Capital and Investment Strategy 2022/23 - Cornwall Council

←

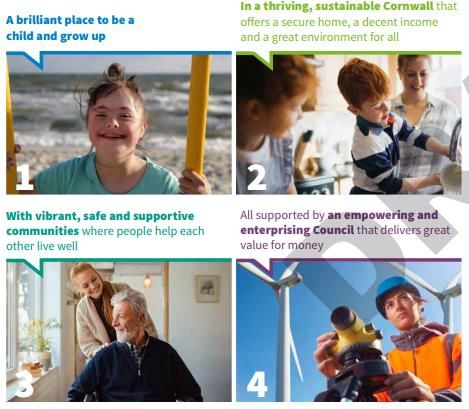

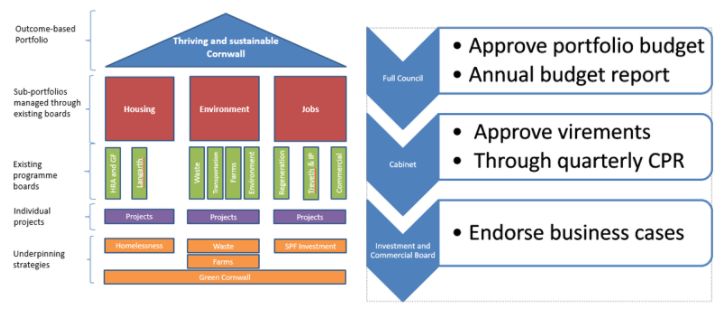

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Information Classification: PUBLIC Capital and Investment Strategy 2022/23

Information Classification: PUBLIC Contents 1. Introduction 2. Background and Council priorities 3. Prioritisation policy 4. Governance, Scrutiny and Assurance process 5. Capital Programme 6. Loans, guarantees and non-treasury investment 7. Capital Indicators 8. Asset Management 9. Risk Management 10. Knowledge and Skills Appendices 1. Capital Programme (by Outcome) 2. Capital Financing 3. Capital Expenditure

Information Classification: PUBLIC

CORNWALL COUNCIL CAPITAL STRATEGY 2022/23 – 2025/26

1. Introduction

1.1 The capital strategy sets out the direction for the Council’s capital programme

management and investment decisions in support of our outcomes. It sets out

the principles for prioritising our capital investments, the governance, scrutiny

and assurance process. It also provides an overview of the asset management

process and approach to risk management.

1.2 The requirement for councils to prepare a capital strategy is set out in the

Prudential Code for Capital Finance in Local Authorities (2017), and this

document has been produced in accordance with the latest guidance.

1.3 The Prudential Code is changing, with formal requirements to be applied from

2023/24. Through 2022/23 the changes can be viewed as guidance allowing

for a transition period. As the capital programme is forward looking for several

years it is advisable to take on board the guidance and incorporate into this

year’s strategy. The changes are explained further in section 5.6. In line with

updated guidance the Capital Strategy sets out plans to align investment

activity to support Cornwall Council’s functions, identify the borrowing

requirement and not invest for purely commercial return.

1.4 The capital strategy forms an integral part of the Council’s medium to long term

financial and service planning and budget setting process as it can assist with

invest to save activity and will impact the revenue budget through the debt

repayment. It is also fundamental to the Treasury Management Strategy in

relation to investment requirements and decisions.

1.5 Due to several factors including geographical location, the state of the

economy, the supply chain and grant conditions, the ability to deploy capital

expenditure within the county does have a limit and it is imperative that the

Council has a well planned capital investment programme which is deliverable

and allows the supply chain to plan accordingly.

2. Background & Council Priorities

2.1 Historically the Council had a very bottom up approach to capital with individual

schemes being the driver for the overall programme, regardless of size or

scope. This created limitations and did not focus on the level of investment that

the Council can prudently afford, realistically deliver, and support the delivery

of outcomes. In 2021/22 the Capital Strategy introduced a more strategic

approach through a portfolio approach.

Information Classification: PUBLIC

2.2 The Council Business Plan has focused delivery through four priority outcomes.

The management of the capital programme will mirror this with a portfolio for

each outcome. Alignment of the capital programme to Council priorities will

ensure that schemes are approved which clearly demonstrate delivery of key

objectives. There will be a consistent approach across the Council in relation to

scheme approval and funding. The capital programme can support the

development of the capital public works supply chain and the Council’s

commitment to increase spend with local suppliers.

2.3 A portfolio is defined as a grouping of programmes and projects to deliver an

organisation’s strategic objectives. In this year’s capital strategy the portfolio

approach is strengthened to support the four business plan outcomes:

2.3 Each portfolio will consist of individual projects or groups of projects managed

on a programme basis. Portfolio boards will be required to manage programmes

and projects through a clear and transparent phased approach that is

consistent with best practice and the Treasury green book. The portfolio

management will be designed in line with the Outcome Delivery Plans

Example Portfolio structureInformation Classification: PUBLIC

2.4 The Outcome focus that the Council has adopted is also to maximise value for

money and remove silo working. In terms of the capital programme this

approach may create the opportunity for previously siloed service projects to

benefit from wider engagement. As with all aspects of the Council’s finances

the capital programme also needs to work efficiently. In this regard the Council

will have clear and affordable prudential indicators set as targets to frame the

size of future capital programmes to ensure the programme is affordable in the

short and long term.

