Wilton Junction Employment Projections & Land Need May 2014 - Amazon AWS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Wilton Junction

Employment Projections & Land Need

May 2014

MacroPlan Dimasi MELBOURNE SYDNEY Level 4 Level 4 356 Collins Street 39 Martin Place Melbourne VIC 3000 Sydney NSW 2000 (03) 9600 0500 (02) 9221 5211 GOLD COAST PERTH Suite 5 Ground Floor 492 Christine Avenue 12 St Georges Terrace Robina QLD 4226 Perth WA 6000 (07) 5562 0767 (08) 9225 7200 Prepared for: Client Name Wilton Junction Landowners Group MacroPlan Dimasi staff responsible for this report: Wayne Gersbach NSW State Manager James Turnbull Senior Economist David Dragicevic Senior Economist Luke Crawford Analyst

Table of Contents

Executive Summary ..................................................................................6

Introduction ........................................................................................... 10

Project Background 10

Study Area 11

Land Ownership 14

Vision for Wilton Junction 16

Delivering the Vision and Project Description 16

Employment Projections and Land Need 17

SEPP Study Requirements 20

Section 1: Employment Forecasts ............................................................. 22

1.1 Wollondilly’s Population and Employment Base 22

1.2 Regional Employment Conditions 23

1.3 Employment Projections 30

1.4 Future Industry Composition 35

1.5 Employment Staging & Sequencing 43

1.6 Employment Outcomes 46

1.7 Employment Land Need 48

1.8 Testing our Employment Estimates 50

1.9 Infrastructure Considerations 51

Section 2: Retail Needs & Delivery Implications .......................................... 54

2.1 Trade Area Definition 54

2.2 Trade Area Population 59 2.3 Socio-demographic Profile 61 2.4 Retail Expenditure Capacity 64 2.5 Retail Floorspace Demand 69 2.6 Traditional Retail Competition 70 2.7 Bulky Goods Competition 74 2.8 Capture Rates 76 2.9 Supportable Floorspace 78 2.10 Retail Composition & Siting 80 2.11 Retail Land Requirements 83 2.12 Retail Distribution across Wilton Junction 84 2.13 Timing & Staging of Delivery 85 2.14 Potential Employment 88 2.15 Potential Impacts on Surrounding Centres 91

This page has been intentionally left blank.

5

Executive Summary

MacroPlan Dimasi has prepared this report to inform the SEPP-based rezoning of

Wilton Junction. Specifically our undertakings seek to project the magnitude,

timing and type of employment that is expected at the new township of Wilton

Junction. In doing so, the report specifically addresses the Director General’s

Requirements (DGRs) for the SEPP-based rezoning, as outlined by the

Department of Planning & Infrastructure (DPI).

The projected employment outcome for Wilton Junction (as at 2041) is

summarised as follows:

Population and Jobs In Wilton Junction (2041)

Count

Total Residents 34,955

Employed Residents 12,000-13,200

Jobs in Wilton Junction 10,440-11,770

Work from home & not fixed 1,560-1,770

Jobs in designated EL 8,880-10,000

We project that the majority of the expected employment will be in the form of

service-based industries that cater to the needs of Wilton Junction’s population

growth i.e. predominantly population driven (approximately 60%). While less in

absolute terms, other ‘external’ industries are also expected to locate at and

generate jobs in Wilton Junction.

We provide a detailed account of likely industries that may be attracted to Wilton

Junction and provide a staging sequence of industry growth and associated

employment. We also consider the employment consequences of major

infrastructure investment in the area (e.g. the Maldon-Dombarton rail extension

and the Brisbane-Melbourne fast train) but do not base our employment

projections on these projects.

Wilton Junction – Housing & Employment Needs

6

WJLG

Our report provides a market-based estimation of the likely retail floorspace

needs associated with a new township of 34,955 people and considers the

delivery and employment implications of this provision.

We anticipate that Wilton Junction will accommodate approximately 70,000m2 of

retail floorspace, inclusive of bulky goods retailing and neighbourhood centres.

This floorspace is sufficient to underpin a vibrant town centre offering and other

neighbourhood or recreation based provisions.

Wilton Junction – Recommended Indicative Retail Composition

Wilton Junction - Indicative Com position

Land Area

Centre Role & Function Retail Size (GFA sqm ) Tim ing Land Uses

(Net) (ha)

Primary retail and commercial 2017 onw ards 1 x DDS, 2 x supermarkets, specilaty

Tow n Centre 25,000 sq.m 7.5-10 ha

centre. (various stages) retail and secondary retail

Local services and

Bulky goods and highw ay oriented

Bulky Goods employment as w ell as 30,000 sq.m 7.5-10 ha 2020 onw ards

retail

serving passing traffic

Supporting convenience retail 2017 onw ards Small supermarket/s plus retail and

Village Centre/s 10-12,000 sq.m 5 ha

and business services. (various stages) non-retail specialties

Small shop/s, Convenience shops, local services,

Local Shop/s & 2017 onw ards

cafes/restaurants and 4,000 sq.m 1-2 ha and small mixed use precinct near

Mixed Use (various stages)

offices lakeside

Total WiltonJunction Retail Floorspace 65,000-70,000 sq. m 20-25 ha

*Net o f lo cal ro ads and parks etc

NB : To wn centre FSR = 0.35; village centre FSR = 0.4; bulky = 0.4

GFA : Gro ss Flo o r A rea, o f lettable flo o rspace. Do es no t include co mmo n mall area, circulatio n etc.

So urce: M acro P lan Dimasi

Our employment delivery projections are provided below. These are based on our

calculated correlation between population growth and service-based employment

sectors and on our estimation of external industry attraction given the locational

attributes of Wilton Junction.

Our delivery projections are segregated by industry based on the distinction

between being population driven or that which is likely to be attracted to locate in

the area but which will predominantly trade to broader, external markets.

