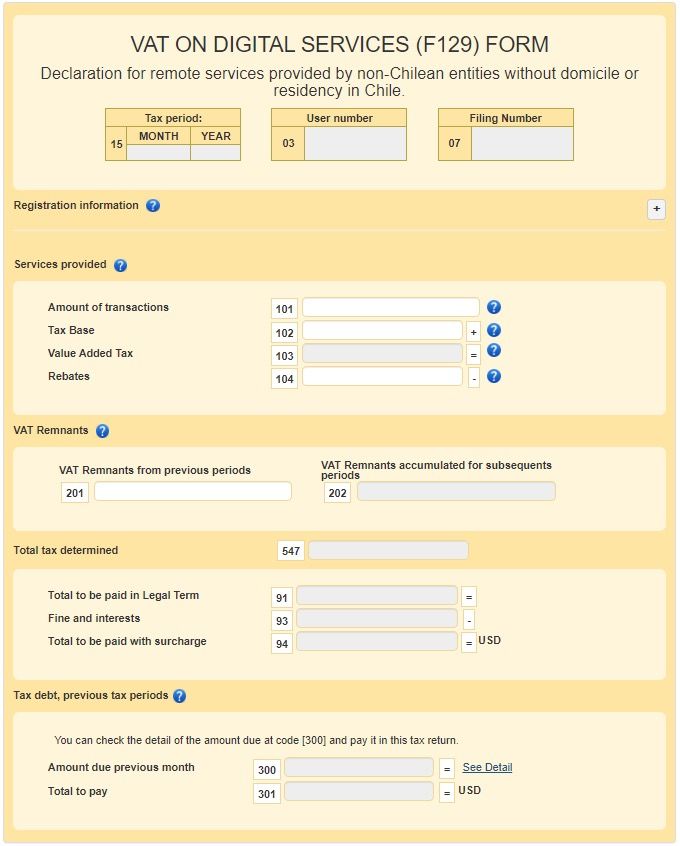

The taxpayer must enter:

• Number of transactions for the period

• Tax base

Declare Form 129

(F129) • Rebates

The system will automatically calculate 19%

VAT

If the taxapayer carries a debt, the

outstanding amount will show so it can be

paid in F129REGISTRATION– DECLARATION – PAYMENT

REGISTRATION– DECLARATION – PAYMENT

• Declarations in foreign currency (EUR

Payment of F129 or USD) must be paid through a

SWIFT transfer.

• Declarations in national currency

(CLP) can be paid online.

The VAT Portal on digital services shows the

Check F129 Status status of the tax return (current or not

current) and the status of payments made

(full, partial or no payment).

Additionally, the taxpayer can amend current

tax returns.

Check Outstanding If there are tax periods with outstanding

Amounts $ amounts, the taxpayer will be able to

know the details of such debt.REGISTRATION– DECLARATION – PAYMENT

Frequently Asked Frequently asked questions addressed to

nonresident suppliers, regarding VAT on

Questions Digital Services, the Portal, and how to

declare and pay VAT

Assistance Tutorials Step by step guides to complete the

Registration Form on the Portal, and

instructions for declaring and paying

Form 129.

Current regulations both available in

Regulations English and Spanish.REGISTRATION– DECLARATION – PAYMENT Assistance

REGISTRATION–

AYUDAS DECLARATION – PAYMENT

The list of taxpayers registered is

Registered Taxpayers available for consultation on the VAT

Portal on Digital Services and is

weekly updated.

The Portal´s functionality allows nonresident

Assistance suppliers to report to the SII the list of

Chilean service beneficiaries who informed

VAT / WT Taxpayers them of their VAT taxpayers´ status or of

being withholding agents of services subject

to Withholding Tax.

Report Non The Portal´s functionality allows users of

Compliances the Portal to report noncompliancesLEGAL CONTROL MECHANISMS

LEGAL CONTROL MECHANISMS

The SII may order the issuers of credit

cards, debit cards, or other similar on line

payment systems, to withhold in whole or

Withholding by the

in part taxes with respect to all or part of

Issuer of Online

Payment Means the operations carried out by nonresident

suppliers who have failed to register in the

Simplified Registration and Compliance

Regime.LEGAL

ALTERNATIVAS

CONTROLPARA

MECHANISMS

EL CONTROL

The SII may use all available

technological means to verify the

taxable events of article 8th letter n),

Audit of the VAT Law independent of the

jurisdiction.

Article 35 i of the VAT Law.LEGAL

ALTERNATIVAS

CONTROL MECHANISMS

PARA EL CONTROL

Information can be requested:

a) Taxpayers who intermediate can be required

to identify of sellers or service providers for

which they intermediate.

b) The amounts that are paid or made available

Information to such sellers or service providers.

Regarding

Underlying The exercise of this legal authority is aimed at

Providers obtaining information regarding the underlying

operations or the object of the intermediation,

and therefore the tax compliance in Chile of the

sellers or service providers, and does not

necessarily imply the initiation of an audit

procedure with respect to the nonresident service

provider.LEGAL

ALTERNATIVAS

CONTROL MECHANISMS

PARA EL CONTROL

In use of the powers granted and in order to

access relevant information to detect

noncompliance, the SII issued Resolution No.

91 of 2020 and No. 167 of 2020, which required

bank and non-bank issuers, respectively, of

credit, debit, payment cards with provision of

funds or other similar online payment systems,

Resolución N° 91 periodically inform the SII of the acquisitions of

and N° 167 de goods or provision of services made by

2020 nonresident sellers or service providers.

