26-28 HAMMERSMITH GROVE - HOTEL NEEDS ASSESSMENT DECEMBER 2020 - Planning Alerts | UK

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

26-28 HAMMERSMITH GROVE HOTEL NEEDS ASSESSMENT DECEMBER 2020

MARK STANTON BRITEL FUND TRUSTEES LIMITED 150 CHEAPSIDE, LONDON, EC2V 6ET Dear Mark In accordance with your instructions, and our proposal dated 22nd October 2020, we are pleased to present our report assessing the market and financial opportunity for the proposed Apart-Hotel at 26-28 Hammersmith Grove, W6 7HA. We have carried out desk-based research to assess the subject site’s suitability for apart-hotel use, and its accessibility and location in relation to potential demand generators, both corporate and leisure. In addition, we have conducted research into the potential future hotel supply threat in the local market of relevance as well as into local hotel market performance utilising STR market performance data. Based on this research we have provided our comments and recommendations on the identified development opportunity as well as our projections of estimated room occupancy and average room rate for the first three years of operation. We have welcomed the opportunity of preparing this report on your behalf and would be pleased to discuss it with you if so required, or to answer any queries which may arise. Yours Sincerely, AUREL BARKOWSKI JOE STATHER Associate Director Associate Director London, UK London, UK Aurel.Barkowski@cbrehotels.com Joe.Stather@cbrehotels.com

DISCLAIMER This report (the “Report”) has been prepared by CBRE Hotels Ltd (“CBRE”) exclusively for Britel Fund Trustees Limited (the “Client”) in accordance with the terms of engagement entered into between CBRE and the client dated 22/10/2020 (“the Instruction”). The Report is confidential to the Client and the Client may not disclose the Report unless expressly permitted to do so under the Instruction. If you are not the Client, then you are viewing this Report on a non-reliance basis and for informational purposes only. You may not rely on the Report for any purpose whatsoever and CBRE shall not be liable for any loss or damage you may suffer (whether direct, indirect or consequential) as a result of unauthorised use of or reliance on this Report. CBRE gives no undertaking to provide any additional information or correct any inaccuracies in the Report. Nothing in the Report is, or should be relied on as, a promise or representation as to the future. The Report may include certain statements, estimates and projections, which may or may not prove to be correct. No undertakings, representations or warranties are made by CBRE as to the accuracy of such statements, estimates or projections. None of the information in this Report constitutes advice as to the merits of entering into any form of transaction. Novel Coronavirus (COVID-19) The outbreak of the Novel Coronavirus (COVID-19), declared by the World Health Organisation as a “Global Pandemic” on the 11th March 2020, has impacted many aspects of daily life and the global economy – with the hotel markets experiencing significantly lower, or no, levels of trading activity. As at December 2020 there is a shortage of market evidence for comparison purposes, with hotel revenue streams and operational costs being impacted by many different factors, due to COVID-19. However, we have utilised data as at 31 December 2019 – where enough relevant benchmark data and other supporting research is available on which to formulate our initial projections of future cash-flow – which we have then adjusted appropriately, as set out within this report, to take into account the effects of COVID-19. Our projection of future cash flow is therefore reported as being subject to ‘material uncertainty’ as set out in VPS 3 and VPGA 10 of the RICS Valuation – Global Standards. Consequently, less certainty – and a higher degree of caution – should be attached to our projections than would normally be the case. For the avoidance of doubt, the inclusion of the ‘material uncertainty’ declaration above does not mean that the cash-flow cannot be relied upon. Rather, the declaration has been included to ensure transparency of the fact that – in the current extraordinary circumstances – less certainty can be attached to the cashflow than would otherwise be the case. The material uncertainty clause is to serve as a precaution and does not invalidate the cash-flow. Given the unknown future impact that COVID-19 might have on the real estate market and hotel operations, with many business practices and behaviours needing to change either temporarily or permanently, we recommend that you keep the market and financial feasibility and resulting cash flow projections contained within this report under frequent review.

CONTENTS 01 EXECUTIVE SUMMARY 05 02 PROPOSED SCHEME 10 03 MARKET TRENDS 13 04 HOTEL MARKET 26 05 PROJECTIONS 39 06 APPENDICES 43

EXECUTIVE SUMMARY 01

EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES EXECUTIVE SUMMARY 01

In our view, there is a strong market opportunity to develop a 85-bedroom Apart-Hotel at 26-28 Hammersmith Grove. This is supported by the performance of local hotels in

Hammersmith, which operated close to 85.0% occupancy in 2019, indicating a supply constrained market. Should demand levels return to pre-pandemic levels, which is widely

expected to be the case, there will be a need for additional quality guest accommodation in Hammersmith to capture historically unsatisfied demand as well as to support and

complement future development projects, and private sector investment, in the local area. The following three slides summarise the market factors on which we have based our

assessment of the development opportunity.

▪ The subject site benefits from a central location within Hammersmith, a key employment and

Location, Infrastructure, Demand Generators commercial district of London.

▪ Hammersmith acts a the Western gateway to Central London with strong communication

links by road and public transportation. This includes direct access to the A4, which links

Heathrow Airport to Central London and four London Underground lines.

▪ The local area is an established commercial district, proving particularly popular with media

and business services firms. Blue-chip companies of national and international significance

such as Disney, BBC, L'Oréal, Philip Morris and Novartis, represent strong corporate demand

providers within the local hotel market.

▪ The local area around the site has established itself as a vibrant area and entertainment hub

with notable demand drivers including the Westfield Shopping Centre, the Lyric Theatre and

the Hammersmith Apollo area. The pedestrianised riverside, within a short-walking distance

from the subject site, is also popular with tourists.

▪ With numerous public transport stations in close proximity, the subject site is also well

connected to Central London’s main shopping districts and major tourist attractions such as

the Natural History Museum and the Royal Albert Hall.

▪ Whilst the local economy is anticipated to rebound strongly in 2021 and to recover to 2019

levels by 2022 (according to latest projections from Oxford Economics), the tourism sector is

Market Recovery forecast to only fully recover by 2024. This is in part due to the reliance of London, as a

major gateway city, on international demand, which will likely face a more protracted

recovery.

▪ However, in line with industry experts such as Tourism Economics and STR Global, we do

expect the tourism sector in London to recover from the current crisis and to have a strong

come back once travel restrictions are lifted and a cure for the virus becomes widely

available. This can be supported by the resilience and endurance of the tourism sector

through previous demand shocks such as the global financial crisis as well as several terrorist

attacks. A recovery in tourism demand will in part be driven by a number of megatrends,

including Globalisation and the increased facilitation of cross-boarder travel, which are

discussed in further detail in this report.