7

Persons Employed & Resident Population, Wilton Junction (2016-41)

2021 2026 2031 2036 2041+

Lower Upper Lower Upper Lower Upper Lower Upper Lower Upper

Employment 1,805 2,060 4,065 4,601 6,304 7,131 8,577 9,690 10,440 11,770

Non-WJ residents working in WJ 353 443 794 989 1,232 1,533 1,676 2,083 2,040 2,530

Self contained jobs 1,452 1,617 3,270 3,612 5,072 5,598 6,901 7,607 8,400 9,240

Work from home & not fixed location 271 309 610 690 946 1,070 1,286 1,453 1,566 1,766

Employed residents in WJ employment lands 1,181 1,308 2,661 2,922 4,126 4,529 5,614 6,153 6,834 7,475

Predominantly Population Driven

Retail Trade 345 360 920 960 1,380 1,440 1,840 1,920 2,300 2,400

Education and Training 113 120 375 400 525 560 675 720 750 800

Health Care and Social Assistance 240 280 480 560 720 840 960 1,120 1,200 1,400

Electricity, Gas, Water and Waste Services 25 50 50 100 75 150 100 200 100 200

Public Administration and Safety 180 204 360 408 480 544 600 680 600 680

Arts and Recreation Services 42 60 84 120 112 160 126 180 140 200

Other Services 120 156 240 312 360 468 480 624 600 780

Financial and Insurance Services 24 30 48 60 96 120 128 160 160 200

Rental, Hiring and Real Estate Services 13 20 23 36 33 52 43 68 50 80

External & Other

Manufacturing 70 79 140 158 315 356 525 593 700 790

Construction 64 68 160 170 288 306 480 510 640 680

Wholesale Trade 150 158 300 316 450 474 600 632 750 790

Accommodation and Food Services 75 84 150 168 275 308 400 448 500 560

Transport, Postal and Warehousing 105 119 245 277 420 474 595 672 700 790

Information Media and Telecommunications 10 18 20 36 30 54 40 72 50 90

Administrative and Support Services 125 138 225 248 325 358 425 468 500 550

Professional, Scientific and Technical Services 105 117 245 273 420 468 560 624 700 780

Total 1,805 2,060 4,065 4,601 6,304 7,131 8,577 9,690 10,440 11,770

Wilton Junction – Housing & Employment Needs

8

WJLG

Finally, we estimate the amount of land that the employment sectors are likely to

require across the Wilton Junction master-planned area. We anticipate that a

provision of between 140 and 163 hectares is required for employment land

purposes. This estimate is a gross figure and includes open space, building

setbacks, parking and interior and external roadways. It does not include the land

area required for schools/education purposes or other community facilities and

assets.

Employment Land Need, Wilton Junction

GFA FSR

Land Owner Land (hectares)

Lower Upper Lower Upper

Retail 65,000 75,000 0.3 0.3 20.0 25.0

Commercial* 86,343 101,592 1.0 1.0 8.6 10.2

Industrial 334,305 384,285 0.3 0.3 111.4 128.1

Total 485,648 560,877 1.6 1.6 140.1 163.3

** Other includes existing Township

*Excludes schools/education and community Source: MacroPlan Dimasi

**FSR applied to GFA to derive total land allocation

A separate strategy for driving employment outcomes at Wilton Junction is

provided under separate cover.

Wilton Junction – Housing & Employment Needs

9

WJLG

Introduction

Project Background

In November 2011, the State Government invited landowners with large

properties in suitable locations to nominate sites which might be able to deliver

additional housing to address Sydney’s housing supply shortfall. Walker

Corporation, Governors Hill, Bradcorp and Lend Lease responded to the Program

and nominated landholdings of more than 100ha in Wollondilly Shire, surrounding

the Hume Highway-Picton Road intersection for consideration. This area has

subsequently become known as Wilton Junction, and is the subject of this

application.

Following a Wollondilly Shire Council resolution in May 2012, four major

landowners (collectively known as the Wilton Junction Landowners’ Group) signed

an agreement to work cooperatively with Council in the preparation of a high level

master plan for Wilton Junction. The master plan aims to deliver high quality new

housing, jobs close to home, supporting social and utilities infrastructure and

services, and a range of complementary land uses.

A high level Master Plan and a Preliminary Infrastructure Requirements Report

were considered by Wollondilly Shire Council on 17 th December 2012, with Council

resolving to give in-principle support to the proposal. Council also resolved to

request that the rezoning be a state driven process.

Subsequently, the NSW Government decided to coordinate the statutory planning

process, led by the Department of Planning and Infrastructure (now the

Department of Planning and Environment, DP&E). The Minister for Planning and

Infrastructure (now the Minister for Planning and Environment) proposed to

prepare a State Environmental Planning Policy (SEPP), as per Section 24 of the

Environmental Planning and Assessment Act 1979 (EP&A Act), which identifies

that a SEPP is an Environmental Planning Instrument, and Section 37 of the EP&A

Act, which relates to the making of a SEPP for State or regional significant

development. This was done with a view to rezone the land through an

Wilton Junction – Housing & Employment Needs

10

WJLGamendment to the Wollondilly Local Environmental Plan 2011 (LEP) to facilitate

the early delivery of housing and infrastructure, linked to an agreed

Infrastructure, Servicing and Staging Plan.

The Department of Planning and Infrastructure issued Key Study Requirements

(KSRs) to the Proponents (Walker Corporation, Bradcorp and Governors Hill) to

guide the planning investigations for a new town at Wilton Junction. The KSRs set

the criteria for carrying out environmental investigations across the Study Area

(excluding both Bingara Gorge and the existing Wilton village which will not be

affected by any proposed amendments to their current zoning and planning

provisions). The investigations examine the potential for the Wilton Junction

Study Area to be rezoned under a SEPP.

The Department of Planning and Infrastructure has issued specific Director-

General’s Requirements (DGRs) to guide planning investigations for a new town at

Wilton Junction. The DGRs set the criteria for carrying out environmental

investigations across the site.

MacroPlan Dimasi has prepared this report to inform the SEPP-based rezoning of

Wilton Junction. Specifically our report seeks to establish the likely demographic

characteristics and housing needs of the new township of Wilton Junction. In

doing so, the report specifically seeks to address the DGRs that have been issued

to guide the necessary planning investigations.

Study Area

Wilton Junction is located within Wollondilly Shire Council and is approximately

80km from Sydney Central Business District, and 30km west of Wollongong. The

study area includes the existing village of Wilton and the adjacent Bingara Gorge

estate.

The area is strategically located around the Hume Highway/Picton Road

interchange and represents the next potential major town along this transport

corridor south of Campbelltown – Macarthur.

11Wilton Junction has the distinct advantage of a consolidated land ownership of

nearly 2,700ha in the control of recognised developers, with the resources and

capability to expedite housing delivery, roll out enabling infrastructure, deliver

social services and provide local employment.