2.5 This approach will require programmes and projects to be developed to a higher

level of detail before they progress to full approval and enter into the

construction phase. In doing so business cases need to be prepared with

reference to:

• HM Treasury Green Book (Green Book)

• Construction playbook

• Best practice project management

• Internal audit findings

3. Prioritisation Policy

3.1 When there are limited resources, not all proposals can be supported and

delivered. To assist the prioritisation of limited resources new proposals will

need to consider their outcomes against the following criteria:

• Strategic fit, delivery of Council outcomes;

• Climate change implications;

• Impact on the Council’s revenue budget;

• Deliverability;

• Project risk;

• Safeguarding of existing assets;

• Health and safety implications;Information Classification: PUBLIC

• Funding (including external funding leverage) and affordability.

3.2 Portfolios will need to assess new projects and prioritise within existing

resources. For 2022/23 the Council has no provision for additional borrowing.

• No new projects to start that requiring Cornwall Council resources

• Priority need identified that is not already in the programme requires

reallocation from existing portfolio resources. This will require other

projects to stop or find alternative external funding.

• Projects applying for external grants that require Cornwall Council match

resources must identify the match element from existing portfolio

budget prior to submitting the grant bid. If the match is not identified

and agreed through Outcome Delivery Boards prior to submission the

grant application will not be supported by the S151 Officer. This will

result in the project not progressing and the grant being returned to the

funding body.

• Projects with 100% external funding, requiring no match from Cornwall

Council, will be assessed and approved through standard governance.

• Grant funded projects carry the risk of cost over run and scope changes

that the Council is liable for. Any project costs due to contract, inflation

or project scope changes will need to be met from the portfolios existing

budget.

4. Governance, Scrutiny and Assurance Processes

4.1 Governance processes are in place to ensure capital investment decisions

(including loans and grants) are made legitimately, transparently and deliver

the priorities of the Council. No capital expenditure can be incurred without

formal approval and inclusion in the capital programme.

4.2 The capital programme is agreed annually by Full Council as part of the budget

setting process. Full Council will set the size of the capital programme, based

on the affordability indicators. Allocation to Outcome capital portfolios will be

set as part of the budget process. This will include the activity of the Council’s

Group of Companies.

4.3 Projects and programmes will need to be assessed through a business case by

the Outcome Delivery Board. The Outcome Delivery Board will be responsible

for allocating the portfolio capital budget to projects and programmes to

support the Outcome Delivery Plan. Review, prioritisation and allocation of

capital portfolio resources will be ongoing through each financial year.

4.4 The process is the same for Treveth and other Council companies. The Business

Plan will be approved by Cabinet. Any capital requirement will be reported to

Full Council for approval into the capital programme. Due to the timing of the

group of companies’ business planning cycle if the capital requirements are notInformation Classification: PUBLIC

fully assessed for inclusion in the February budget report they will be presented

to Cabinet in March, and to Full Council in the next capital report for inclusion

in the capital programme. The Outcome Delivery Board responsible for

commissioning the activity from the group company will review business cases

and approve allocation of budget to individual projects or programmes.

4.3 The capital programme will consist of two separate categories and scheme will

progress through the categories in line with the gateway process highlighted

above. The two categories are:

• Approved schemes: these are projects / programmes that are already

in delivery or ready to be delivered;

• Indicative schemes: these are projects / programmes that have been

approved at Full Council, which demonstrate alignment with the Council

Outcomes but only have a strategic or outline business case. Additional

work is still required to demonstrate that they are deliverable and

affordable. These schemes can’t progress to the ‘approved’ category of

the capital programme until a detailed business case has been approved

by ICB. Indicative scheme development needs to be funded from

revenue resources and be planning for future years (e.g. 2024/25 on).

4.3 Proposals will follow a gateway process, ensuring Treasury Green Book

compliance, and must be successful at each gateway to proceed to the next

before they achieve full approval to the capital programme, and are allowed to

commence delivery. The Investment and Commercial Board (ICB) will manage

this gateway approval process. The table below sets out the different phases

of activity and gateways:

Project Phase Opportunity Policy Delivery Phase Managed and Completion

Phase Formulation Construct Phase

Phase (Phase 3) (Phase 4)

(Phase 2)

(Phase 1)

HM Treasury Strategic Outline Outline Business Full Business Case

Green Book Case Case

Procurement Idea Define Procure/ IDA Manage Complete

LifecyleInformation Classification: PUBLIC

Types of Opportunity Business Delivery – Contract and Close

activities framing phase Justification publication, Implementation

selection, • Deal with

• Development evaluation, and • FBC to be defects period

of business award. approved • Close contract

Pipeline need (transition and move to

activity •

• Articulation Sourcing between operational

of outcomes Strategy Phase 3 and stage

• Category (make, do, Phase 4) • Handover

Strategy and buy) • Award and process and

should costs • Specification, sign asset transfer

• Pre tender contracts • Project /

engagement documents underpinning Programme

with the and delivery close and benefit

market contracts. approach realisation

• SOC and • Market • Manage and

formally engagement monitor

added to the • OCB and performance

pipeline preferred • Alignment

• Budget option and reporting

approval identified through the

• Set up of • Refinement project,

project, of budget programme,

programme assumptions. portfolio

governance • Enact governance

to deliver procurement to deliver.

