Electra Battery Materials - Commencing operations in Q4'22 Investor Presentation - May 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Electra Battery Materials Commencing operations in Q4’22 NASDAQ: ELBM; TSX-V: ELBM Investor Presentation – May 2022

Forward Looking Statements All statements in this presentation other than statements of historical fact constitute “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995, and “forward-looking information” under similar Canadian legislation and are based on the reasonable expectations, estimates and projections of Electra Battery Materials Corporation as of the date of this presentation. Forward-looking statements and forward-looking information include, without limitation, possible events, trends and opportunities and statements, including with respect to the state of the cobalt market, global market conditions, the proposed development of the Electra Battery Materials Park, the processing of raw material feedstocks, the ability to secure financing, results of exploration activities, potential acquisitions, capital expenditures, successful development of assets, currency fluctuations, government policy and regulation and environmental regulation. In particular, forward-looking information included in this presentation includes, without limitation, the opportunity to restart the Electra refinery and targeted metrics. Generally, forward-looking statements and forward-looking information can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes”, or variations of such words or state that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”. Forward-looking statements and forward-looking information are necessarily based upon a number of estimates and assumptions that, while considered reasonable by the Company as of the date of such statements, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements and forward-looking information. Such factors include changes in supply and demand for cobalt ,nickel and other battery raw materials, the results of metallurgical and engineering studies, changes in competitive pressures, timing and amount of capital expenditures, changes in capital markets, changes in exchange rates, unexpected geological or environmental conditions, changes in and the effects of, government legislation, taxation and regulations and political or economic developments, success in attracting officers for the future success of the Company’s business, success in obtaining any required additional financing to advance strategic priorities, and risks associated with obtaining necessary licenses or permits. Many of these uncertainties and contingencies can affect the Company’s actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements and forward-looking information made by, or on behalf of, the Company. There can be no assurance that forward-looking statements and forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. All of the forward-looking statements and forward-looking information made in this presentation are qualified by these cautionary statements. Although management of the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or forward-looking information, there may be other factors that cause results not to be as anticipated. There can be no assurance that such statements will prove to be accurate, as actual results could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements and forward-looking information. The Company does not undertake to update any forward-looking statements or forward-looking information that are incorporated by reference herein, except in accordance with applicable securities laws. Timelines used in this presentation are for the purpose of aiding management in the planning and implementation of the projects and are not based on a detailed assessment of project requirements. Consequently, the timelines are subject to material revision as subsequent technical reports and assessments are completed. Future phases of the project are contingent upon completion of preceding phases. Nothing in this presentation should be construed as either an offer to sell or a solicitation of an offer to buy or sell shares in any jurisdiction. Mark Trevisiol, P.Eng. and Dan Pace, P.Geo are Qualified Persons as defined by National Instrument 43-101 - Standards of Disclosure for Mineral Project (“NI 43-101”) and both are employed by Electra. They have reviewed and approved the technical content in this presentation. NASDAQ: ELBM | TSX.V: ELBM 2

Strategy: Onshore EV Supply Chain

Electra Battery Materials Rationale

Battery materials company – OEM and cell maker requirement for an integrated, localised and

environmentally sustainable solution for battery materials

Commission battery grade cobalt sulfate plant (Q4) sourcing in North America

2022 – Third-party cobalt hydroxide feed

– North American need for industrial hub to convert regional nickel

– Iron Creek primary cobalt extraction

resources to battery grade sulfate

2023 Lithium-ion battery recycling

Battery grade nickel sulfate production

2024

– Third-party North American nickel raw material feed

North America’s

2025 Battery precursor manufacturing integrated, sustainable

National or international expansion

battery materials solution

2023-26

Iron Creek cobalt-copper project development

Products Cobalt, Nickel, Lithium, Copper, Graphite, Precursors

NASDAQ: ELBM | TSX.V: ELBM 3

Strategically located in North America

Electra China

Battery pipeline of >600 GWh,

sufficient to supply more than Distance to USA2 1,350 km 13,250 km 10x

9 million full-battery electric

vehicles per year1 Distance to Europe3 6,100 km 19,500 km 3x

Funded to production in Q4 2022

Only hydrometallurgical facility of its kind

in North America

Up to 51% lower GHGs than Chinese

peers due to hydroelectric power grid

Eliminates tariffs imposed on

Chinese imports

Existing cell plant Future cell plant

Pilot cell plant Electra Battery Materials Park

1. Assuming average vehicle pack size of 67kWh (2021 average in North American market). 2. Rotterdam. 3. Frankfort, KY

Source: Electra Battery Materials, CIC energiGUNE

NASDAQ: ELBM | TSX.V: ELBM 4

Leadership Team

Management

Trent Mell Mark Trevisiol Renata Cardoso Michael Insulán Regan P. Watts Ken Murray Dr. George Puvvada