Wilton Junction presents a good opportunity to address significant housing supply

shortages and affordability pressures in Sydney. The new town will provide

housing choice through a variety of dwelling sizes and locations. It will also

provide a new ‘district’ level retail and commercial focus for the people of

Wollondilly, deliver social infrastructure and provide jobs and services for the local

population.

Wilton Junction – Housing & Employment Needs

12

WJLGFigure 1. Study Area

Source: Connor Holmes (2014)

13Land Ownership

There are four major landowners within the Investigation Study Area:

Bradcorp Pty Ltd (land at Wilton West)

Walker Corporation (land south of Picton Road and east of the Hume

Highway)

Governors Hill (land including the Wilton Aerodrome and land on both

sides of Picton Road west of the Hume Highway)

Lend Lease (land to the north-west of the Hume Highway-Picton Road

intersection; but is excluded from the study requirements)

The Investigation Study Area includes the proponents’ land and other land held by

individual private owners, as outlined in the table below. A plan of the extent of

ownership is provided below.

Net Developable

Land Owner Gross area (ha)

Area (ha)

Lend Lease 455.0 240.0

Bradcorp 872.4 458.7

Governors Hill 175.3 123.5

Walker Corporation 405.2 230.3

Other land owners** 572.3 489.2

Total 2,480.2 1,541.7

** This comprises 113 other private landowners, excluding the new Bingara Gorge estate and the

existing Wilton village which will not be affected by any proposed amendments to the existing

Wollondilly Shire Council planning provisions.

For the purpose of this rezoning application, the Proponents include Walker

Corporation, Governors Hill and Bradcorp. Lend Lease will continue with the

planning and delivery of its Bingara Gorge community at Wilton, which is already

zoned for residential development. Lend Lease is working with the proponents to

plan and deliver the new town at Wilton Junction and its associated infrastructure.

Wilton Junction – Housing & Employment Needs

14

WJLGFigure 2. Land Ownership

Source: Connor Holmes (2014)

15Vision for Wilton Junction

The Proponents have a vision for the proposed rezoning of land at Wilton

Junction, which is:

Wilton Junction is a new community cradled in a unique landscape characterised

by bushland, rivers, creeks, lakes and ridges set against the backdrop of the

Razorback Range. By design, the place and the lives of its people are intertwined

with the bush.

The community respects the location’s rich bushland setting, engages with

surrounding water features and embraces sustainability.

Inclusive and welcoming of diversity, it’s a place to nurture relationships, grow a

family - to put down roots.

Founded on a 21st century interpretation of timeless "Garden City" principles,

Wilton Junction combines the best features of our most loved country towns with

the facilities, services and technologies found in Australia's most successful, edgy,

and vibrant town centres.

A safe place to visit – a healthy place to live – a great place to learn - a rewarding

place to work – the local community takes pride in the strength of its cultural and

civic life and the role of their town in Wollondilly Shire and the region.

Delivering the Vision and Project Description

The vision will be delivered through the creation of a new town with between

11,000 and 13,000 new homes and 11,000 jobs. Residential neighbourhoods will

be created around green spaces to provide a range of housing choice and to

facilitate healthy lifestyles options for residents.

A new town, comprising of approximately 17ha, will be established within the

north-west quadrant of the study area and will be surrounded by employment

generating uses for business, bulky goods and light industry. It will comprise of

approximately 120-130ha of land.

Smaller neighbourhood centres will be created within the residential

neighbourhoods to cater for convenient daily shopping choices. Social and

physical infrastructure will also be provided facilitating the creation of a new

community. Existing significant environmental features and heritage items will be

preserved commemorating the natural and historical setting of the study area.

Wilton Junction – Housing & Employment Needs

16

WJLGThe proposed Master Plan will be informed by the following key principles:

Employment and commercial drivers. The delivery of approximately

11,000 jobs focused around a new town centre and in close proximity to the

Hume Highway & Picton Road.

Housing. Providing between 11,000 and 13,000 new dwellings across the

precinct, inclusive of the 1,165 already approved at Bingara Gorge.

Community facilities. Providing a diverse range of high quality community

facilities including a range of schools, a library, a community centre and

three neighbourhood centres.

Environment. Conserving ecological features and biodiversity and

establishing a Trust to rehabilitate and manage approximately 630 ha of

bushland.

Place making. Delivering a high quality and connected network of streets,

spaces and squares throughout the development.

Activity centres. Focusing on the delivery of a new town centre and three

smaller neighbourhood centres with a diverse mix of retail, commerce,

business & light industry.

Traffic and transport. Providing strategic motorway and bus access to

surrounding areas and legible movement throughout the development.

Infrastructure. Integrating water, waste water and stormwater

management systems and access to all other utilities including gas and NBN.

Employment Projections and Land Need

This report forms part of a series of studies required to be undertaken to meet the

Director Generals’ Study Requirements outlined by the NSW DPI (now the DP&E)

to inform SEPP-based rezoning process.

Our report focuses on the potential employment outcome for Wilton Junction and

the resultant land take required to accommodate employment land uses. Our

report considers the characteristics and forces that will drive the likely

employment outcomes for the township.

17We assess need through our analysis of recent ABS Census 2011 data and by

examining prevailing local and regional market forces as well as, where

appropriate, the experiences of other ‘like’ locations.

Our employment forecasts are derived in a manner that considers the likely level

of employment generated by industries that are predominantly population driven

or service-based and others that are underpinned by external markets. In doing

so we reference the employment influence of south-west Sydney but also have

regard for the unique locational attributes of Wilton Junction as a stand-alone

township and as the major centre/hub for the broader Wollondilly LGA, i.e. we

consider Wilton Junction as a distinct and primary township within the LGA, able

to support its own employment and service needs and to trade beyond its local

borders.

The report’s outcomes and findings have informed the development and

preparation of a Master Plan for Wilton Junction.

The derived Master Plan is presented below.

Wilton Junction – Housing & Employment Needs

18

WJLGFigure 3. Wilton Junction Master Plan

19SEPP Study Requirements

In preparing our report, MacroPlan Dimasi has considered the specific Director-

General’s Requirements (DGRs) pertaining to the investigation of ‘Economic

Development and Employment Need’.

The schedule below provides a concise response to each specific DGR item

addressed in the report.