/ IDA/ other

delivery

route process

• Prepare FBC

following

outcome of

the delivery

route

Governance ICB – Gateway ICB – Gateway ICB – Gateway ICB – Project Close

gateway Approval of SOC Approval of ICB Approval of FBC

approval (Officer

Governance)

Cabinet (Political

Approval of the

SOC andInformation Classification: PUBLIC

incorporation into

the MTFP)

Relationship Pipeline SOC required for Refinement of Full draw down of

with the schemes approval in the assumptions in funds in the MTFS

Budget developed MTFS. outcome portfolio for the

process into SOC. budgets. implementation

SOC only included

if affordable

Outcome within Outcome

board to portfolio total.

prioritise

within budget New borrowing

resources. and external

grant increases

New projects managed through

exceeding the Headroom

Outcome budget.

budget to be

considered for

Headroom

allocation

4.4 The gateway process will need to align with other Council processes and the

management of the capital programme. This is set out in the diagram below:

4.5 The capital financing budget will take into account the capital programme

(approved and indicative) funding requirements.

4.7 The capital programme will be governed by Outcome Delivery Board. The

Outcome Delivery Board should meet to review the additions, reductions,Information Classification: PUBLIC

movements and delivery of their capital programme portfolio on a regular basis

proportionate to the size, scope and risk of their delivery plan. The function of

the Outcome Delivery Board in relation to the capital programme will be to have

oversight, stewardship, provide strategic direction and approve the inclusion of

new schemes supported by a business case. They will be responsible for

prioritising and challenging the delivery of individual projects and programmes

by:

• ensuring that risks are managed and mitigated;

• spend is in line with the approved budget and pressures identified;

• deliver the programmes and projects in accordance with the detailed

business case;

• recommend the reallocation of approved capital budget in line with

emerging priorities if required.

• take mitigating action to stop or slow projects in order to operate

within the approved portfolio target.

4.8 The Outcome Delivery Board will also have challenge and input into new capital

projects. No capital project should be considered for the gateway process

without the support of the Outcome Delivery Board.

4.9 Investment and Commercial Board (ICB) will be responsible for the gateway

approval process outlined above.

4.10 Capital Oversight Group (COG) will take senior ownership of the capital

strategy. The focus of COG will be to ensure that resources are used to best

effect, review pipeline development in advance of the budget process, monitor

the impact of the programme on debt indicators, capital receipts and

affordability.

4.11 The responsibilities of the Outcome Delivery Board and COG do not detract

from the individual accountabilities of those officers responsible for the

development, implementation, and completion of the projects within the capital

programme. On completion of significant capital projects or programmes, the

Senior Responsible Officer should undertake a post scheme evaluation. They

should assess if the project has delivered its objectives and outcomes,

suitability of design and construction, affordability, identify good practice and

lessons learnt.

4.12 Annually as part of the budget setting process, all projects and programmes

will be reviewed to ensure they continue to contribute to the Council’s Priorities

and remain affordable. Any that fail to satisfy these conditions will be removed

from the programme with the residual budget allocated to the Council

headroom capacity.Information Classification: PUBLIC

4.13 A quarterly capital report will be update Cabinet and Full Council on the

progress and delivery of the approved capital programme and any variations

for which agreement is sought.

5. Capital Programme

5.1 Cornwall Council’s approved capital programme and funding set out by

portfolio below:

Summary of existing Capital Programme

2025/26

2021/22 2022/23 2023/24 2024/25 Total

& Beyond

(£m) (£m) (£m) (£m) (£m)

(£m)

Existing programme

Empowering and enterprising Council 7.277 13.161 12.784 10.460 10.099 53.782

A thriving, sustainable Cornwall 275.138 349.674 299.820 170.584 106.957 1,202.172

A brilliant place to be a child and grow up 25.973 42.769 15.736 10.119 - 94.597

Vibrant, safe, supportive communities 4.135 9.819 11.749 5.024 7.010 37.737

Total existing programme 312.523 415.423 340.089 196.187 124.065 1,388.288

Existing programme - Funding

Revenue 5.686 5.055 4.647 4.732 5.740 25.860

Prudential Borrowing 167.543 210.436 202.934 116.555 83.251 780.718

Capital Receipts 11.359 17.884 11.895 2.595 6.687 50.420

Specific Reserves 34.563 47.483 29.098 19.630 19.854 150.628

Grants & Contributions 93.372 134.565 91.515 52.675 8.534 380.662

Total existing programme 312.523 415.423 340.089 196.187 124.065 1,388.288

5.2 The table illustrates how the Council proposes to direct c£1.4bn of capital

resource towards its strategic objectives over the life of the Medium-Term

Financial Plan.

5.3 As the Council transitions to operating through Outcome Delivery Plans

alignment of activity will release further resources to create £50m headroom

capacity to support new starts and provide a contingency allowance. This will

be allocated through the annual budget process.

5.4 There is no further capacity in the programme for new projects that require

prudential borrowing in 2022/23. Outcome capital portfolios are expected to

operate within their approved budget and will require projects to be prioritised.

5.5 It is expected that projects with 100% external funding will be added to the

programme once business case requirements are met:

• Strategic fit

• Investment appraisal

• Financial impacts

• Commercial approach

• Management resources

5.6 External funding should only be applied for to support identified priorities and

activities in the Outcome Delivery Plan. On this basis any external fundingInformation Classification: PUBLIC

awarded to support existing projects and priorities will require the Outcome

capital portfolio to release Council resources equivalent to the external funding

value to the Council Headroom budget. The Outcome capital portfolio will have

the same allocation to deliver the identified and agreed projects, only the

funding will change. This will allow the Council to build up additional headroom

for forward planning and annual allocation to Outcomes Delivery Boards in line

with revised Delivery Plans.