▪ The shortfalls in international accommodation demand are expected to be partially

substituted by domestic demand over the short-to-medium term and to be complemented by

short-haul travel from continental Europe. As a result, the latest Tourism Economics forecast

estimates overall accommodation demand for London to fully recover to pre-pandemic levels

by 2024. The recent news regarding a vaccine gives us greater confidence in this forecast,

which predicts a material bounce back in demand from H2 2021.

CBRE | HAMMERSMITH GROVE 6

EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES EXECUTIVE SUMMARY 01

▪ The local hotel market (1-mile radius from subject site) is presently dominated by 4-star

Hotel Supply & Pipeline hotels, accounting for 54.0% of the total bedroom supply.

▪ The serviced-apartment sector is represented by nine properties, which are generally small in

size with an average bedroom count of 27 units, and account for 12.5% of the total bedroom

supply in the local market.*

▪ Whilst the current serviced apartment provision is small in size relative to other hotel

categories, the presence of well-known apartment operators demonstrates that there are

good levels of long-stay demand in the market.

▪ Confirmed future supply additions in a 1-mile radius of the subject site are limited to one

serviced apartment development with 74 bedrooms. Based on the significant demand levels

in the local market, we would expect this property to be absorbed with minimal impact into

the market place.

▪ Over the past six years, the local hotel market consistently operated well above 80.0%

occupancy. This was achieved despite strong supply additions in Hammersmith and the wider

London area, providing evidence that new hotel openings were effectively absorbed into the

market place. In fact, occupancy reached 84.7% in 2019, which was above the wider

London market (+1.4 ppt) and indicates constrained supply during peak demand periods.

Requirement for Serviced Accommodation Based on 2019 data, peak demand periods include Tuesday to Wednesday nights as well as

Saturdays, throughout the year. During these time periods occupancy reached close to

90.0%, indicating that a significant number of room nights were displaced to neighbouring

boroughs or other parts of London and demand for the local hotel market was unsatisfied.

▪ Ongoing and planned development projects in the wider local area will further increase

serviced accommodation needs in the local area over the mid- to long-term. This presents an

opportunity for the proposed development to support and complement new development

projects and existing office occupiers by providing quality serviced accommodation.

▪ Key projects include the continued expansion of the Imperial College, White City Campus,

the provision of additional office space (e.g. White City Gateway) as well as the

redevelopment of Olympia London into a world-leading cultural and entertainment hub.

*This excludes the Residence Inn London Kensington with 319 bedrooms, 1.5 miles from the

subject site.

CBRE | HAMMERSMITH GROVE 7

EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES EXECUTIVE SUMMARY 01

▪ We consider there to be a strong opportunity for the development of a 85-bedroom Apart-Hotel

as proposed by Britel Fund Trustees Limited. The proposed location of the development, as well

as strong appeal of Hammersmith as a place to live and work, combined with the ongoing

gentrification of the wider local area, should enable the proposed development to successfully

compete within the local hotel market and attain a strong market position.

▪ The proposed type of development should complement and enhance the currently short-stay

focused hotel market by providing high-quality apart-hotel accommodation that will cater to both

leisure and corporate travellers. The accommodation offer is envisaged to include spacious, self

Proposed Development contained rooms, equipped with additional cooking, eating and living spaces.

▪ Going forward, we expect travellers to express some apprehension about staying in transient

accommodation and potentially coming into contact with others, at least in the short-to-medium

term. This is likely to benefit the performance of serviced apartments over traditional hotels, as

evidenced by year-to-date trading statistics of the London serviced apartment sector as presented

in this report.

▪ We also note that the proposed Apart-Hotel is aligned with the 2016 London Plan (Policy 4.5)

and the Intend to Publish London Plan 2019 (Policy E10), which account for the importance of

London’s visitor economy. They highlight a requirement for boroughs to stimulate growth, taking

account of the importance of business and leisure visitors, and to support an increase in the range

and improvement in the quality of guest accommodation.

The images below provide examples of serviced apartment operators in the local hotel market.

Lamington Apartments Hammersmith Residence Inn by Marriott London Kensington

CBRE | HAMMERSMITH GROVE 8

PROPOSED SCHEME 02

EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES PROPOSED SCHEME 02

PROPOSED SCHEME

SITE ANALYSIS

CBRE ANALYSIS

▪ The subject site is centrally located within Hammersmith, in West London and on the

north bank of the River Thames. Hammersmith serves as the main gateway into

Central London from the west and is a key employment and commercial district.

▪ The site is positioned between Hammersmith Grove to the West and the London

Underground railway tracks to the East, approximately 0.2 miles north-west of

Hammersmith town centre.

▪ Hammersmith is a major transport hub benefiting from an excellent link to the road

Proposed network. It is located at the junction of the A4 and several local feeder roads. The A4

Development Area runs directly through Hammersmith and provides direct access to Central London

Boundary and the M4 motorway, which links to Heathrow Airport. In addition, Hammersmith is

served by two Underground stations with four tube lines and a bus terminal,

providing fast and frequent public transportation links to both Central London and

Heathrow Airport.

▪ As a key office location, the local area is particularly popular with media and

business services firms, including notable occupiers such as BBC, ITV and Walt

Disney.

Kensington (Olympia)

Shepherds Bush Rd

Strong corporate demand Western Gateway into Central

drivers within the local area, London with strong

SUBJECT SITE Hammersmith Rd

including numerous blue-chip accessibility by road and train.

occupiers.

Hammersmith

King St.

Hammersmith

West Kensington Ongoing expansion of Imperial College London, White

A4

A4

City Campus should further strengthen the local area’s

Barons Court reputation as a destination for research and innovation and

Hammersmith Bridge attract companies and institutions of national and international

significance.

Source: Google Maps, Britel Fund Trustees Limited, 2020

CBRE | HAMMERSMITH GROVE 10EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES PROPOSED SCHEME 02

PROPOSED SCHEME

OVERVIEW SCHEME

COMPONENT CHARACTERISTICS ▪ The proposed development is envisaged to be a quality mid-scale Apart-Hotel, providing the

Mid-scale standards, security & service of a hotel but with the added comfort of larger bedrooms,

Market Positioning

including more generous living areas and self-catering facilities within each unit.

Service Offer Apart-Hotel

▪ In line with the typical target market of serviced apartments, the proposed development will

61 Studio Rooms

likely cater for corporate and leisure travellers requiring accommodation for medium to long-

15 One-Bedrooms

Bedrooms term assignments, in addition to those relocating and requiring interim accommodation.

9 Wheelchair Accessible Rooms

▪ Based on the envisaged target market and accommodation offer, we would expect a lower

85 Rooms in Total guest turnover for the proposed Apart-Hotel than a typical hotel, driven by a longer average

Food & Beverage Café on ground floor length of stay. This should reduce the overall customer traffic in and around the subject site

Other Facilities Exercise Room (26m²) compared to a traditional hotel, which would typically cater to a more transient customer base.