DGR Item Response

Prepare an assessment of the retail, MacroPlan Dimasi has undertaken an assessment of

commercial, industrial and other employment outcomes and employment land need based on

employment needs for the projected demand from the future resident population, and the

population of the Precinct and wider comparative advantages (i.e. location and accessibility)

LGA to support the preparation of a presented at Wilton Junction.

local economic development Our findings support the development of a local employment

strategy, including impacts on strategy, provided under separate cover to this report.

existing towns within the LGA Our examination of employment need has considered the

likely level of employment generated by industries that are

predominantly population driven or service-based and others

that are underpinned by external markets. Our report

references the employment influence of south-west Sydney

but also has regard for the unique locational attributes of

Wilton Junction as a stand-alone township and as the major

centre/hub for the broader Wollondilly LGA.

Consider future industry dynamics Our assessment of employment need has considered both

for key sectors both currently in the historical data relevant to the Wollondilly LGA as well as trend

area and those which could benefit data from south-west Sydney. We have tested our

from locating in the area. This assumptions of employment drivers and characteristics using

requires strategic analysis and a number of exemplar regions.

should not be limited to existing On the basis of existing and projected differences between

forecasts based on historical data. Wollondilly and the south-west Sydney region, we have

estimated the employment potential of Wilton Junction as a

stand-alone township.

Identify factors that may drive Primarily, there are three factor or attributes that are

certain types of commercial, expected to support industry and employment generation at

industrial or retail development Wilton Junction, including:

investment and activity, particularly A 35,000-strong resident population will support the creation

in relation to the site’s connections of industries that are predominantly population-driven e.g.

between the Southern Highlands and retail, service provision, education, etc. Wilton Junction will

South-West Sydney and placement become the major centre/hub for the Wollondilly LGA.

Wilton Junction – Housing & Employment Needs

20

WJLGin the Sydney-Canberra-Melbourne Wilton Junction is at a strategic junction of two significant

corridor. roads (Hume Highway and Picton Road). Its locational

attributes will drive interest from externally trading

industries.

Finally, Wilton Junction’s separation from Sydney’s south

west and positioning on the Sydney-Canberra-Melbourne

trade corridor is expected to facilitate a healthy

representation of industries that predominantly operate in

external markets.

Develop an employment strategy to Our employment strategy is provided in the Economic

support a high level of employment Development and Employment Strategy report (EDES).

self-containment in the Precinct. This It provides a strategy that supports the achieving regional job

strategy should assess how jobs targets, the capturing of service-driven employment and

generated within the Precinct will proposes a series of development initiatives and promotional

contribute to jobs targets for the measures to attract external industries to facilitate local

sub-region. employment opportunities for future residents.

Through the use of case studies, a series of sector-specific

strategies are presented in detail. The EDES also comprises

of Government grants, incentives, partnership opportunities,

initiatives and business developing services available to

businesses.

21Section 1: Employment Forecasts

Our working resident and employment projections for Wilton Junction are based

on a consideration of:

Outer South West & Wollondilly LGA employment and business conditions;

Anticipated participation rates amongst working aged residents;

Employment trends in the nearby Southern Highlands;

The locational attributes of Wilton Junction and its place as the primary

centre within the Wollondilly LGA;

The likely delivery of retail and other service-based (population driven)

employment; and

The types of other industries likely to be attracted to Wilton Junction.

Notably, since our initial projections were undertaken as part of the early stage

reporting to Wollondilly Council, we also re-examine the township’s potential to

retain employment and its work-from-home potential.

1.1 Wollondilly’s Population and Employment Base

The Estimated Resident Population (ERP) of Wollondilly (2011) is:

Wollondilly – 44,403 (41,221 at 2006)

By comparison, Wingecarribee, the LGA immediately south of Wollondilly, has a

similar ERP of 44,396 persons (2011).

As at Census 2011 Wollondilly LGA had 21,300 working residents.

No individual town within the Wollondilly LGA holds a population greater than

5,000 people. The largest towns as at Census 2011 are:

Picton - 4,595

Tahmoor - 4,505

Bargo - 4,130

Wilton Junction – Housing & Employment Needs

22

WJLG Wilton – 1,890

Picton has the largest share of employment offerings within the LGA. Wollondilly

Council’s chambers are situated in Picton.

Wilton Junction is expected to accommodate around 35,000 residents upon full

development. This population will gradually build up, in sync with land and

housing development, until 2041.

1.2 Regional Employment Conditions

In order to ascertain employment trends that may impact on future industry and

employment structures at Wilton Junction we firstly consider employment and

business growth tendencies in the Outer South West Sydney SA4 region

(comprising of Camden, Wollondilly and Campbelltown SA3 regions) and across

the Wollondilly LGA in which Wilton Junction is located. We later make some

relevant comparisons with the neighbouring Southern Highlands region

(Wingecarribee Shire LGA).

Outer South West Sydney - Employment by Industry

The table below presents the number and proportion of employed persons by

industry in the Outer South West Sydney Region (OSWSR). As at February 2012,

there were approximately 203,500 employed persons in the OSWSR.

Table 1. Outer South West Sydney Statistical Region – Top 7 Employing Industries

Employed

Industry Proportion (%)

persons ('000s)

Manufacturing 17.1 13.5%

Construction 12.5 9.9%

Retail Trade 12.0 9.5%

Health Care and Social Assistance 11.9 9.4%

Transport, Postal and Warehousing 9.1 7.2%

Public Administration and Safety 9.0 7.1%

Wholesale Trade 8.3 6.6%

Source: Census 2011, MacroPlan Dimasi

23Manufacturing is the largest employing industry in the region, accounting for

around 14% of the workforce (17,100 jobs). The next largest employing industry

is Construction (9.9%), followed closely by Retail Trade (9.5%) and Health Care &

Social Assistance (9.4%).