Capital Council Council

Revised

Capital Portfolio Programme Resource Resource

Programme

£m £m £m

£m

Outcome Portfolio 1,000 800 1,000 795

Council Headroom 50 50 55 55

Total 1,050 850 1,055 850

5.5 Projects that are income generating or provide an invest to save option will be

considered on the basis that the income or saving created offsets the cost of

borrowing.

5.6 The Capital Strategy reflects the categorisation of investments in line with

the Prudential Code.

• Service delivery investment is the primary function of the Council’s

capital programme to deliver public services such as housing,

regeneration and local infrastructure. In some instances, these

investments may generate a small return, which can be used to help

pay for borrowing. Service investments are made with statutory

powers and service outcomes as the first requirement. These

investments are from budgeted Council resources e.g. capital or

revenue.

▪ Asset build and refurbishment

▪ Financial instruments e.g. an investment fund that supports

housing or shares in a regeneration project

▪ Loans

▪ Grants

▪ Non – Treasury investments. Linked to Service delivery but

utilise the Council’s cash balances. Non-Treasury investments

can include loans to community organisations for cash flow

assistance while waiting for grants to be paid to them.

• Treasury management investments utilise the Council’s cash

balances and are governed by the Treasury Management Strategy. The

aim of Treasury investments is to ensure there is sufficient cash for the

Council to operate and when the Council needs to take out borrowing.Information Classification: PUBLIC

• Commercial return given the level of risk associated with commercial

investments and the update to the Code the Council has not, and will

not, invest for purely commercial return.

6. Loans, guarantees and non-treasury investments

6.1 The Council may consider some investments that fall into a non-treasury

investment category. The Council has the power to lend monies to third

parties subject to a number of criteria. These are not treasury type

investments, rather they are service delivery policy investments e.g. to

support local business, for regeneration and economic development.

6.2 Loans of this nature will be approved in line with the Council’s Financial

Regulations and only after relevant due diligence has been undertaken. There

are a number of instances where this may occur, and it is deemed good

practice that there are is a framework and criteria that the Council sets and

uses to manage these arrangements.

6.3 Non-Treasury investments utilise the Council’s cash balances, but the

organisations invested in do does not meet the Treasury investment criteria for

risk rating, liquidity or security.

6.4 The type of loans/investments covered by this framework are:

• Parish & Town Council Loans not covered by Treasury Strategy (i.e. over

5 Year)

• Council Owned Companies Loans

• Council Owned Companies Equity

• Charity and not for Profit Community Interest Companies

• Local Businesses

• National Businesses as part of a service provision contract or partnership

The framework should set the requirements relating to:

• Criteria for Assessment

• Security

• Financial Limits

• Method of Interest Rate Calculation

Criteria for Assessment

6.5 All proposals will need to be assessed and a risk or rating category allocated.

In most cases it is unlikely that the organisation involved will hold a formal

credit rating as issued by one of the three credit rating agencies, hence the

assessment will need to be manual and based on a financial analysis of the

organisations financial status which will involve analysis of recent accounts andInformation Classification: PUBLIC

credit ratings. The assessment will need to identify whether the organisations

financial position is:

• Strong

• Good

• Satisfactory

• Weak

• Bad/Financial Difficulty

Security

6.6 In all instances security should be sought as this is a form of collateralisation

that ensures the Council is protected in the event of a default. Security should

be a first charge against the asset and should be against an asset that can be

made liquid fairly quickly and without significant effort. Security will not be

obtainable in all instances, and in these cases the rating category set out above

becomes increasingly important. In addition, the level of security is a factor in

setting the interest rate.

Financial Limits

6.7 The financial limits will be based on both an individual organisation, the type of

organisation and the Council’s overall risk appetite. In terms of an individual

organisation’s limit this will be generic for all organisations in terms of total

exposure, there will need to be part of the assessment process an analysis of

an acceptable level for each specific application if it’s within the overall total.

Interest Rate Calculation

6.8 Interest Rates chargeable will need to reflect base and market rates and will

always vary. For short term loans (< 3 years) the rate can be fixed for the

duration of the loan and should be calculated on the forecast rate at the halfway

duration period. For loans of a longer duration there should be a clause built

into the loan agreement to review rates on a periodic basis and should be

calculated based on the rate at the commencement of the loan.

6.9 The rates set should take into account the Council’s cost of securing similar

length duration money as this is the opportunity cost of using the Council’s

surplus cash, the risk and level of security that is obtained and a 25bps margin

added on to cover the cost of administration and potentially providing for

defaults. The table below sets out the framework for calculating interest rates:Information Classification: PUBLIC

Loan Rates per annum

Financial Rating / Rating

Security

Category

High Moderate Low

75 -100% 25-74% 60%)

59%)

Strong (AAA-A) 60 75 100

Good (BBB) 75 100 220

Satisfactory (BB) 100 220 400

Weak (B) 220 400 650

Bad/Financial Difficulties (CCC

400 650 1000

& Below)

LGD is the Loss Given Deafault - expected loss in % terms of the debtors exposure

taking into account recoverable amounts from collateral and the bankruptcy of

assets (Inverse of Collateral/ security)Information Classification: PUBLIC

6.11 The reference rate is published by the European Commission and is based on

each individual Countries IBOR (Interbank Offered Rate). For example, if IBOR

was 1% and an organisation was deemed to have normal collateralisation but

a weak credit rating then 400bps would be added to the IBOR rate giving a

minimum interest rate of 5% p.a.