Banks cover 95% of transactions made through

credit cards.

The information is sent to the SII through a

"Payment Cards Report".THE OUTCOME

THE OUTCOME

RESULTADOS

Non Resident Service Providers Registered on Monthly Basis

(Total 199)

250

200

150

100

50

0

may-20 jun-20 jul-20 ago-20 sept-20 oct-20 nov-20 dic-20 ene-21 feb-21 mar-21 abr-21 may-21 jun-21

Report as of June 14, 2021THE OUTCOME

RESULTADOS

Total paid in the Monthly average Total tax returns Monthly average paid per

Period

period (USD) mensual (USD) filed tax return (USD)

Jun-Jul-Augu-Sep

72.203.943 18.050.986 136 132.728

(2020)

Oct-Nov-Dec (2020) 60.428.478 20.142.826 138 145.963

Jan-Feb-Mar (2021) 61.027.791 20.342.597 152 133.832

Report as of June 14 2021CHILEAN EXPERIENCE IN THE

IMPLEMENTATIPN OF VAT ON DIGITAL

SERVICES (VAT DS)

CIAT - Guatemala 2021Uruguay El Impuesto al Valor Agregado en los servicios digitales

El Impuesto al Valor Agregado en los servicios digitales • Introducción • Generalidades del Impuesto al Valor Agregado en Uruguay • Desafíos de los servicios digitales • Medidas normativas que abordan la problemática identificada • Acciones de fiscalización en la materia • Reflexiones finales

El Impuesto al Valor Agregado en Uruguay

• País pionero en la introducción del impuesto (año 1967).

• Tasa general: 22% (tasa reducida del 10% / exoneraciones).

• Ámbito espacial:

o Operaciones internacionales de bienes: criterio de destino.

o Operaciones internacionales de servicios: criterio de territorialidad +

figura de “exportación de servicios” (listado taxativo).Desafíos de los “servicios digitales”

• Incremento exponencial de operaciones internacionales.

• En particular:

o transacciones B2C;

o “productos digitales” (intangibles y servicios digitales); y

o prestadores no residentes sin EP en el país.

• Evitar competencia desleal con modalidades tradicionales.

• Prevenir la erosión de la base imponible del impuesto.Medidas normativas que abordan la problemática • Ley N° 19.535 de 25/09/2017 y reglamentación. • Disposiciones o de carácter sustantivo y formal; o sobre tributación de ciertos servicios digitales. • Garantizar seguridad y previsibilidad a los contribuyentes. • Facilitar el cumplimiento tributario de los contribuyentes. • Diálogo cooperativo: fisco, contribuyentes y otras partes interesadas.

Medidas normativas (cont.)

Servicios digitales de transmisión de contenido audiovisual

(plataformas digitales de películas y series, música, etc.)

cuando “tengan por destino, sean consumidos o utilizados

económicamente en el país”, se consideran realizados

íntegramente dentro del territorio nacional.Medidas normativas (cont.)

• Definición de “contenido audiovisual”.

• Exclusiones:

o servicios de publicidad y propaganda y de carácter técnico;

o servicios de enseñanza a distancia;

o servicios contratados correspondientes a “Plan Ceibal” y “Plan

Ibirapitá”.Medidas normativas (cont.)

Servicios digitales de intermediación en la prestación de servicios

(plataformas digitales que intermedian en transporte, alojamiento, etc.)

o en los que oferente y demandante “se encuentren en el país” se

consideran realizados íntegramente dentro del territorio nacional.

o en los que oferente o demandante “se encuentre en el exterior” se

consideran realizados en un 50% dentro del territorio nacional.Medidas normativas (cont.)

• Proxy para localizar a oferente y demandante del servicio

subyacente en el país

o Oferente: el servicio subyacente se preste en territorio nacional.

o Demandante: dirección IP, dirección de facturación, administración

de medios de pago en territorio nacional.Medidas normativas (cont.)

• Medidas de carácter formal:

o Posibilidad de prescindir de designación de representante.

o Pagos trimestrales.

o Posibilidad de presentar declaración jurada y realizar pagos en dólares

estadounidenses.

o Validación de documentación emitida según normativa del país de

residencia del prestador.Acciones de fiscalización en la materia

• Fiscalización en su definición amplia.

• Medidas han de ser:

o permanentes;

o omnicomprensivas;

o sistemáticas; y

o eficientes.

• Foco en control preventivo.Acciones de fiscalización en la materia (cont.) • Fiscalizaciones automatizadas. • Proceso de diseño e implementación. o Efectos de la irrupción de la COVID-19. o Plan de Control Tributario 2021. • Cruces de información proporcionada por terceros (administradores de medios de pago electrónicos). o Identificación e inscripción de prestadores. o Desafíos y oportunidades.

Acciones de fiscalización en la materia (cont.) • Auditorías tributarias. • Desafíos propios de la ausencia de presencia física en el país. • Equipos multidisciplinarios. • Relevancia del “representante” (vocero) local. • Ausencia de litigios/riesgo reputacional o prohibiciones de la actividad.

Reflexiones finales • Alcance a ciertos servicios digitales. • Primer acercamiento en la materia. • Solución exitosa a la problemática identificada. • Caso del transporte terrestre de pasajeros: rol de las plataformas digitales. • Uso de tecnologías al interior de la AT y reingeniería de procesos.

Muchas gracias por su atención.

You can also read