ASX CEO Connect March 2018 - Chris Jewell - CHIEF FINANCIAL OFFICER

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ASX CEO Connect March 2018 Chris Jewell – CHIEF FINANCIAL OFFICER GENESIS ENERGY LIMITED

About New Zealand

— good growth in a stable regulatory environment

Source: Economy Rankings 2017 (The World Bank), The Heritage Foundation 2017, Forbes Lists 2016, Legatum Prosperity Index

2016, Energy Architecture Performance Index 2017 (World Economic Forum)

NOV17 INVESTOR ROADSHOW 2

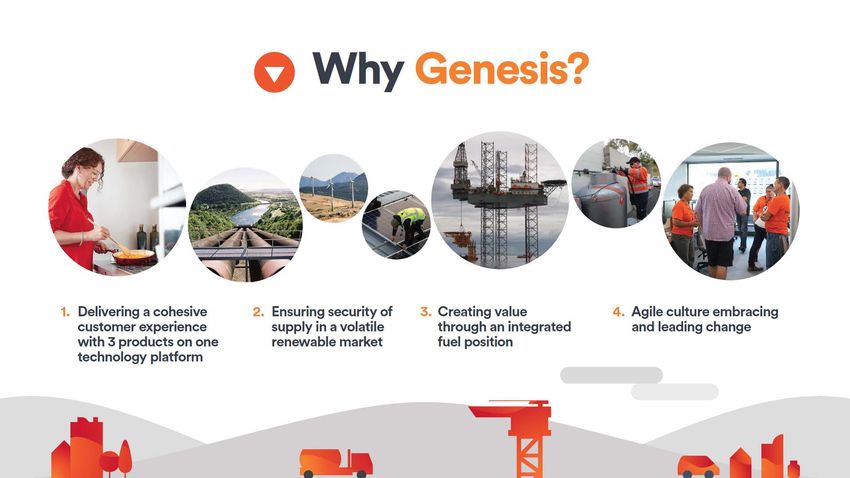

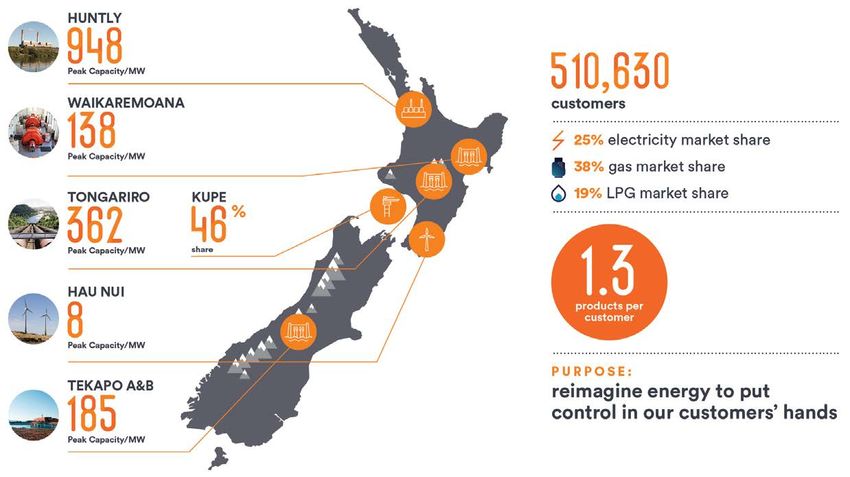

About Genesis Energy

— only integrated energy management company in New

Zealand

KEY INFORMATION

,

Revenue: NZ$2.0 billion

EBITDAF Guidance (FY18): NZ$350-360

million

Dividend Yield: 6.7%

Share Price: NZ$2.40

Market Capitalisation: NZ$2.4 billion

Average Daily Turnover: 750,000 shares

Credit Rating: BBB+ (Standard & Poors)

Genesis Energy is a large, fully integrated

energy management company. It is New

Zealand’s largest energy retailer, generates

electricity from a diverse portfolio of thermal

and renewable assets located throughout the

country, and has an interest in the Kupe oil

and gas field offshore of Taranaki.

NOV17 INVESTOR ROADSHOW 3

Market fundamentals outlook

— continue to be supportive

• Electricity demand growth of 1% in 2017 with EV penetration accelerating

Customer • Total NZ gas demand down due to industrial however retail growth continues with

connections up over 15,500 in past five years

• LPG demand growth remains strong, with 6% growth in market over last 12 months

• Forward electricity prices more reflective of tightening supply/demand dynamics.

Wholesale Year 2 price is up $4MWh (5%) on prior comparable period

• Tiwai Point Aluminum Smelter economics stable with a more positive outlook

• Forward carbon prices up to $24 per tonne in 2020

• Brent crude up 20% in 2017 with consensus outlook for 2018 in the range of US$59 to

Kupe $62/bbl

• LPG supply/demand balance tightening with a possible move to net import early 2020’s

HY18 RESULT PRESENTATION 4

Strategy

Company

Financial Investor

Company strategy

— five key strategic initiatives underpin our transformation

REIMAGINING ENERGY

to put control in our customers’ hands

Optimise Innovate Invest

To improve short term return For medium term growth For long-term value creation

Core

Strategic

Deliver operational Increase value Targeted growth in

Initiatives Grow LPG Build energy

excellence and share of residential business category

value optimisation category category services

Insights and Analysis

Foundation investments in technology & digital

Enabling

Embed data-driven decisions

Initiatives

Ways of working

NOV17 INVESTOR ROADSHOW 6

Company strategy: Recent strategy

highlights

— transformation journey underway Launched NZ’s first real

world research and

Reset development energy

Strategy and vision community

Acquired additional

15% of Kupe for $168

million

Acquired retail LPG

distribution business

of Nova Energy for

Delivered $200m $200m $192 million

EBITDAF H1 FY18

- Up 28% Supported NZ Launched loyalty

security of supply program with

during two dry >120,000 customers

periods linked

NOV17 INVESTOR ROADSHOW 7

Company strategy: Innovating to

lead

— working with customers collaboratively to build our energy management

capabilities

Energy Innovation

Management

R&D

Local Energy Energy

Project Management

My New

Technologies

Account

Technology

“Making Energy management real for our “Partnering with customers to test and develop

customers by initiating trials for our new the latest energy innovations and deliver

services which include energy forecasting products and services that give them control

which went live this month.” about their energy use.”