Criteria and Limits

6.12 The table below sets out the limits and criteria for the making of loans or

investments that are non-treasury. As this is the first attempt at introducing

such a framework it will need to be kept under review to see if it delivers the

outcomes required (the table has been updated to reflect the lending to Treveth

as part of the updated financial model)

Maximum Total

Total Exposure

Organisation Rating Criteria Security Period

Exposure per to

Organisation Category

Parish & Town Councils Manual Assessment N/A £250,000 5 - 25 years £10m

Council Owned Companies

See Treasury Management Strategy

(Cash Flow revolving Loans)

Council Owned Companies

Manual Assessment N/A £250M Upto 50 Years £300m

(Term Loans)

Council Owned Companies

Manual Assessment N/A £50m N/A £100m

(Equity)

Charity & not for profit High £5m Up to 7 Years

Financial Rating /

Community Interest

Manual Assessment Medium £2m Up to 5 Years £15m

Companies

Low £1m Up to 2 Years

High £2m £15m

Financial Rating /

Small Local Business (SME)

Manual Assessment Medium £1m

Low £500,000

Length of Contract

National High £10m

or 7 years

Organisations/Contractor

Financial Rating / Length of Contract

(only as part of Medium £5m £25m

Manual Assessment or 5 years

Procurement

Contract/partnership) Length of Contract

Low £2.5m

or 3 years

(Changes in bold)

6.13 Financial Regulations All loans and investments must comply with the

Council’s financial regulations, for ease the approval limits for loans covered

by the financial regulations are:

• For amounts up to £1m, the Section 151 Officer can authorise where

there is no adverse impact on Council Policy or service delivery and

can be funded from approved budgets.

• For amounts over £1m and funded from existing resources the

Cabinet.

• For amounts of £1m to £5m which are not funded from existing

resources the Cabinet.Information Classification: PUBLIC

• For amounts over £5m and not funded from existing resources the

Cabinet can authorise but only after Council has made specific

provision in the capital programme/budget

7. Capital Indicators

7.1 The overall size of the capital programme is in part driven by third party funding

from grants and contributions that align with the Council’s priorities. In addition

to external funding the Council needs to set targets for the level of borrowing

it can afford to ensure that short term and long term debt repayments are

affordable at a rate that allows the Council to continue to invest, maintain and

develop new and existing assets into the future.

7.2 A further consideration is that a proportion of the programme funded by

borrowing relies on income generated by the project to repay the debt; in the

main this relates to Treveth housing and employment space investments but

may include other areas such as low carbon initiatives. To ensure compliance

with the prudential code for capital it is important that some control is exercised

around the proportion of debt that is being serviced from income. The debt will

continue to need to be serviced for many years, hence there is a need to ensure

income streams are robust, sustainable and manageable if there is downturn

in income.

7.3 The capital strategy therefore outlines that the following indicators are adopted

for the general fund:

7.4 The current Council asset to debt ratio is 1.7x (as at 31 March 2022) and will

continue to be monitored as part of the regular review of the capital strategy.

7.5 The capital programme can also be funded by capital receipts, generated from

the sale of assets. Capital receipts are a valuable resource as it removes the

need for borrowing and the associated cost and long-term commitment.

Ensuring that all capital receipt opportunities are fully captured is a critical

element of managing the Council’s capital programme. Therefore, as part of

introducing a new approach to capital for the Council, a capital receipt target isInformation Classification: PUBLIC

to be set as part of the capital strategy. The target is currently set at £10m and

will be reviewed at 6 month intervals.

7.6 The Housing Revenue Account (HRA) and Investment Programme will be

included in the calculation of the Council limits above, but also have separate

criteria and indicators which will be assessed through their governance and

approval process.

8. Asset Management

8.1 Cornwall Council’s Asset Management practices are to balance costs,

opportunities and risks against the desired performance of our assets to

achieve corporate objectives, and optimise the delivery of value.

8.2 The objective of Cornwall Council Asset Management approach is to apply a

systematic approach to the governance and realisation of value from the

tangible assets (physical objects such as buildings or equipment) and to

intangible assets (such as human capital, intellectual property and/or financial

assets).

8.3 Cornwall Council recognises the benefits and objectives of Asset Management

to include:

• Enhanced satisfaction from improved performance and control of non-

performance;

• Improved health, safety and environmental performance;

• The ability to demonstrate coherent and sustainable planning and

investment decisions;

• Demonstrate evidence of controlled processes to meet legal,

regulatory and statutory requirements alongside strong returns on

investment; and

• Improved risk and opportunity management with corporate

governance and clear audit trials.

8.4 A process of physical asset management has started by forming an initial

systematic base line approach to developing, operating, maintaining, upgrading

and disposing of physical assets in the most cost-effective manner.

Real Estate

8.5 The Council has a real estate portfolio of around 15,000 assets of land and

buildings (including Council dwellings), with a book value of c£1.4bn that are

held mainly for operational service requirements and administrative buildings.

8.6 Under the Estate Transformation Programme the Council is developing the

strategic approach for managing the portfolio of estate assets. To achieve a

robust and sustainable cycle of real estate asset management and achieve

strategic alignment with corporate objectives, a corporate landlord real estate

management approach has been developed.