CEO & Director P.Eng Vice President, PhD Vice President, Project Manager, P.Eng., PMP, PhD

Vice President, Corporate Affairs Refinery Expansion Refinery

Vice President, Sustainability and

Commercial Technical Manager

Project Development Low Carbon

Board of Directors

John Pollesel Garett Macdonald Gov. Butch Otter Susan Uthayakumar

Chairman Director Director Director

CEO, President & CEO , Retired, Governor of Idaho MD, Chief Energy and

Boreal Agrominerals Inc Maritime Resources (’07-’19) Sustainability Officer,

Prologis

NASDAQ: ELBM | TSX.V: ELBM 5

Battery Materials Park Ontario, Canada

Battery Materials Park – Unique Position in North America

Electra’s ambition is to operate in the first four stages of the battery supply chain

Primary extraction Recycling Primary refining PCAM1 CAM2 manufacturing Cell manufacturing Electric vehicle

manufacturing assembly

Primary extraction Recycling Refining PCAM CAM Cells Electric vehicles

Selection of lithium-ion battery supply chain

participants in North America

Electra Battery Materials

Tesla

Ford

GM

Toyota

Stellantis

SK Innovation

LG Chem

Li-Cycle

Redwood Materials

1. Lithium-ion battery precursor material; 2. Lithium-ion battery cathode active materials

Source: Electra Battery Materials

NASDAQ: ELBM | TSX.V: ELBM 7

Ahead of the Pack

Existing refinery, infrastructure and permits

– Hydrometallurgical facility with a 10-year operating history

– Only facility of its kind in North America, capable of supplying

the electric vehicle market

– Located in Ontario, Canada, a location with exceptional

infrastructure and labour force in place

– Modular design to grow with the EV market

– 51% lower GHGs than Chinese peers, in part owing to

hydroelectric power grid

– Work commenced to commission lithium-ion battery recycling

line in 2023

Cathode materials require extremely

high purity levels – it all starts here

Source: Electra Battery Materials

NASDAQ: ELBM | TSX.V: ELBM 8

Phase 1 – Battery Grade Cobalt Sulfate

Commissioning in December 2022

Global battery grade sulfate capacity, 2023 (kt Co)

– China dominates global cobalt sulfate production with

80% market share China Ex. China

Huayou 30.0

– Finland hosts the only significant cobalt sulfate

refining outside Asia GEM 21.0

Kokkola 14.5

– Funded US$67 million capital program to achieve

Tengyuan 8.5

commissioning in December 2022

Jiana New Energy 8.0

– Electra will operate the only refinery in North America Umicore China 8.0

– 50 tpd cobalt hydroxide feed from Glencore and IXM Various 7.5

– Ramping up to 6,500t battery grade cobalt per year Greatpower 6.5

Electra 5.0 1.5 6.5

– Stratton Metals backstop purchase option while

Chengtun 4.5

offtake contracts are finalized Electra’s Canadian Refinery

Harjavalta/NN 2.4

– North American market share: 100% (100%1)

Olen 1.5 – Ex. China market share: 21% (26%1)

Jinchuan 0.5 – Global market share: 4% (5%1)

1. Based on 2022 forecast, when Electra’s refinery commences operations.

Source: Electra Battery Materials, BNEF

NASDAQ: ELBM | TSX.V: ELBM 9

Phase 2 – Recycling

Lack of hydrometallurgical refining capacity to support established network of battery shredders