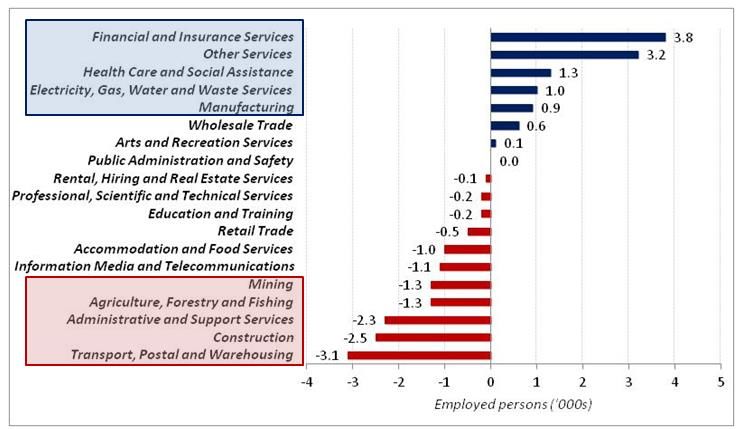

Figure 4. Change in Employment (‘000s), February 2008 – February 2012

Source: Census 2011, MacroPlan Dimasi

Over the four years to February 2012, seven industries recorded positive

employment growth. Of all industries, Financial & Insurance Services and Other

Services incurred the greatest increase – an increase of 3,800 and 3,200 jobs

respectively.

The number of employed persons decreased in eleven industries over this period.

The five largest reductions were recorded in the Transport, Postal & Warehousing

(-3,100 jobs), Construction (-2,500 jobs), Administrative & Support Services (-

2,300 jobs), Agriculture, Forestry & Fishing (-1,300 jobs) and Mining (-1,300

jobs) industries.

With the exception of manufacturing, four of the top five growth industries are

service denominated. This emulates the transition apparent throughout Australia’s

broader economy, which has seen service or ‘experience’ based employment

increase at the expense of traditional industries (such as manufacturing and

construction).

Wilton Junction – Housing & Employment Needs

24

WJLGOuter South West Sydney - Business Growth

Over the two years to June 2011, an additional 620 employing businesses were

formed within OSWSR.

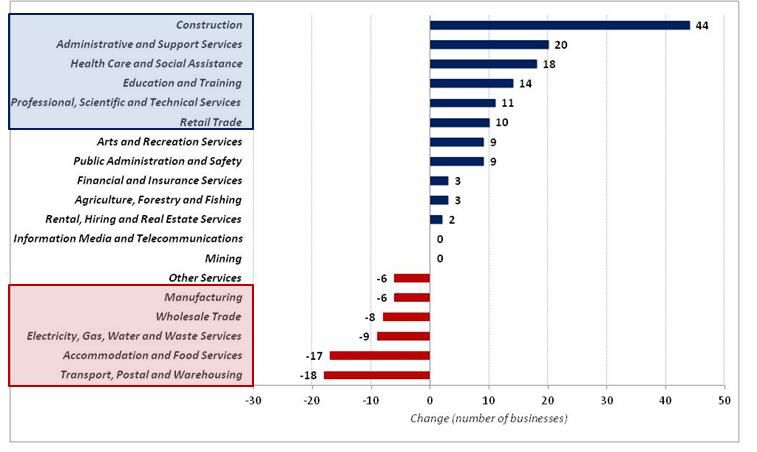

Figure 5. Change in Employing Businesses, June 2009 – June 2011

Source: 8165.0 Counts of Australian Businesses (2012), MacroPlan Dimasi

Of all sectors, business growth had been most pronounced in the manufacturing

(+328 businesses), wholesale trade (+179 businesses) and the construction

(+166 businesses) industries. In contrast, accommodation & food services (-58

businesses), retail trade (-33 businesses) and financial & insurance services (-25

businesses) incurred the largest reduction in business numbers.

Some business growth observations are clearly contrary to the broader OSWSR

employment trends and highlight the peculiarities of employment tendencies and

location distinctions.

The rise in manufacturing, wholesale trade and construction denominated

business registrations parallels a broader trend of industry movement from inner

and middle ring Sydney to western Sydney, generated by a combination of

cheaper rents, the availability of newer custom-built premises and improved

access to Sydney’s orbital road system.

25Although less in absolute magnitude, there has also been a universal rise in

service-based businesses – administrative & support services, other services and

education & training.

Wollondilly LGA - Employment by Industry

The highest employing industries in Wollondilly LGA are ‘Mining’ and

‘Manufacturing’, each accounting for around 14% of jobs in the LGA.

The next four largest employing industries are ‘Construction’ (11%), ‘Education &

Training’ (8%), ‘Retail Trade’ (8%) and ‘Health Care & Social Assistance’ (6%).

The high share of workers engaged in the manufacturing and construction

industries is consistent with our observations for OSWSR. A high representation of

mining workers is influenced by the nearby operations of Illawarra Coal.

Table 2. Employment by Industry, Wollondilly LGA (place of work)

Industry %

Mining 14%

Manufacturing 14%

Construction 11%

Education and Training 8%

Retail Trade 8%

Health Care and Social Assistance 6%

Agriculture, Forestry and Fishing 5%

Accommodation and Food Services 5%

Professional, Scientific and Technical Services 5%

Transport, Postal and Warehousing 4%

Public Administration and Safety 4%

Other Services 4%

Wholesale Trade 3%

Electricity, Gas, Water and Waste Services 2%

Administrative and Support Services 2%

Arts and Recreation Services 2%

Rental, Hiring and Real Estate Services 1%

Financial and Insurance Services 1%

Inadequately described 1%

Information Media and Telecommunications 0%

Total 100%

Source: Census 2011, MacroPlan Dimasi

Wilton Junction – Housing & Employment Needs

26

WJLGCensus data suggests that the majority of jobs in Wollondilly LGA are of a

technician or trade capacity (20%). The next largest occupation types in

Wollondilly LGA are clerical & administrative (15%) and professional (14%).

In compositional terms, compared to OSWSR, the Wollondilly LGA has less Sales

Workers (-5%), Professionals (-4%) and Community & Personal Service Workers

(-3%). However, there is a larger share of Technicians & Trade Workers (+6%),

Machinery Operators & Drivers (+4%), Labourers (+2%) and Managers (+2%).

Figure 6. Occupation, Wollondilly LGA (place of work)

Technicians and Trades Workers

7%

7% 20% Machinery Operators and Drivers

Professionals

12% Managers

15% Labourers

12% Clerical and Administrative Workers

Community and Personal Service Workers

13% 13%

Sales Workers

Source: Census 2006, MacroPlan Dimasi

Wollondilly LGA - Business Growth

Over the two year period to June 2011, an additional 44 (employing)

‘Construction’ businesses were formed in Wollondilly LGA. This represented the

fastest growing business sector, with the closest other sector (‘Administrative &

Support Services’) increasing by just 20 businesses.