8.7 The aim of corporate landlord is to guide the future shape and direction of the

property estate management to ensure that the portfolio of land and buildings

is optimally structured to perform and deliver corporate and service aims.Information Classification: PUBLIC

8.8 By applying an effective real estate asset management strategy, the benefits

will include:

• Assets aligned with financial objectives and service aspirations and

customer needs;

• Devolution of services to the locality with community asset transfer

where appropriate;

• Ensuring the right mix of property interest to provide both flexibility

and surety;

• Integrated service delivery through co-location with partner

organisations, improving property efficiency, choice and accessibility

for customers;

• Cooperative estate service provision driving economies of scale;

• Improving the sustainability of the corporate estate;

• Better targeting of funding by reducing revenue cost and identifying

long term capital investment needs;

• Challenging the retention of assets, introducing innovative non-asset

dependent service delivery models; and

• Ensuring appropriate long-term investment in maintenance and

statutory property compliance.

Real Estate Asset Management

8.9 The role of asset management is in essence to become a service property

partner to implement a centralised and standardised asset management

practice across all service estates to ensure there is alignment of estates to

services’ priorities, corporate estate financial targets, and RICS Public Sector

Asset Management guidelines and standards across the full estate.

8.10 The primary aim of asset management will be to act as property partners for

directorates, to set five year service estate improvement plans that drive better

use of space for each service, whilst managing estate in line with the overall

estate financial plan, and to ensure properties are managed to industry

recognised standards.

8.11 The Asset Management Group (AMG) undertakes the co-ordination of

purchases, reallocations, and disposals of properties.

Capital Projects Team

8.12 The Capital Projects Team, part of the Finance & Commercial Service, is the

main delivery route for major construction and infrastructure projects within

the Council. This team provides support and assistance in all aspects of

planning and delivering major projects from inception and feasibility through

to the final handover, including the management of risk and project budgets.

8.13 Early engagement with the team is imperative to ensure planned projects are

viable and robust.Information Classification: PUBLIC

Roads and Highways

8.14 Cornwall Council adopts an Asset Management approach to the management

of its highways assets that:

• demonstrates a systematic approach to highways maintenance which

takes a long-term view of treatments

• applies lifecycle planning and costing in the consideration and

determination of the most appropriate maintenance treatments over the

life of highway assets; this is to inform the optimal treatment at each

stage of the asset’s life.

• considers customer expectations and defined levels of service - as

outlined in the Highways Maintenance Manual and aligned, as far as

reasonable practicable, to the national code of practice.

• optimises and prioritises works based on assessed needs derived from

the defined levels of service

8.15 All of the above, when implemented in a formalised framework approach,

enables better decision making which takes account of the relationship between

cost and performance.

8.16 The Highways Maintenance Manual (HMM) sets out how Cornwall Council

manages and risk assesses the maintenance of its highways to fulfil its

statutory obligations and deliver a safe, serviceable and resilient highway

network. Taken as a whole the HMM sets out how the Council complies with the

objectives and recommendations set out in national guidance documents and

in particular the UK Roads Liaison Group Code of Practice “Well Managed

Highway Infrastructure” published in October 2016. The manual is regularly

review to ensure ongoing best practice is reflected.

8.17 The Local Transport Plan includes details and plans for the authority’s

transportation and infrastructure assets.

Other

8.18 Local Authorities have a statutory duty to ensure a sufficient supply of primary

and secondary school places, including suitable provision for vulnerable

children and those with additional needs. The Pupil Place Planning Strategy sets

out the how the Council aims to deliver the required provision and forms the

basis for the development and implementation of the Schools Capital

Programme.

8.19 Vehicle, Plant and Equipment replacement policies and asset registers are

maintained and managed by Cornwall Fire & Rescue Service. The Council’s

Information Technology assets and their development are managed within the

Council’s IT Service.

9. Risk Management

9.1 A key investment principle is that all investment risks should be understood

with appropriate strategies to manage those risks. Major capital projects and

programmes require careful management to mitigate the potential risks whichInformation Classification: PUBLIC

can arise. The effective monitoring, management and mitigation of these risks

is a key part of managing the capital programme.

9.2 In managing the overall programme of investments there are inherent risks

associated such as change in interest rates, credit risk of third party

contributors, global economy (e.g pandemics). Accordingly, the Council will

ensure that robust due diligence procedures cover capital investment decisions

and where possible contingency plans will be identified and enacted when

necessary.

9.3 No project should be approved where the level of risk is determined to be

unacceptable to the Council.

10. Knowledge and Skills

10.1 The capital strategy has been developed by Officers of the Council, who have

relevant knowledge and technical skills. In addition, external advice and

management is employed by the Council procuring and appointing suitably

qualified advisors and consultants to support the development, operation and

design of the programmes and project.

10.2 Appropriate training is provided to all individuals with investment

responsibilities. This includes all those making investment decisions such as

officers of portfolio boards as well as members with scrutiny and governance

responsibilities. Training is either provided as part of the meeting or by

separate ad hoc arrangement.

10.3 The Council’s property portfolio is managed by its Property Services Team. The

team has extensive knowledge of the Cornwall property market and experience

in dealing with a mix of property types and professional works (including

professional services, landlord and tenant, statutory valuations, acquisitions

and disposals, commercial and residential property management).