FACILITY MIX

▪ Based on the latest plans, the proposed Apart-Hotel will be developed over ground floor and

five upper floors and comprise a mix of studios and one bed rooms. In total there are plans for

85 rooms of which nine rooms will be wheelchair accessible.

▪ All rooms will feature ensuite bathrooms, a fitted kitchen and a lounge/dining area. Within the

larger one bed rooms, the lounge/dining area is physically separated from the bedroom. Room

sizes range from approximately 20 square metres for a studio room up to 37 square metres for

a one-bedroom apartment. Accessible rooms are larger and up to 44 square metres.

▪ In line with the typically limited ancillary facilities of apart-hotels, the proposed development will

feature a café/ breakfast area on the ground floor as well as a small exercise room on the same

level. As such, we expect local restaurants, cafes and bars to benefit from an increase in

demand.

OPERATOR

▪ We understand that Britel Fund Trustees Limited are currently in discussions with an established

Source: Britel Fund Trustees Limited, 2020 serviced apartment brand to operate the proposed development. This serviced apartment

operator currently manages several existing properties within the wider Hammersmith area and

as such has an excellent understanding of the local market dynamics. The addition of a further

property to its portfolio would deliver significant operational and marketing advantages to the

operator, positively impacting the feasibility and operation of the proposed development.

CBRE | HAMMERSMITH GROVE 11MARKET TRENDS 03

EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

TRAVEL & TOURISM DEMAND

Travel and Tourism Is cyclical and has always bounced back…

The outbreak of COVID-19 has impacted many aspects of daily life and the global economy – with leisure and travel-related sectors amongst the worst hit. To provide further context

to this report and our analysis of the Apart-Hotel development opportunity, we detail on the following slides the historic performance of the travel industry and general outlook,

including impact and anticipated recovery from the pandemic.

Global International Arrivals Global International Tourism Receipts, 2000-2019

1950-2019 2000-2019

2,000 2,000

9/11 and Early

(2009, -9%)

1,500 Early 1990s 2000s recession 1,500

Receipts, $US bn

Early 1980s recession

Arrivals, mn

recession (2001, -2%)

1,000 1,000

Economic

500 500 slowdown

2007-2009

(2015, -5%)

Financial Crisis

0 0

Source: United Nations World Tourism Organisation, 2020 Source: United Nations World Tourism Organisation, 2020

▪ The number of global international arrivals has increased at a compound annual ▪ Over the period 2000-2019, the global value of tourism has grown at a CAGR of

growth rate (CAGR) of 6.1% over the period 1950-2019. 5.9%; exceeding the growth in world GDP of 5.1%. In 2019, total tourism receipts

▪ There was a notable acceleration in the growth rate of international tourism arrivals in reached US$1.48 tn.

the 10-years to 2019. A similar growth trajectory has only been observed during the ▪ The value of tourism (receipts) has been more volatile than the volume of tourism

post-war package holiday boom of the 1960’s and in the period 2003-2007, (arrivals), with higher growth rates observed in an expansionary period and larger

following 9/11 and the early-2000’s recession. declines during a period of contracting demand. These characteristics are not

▪ Growth in the last decade has been supported by a number of megatrends, which we dissimilar from other consumer discretionary sectors.

expect to support the future expansion of the travel and tourism industry. This includes ▪ However, the travel and tourism industry has always recovered relatively quickly from

Globalisation and the increased facilitation of cross-border travel. These trends and market shocks, partly due to the underlying megatrends mentioned opposite, but also

their impact on the travel industry are presented in more detail on the following slide. due to its adaptive capacity – targeting different consumer segments to stimulate a

faster recovery. This can be underpinned by recent research, which points towards the

continued strong desire of people to travel. Based on a survey from the World Travel

& Tourism Council in October 2020, 99.0% of the respondents indicated a continued

strong motivation to travel and 70.0% planning to take a holiday in 2021 (WTTC,

2020). This suggests that as concerns about COVID-19 are addressed, travel activity

is likely to rebound strongly.

CBRE | HAMMERSMITH GROVE 13EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

TRAVEL & TOURISM DEMAND

There are multiple structural drivers which will support long-term growth

Economic Drivers

▪ Globalisation will continue to result in easier access across borders, which is likely ▪ Generation Y, comprising those born between the early 1980’s and early 2000’s,

to facilitate further growth in the number of international business and leisure is an influential demographic group with high earning potential. The Generation Y

tourists. Whilst we appreciate that there are a number of disruptors, general cohort is the biggest in history by population and is about to move into its prime

factors which will promote economic dynamism and continue to support spending years. The demands of Generation Y for memorable moments and

globalisation include: activities over material goods has elevated the ‘Experience Economy’, and older

generations are also starting to follow the trend. Demand for travel, the ultimate

− Political pressures for higher living standards;

experience, has and will continue to grow as a result. Travel is increasingly seen as

− Deregulation/liberalisation; a status booster and social media is supporting this change. However, it is

− Rising trade and investment; and generally recognised that the travel industry needs to adapt to fully capitalise on

this trend, by focusing on authenticity, local experiences and personalisation.

− Increasingly dynamic private sectors.

Travel Mobility

▪ Rising incomes correlate strongly with tourism flows and the expansion of the

global middle class will play a major role. Emerging economies, pre COVID-19, ▪ Transport is an essential component of the tourism system. Whilst there remains

led the growing demand for international tourism. The European Travel considerable uncertainty surrounding the near-term impact of the COVID-19

Commission, in 2019, predicted that the number of annual visitors to the pandemic on air travel, the International Air Transport Association (IATA), as of

European Union from the Asia-Pacific region would increase from 26m to 34m by May, predict a baseline increase of 48.8% in global air passengers between 2019

2030. and 2039, to 8bn per annum. For shorter-routes, growth in high-speed rail,

Social Trends including established and expanding networks in Europe, will compete with

aviation. Ultimately, the Organisation for Economic Co-operation and

▪ Increasing expectations of people will generate increased demand for Development (OECD) predict that old and new destinations alike will benefit from

discretionary expenditure including travel and tourism. This will be further the upward trend in passenger capacity. Notably 55% of inbound arrivals to the

compounded by urbanisation and rising stress levels leading to growing emphasis EU are by land or water, versus 45% by air (UNTWO, 2016).

on travel as a means to ‘escape’. To improve work-life balance we will also

continue to observe growing demand for ‘bleisure’ travel – extending a business

trip for leisure purposes. As people are increasingly money rich-time poor, they are

more likely to fill their spare time with travel experiences and are willing to pay

more.