Other expanding industries include ‘Health Care & Social Assistance’ (+18

businesses), ‘Education & Training’ (+14 businesses) and ‘Professional, Scientific

& Technical Services’ (+11 businesses).

‘Transport, Postal & Warehousing’ registered the largest decline (-18 businesses),

followed closely by ‘Accommodation & Food Services’ (-17 businesses).

27Figure 7. Change in business count, Wollondilly LGA (June 2009 - June 2011)

Source: Census 2011, MacroPlan Dimasi

Not including construction, business growth in the Wollondilly LGA has been

dominated by service and professional related industries e.g. Health Care & Social

Assistance, Education & Training and Retail Trade.

This contrasts with trends observed in the OSWSR, where business growth has

been concentrated amongst traditional industrial business types, a function of the

exodus of industrial/manufacturing activity from inner and middle ring locations.

The difference suggests that the likely mix of businesses operating at Wilton

Junction will differ from that observed in the OSWSR.

Wollondilly’s Labour Surplus

According to Census 2011 data, approximately 72% of Wollondilly’s employed

residents work outside the LGA. Journey to work data indicates that there is a

movement of local workers to established employment locations such as

Campbelltown and Liverpool LGAs. The major work destination places for

Wollondilly’s working residents are presented below.

Wilton Junction – Housing & Employment Needs

28

WJLGAn ‘export’ of Wollondilly’s labour resources is partly a natural consequence of

scale economies for most businesses. Larger populations will tend to be favoured

by businesses, rather than small populations. Over time, the gradual growth in

the Wollondilly population will make more and more businesses viable within the

local area. At this point, the employment structure is a ‘work in progress’ relative

to other established regions.

Table 3. Work Destination for Employed Residents, Wollondilly LGA (2011)

Work Destination LGA Number Proportion

Wollondilly (A) 5,657 28%

Campbelltown (C) 2,518 12%

Camden (A) 2,515 12%

Liverpool (C) 1,131 6%

POW No Fixed Address (NSW) 1,081 5%

POW State/Territory undefined (NSW) 901 4%

Wingecarribee (A) 868 4%

Penrith (C) 787 4%

Sydney (C) 626 3%

Blacktown (C) 540 3%

POW Capital city undefined (Greater Sydney) 491 2%

Fairfield (C) 450 2%

Wollongong (C) 413 2%

Bankstown (C) 360 2%

Parramatta (C) 322 2%

Holroyd (C) 203 1%

Auburn (C) 170 1%

Sutherland Shire (A) 148 1%

Botany Bay (C) 146 1%

The Hills Shire (A) 116 1%

Source: Census 2011

By industry, the largest areas of labour ‘export’ (i.e. leaving the area to work

elsewhere) relate to the ‘Financial & Insurance Services’ sector (85%), ‘Public

Administration & Safety’ (85%) and ‘Information, Media & Telecommunications’

(83%). Consistent with industry composition, the ‘export’ of white collar labour is

greater than for that for blue collar occupations.

Overall, Wollondilly LGA’s job-containment rate is at 28% (i.e. the proportion of

local jobs held by local workers to the total number of local working residents).

29Table 4. Major Labour ‘Exporting’ Employing Industries – from Wollondilly LGA to other locations (2011)

Proportion

Employing Industry

Financial and Insurance Services 85%

Public Administration and Safety 85%

Information Media and Telecommunications 83%

Health Care and Social Assistance 83%

Wholesale Trade 80%

Electricity, Gas, Water and Waste Services 76%

Transport, Postal and Warehousing 76%

Education and Training 75%

Occupation

White Collar Industries 74%

Blue Collar Industries 70%

Source: Census 2011

Notwithstanding other factors (e.g. income disparity, travel time, job loyalty etc),

the lack of labour demand in Wollondilly LGA is most likely due to its limited

number of medium-large sized businesses. According to the ABS1, approximately

74% of employing businesses operating in Wollondilly LGA engage less than four

workers. While this may currently be deemed a shortfall or weakness of the

Wollondilly LGA, an available labour supply presents as an attractive proposition

for new businesses and industries seeking to enter the area.

We note also that with the advent of a 35,000 township at Wilton Junction,

representing almost a doubling of the LGA’s population, the employment

characteristics of the LGA will be significantly altered.

1.3 Employment Projections

We have estimated the generation of between 10,400 and 11,770 jobs arising

from the development of Wilton Junction, based on expected employment

outcomes for industries that are population driven (i.e. retail and other service-

based sectors) and those which operate to service broader external markets.

1

8165.0 Count of Australian Businesses, including Entries and Exits (2012)

Wilton Junction – Housing & Employment Needs

30

WJLGOf the 12,000-13,200 working residents that a township of 35,000 people will

generate (i.e. excluding retirees and younger age cohorts and applying typical

participation rates), approximately 70% are anticipated to be employed in Wilton

Junction – including 1,566-1,766 ‘home-based’ jobs or jobs not undertaken at a

fixed location.

Table 5. Population and Jobs In Wilton Junction (2041)

Count

Total Residents 34,955

Employed Residents 12,000-13,200

Jobs in Wilton Junction 10,440-11,770

Employed residents working in WJ 8,400-9,240

- Work from home & not fixed 1,566-1,766

- Work in designated EL 6,834-7,474

Source: MacroPlan Dimasi

Job Containment Analysis

Job containment refers to the proportion of working residents who are employed

within their LGA to the total number of local working residents. Wollondilly’s job-

containment rate is 28% (i.e. almost 6,000 of the 21,300 working residents in

Wollondilly work within the LGA). This is a similar rate to that experienced in the

outer-Sydney metropolitan LGAs of Blacktown (27%), Liverpool (28%),

Campbelltown (33%) and Camden (28%).

Employment self-sufficiency, on the other hand, refers to the proportion of

working residents who are employed within their LGA to the total number of local

jobs. Wollondilly has an employment self-sufficiency rate of 61% (i.e. of the

almost 10,000 local jobs, approximately 6,000 of them are filled by local

residents).