Battery collection and shredding process

+ -

+ - + -

+ -

+ - + -

+ -

Pack removed Loaded for transport Transported to Discharged Stored Dismantled

from EV recycling facility

Source: Electra Battery Materials

Hydrometallurgical refining of “black mass” is superior to pyrometallurgy

Lithium and graphite not recovered

Higher yields, significantly lower energy intensity and lower GHG

emissions, compared to pyrometallurgical facilities

NASDAQ: ELBM | TSX.V: ELBM 10PHASE 2 – RECYCLING

Demonstration Plant in 2022; Commissioning in 2023

Recovery of nickel, cobalt, lithium, copper

and graphite

US$3M demonstration plant in 2022

using existing facilities and equipment

Commercialization in 2023

Hydrometallurgical process and

hydroelectric power ensures nearly zero

GHG emissions

Engineering work completed by Hatch

and met work by SGS Lakefield

Source: Electra Battery Materials

NASDAQ: ELBM | TSX.V: ELBM 11PHASE 2 – RECYCLING

Established Network of Black Mass Supply

Modular approach

– 25+ potential black mass partners

– Marubeni alliance to leverage Battery Materials Park

Ontario

network in Asia and elsewhere to

source battery material for Electra

– Module 1: Scalable and initially

targeting 4,500t black mass, treating

multiple types of black mass

– Module 2: Expected to treat constant

quality stream from cell partner

– Further modules will be designed

according to black mass types

Source: Electra Battery Materials

NASDAQ: ELBM | TSX.V: ELBM 12Phase 3 – Battery Grade Nickel Sulfate

Large nickel endowment but no battery grade nickel production in North America

Yellowknife

NWT

Thompson Nickel Belt

Manitoba

Ungava Peninsula

– Glencore and Talon collaborating with Electra on

Quebec government-sponsored nickel sulfate refinery study

Voisey’s Bay

Stewart

Newfoundland

B.C. – Sufficient nickel and cobalt supply potential in North

Duluth Complex

Minnesota

‘Ring of Fire’

Ontario

America to fully sustain region’s long-term requirements

Amos

Idaho Cobalt Belt

Quebec – Electra’s Battery Materials Park strategically located

Idaho Cobalt Camp

Ontario – OEM demand expected to fast-track North American nickel

Timmins

Ontario supply, pushing down long-term raw material costs

Sudbury Basin

Ontario

through economies of scale

Significant nickel

operations and projects – Carbon footprint of Canadian nickel sulfate production

Significant cobalt

operations and projects Battery Materials Park estimated to be up to 7x lower than conversion of

Ontario

Indonesian nickel deposits

Source: Electra Battery Materials, USGS

NASDAQ: ELBM | TSX.V: ELBM 13Phase 4 – Precursor Cathode Active Materials (PCAM)

Improved margins and lowed GHGs when PCAM is co-located with refining and recycling

Government of Canada and Government of Ontario sponsoring engineering studies Battery Materials Park concluded with PCAM production

for PCAM partnership realization

– Sulfate plants constructed at optimal industrial permitting and raw material feed

intersect

– Precursor plants ‘attracted’ to sulfate location as a result of lower raw material

feed costs

Battery Materials Park CAM

Refinery (Sulfates) Cells

PCAM Electric vehicles

Recycling Battery and EV Park

Harjavalta Industrial Park (Finland) Quzhou Industrial Park (China)

Source: Electra Battery Materials

NASDAQ: ELBM | TSX.V: ELBM 14Iron Creek Project Idaho, USA

Idaho Cobalt Belt

Critical Minerals in the USA Ram/ICP

Blackbird Salmon

Largest unmined cobalt resource in the

Iron Creek

U.S. (USGS 2017)