CBRE | HAMMERSMITH GROVE 14EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

TRAVEL & TOURISM DEMAND

Europe will remain the most popular region for inbound travel

International Tourist Arrivals by World Region, Travel and Tourism Competitiveness Index

1950-2019 2019

1,600 Cultural Resources and Business Travel

Natural Resources

1,400 Tourist Service Infrastructure

1,200 Ground and Port Infrastructure

Air Transport Infrastructure

1,000

Arrivals, mn

Environmental Sustainability

800 Price Competitiveness Global Average

International Openness

600 Prioritization of Travel and Tourism Europe and Eurasia

400 ICT Readiness

Human Resources and Labour Market

200 Health and Hygeine

0 Safety and Security

Business Environment

0 2 4 6

Africa Americas Asia Pacific Europe Middle East Score (1 = worst, 7 = best)

Source: United Nations World Tourism Organisation, 2020 Source: World Economic Forum, 2019

▪ As of 2019, the European region accounted for over half (51%) of total global ▪ The Travel and Tourism Competitiveness Index, compiled by the World Economic

international arrivals (741bn). Its share has reduced by 7ppts in the last twenty Forum (2019), ranks Europe as the world’s most competitive region for Travel

years due to the rapid development of the Asia-Pacific market, although the share and Tourism. One of the key drivers of Europe’s success as a travel destination is

of arrivals captured by the Americas has declined to a greater extent (-9ppts). its abundant cultural resources. The large number of visitors that these attract are

▪ International arrivals to Europe increased at a CAGR of 7.9% over the period accommodated by the “world’s most robust tourism infrastructure, including

1950-2019 and 4.9% in the last decade. This is relatively strong recent growth world-class transport infrastructure”. Most European economies have strong

considering the maturity of the European region as a travel destination, and enabling environments, particularly relating to business environment. The region

considering volatility and setbacks resulting from various terrorist attacks and the scores strongly in terms of health and hygiene, which are likely to become

UK’s decision to leave the European Union. increasingly important factors in a post-COVID-19 environment, and the region’s

high degree of ICT readiness allows Travel and Tourism businesses and travellers

▪ Tourism generates 10.0% of GDP and represents 9.0% of total employment in the to leverage increased use of online and digital platforms in B2B and B2C industry

Europe. For this reason, we are confident that the industry will continue to be services.

prioritised in terms of public and private investment, including through the current

COVID-19 pandemic and during the recovery phase which will follow. ▪ Notably, cultural resources cannot be easily replicated and infrastructure is costly

and time consuming to develop. This will support Europe’s position as the leading

region for travel and tourism going forward.

CBRE | HAMMERSMITH GROVE 15EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

TRAVEL & TOURISM DEMAND

Europe International Arrivals vs Domestic Arrivals Europe Domestic and International Tourism Spend

% difference from 2019 levels Domestic % Share as Labels, 2019

20% 12% 500

1% 0% 2%

0% 400

-17% -17% -15% 300

-29%

US$, bn

-20% -35% -32% -12%

-41%

-55% -52% 200

-64%

-40% -75% 100 39% 48% 70% 79% 85% 88%

35% 73% 36% 33% 52% 59% 61% 55% 73%

0

-60%

-80%

2020 2021 2022 2023

Long-Haul Mid-Haul Short-Haul Domestic Inbound Domestic

Source: Tourism Economics, October 2020 Source: WTTC

▪ The COVID-19 outbreak has resulted in a sudden and large drop in travel activity ▪ It is widely accepted, that domestic demand (travel within the country of residence) will

with inbound travel to Europe forecast to decline by 61.0% in 2020. Based on the drive the early phase of recovery following COVID-19.

latest available information from Oxford Economics (October 2020), Europe is ▪ The United Kingdom, Germany and Italy traditionally have the highest share of

assumed to see an earlier recovery than other world regions with almost all European domestic tourism spend. Notwithstanding the economic impact of the virus within

countries set to regain 2019 tourism levels by 2024. each country, these nations are well positioned for a more immediate recovery.

▪ In the near term, recent trends are likely to continue with tourist remaining closer to ▪ As social distancing requirements are lifted, we also expect that pent-up demand for

home and to travel either domestically or to short-haul destinations. Therefore, leisure travel, including visiting friends and relatives, will support demand in the short-

domestic travel will be the key demand driver and achieve a quicker rebound, term, as evidenced during the recent summer period. Whereas corporate, group

returning to pre-crisis levels by 2022. International travel will take longer to recover meetings and convention travel is unlikely to restart in earnest until there is a vaccine

due to ongoing travel restrictions in some countries, reduced disposable income as or widely available treatment for COVID-19.

well as associated confidence effects. These are temporary short-to medium term

impacts of COVID-19 and not structural trends. ▪ Several vaccines are currently in final stage of testing with pharmaceutical company

Pfizer/BioNtech and Moderna having recently reported their vaccine to be more than

▪ The comparatively swift recovery of short-haul travel (2023) will benefit Europe and 90% effective in a first analysis. Whilst some pharmaceutical companies hope to get

the UK as a tourism destination as more than half of all visitor arrivals to the region their vaccine approved by the end of 2021, The World Health Organisation does not

are from short-haul feeder markets. expect to see widespread vaccination against COVID-19 until the middle of 2021.

We note that current baseline projections by Tourism Economics presented above and

on the following slide are based on the assumption that a COVID-19 vaccine will be

in circulation from the middle of next year.

CBRE | HAMMERSMITH GROVE 16EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

TRAVEL & TOURISM DEMAND

London International and Domestic Nights in Paid Accommodation (2019-2024) Domestic Nights in Paid Accommodation

Recovery Index Based on 2019

151,000 150%

106%

Domestic and International Nights

100% 97%

82% Paris (FR)

Recovery Index

101,000 100%

60% Brussels (BE)

38% Berlin (DE)

51,000 50%

(000s)

Vienna (AT)

1,000 0%

Amsterdam (NL)

2019 2020 2021 2022 2023 2024

Birmingham (UK)

London (UK)

Domestic nights in paid accommodation International nights in paid accommodation Manchester (UK)

Madrid (ES)

Overall Recovery Index to 2019 lvls

Barcelona (ES)

Source: Tourism Economics, October 2020 50 60 70 80 90 100 110 120

▪ Most of the European gateway cities, by definition, are highly exposed to

international tourism. Whilst, for many, international demand typically comes from 2024 2022 2020

a diverse array of source markets and customer segments, which would ordinarily Source: Tourism Economics, October 2020

make a market less volatile in light of external market shocks, the nature of ▪ As a result of a strong domestic demand coupled with a rebound in short-haul travel,