NOV17 INVESTOR ROADSHOW 8

Financial strategy: FY21 target

— target to deliver $400 - $430 million by FY21

$15m -$20m

$12m -$17m

$13m -$17m

$6m -$10m $2m -$3m

$5m -$8m $400m -

$9m -$14m

$5m -$8m $430m

$385m -

$410m

$333m

FY17 EBITDAFOperational Residential Business Grow LPG Energy services Kupe Core growth 4 Original Nova Energy Revised FY21

excellence value sharecategory growth category FY21 EBITDAF retail LPG EBITDAF

3

target business target

NOTES

1. Several initiatives are interdependent. As an example, energy services capability will contribute towards residential value share

2. All ranges are net of operational investment required to achieve target outcomes

3. Represents acquired EBITDAF in the acquisition of the Nova Energy retail LPG business not in original FY21 target. $4-6 million of synergies from the acquisition will be

reflected in the “grow LPG category”

4. Core growth represents partial benefit from the rolling off of the take or pay gas contracts and natural growth in wholesale prices over time

NOV17 INVESTOR ROADSHOW 9

Investor Strategy

— continued growth in dividends with a 8.6% gross yield1 and outperformance of TSR relative to peers

• FY17 16.6c of dividends declared up 1.2% representing a cash yield of 6.7%. Dividend policy to grow in

real terms over time with 3.8% growth delivered in past three years against inflation of 2.5%

• TSR target of top quartile, translating to ~14%, with a focus on dividend yield plus growth

• TSR has exceeded market by 7.2% and peer index by 4.1% in past 12 months

DIVIDEND & PAYOUT HISTORY 2017 TOTAL SHAREHOLDER RETURN

200 100%

Total Dividends Paid ($millions)

80% 81% 81% 84% 2017 closing share price: $2.52

73% 29.2%

80%

% of Free Cash Flow

150 25.1%

22.0%

60%

100

160 164 166 40%

130

50 114

20%

0 0%

FY2013 FY2014 FY2015 FY2016 FY2017

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Total dividends paid Total Dividend Paid as % of FCF

Genesis Peer Index NZX50

1. Gross yield based on closing share price as at 29 December 2017.

HY18 RESULT PRESENTATION 10Financial Performance

Financial overview

— a diverse portfolio delivering consistent earnings over

time

• HY18 EBITDAF $200 million, up 28%, FY18 guidance of $350 - $360 million

• NPAT down 24% to $28 million, due to fair value movements, underlying earnings up 14% to $43

million

• Operating cash flow up 57% to $199 million, and free cash flow up 37% to $129 million

EBITDAF EBITDAF BY SEGMENT

$ MILLIONS $ MILLIONS

400 400 55

350 350 50

94 80 84

300 300 107 45

172 159 40

250 177 250

157 35

200 200 194 176 56

201 30

150 169

150

25

100 106

173 176 200 100 20

151 156

50 50 87 103 110 15

83 58

0 0 10

FY14 FY15 FY16 FY17 HY18 FY14 FY15 FY16 FY17 HY18

Customer Generation & Wholesale Kupe Corporate

NOV17 INVESTOR ROADSHOW 12Capital structure overview

— long tenure debt in place at lower cost, with BBB+ rating from S&P, DRP in

place

• Average cost of debt 5.8%, down 20 basis points

Key Debt Metrics 31 Dec

• Average tenure 11 years, up 3.1 years 2017

• S&P reaffirmed BBB+ rating post acquisitions in January 2018 Total Debt $ 1,229.1

Cash and Cash Equivalents $ 40.6

with Net Debt/EBITDAF expected to return to upper end of target

Headline Net Debt $ 1,188.5

range by end of FY18

USPP FX and FV Adjustments $ 25.2

• Dividend reinvestment plan announced at HY18, 2.5% discount Adjusted Net Debt1 $ 1,163.3

Headline Gearing 39.1%

GENESIS ENERGY DEBT PROFILE

Adjusted Gearing 38.6%

$m

$300 Net Debt/EBITDAF2 3.0x

$250 Interest Cover 6.9x

$200

1. Net debt has been adjusted for foreign currency translation and fair value

$150 movements related to USD denominated borrowings which have been fully

hedged with cross currency swaps

$100 2. EBITDAF is based on the midpoint of the guidance range provided for FY18

$50

$0

FY FY FY FY FY FY FY FY FY FY FY FY

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2042 2047

Retailable Bonds Wholesale Domestic

Drawn Bank Undrawn Bank

Capital Bonds USPP

NOV17 INVESTOR ROADSHOW 13Summary

15

FY17 15

15Genesis Energy

— our mission is to reimagine energy, to put control in our

customers’ hands

• Company strategy

• Deliver operational excellence and value optimization

• Increase value share of residential category

• Grow business 2 business & LPG categories

• Build energy services

• Financial strategy

• Deliver EBITDAF of $400 - $430 million by FY21

• Investor strategy

• Deliver yield plus growth, target top quartile TSR (~14%)

NOV17 INVESTOR ROADSHOW 16You can also read