28

– America’s best opportunity to reduce

reliance of DRC and China for

cobalt supply

– High grade deposits amenable to

underground mining with a minimal 10 km 93

environmental footprint

Challis

– 53 Mlbs of Cu and 14 Mlbs of Co produced

historically

– Many prospects and targets in the

80 km x 20 km belt which have seen

minimal modern exploration

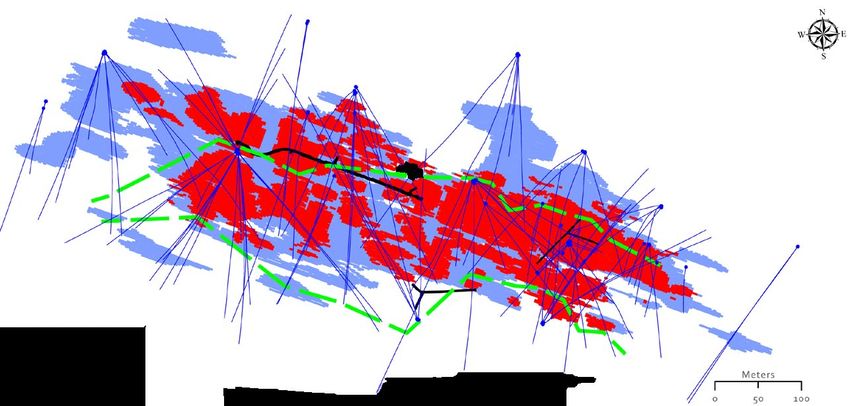

NASDAQ: ELBM | TSX.V: ELBM 16Iron Creek Resource Estimate

High grade, underground, open in all directions

43-101 completed in Resource remains Step-out and

2019 with 105 holes open along strike regional drilling

for 29,000m and down dip expected to grow

the size of the

deposit and identify

new targets Indicated Resource Inferred Resource

Collar and drill-hole trace Adit Surface projection of siltite contact

CoEq Cobalt Cobalt Copper Copper

Category Tonnes

(%) (%) (MIbs) (%) (MIbs)

Indicated 2,154,000 0.32 0.26 12.3 0.61 29.1

Inferred 2,676,000 0.28 0.22 12.7 0.68 39.9

Prepared by Mine Development Associates in compliance with National Instrument 43-101 (“NI 43-

101”) - available on SEDAR.

A cutoff grade of 0.18% CoEq is used for the resource calculation and deemed viable for potentially

NASDAQ: ELBM | TSX.V: ELBM underground minable material. %CoEq = %Co + (%Cu/10) 172021 Drill Program

– 2433 m drilled in 6 holes

– Targeted extensions of the mineral

system along strike

– Extended the mineral system to the

west, targeting extensions of both

the hangingwall Cu zone and the

footwall Co zone

– Extended the mineral system to the

east down dip targeting the deeper

portions of the Co zone

– Assays results:

– Five of six exploration holes drilled

intersected high grade cobalt

mineralization

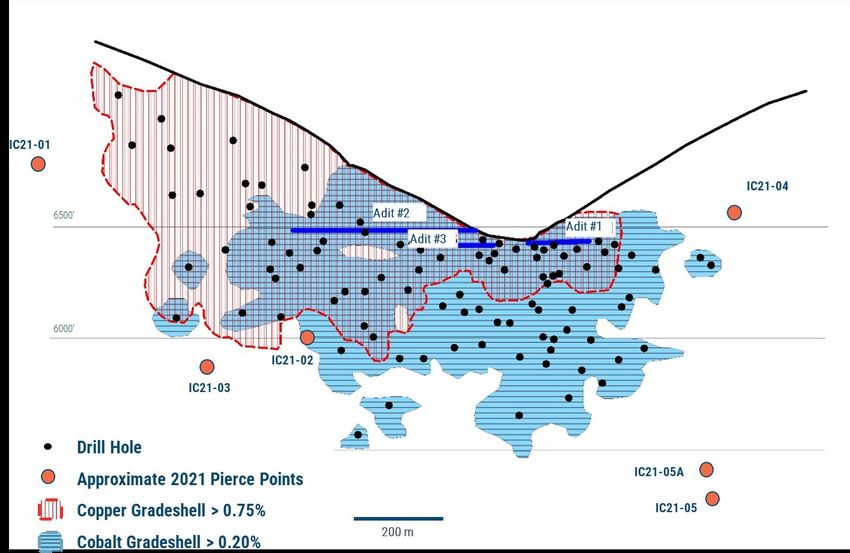

NASDAQ: ELBM | TSX.V: ELBM 18Additional Targets

Ruby Zone and other targets support a regional program to identify new targets

Iron Creek, West Fork and Redcastle properties – 2021 Acquisitions

Challis Volcanics

Banded Siltite

Argillite-Siltite

Coarse Siltite

Interpreted Contact

Interpreted Fault

Bedding Orientation

Iron Creek Co-Cu Resource

Surface Projection

Land package more than tripled in 2021 to 23 km2 with acquisition of West Fork and Redcastle properties

NASDAQ: ELBM | TSX.V: ELBM 19Valuation and Corporate Information

Cobalt Sulfate Plant – Production and EBITDA Profile 1

Production (tonnes of cobalt) EBITDA (US$ millions) Trading – EV to forward EBITDA Key Assumptions

6,500

40.1 Cobalt sulfate price of

5,750 $37.25/lb (spot)

34.4

4,375 Cobalt metal price of

8-10x $34.33/lb (spot)

24.1

Cobalt hydroxide payability

of 89% (spot)

Commissioning

Commissioning

3-5x

Operating costs and

recoveries in line with

internal technical estimates

(commercially sensitive)