COVID-19 and the subsequent measures restricting cross-border tourism flows are overall accommodation demand for London is anticipated to reach approximately

having a material impact. 103m by 2023 (3% below 2019) and to fully recover and exceed 2019 levels by

▪ London is positioned as the most visited city in Europe by international travellers, 2024 with 113m overnight stays.

having attracted approximately 80m overnight stays in 2019, equivalent to 75% of ▪ The underlying demand drivers (as detailed on slide 13-14) will support this recovery

total overnight stays. Demand from long haul feeder markets such as North and subsequent growth; however, we do expect COVID-19 to leave its mark in terms

America and North East Asia (e.g. US, China) will take longer to recover to pre- of the way people travel going forward. Tourism and leisure service providers, which

pandemic levels, which means for London that international overnight demand is can align their product offer with the demands of the modern-traveller, plus an

forecast to only recover by 2024/2025. additional focus on safety and hygiene, are likely to perform strongly in the

▪ However, London is well placed to benefit from a recovery in demand from short- anticipated recovery.

haul feeder markets, including France, Germany, Spain and Italy, which overall ▪ This is particularly the case for the serviced apartment sector (including apart-hotels),

have accounted for approximately 50.0% of the city’s overnight stays in 2019. which has proven to be one of the most popular accommodation types during the

▪ In contrast to international demand, Tourism Economics forecasts domestic pandemic. Going forward, we expect travellers to express some apprehension about

demand for overnight accommodation to have exceeded 2019 levels considerably staying in transient accommodation and potentially coming into contact with others, at

by 2024. This would suggest that in the short-to-medium term, London, in line least in the short-to-medium term. As a result, and based on the trends to date, this is

with other major European gateway destinations, are likely to adapt and cater to a likely to benefit the performance of serviced apartments over traditional hotels (further

more domestic audience. As mentioned previously, the adaptability of the travel details on the London serviced apartment sector are provided on slide 30-32.)

and tourism industry has supported its recovery following previous downturns.

CBRE | HAMMERSMITH GROVE 17EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

TRAVEL & TOURISM DEMAND

Downside Risk Scenario Analysis

UK Inbound and Domestic Overnight Visits (Recovery Index Based on 2019)

120,000

100,000

116%

111% 112%

103% 107%

80,000

90% 97%

60,000 75%

70%

40,000 47%

36% 34%

20,000

0

2019 2020 2021 2022 2023 2024 2025

Source: Tourism Economics, October 2020 Inbound Visits Domestic Visits

▪ Downside risks remain for the UK travel outlook as infections continue to rise in the absence of a widespread vaccine and new lockdown measures have been re-introduced

across a number of European countries.

▪ The above graph compares the latest baseline scenario from Tourism Economics against a downside scenario. The downside scenario reflects the risk of travel restrictions

lasting 18 months, compared to the 10-month period assumed in the baseline forecast. In such a scenario, a weaker economic outlook coupled with prolonged travel

restrictions would further depress consumer confidence and result in a sharper drop in tourism activity.

▪ As illustrated by the above graph, this would mean that overall volume of domestic and overnight visits to the UK would only regain 2019 levels by 2024, one year later than

in the baseline scenario. A similar impact would likely to be expected for the recovery of overnight stays.

▪ However, we note that even under the downside scenario, tourism demand is anticipated to ultimately recover to pre-pandemic levels.

CBRE | HAMMERSMITH GROVE 18EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

TRAVEL & TOURISM DEMAND

Leisure Demand

Key Leisure Attractions

DISTANCE FROM SITE (PUBLIC

ATTRACTION CATEGORY ANNUAL VISITORS ▪ Hammersmith has established itself as a vibrant area,

TRANSPORTATION)

Westfield Shopping Centre Shopping Centre 27,500,000 14 minutes entertainment-hub and as a hotbed for creativity. The

area is sought after by those seeking good connectivity

Natural History Museum Museum & Art Galleries 5,423,932 20 minutes

as well as a suburban atmosphere.

Victoria & Albert Museum Museum & Art Galleries 3,992,198 18 minutes

▪ Riverside studios, the Lyric Theatre and the

Science Museum Musum & Art Galleries 3,301,975 20 minutes

Hammersmith Apollo Theatre are some of the main

Royal Albert Hall Concert Hall 1,700,000 33 minutes demand drivers of the area. Moreover, the

Saatchi Gallery Museum & Art Galleries 1,200,000 23 minutes pedestrianised riverside includes pubs, rowing clubs and

Design Museum Museum & Art Galleries 600,000 15 minutes the Furnival Gardens.

Kensignton Palace Historic Properties 510,304 28 minutes ▪ Further London key tourism drivers are in close

WWT London Nature Reserve 190,206 40 minutes proximity as the adjacent table shows. This includes

Osterley Park House Historic Properties 82,151 40 minutes some of London’s most visited cultural attractions such

The Queens Club Sports Venue n/a 11 minutes as the Natural History Museum, V&A Museum, the

Science Museum and the Royal Albert Hall, combined

Kyoto Garden & Holland Park Gardens n/a 27 minutes

attracting close to 15m visitors per annum.

Craven Cottage (Fulham FC) Sports Venue n/a 23 minutes

▪ The proposed Apart-Hotel is also in proximity to two

Stamford Bridge (Chelsea FC) Sports Venue n/a 30 minutes

football stadiums, including Stamford Bridge, home of

Premier League Club Chelsea and Craven Cottage, the

home ground of Premier League Club Fulham F.C.

Both venues are strong accommodation demand drivers

on match and event days. Adding to the local area’s

sports offer is the Queens Club, a tennis venue with

capacity for more than 9,000 people, hosting a number

of annual tournaments including the Queen's Club

The local area benefits from a multitude of leisure demand generators ranging from major retail destinations to museums and Championships, part of the ATP World Tour 500 series.

sport venues. The majority of these demand generators are located within a 30-minute tube ride of the proposed Apart-Hotel

▪ The 2016 London Plan (Policy 4.5) and the Intend to

site and attract a large number of international and domestic tourists throughout the year. Publish London Plan 2019 (Policy E10) both support

London’s visitor economy and require boroughs to

stimulate growth, taking account of the need of

business and leisure visitors. The proposed development

is therefore aligned with the London Plan by improving

the quality and range of accommodation in proximity to

major visitor attractions.

Source: CBRE Research, Visit England, 2020

CBRE | HAMMERSMITH GROVE 19EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

LOCAL ECONOMY

GDP Growth, 2018-2024F CBRE ANALYSIS

▪ Hammersmith is a key business and commercial centre in the West of London.

10% 7.5% Following the closing and redevelopment of its power stations and factories, the area

has moved from an industrial base towards a greater focus on commerce and

5%

services.