10.4 The Council’s asset valuation for the financial statements are assessed on an

agreed five year programme covering the whole property portfolio. The Council

also has internal building surveying resource to advice on construction, repair

and maintenance, and statutory compliance across its property portfolio.Information Classification: PUBLIC

Appendix 1: Capital Programme (by Portfolio Board)

Existing programme

Summary of existing Capital Programme

2025/26

2021/22 2022/23 2023/24 2024/25 Total

& Beyond

(£m) (£m) (£m) (£m) (£m)

(£m)

Existing programme

A secure home for all 159.734 170.645 201.106 100.013 77.666 709.163

A decent income for all 23.858 16.930 8.852 6.903 9.167 65.710

A great environment for all 91.546 162.099 89.862 63.668 20.124 427.299

A thriving, sustainable Cornwall 275.138 349.674 299.820 170.584 106.957 1,202.172

A brilliant place to be a child and grow up 25.973 42.769 15.736 10.119 - 94.597

Empowering and enterprising Council 7.277 13.161 12.784 10.460 10.099 53.782

Vibrant, safe, supportive communities 4.135 9.819 11.749 5.024 7.010 37.737

Total existing programme 312.523 415.423 340.089 196.187 124.065 1,388.288

Existing programme - Funding

Revenue 5.686 5.055 4.647 4.732 5.740 25.860

Prudential Borrowing 167.543 210.436 202.934 116.555 83.251 780.718

Capital Receipts 11.359 17.884 11.895 2.595 6.687 50.420

Specific Reserves 34.563 47.483 29.098 19.630 19.854 150.628

Grants & Contributions 93.372 134.565 91.515 52.675 8.534 380.662

Total existing programme 312.523 415.423 340.089 196.187 124.065 1,388.288Information Classification: PUBLIC

Appendix 2: Capital Financing

1.1 The level and availability of capital funding determines the size of the overall

capital programme. There are largely two main funding streams, external

(including grants & contributions) and direct funding from the Council. The

Council seeks to utilise a wide range of funding to support its capital

programme, maximising external funding opportunities and limiting internal

resources in the most efficient way to deliver its priorities.

1.2 The current capital programme is funded as shown below:

Types of Funding:

Internal / Type of Funding Detail

External

Internal Prudential Local Authorities are permitted to undertake

Borrowing borrowing to finance capital expenditure. In

planning for long term capital investment, it is

essential the long term revenue financing cost

is affordable. There are close links between the

Capital Strategy and Treasury Management

Strategy and Local Authorities must manage

their debt responsibly with decisions made in

consideration of prudent treasury management

practice, as outlined in the Council’s Annual

Treasury Management Strategy.Information Classification: PUBLIC

This type of borrowing has revenue implications

in the form of financing costs:

• interest payable to external lenders;

• minimum revenue provision (MRP), and

amount set aside for repayment of the

principal debt. (Note: the charge in the

first year will consist of interest only and

will be based on the amount borrowed

for a full year. However, there will be no

principle (MRP) element payable in the

first year and this will commence in the

year following completion.)

The Council has set capital indicators for

borrowing. Over the medium term the costs of

borrowing and minimum revenue provision

(MRP) must not exceed 11.0% of the net

revenue budget and borrowing must not

exceed 2.6 times the annual net revenue

budget.

Capital Receipts The sale of capital assets generates a capital

receipt. These receipts are ring-fenced, by

statute, and can only be used to fund capital

expenditure. Receipts under £10,000 are de

minimis and classed as revenue. All capital

receipts are pooled, allocation and use is

determined as part of the overall capital

programme requires.

However, there are the following exceptions:

• Cornwall Council Farms Estate; 40% of

any receipt is retain for maintenance and

improvement of the Farms Estate.

• Housing; in accordance with legislation

HRA derived proceeds are ring-fenced

for reinvestment in housing projects.

• Cornwall Land Initiative; receipts will be

reinvested / recycled for further

advancement of this scheme.

• Revolving Loan Initiatives.

• Langarth Garden Village; any receipt

from sale of assets associated with the

Langarth scheme will be reinvested /

recycled to fund further investment to

ensure delivery of the master plan.

• Where the sale of an asset has been

specifically approved by Cabinet to be

ring-fenced to fund further development

of that site or associate project.

• Where the sale of an asset leads to the

requirement to repay capital grant, then

the first call on the capital receipt will be

for this purpose.

• Where otherwise explicitly approved by

Cabinet.Information Classification: PUBLIC

Revenue The Council can use revenue resources to fund

capital projects on a direct basis. However,

given the pressures on the revenue budget it is

unlikely that the Council will choose to

undertake this method of funding if other

sources are available.

Reserves The Council will regularly review its reserves to

identify resource that can be used to deliver

Council priorities including, if appropriate,

funding of capital investment. (The Place based

and Capital Financing Reserve are the Council’s

main reserves set aside for financing future

capital investment.)

Leasing Services may enter into finance leasing

agreements to fund capital expenditure.

However, a full options appraisal and

comparison of other funding sources must be

made and the Council’s Section 151 Officer

must be certain that leasing provides the best

value for money method of funding the

scheme. Finance leasing agreements are

included within the overall borrowing levels

when considering prudence and affordability

and calculating the capital indicators.

External Grants Grant funding is one of the largest sources of

financing the capital programme. This could be

from central government departments (such as

Department for Transport and Department for

Education) or other organisations such as

Environment Agency (EA), Homes England

(HE), Heritage Lottery Fund (HLF).

These will be applied to specific projects /

programmes in accordance with their grant

conditions.

S.106 / Significant developments across the County are

Community often liable for contributions. They are provided

Infrastructure by developers towards provision of public

Levy (strategic infrastructure required as a result of the

element) development.

These will be applied to suitable and relevant

expenditure according to

Private Sector / Any other contribution from an external

Other External organisation (e.g. Town or Parish Councils),

Contribution often contribution to a jointly beneficial

scheme.