In employment self-sufficiency terms, Wollondilly is different to and outperforms

the outer-Sydney metropolitan LGAs of Blacktown (44%), Liverpool (38%),

Campbelltown (52%) and Camden (48%), reflecting the distinct ‘stand-alone’

character of the LGA. In this sense we do not envisage future Wollondilly, with the

advent of a 35,000-strong town at Wilton Junction, as contiguous to the Sydney

south-west metropolitan area. Instead, we consider Wilton Junction as a distinct

31and primary township within the LGA, able to support its own employment and

service needs and to trade beyond its local borders.

To test our applied job containment rate we have considered job containment

achievements at other like locations including the Southern Highlands (NSW),

Beaudesert (QLD) and Murray Bridge (SA). We have chosen these exemplar

regions given similarities in their township character, major highway location and

positioning relative to major centres.

2011 Census data shows that, of total employed residents across the Southern

Highlands region, approximately 8,470 were employed locally. The Southern

Highlands therefore achieves an employment self-containment level of 69% (i.e.

the proportion of working residents who are employed within the Wingecarribee

LGA to the total number of local working residents).

Table 6. Southern Highlands - Job Containment, 2011

Local Jobs Held by Employed

Employed Residents

Bowral 3,848 4,888

Mittagong 2,158 3,441

Moss Vale-Berrima 2,465 3,952

Southern Highlands 8,471 12,281

Job Containment for Southern Highlands 69%

Source: Census 2011

Achieved containment rates for Beaudesert and Murray Bridge are listed below.

Table 7. Exemplar Regions - Job Containment, 2011

Local Jobs Held by

Employed Job-

Employed

Residents containment

Residents

Beaudesert 3,063 5,156 59%

Murray Bridge 5,677 8,190 69%

Source: Census 2011

Wilton Junction – Housing & Employment Needs

32

WJLGThe job containment rates in the like locations that we have examined are not

materially different to the rate that we have applied for our Wilton Junction

employment projections (i.e. 70%).

Again we note the high level of employment self-sufficiency achieved already at

Wollondilly and are confident that as more jobs are created in the LGA (i.e. in

tandem with the development of Wilton Junction) a good proportion of these will

be filled by local residents.

What has held back Wollondilly’s job containment achievement thus far is simply

a lack of jobs which is not assisted by the predominance of small towns of less

than 5,000 persons throughout the LGA. The advent of a 35,000-strong town at

Wilton Junction will change the employment dynamics of the LGA, boosting

service-based employment significantly and providing good reason for external

industries to consider the locational benefits of the area.

We note further that the predicted rate of containment for Wilton Junction will

increase the overall LGA’s containment rate, but not to the same extent.

Work from Home Potential

According to Census 2011 data, approximately 1,093 or 5.1% of Wollondilly’s

employed persons nominated that they worked from home. Given that the specific

Census question asked to state the method of travel, if any, used to get to work

on a specific day, significant weighting cannot be placed on this finding.

The ABS Locations of Work (2008) publication suggests a slighter higher work

from home rate. It indicates that approximately 7% of persons in the Outer South

West Sydney region worked mainly at home. In estimating a likely work-from-

home outcome for Wilton Junction as at 2041 we need to consider advances in

technology and workplace practices that may facilitate higher rates of tele-

working.

We note, for instance, that Wilton Junction intends to provide access to the NBN

high-speed internet fibre optic (already located at the nearby Jarvisfield

residential estate).

33The ‘Impacts of Teleworking under the NBN (2010)’ report by Access Economics

suggests that improved technologies to be provided under the NBN rollout will act

as a further catalyst for tele-working. The Australian Government’s Department of

Broadband, Communication and the Digital Economy has set a target of 12% by

2020 but also acknowledges the potential regionalisation of businesses that could

be encouraged by the NBN provision. Accordingly, we believe that a work from

home outcome of around 10% is plausible for Wilton Junction (by 2041).

Furthermore, an additional 4-5% of working residents are expected to be engaged

in occupations that are not based at a fixed premises e.g. consultants,

salespersons and some trade orientated occupations. Bureau of Transport

Statistics (2012) data prescribes a rate of 4-5% for New South Wales.

Therefore, at an employment outcome of 10,440 to 11,770 jobs for Wilton

Junction, we estimate that between 1,566 and 1,766 (or 15%) of these jobs will

be carried out from home and non-traditional employment lands.

Alternate Projection Approaches

We note from our research that other approaches have been used to project the

employment outcomes of new development areas. A common method is to apply

a top-down/bottom up estimate that seeks to match projections based on likely

industry profiles.

Another method is to separate population-based industries from those that are

dependent on external or other trade, and to nominate the potential for the latter

by identifying market gaps or industries that match the available skill sets of the

local population.

There are misgivings with either of these approaches, given the ‘market’ basis of

industry’s locational decisions, i.e. which would normally involve a trade-off

between the cost of land and the cost of being located outside an established

employment zone (e.g. transport and other costs).

Our approach has been to develop an evidence-based consideration of prevailing

regional employment trends and expected demographic characteristics of the

Wilton Junction – Housing & Employment Needs

34

WJLGarea, and to assess other locations and the specific employment attributes of the

study area.

Further, to test the derived projections we consider the likely employment

capacities of the various service-based or population-driven industries that will

support Wilton Junction’s population base and step through a staged delivery of

the development to identify particular employment needs at particular points in

time.

Finally, a likely composition of external and other industry potential has been

generated for Wilton Junction, considering the relative ‘locational’ merits

presented at Wilton Junction.

1.4 Future Industry Composition

Based on our local and regional observations we project that a majority

component of the estimated 10,440-11,700 jobs for Wilton junction will be

population based. In this section of the report we ground-proof this projection by

examining in detail the employment capacities of the various industries that make

up this employment component.

At the completion of Wilton Junction, the population of Wollondilly LGA is set to

nearly double, significantly changing the business and employment character of

the area.

We anticipate employment generated at the township to be anchored

predominantly by the specific needs of its incoming residents (i.e. service-based

retail, health, professional services and education/training). Additionally, new

businesses will be attracted to the area for its specific trade and locational

benefits, allowing those businesses to trade externally.

We recognise the potential for Wilton Junction to operate as a freight and logistics

hub, given its geographical and locational advantages in serving southern Sydney,

the Illawarra, the Southern Highlands and Canberra. However there is a lack of

clarity pertaining to policy and infrastructure direction regarding this potential.