0% ▪ The district is a dynamic and rapidly developing area, known for its diverse cultural

y/y growth %

influences. TV and new media industries are of significant and growing importance.

(5)% ▪ In line with the wider city and other European regions, the local economy has been

severely impacted by the containment measures put in place to limit the spread of

(10)% COVID-19 with Oxford Economics predicting GDP to contract by approximately

-9.7%

10.0% in 2020.

(15)%

2019 2020 2021 2022 2023 2024 ▪ For 2021, the local economy is anticipated to see a strong rebound, growing by

7.5%, fully recovering to pre-crisis levels by 2022. Between 2020 and 2024 the local

UK Kensington and Chelsea & Hammersmith and Fulham European City Average economy is forecast to outpace both the UK and European city averages with GDP

growing by 4.1% per annum. This highlights the underlying strength and resilience of

Source: Oxford Economics, 2020 the local economy. The recovery will particularly be driven by the business services and

information and communication sector, which is forecast to account for half of the

GDP Structure Kensington and Chelsea & hammersmith and Fulham GDP growth over the next four years.

(% Share of Total, Inner Circle 2019, Outer Circle 2024F) ▪ Due to the impact of COVID-19 on the local economy, there will undoubtedly be a

decline in office demand over the short-term. With companies being forced to move

2% their workforce to remote working, demand levels have been further impacted in

8%

recent months. Accelerated by the current market environment, the role of the office is

8% 2% 16% likely to continue evolving with an emphasis on the importance of collaboration and

16% innovation to employee productivity. Whilst this means that the function and design of

Agriculture, mining & utilities

office space will change, it is unlikely that these trends will have a considerable impact

Manufacturing on the aggregate level of office space required. There will be cases of companies who

Construction will reduce space requirements but the economic recovery and de-densification is likely

35% 35% Trade, transport & storage to balance this out, reducing the overall impact.

22% Information & communication

23% ▪ Based on this, we expect Hammersmith to remain a key office location with companies

Finance & insurance

of national and international significance providing strong levels of accommodation

Public services demand.

15%

Business services

▪ New quality accommodation such as the proposed Apart-Hotel will increase the area’s

14% Hospitality & other services

appeal to new corporate occupiers and help to further strengthen the local economy.

Source: Oxford Economics, 2020

CBRE | HAMMERSMITH GROVE 20EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

LOCAL ECONOMY

Corporate Demand

Demand Drivers from the Public and Private Sector

▪ Most employment in Hammersmith is office based while non-office based

employers mainly comprise of public services, including Hammersmith

Hospital, Charing Cross Hospital and Queen Charlotte’s & Chelsea

Hospital.

▪ The traditional office stock is located to the East of Hammersmith centre on

Hammersmith Road, Butterwick and Shortlands. Due to a scarcity of

development sites, office development has moved outside of these areas and

includes 10 and 12 Hammersmith Grove located to the North of the Centre.

Featuring some of the highest quality space in the market, both buildings are

fully let to Philip Morris, Fox International and WeWork, amongst others.

▪ White City, situated to the north of Hammersmith has also developed into an

important alternative office location within the marketplace. This was in part

driven by the opening of the Westfield Shopping Centre in 2008 and a

number of regeneration schemes, which delivered new office and residential

space as well as transport upgrades and improvements to the public realm.

Notable occupiers include the BBC, who partially re-occupied a re-

developed a site following the transfer of more than 4,000 staff to

Manchester and Central London in 2013, ITV, and Publicis Media with

2,000 employees. Further high profile media occupiers include Walt Disney

Company and Virgin Media Group, both located on Hammersmith Road.

▪ White City is also home to a number of pharmaceutical companies, which

are attracted to the local area due to the presence of nearby Imperial

SUBJECT SITE College Campus. The most notable in-mover is Novartis, who relocated

their UK HQ from Frimley in January 2020.

▪ There are also a number of retail based employers, including Harrods, Yoox

Net-a-Porter, Ralph & Russo and the HQ of Victoria Beckham.

In line with pre-COVID-19 trends, we anticipate Hammersmith to remain an

important economic driver of the London economy and major office location. In a

post-pandemic world, the local area is likely to continue attracting occupiers who

wish to capitalise Hammersmith's excellent connectivity, comparatively low

occupational costs and strong amenity provision.

Source: CBRE Research, Promis Office Report, 2020

CBRE | HAMMERSMITH GROVE 21EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

LOCAL ECONOMY

REGENERATION SCHEMES

On the following two pages we present key existing and planned development projects that will enhance the local area and positively impact existing and future hotel supply.

White City Gateway Olympia Earls Court Redevelopment

(1.5 miles from site) (0.9 miles from site) (1.7 miles from site)

▪ Construction commenced in ▪ Planning permission was granted in ▪ After several years of stalled

October 2020 on the Gateway 2019 for a £1.3bn project to turn progress on the proposed

Central building at White City Place, Olympia London into an arts, redevelopment of Earls Court, a

just south of the Westway. entertainment, events and creative new developer, Delancey, took over

▪ The scheme will provide a total floor business quarter. This will include from Capital Counties in 2019 and

space of over 260,000 sq ft and is the redevelopment of the former has recently appointed architects to

scheduled for completion at the end exhibition centre to provide a produce a new masterplan for the

of 2022. 4,100-capacity music venue, a area.

1,400-seat performing arts theatre, ▪ The original scheme was anticipated

▪ In early 2020, L’Oreal confirmed two hotels, a cinema, and 2.5 acres

plans to be an anchor tenant of the to provide 7,500 new homes,

of public space. 10,000 new jobs and state-of–the–

scheme, relocating from their

current headquarters in ▪ The main construction contract is art health, education, cultural and

Hammersmith. expected to be awarded soon with community facilities.

initial work on the scheme due to

begin in 2020.

Scheduled Completion: 2022 Scheduled Completion: 2024 Planning

Source: developmentfinancetoday, exhibitionworld, imperial.ac.uk, commercialnewsmedia, CBRE Research, 2020

CBRE | HAMMERSMITH GROVE 22EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

LOCAL ECONOMY

REGENERATION SCHEMES (CONTINUED)

Imperial College London, White City Campus (1.4 miles from site)

▪ Imperial College London, White City Campus (ICL) has seen a rapid transformation over the past five years, following the opening of the first building in 2012 to accommodate

postgraduate students. In line with the regeneration of the wider White City area, such as the transformation of the Television Centre (former HQ of BBC), ICL has created an

integrated collaborative campus, with embedded corporate, academic and community partners. Key delivery milestones included the opening of several multidisciplinary research

facilities such as the Translation & Innovation Hub in 2016 and the Molecular Sciences Research Hub in 2018.