2022 2023E 2024E 2025E 2022 2023E 2024E 2025E Chemical peers Electra Current

1 Commissioning in December 2022 with ramp up to 5,000 tpa run rate by June 2023 and 6,500 tpa run rate by July 2024.

NASDAQ: ELBM | TSX.V: ELBM 21Electra Strategic Plan – Ontario Battery Materials Park

Cobalt Sulfate Plant Battery Recycling Nickel Sulfate PCAM

Metal Production

5,750 6,500 6,500

4,375

2023 2024 2025 2026

NASDAQ: ELBM | TSX.V: ELBM 22Share Structure

NASDAQ: ELBM; TSX-V: ELBM Research coverage

Share Price (May 10, 2022) C$4.79

52 Week High C$7.65 Target Price

52 Week low C$4.51

Average volume (30-day) 190,926 U$10.40

Capitalization Million

Shares Outstanding 33.0

U$11.00

Options (av $5.94) 1.0

Warrants (av $7.56) 1.3

Fully-Diluted Shares Outstanding 35.0 U$11.52/C$14.40

Market Capitalization C$149.66

Convertible Debt (6.95%) US$36.0

Average target price U$10.97

Working Capital (Dec. 31, 2021) C$69 (incl. govt commitments)

NASDAQ: ELBM | TSX.V: ELBM 23Why Electra Battery Materials?

– North America needs precursor cathode active

materials (PCAM) to support new cell plants

– Electra can deliver this faster than anyone due to

– Existing permitted hydrometallurgical site

– 10 months from commercial production

– Proximity to nickel feed; established black mass

sources

– Infrastructure

– Hydroelectric power

– Peer-leading ESG commitments through recycling, a

low carbon footprint, traceability and a shortened and

secure domestic supply chain

NASDAQ: ELBM | TSX.V: ELBM 24Environmental, Social & Governance

Our Approach to ESG

Our mission is to produce the world’s most sustainable

battery materials

Low Responsible Strong governance

Environmental Sourcing and social

Footprint responsibility

NASDAQ: ELBM | TSX.V: ELBM 26Low Environmental Footprint

We take a proactive, risk-based approach to Life Cycle Assessment, Cobalt Refinery

environmental management, with robust

measures that help ensure we minimize our

environmental impact, while ensuring the viability 51%

of the environment for future generations. In line lower CO2 emissions1

with our overall approach to responsible mining, 30%

the 'zero harm' principle will guide our approach 73%

lower eutrophication

to environmental management lower water consumption1

potential1

At Iron Creek, underground ore sorting is one Removes ~1,500,0002

example of how we are working to reduce our combustion engines from the road every year1

environmental footprint (concentrate the ore for

shipping and processing, fewer trucks on the CO2 reduction of

road and less processing energy = lower 3m tonnes/year1

greenhouse gas emissions)

1. Based on a peer comparison life cycle assessment conducted by Minviro Ltd.; 2. Assuming 50kWh per unit high-nickel NCM

Source: Electra Battery Materials

NASDAQ: ELBM | TSX.V: ELBM 27Onshoring’s ESG Advantage

Electra’s Phase 1 has 40% lower CO2 freight emissions compared to shipments from China

Sea freight, Durban to Shanghai: 1.2t CO2

Sea freight, Shanghai to Vancouver: 0.9t CO2

Road transport, Vancouver to Kentucky: 0.6t CO2

1.5 tonnes of CO2

per container

2.7 tonnes of CO2 per container from China USA from Electra

China

Pacific Ocean

Sea freight, Durban to Montreal: 1.2t CO2

Existing cell plant Future cell plant Road transport, Montreal to Electra plant: 0.1t CO2

Road transport, Electra plant to Kentucky: 0.2t CO2

Pilot cell plant Electra Battery Materials Park

NASDAQ: ELBM | TSX.V: ELBM 28 28Responsible Sourcing

We commit-as a priority-to

We have a responsibility to

prevent the use of child labor in

respect and protect stakeholders

all its forms, whether directly

within our sphere of influence.

through our business' activities

This includes our direct influence

or indirectly through our supply

on human rights as well as

chains. By embedding child

human rights within our supply

labour prevention provisions into

chain. This is in line with the

our business conduct, we can

United Nations Guiding Principles

help ensure that our cobalt is

on Business and Human Rights.

free of such abuses.