2. Optimising Council Resources

2.1 Whilst prudential borrowing is the main source of internal Council capital

resource, it is not the only source. Direct revenue funding, reserves and capitalInformation Classification: PUBLIC

receipts can all be used to fund capital expenditure. However, whilst revenue

and reserves can be used, it is not recommended to use these sources

particularly when there is insufficient budget available to fund the Council’s

ongoing revenue budget.

2.2 The Council can borrow to fund capital investment, but unlike central

government cannot borrow to fund day to day revenue expenditure, therefore

whilst there is a shortfall in revenue funding it is not strategically good practise

to use revenue for something the Council can borrow for.

2.3 Capital expenditure will be funded from capital resources when prioritising

funding and not use revenue linked resources until all available capital

resources have been utilised.

3. Minimum Revenue Provision (MRP)

3.1 The minimum revenue position (MRP) is the amount set aside for the

repayment of debt as a result of borrowing made to finance capital

expenditure. The Council sets its MRP Policy annually as part of the Treasury

Management Strategy. MRP charges reflect the economic benefit the Council

gets from using the asset to deliver services over its useful life. This ensures

the Council Tax payers are being charged each year in line with the asset

usage and prevents future Council Tax payers being burdened with ‘debt’ and

the costs of that debt, relating to assets that are no longer in use.

3.2 As a guide, borrowing incurs a revenue cost burden of approximately 4.1% of

the loan each year i.e. for every £1 million of borrowing, this will incur

revenue costs of approximately £41,000 per annum. This is calculated as

follows:

3.3 Exact costs will depend upon the asset life associated with the particular

capital investment and available interest rates. These are in addition to any

ingoing maintenance and running costs associated with the investment.Information Classification: PUBLIC

3.4 Local authorities must manage their debt responsibly and decisions about

borrowing are made in consideration of prudent treasury management

practice, as detailed in the Council’s Annual Treasury Management Strategy.

4. Flexible use of Capital Receipts

4.1 In February 2021 final settlement it was confirmed that the flexible use of

capital receipts was extended for a further 3 years. The details and impact

are still being assessed by government and guidance is yet to be issued.

4.2 There are no current plans for the Council to use capital receipts under the

flexibility directive. Following guidance from government the Council will

assess the need for use of capital receipts and incorporate into an updated

Capital Strategy during the financial year.Information Classification: PUBLIC

Appendix 3: Capital Expenditure

1.1 Capital expenditure is the acquisition, creation or enhancement of fixed assets

with a long-term value to the Council or on those assets of its partners.

1.2 If expenditure falls outside of this definition, it will be charged to the revenue

account during the year that the expenditure is incurred; this is the default

position. It is therefore crucial that expenditure meets the definition above

before being included in the capital programme to avoid unexpected revenue

charges within the year. Definition of capital expenditure is provided below,

relating to some of the more complicated capital rules.

Allowable Capital Expenditure

Item of Capital or Detail

expenditure Revenue

Feasibility Revenue, but Until a specific solution has been decided

studies could be capital if upon, costs cannot be directly attributable

conditions met to bringing an asset into working condition.

This includes costs incurred whilst

deliberating on an issues, scoping potential

solutions, choosing between solutions and

assessing whether resources will be

available to finance a project. However,

feasibility studies can be capitalised if they

occur after a decision has been made to go

ahead with a capital project (i.e. if they are

directly attributable in bringing an asset

into use, or enhance the value) as long as

they have been included in the approve

project costs.

Demolition of an Revenue, but Demolition would usually be an act of

existing building could be capital if destruction that would be charged to

conditions met revenue; However, if the costs incurred are

necessary in preparing a site for a new

scheme, it can be argued that they are an

integral part of the new project.

Cost of buying Revenue Does not enhance the asset or extend the

out sitting asset life.

tenants of

existing building

Initial delivery Capital As long as directly required to deliver the

and handling asset or bring an asset into use.

costs

Costs of renting Revenue Considered to be a cost of delivering the

alternative regular Service, does not directly deliver

accommodation the asset.

for staff during

building works

Site security Revenue Does not enhance the asset or extend the

during asset life.

constructionInformation Classification: PUBLIC

Installation and Capital As long as required to deliver the asset or

assembly costs bring an asset into use.

Testing whether Capital As long as required to deliver the asset or

the asset is bring an asset into use.

functioning

properly

Rectification of Capital As long as required to deliver the asset or

design fault bring an asset into use.

Liquidated Revenue Does not enhance the asset, relates to a

damages breach of contract.

Furniture and Capital (subject Subject to de-minimis expenditure level.

fittings to de-minimis

level)

Training and Revenue These are revenue as it is training to use

familiarisation of the asset, not costs incurred with getting

staff the asset into a usable state.

NB: Cloud based systems are not capital as

we do not own the asset but purchase a

licence to use it.

Professional fees Capital As long as required to directly deliver the

asset or bring an asset into use.

Borrowing costs Revenue There is currently no provision for

borrowing costs to be eligible for

capitalisation within the Council.

Internal staff Revenue, but Usually these are revenue, but if costs

costs could be capital if /time can be identified that have directly

conditions met contributed to the delivery and getting the

asset into working condition and are

dedicated to that asset then this could be

capitalised, subject to agreement and

funding. General overhead and

apportionment of managerial costs are not

capital.

1.3 Contributions and grants to external organisations / individuals (i.e. not on

the Council’s own assets) can be capital expenditure as long as the ultimate

use of the funds meets the Council’s definition of capital above.You can also read