▪ Ongoing development projects at present, include the delivery of additional office, research and laboratory space across two developments: Scale Space and the 13-storey The

Sir Michael Uren Hub. The first and largest building of Scale Space was completed in Q3 2020 with the construction of the two other buildings currently underway and estimated

for completion in Q1 and Q3 2021. In total, Scale space will provide approximately 200,000 sq ft of office space for smaller start-ups and biotech firms. The Sir Michael Uren

Hub is earmarked for completion in 2020 and will accommodate over 500 engineers, clinicians and scientists who will work together on developing new medical technologies.

▪ In addition to ongoing development projects, the ICL was granted outline planning application in September 2019 to redevelop a 14 acre site located south of the Westway on

Wood Lane. ICL’s long term vision for the £1.3bn development is to provide flexible buildings and facilities which will co-locate businesses, researchers, academia and the local

community to support collaboration and innovation.

The ongoing expansion of the Imperial College London, White City Campus with additional office, research and laboratory space as well as

Source: developmentfinancetoday, exhibitionworld, the current construction of the White City Gateway will further enhance the local area’s reputation as a destination for research, innovation,

imperial.ac.uk, commercialnewsmedia, CBRE Research, culture, commerce and retail. The nature of these developments are likely to attract further students and high-profile companies to the area,

2020 and we foresee an increased need for quality accommodation, particularly accommodation that caters for longer staying guests on project

work, for example.

CBRE | HAMMERSMITH GROVE 23EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES MARKET TRENDS 03

LOCAL ECONOMY

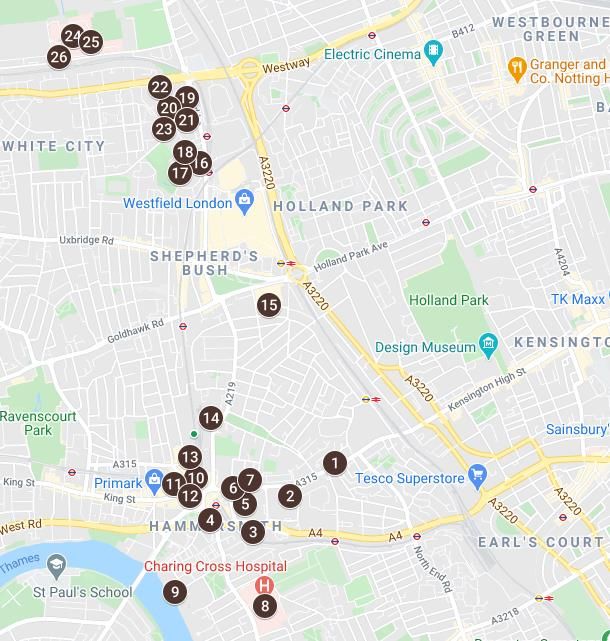

MAP OF KEY REGENERATION PROJECTS

SUBJECT SITE

Source: Google Maps, 2020

CBRE | HAMMERSMITH GROVE 24HOTEL MARKET 04

EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES HOTEL MARKET 04

HOTEL MARKET

SUPPLY OVERVIEW

Hotel Clusters, 1-Mile Radius of the Site

▪ There are currently 4,310 bedrooms (59 hotels) within a 1-mile radius of the proposed

Apart-Hotel, the majority of which are categorised as 2-star (24 hotels). However, more

than half of the total number of bedrooms are 4-star rated.

▪ The hotel stock is centred around the Hammersmith Underground station, King Street,

Shepherds Bush Road and Kensington Olympia Underground station.

▪ The Hammersmith hotel market is dominated by small, independent and budget

accommodation. Budget accommodation, which includes hostels and 2-star hotels,

accounts for 46.0% of the total supply (in number of hotels), with the majority of these

hotels having less than 50 bedrooms and no association to any brand. In terms of total

hotel bedrooms, 4-star rated hotels account for the majority of rooms in the market (54%).

▪ In terms of serviced apartments, we have identified a total of nine properties with 537

bedrooms, which represents 12.5% of the total bedroom stock of the local market. This

includes an number of branded properties such as Residence Inn, SACO and Clarendon

Serviced Apartments. With the exception of the Residence Inn property in West Kensington

with 319 keys, local serviced apartment providers are small and feature on average 27

bedrooms.

Existing Supply by Class 1-Mile Radius of the Site

▪ Whilst the current serviced apartment provision is small in size relative to other hotel

2,500 30 categories, the presence of well-known apartment operators demonstrates that there are

24 good levels of long-stay demand in the market.

2,000 25

20

1,500 2,306 Hotels 59

Number of Hotels

Number of Bedrooms

9 10 9 15

1,000

10

Bedrooms 4,310

4 3

500

651 537

5 Branded (Based on rooms) 30.5%

411

0 217 188 0

4-star 3-star 2-star Budget Apts Hostel Independent (Based on rooms) 69.5%

Bedrooms Hotels

Source: STR, 2020. Republication or other re-use of this data without the express

>100 rooms 15.3%

written permission of STR is strictly prohibited.

CBRE | HAMMERSMITH GROVE 26EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES HOTEL MARKET 04

HOTEL MARKET

Pipeline Overview Hotel Pipeline by Planning Status

▪ Based on data from AM:PM, we are aware of the current development of one serviced apartment

within a one-mile radius of the proposed development. In addition to this, there are a further nine 2,000 15

projects with 1,896 bedrooms currently in final planning stages and eleven projects with 923

bedrooms planned or deferred. 1,800

1881

1,600

− The only confirmed hotel project at present is the Dorsett Shepherds Bush London Apartments II 1,400

with 74 bedrooms, due for completion in May 2021. The property will be positioned adjacent

1,200

to the existing Dorsett Shepherds Bush 4-star hotel, which opened in 2014 and comprises 317

Number of Bedrooms

bedrooms and suites. The newly developed Dorsett property is likely to benefit from operational 1,000 29

synergies with its sister property, such as the sharing of staff and facilities, and at the same time 800

offer an accommodation product geared towards longer-stay corporate and leisure travellers. 600 799

Dorsett Shepherds Bush London Apartments II will be positioned as an upscale hotel with a bar, 400

a high-end restaurant and a café.