NASDAQ: ELBM | TSX.V: ELBM 29Strong Governance and Social Responsibility

Community Relations Environmental, Social & Governance

We will be a catalyst for local community

and economic development Electra tree planting initiative

(Ontario, Canada)

We strive to provide regional

economic opportunities, local employment,

local procurement opportunities,

infrastructure availability, and tax revenues for

service implementation

Health & Safety

Our approach to health and safety is guided by

the 'zero harm' principle, where every employee Wild Basket Initiative (Plant

goes home safely each and every day. We will Study): Timiskaming First Nation

work to embed a strong safety culture into all our and Electra Team (Ontario,

operations Canada)

NASDAQ: ELBM | TSX.V: ELBM 30Market Data

Electric Vehicle Market Developments

New models expected to drive strong sales in 2022; battery shortage remains limiting factor

Global electric vehicle sales (monthly units)1

1,000,000 Global annual sales (million units)

900,000

800,000

700,000 +101%

600,000 6.4

500,000

400,000

300,000 +52%

200,000

+12% 3.2

100,000

0 2.1

1.9

2018 2019 2020 2021 2018 2019 2020 2021

1. New Energy Vehicle (NEV) sales, including Battery Electric Vehicles (BEVs) and Plug-In Hybrid Electric Vehicles (PHEVs)

Source: Electra Battery Materials, Rho Motion

NASDAQ: ELBM | TSX.V: ELBM 32Electric Vehicles | Extraordinary Growth Trajectory

EV sales to 2030 (million units) EV market penetration to 2030 (%)

Global electric vehicle sales are forecast to increase ten-fold from 3.2m Global EV market penetration rates forecast to rise from 4% in 2020 to

units in 2020 to 36.0m units in 2030. 30% by 2030.

Battery Electric Vehicles (BEV) 36.0 New Energy Vehicles (PHEV & BEV)

Plug-In Hybrid Electric Vehicles (PHEV) Internal combustion engine vehicles (ICEV)

31.2

+21% 26.8 1% 1% 1% 2% 2% 4% 6% 7% 9% 11% 14% 17% 19% 22% 26% 30%

CAGR

22.9

19.3

16.1

13.2

10.7

8.5

6.4

3.2

1.9 2.1

0.5 0.8 1.3

2015

2016

2017

2018

2019

2021

2022

2023

2024

2025

2026

2027

2028

2029

2015

2016

2017

2018

2019

2021

2022

2023

2024

2025

2026

2027

2028

2029

2020

2030

2020

2030

Source: Electra Battery Materials, BNEF

NASDAQ: ELBM | TSX.V: ELBM 33Cobalt and Nickel Demand

Higher energy density chemistries lead to stronger nickel than cobalt growth

Global: Key materials demand from NEV segment,

2018-2021 (k tonnes)1

Distribution of cell chemistries

Nickel-cobalt bearing lithium-ion batteries remain dominant chemistry

Cobalt demand growth from electric vehicle segment healthy, but outpaced by nickel

Cobalt +69%

demand growth due to higher nickel chemistries becoming more popular

37.5 Lithium-iron-phosphate (LFP) batteries will remain relevant in entry-level, short-range

+44%

vehicles but NCA/NCM chemistries will continue to dominate in the future

+26%

22.1

15.4

12.2

14% NCA

20%

30% 28%

2018 2019 2020 2021 9% 17% NCM811

3% 5%

9% 8% NCM712

+89%

Nickel 35%

24%

156.5 41% 29% NCM622

+52%

+54%

82.9 20% 15% 12% NCM523

54.6 14% 3% NCM111

35.4 7%

17% 4% 17% LFP

13% 8%

2018 2019 2020 2021 2018 2019 2020 2021

1. Based on NEV sales rather than production; actual demand numbers higher due to length of battery supply chain. Source: Electra Battery Materials, Rho Motion

34Lithium-ion Battery Market Share by Chemistry

Non-cobalt chemistries not viewed as major threat

– High-nickel NCM

batteries forecast to

remain dominant

– NCM chemistries will

continue to contain cobalt

– Innovation in nickel-cobalt

cells ongoing; energy

densities in NCM cells

will remain significantly

higher than alternative

commercial cell chemistries

Source: Benchmark Minerals, September 2021; Nickel Institute June 2020

NASDAQ: ELBM | TSX.V: ELBM 35Electra Battery Materials NASDAQ: ELBM; TSX-V: ELBM info@ElectraBMC.com +1.416.900.3891

You can also read