200 74 69 26

▪ Whilst we are not aware of any further confirmed hotel projects, there are a total of nine projects in 0

final planning stages with full planning approval from the local council. However, we expect a number In Construction Final Planning Planning Deferred

of these projects to be delayed, deferred or to be put on hold indefinitely due to the current market

environment and impact of COVID-19 on the lending market. This is in line with trends observed New Construction Expansion

across the wider European hotel landscape, with projects being re-evaluated due in part to anticipated

financing challenges and changes in market conditions over the short to mid-term. Notable projects

with full planning approval include: Based on our research there is currently one confirmed hotel development

− A dual-branded hotel development by Dominvs Group, including a 425-key Hilton Garden Inn within a 1-mile radius of the proposed Apart-Hotel. However, there are

and a 400-key budget hotel. The hotel complex was granted planning approval by also nine projects with 1,896 bedrooms in final planning stages. Although

Hammersmith & Fulham Council in July 2020; and this represents a strong speculative pipeline, it demonstrates the growing

demand for quality hotel accommodation as the local area continues to

− There are approved plans for the development of two hotels as part of the wider regeneration of

the Olympia site (0.9 miles from the subject site). We understand that funding for the hotels is in

see high levels of regeneration and development activity.

place and that the owners of the site are currently in advanced negotiations with two potential Whilst there was already a clear need for additional hotel supply pre-

hotel operators, both of which are positioned within the 4-star segment. COVID-19 (see slide 35), future hotel developments, such as the proposed

scheme, will further complement the local accommodation offer and

support the delivery of regeneration and commercial development projects.

The proposed development is therefore likely to make a positive

contribution to the local economy in terms of employment, visitor spend

and service contracts.

Source: STR, 2020. Republication or other re-use of this data without the express written permission of STR is strictly

prohibited.

CBRE | HAMMERSMITH GROVE 27EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES HOTEL MARKET 04 HOTEL MARKET Pipeline Overview HOTEL NAME GRADE ROOMS BRAND PLANNING STATUS POSTCODE PROJECT TYPE DUE 2021 Dorsett Shepherds Bush London Apartments II Apts 74 Dorsett Under Construction W12 8QE New Construction SUBTOTAL 74 FINAL PLANNING Hammersmith Magistrates Court - hotel 2 Budget 400 TBA Approved (2020) W6 8DN New Construction Hilton Garden Inn London Hammersmith 3 425 Hilton Garden Inn Approved (2020) W6 8DN New Construction Hellenic Hotel 2 1 Independent Approved (2017) W6 7LR Extension Hoxton Shepherd's Bush 4 214 The Hoxton Approved (2019) W12 8TX New Construction Landmark House site 4 288 Independent Approved (2018) W6 9DR New Construction National Hotel 4 123 Independent Approved (2019) W14 8UX New Construction Olympia Hotel 4 242 Independent Approved (2019) W14 8UX New Construction Premier Inn Shepherd's Bush Budget 189 Premier Inn Approved (2019) W6 7AN New Construction So Sienna Apts 14 Independent Approved (2018) W6 0LS Extension SUBTOTAL 1,896 PLANNING & DEFERRED 11 -114 North End Road 3 46 Independent Planning W14 9LE New Construction Aparthotel Adagio London Hammersmith Apts 240 Aparthotel Adagio Planning W6 8DA New Construction Bakery House Apts 16 Independent Planning W12 7EN New Construction Chiswick Rooms 4 25 Independent Planning W6 0SA Expansion Hammersmith Grove Hotel Apts 85 Independent Planning W6 7HA New Construction Motel One London Hammersmith Budget 400 Motel One Planning W6 0LG New Construction So Sienna Apts 4 Independent Planning W6 0LS Expansion The Clarence Hostel 12 Independent Planning W14 9PP New Construction Abercorn House Hostel Hostel 26 Independent Deferred W6 7DS New Construction Holiday Inn Express London Hammersmith Budget 60 Holiday Inn Express Deferred W6 0QU Expansion Kensington West Hotel 2 9 Best Western Deferred W14 8SN Expansion SUBTOTAL 923 TOTAL 2,893 CBRE | HAMMERSMITH GROVE 28

EXECUTIVE SUMMARY PROPOSED SCHEME MARKET TRENDS HOTEL MARKET PROJECTIONS APPENDICES HOTEL MARKET 04

HOTEL MARKET

The London Serviced Apartment Sector

London Serviced Apartments Supply Evolution 2017-2022F The following four slides provide an overview of the London serviced apartment sector, including supply

statistics, performance trends pre- and during the current pandemic as well as general operating

characteristics.

15,000 11%

▪ The London serviced apartment landscape has seen a notable increase in development activity over the

14,000 9% last few years with rooms supply growing by 3.3% per annum between 2017 and November year-to-date.

13,000 ▪ Whilst serviced apartments were historically dominated by small scale owner operators, over recent years,

7% a number of high profile operators have opened properties in London. This includes new lifestyle brands

12,000 such as Locke, Wilde Aparthotels by StayCity, STAY by the LABS Collective and room2. These concepts

5%

11,000 target a new generation of travellers who increasingly combine business travel with leisure time (i.e bleisure

3% travel) and thus desire a flexible accommodation offer, combining work and play.

10,000

▪ In addition to new brands, established groups such as Adagio and Native have also continued to expand

9,000 1%

their presence in the market place.

8,000 -1% ▪ Driven by the ongoing success and resilience of the serviced apartment model, recent development trends

2017 2018 2019 2020 Due 2021 Due 2022 are likely to continue.

Total Rooms Pipeline % change ▪ Based on data from AM:PM Hotels there are currently a total of 18 serviced apartment projects scheduled

to open over the next two years in London with a total of 2,145 rooms. Pipeline projects are generally

London Top 10 Branded Serviced Apartments evenly distributed across Central London. This is with the exception of the City fringe area around Aldgate,

which has a notable cluster of three pipeline projects, including high profile brands such as Locke, Wilde

Citadines by Staycity and Adagio. With already a strong presence of serviced apartment operators on the City

fringes, development activity is likely driven by strong demand generated by existing and new office

StayCity Serviced Apartments

developments. This includes the Whitechapel area, which is seeing increased investment activity in

Marlin Apartments anticipation of the arrival of the Elisabeth Line.

Locke ▪ Canary Wharf is another area in London that has a very high density of serviced apartment

Residence Inn accommodation, accounting for 22.0% of total accommodation supply. This compares against the wider

Bridgestreet Accommodations London market, where serviced apartments only account for 7.0% of total bedroom supply. This highlights

the popularity of extended stay product in office locations with a high proportion of national and

City Apartments

international companies.

Cheval Residence Group

SACO Based the existing presence of serviced apartments in London and future development trends, we consider the

Clarendon Serviced Apartments proposed location in Hammersmith to present a highly suitable location for the development of an extended stay

product. This takes into account the strategic location of the site in relation to key transportation links as well as

major international corporate demand drivers and leisure attractions. Further to this, the development of an extended

Existing Beds Pipeline

stay product is considered to be more resilient to absorb demand shocks such as COVID-19, as will be detailed on the

Source: STR, 2020. Republication or other re-use of this data without the

express written permission of STR is strictly prohibited.

following pages.

CBRE | HAMMERSMITH GROVE 29You can also read