35Also, given the development of an intermodal facility at Moorebank and the

abundance of existing and planned employment land in south west Sydney, our

employment forecasts for Wilton Junction are not tied to its development as a

freight and logistics centre. Notwithstanding, Wilton Junction’s transport

connections and regional access will undoubtedly attract businesses that can

benefit from these features.

There is a divergence in business growth which sets the Wollondilly LGA apart

from south-west Sydney. Business and employment growth has been most

pronounced in service-based industries. In contrast, manufacturing and industrial-

based businesses are more prominent in the Outer South West Sydney region,

assisted by significant infrastructure development and employment land zonings.

We examine the likely employment capacities of the various employment sectors

that are expected to locate at Wilton Junction in the following sections of this

report.

Town Centre – Retail & Commercial

The main role and function of the Wilton Junction town centre will be to provide

local supporting commercial services that are complementary to the retail

floorspace. Recreation, community facilities, medical centres, short-term

accommodation, allied health, entertainment uses such as taverns and local

professional suites are expected to locate at the Wilton Junction Town Centre.

Supporting commercial office tenants that may locate within the town centre

include lawyers, accountants, regional businesses, commercial banks (branch),

administration, architecture/design firms, financial planners and arts/creative

industries. We would also expect that early offerings at the town centre would

allow business incubation and business life-cycle evolution.

Estimates of the employment capacities and commentary on the delivery

mechanics of retail and related services is provided in the Section 2 of this report.

In all, retail and related services are expected to generate approximately between

2,000 jobs at Wilton Junction across 70,000m2 of retail provision.

Wilton Junction – Housing & Employment Needs

36

WJLGHealth Care & Social Assistance

The health services sector is projected to be one of the fastest growing sectors in

the Australian economy over the next 10 years. There will be above average per

capita demand for medical centres and allied health professionals at Wilton

Junction, given the likely demographic composition – which will be skewed

towards young families and a higher than average portion of persons aged above

65 years.

Co-located health and medical facilities (including allied health) provision will be

required to ensure that localised demand is sufficiently serviced. In addition, the

possibility (and suitability) of a specialised aged care offering will also amplify the

number of health care professionals in Wilton Junction.

It is envisaged that a large medical and allied health service offering will be

required at Wilton Junction. With the exception of trauma related and other major

health procedures, the medical centre should be capable of undertaking routine

medical procedures. Looking forward, consideration can also be given to the

potential for a small private hospital or day surgery to be situated within the

Wollondilly LGA.

High participation rates amongst young working adults, 3,000+ children (aged

between 0-4 years) and 4,000-odd 65+ year olds are expected to underscore

additions to child care and senior service provision in Wollondilly LGA.

At present, there are 18 childcare centres operating in Wollondilly LGA which, in

total, employ 148 workers2. While some demand arising from Wilton Junction may

be serviced by existing centres, there will be a need for additional services.

An extensive suite of senior programs, courses and services are delivered

throughout the Wollondilly area by Council and major religious affiliations (such as

the Anglican, Presbyterian and Uniting Church). While the current offer is

extensive, the rise in 65+ persons from development at Wilton Junction will

increase demand for a more frequent and broader service provision.

2

According to Census 2011, there were 148 Child Care Service workers in

Wollondilly LGA.

37To gauge the potential employment of health care and social assistance at Wilton

Junction we rely upon the relationship between the population change and

employment across all NSW LGAs. As demand for health care and social

assistance is driven mainly by a portion of the total population, viz., children aged

10 and under, women of children bearing age (25-34 years) and the elderly

(65+), we adjust the state based average to reflect real population conditions at

the new township. The relevant age cohorts comprise approximately 36% of total

population at Wilton Junction.

The derived ratio range suggests that for every increment to population in the

selected age cohorts, an additional 0.10-0.12 jobs are expected to be formed. At

Wilton Junction therefore, an estimated 1,200-1,400 health care and social

assistance jobs are projected.

Education & Training

The Masterplan includes provision for five schools to be in operation by 2031. In

terms of sequencing, two schools are to be in operation by 2016 with a third

under construction. The following five year period to 2021 will see the completion

of the third school and the addition of a fourth. The fifth school is anticipated to

be operational by 2031. In addition to primary and secondary schools, there will

also be demand for career development and skills training programmes and

courses. Demand for this provision will come mainly from persons aged 19-22

years.

Overall, by completion, it is anticipated that there will be approximately 10,200

people between 5 and 22 years of age engaged in some form of educational

training at Wilton Junction.

Staff-to-child ratios provided by the ABS3 show that across all education

provisions there is approximately one teacher to every 14 or 15 students.

Allowing for professional and skills-based development courses, a teacher-to-

student ratio of between 13 and 14 has been implied for Wilton Junction. The

employment outcome is shown below.

3

Catalogue Number 4221.0 – Schools, Australia, 2012

Wilton Junction – Housing & Employment Needs

38

WJLGTable 8. Education and Training Employment – Wilton Junction 2041

Age cohort Anticipated Population Staff to Teacher Ratio Total Jobs Created

5-24 11,140 14 750-800

Source: ABS, MacroPlan Dimasi

An employment potential of 750-800 jobs is generated. We note, however that

the development of a University or TAFE would yield a significantly larger

employment outcome.

Public Administration & Safety

To quantify the potential employment from Public Administration & Safety at

Wilton Junction we again rely on the relationship between population change and

employment across all NSW LGAs.

The observed relationship between population change and change in employment

indicates an average ratio range of 0.025-0.03 across NSW LGAs for employment

growth in the public administration and safety sector. Accordingly, between 875

(i.e. 0.025 x 34,955 residents) and 1,050 jobs (i.e. 0.03 x 34,955 residents) are

expected to be generated in this sector arising from the development of Wilton

Junction, across the Wollondilly LGA.

We note, at this stage, there has been no specific indication that any government

departments will move to Wilton Junction or that Council’s chambers will be

relocated to the new township.

Rather, our employment forecast demonstrates the average additional number of

jobs generated in this sector from population growth. Some of the expected

increase in employment demand will be absorbed by the established towns of

Wollondilly. Other new employment opportunities will ensue. As such, an

employment outcome of between 600-680 jobs is expected for this industry at

Wilton Junction.

Arts & Recreation Services

The arts and recreational service industry is a population driven industry that will

directly benefit from population growth at Wilton Junction. Aggregate LGA data for

39NSW shows an average relationship between population and employment change

in the range of 0.01-0.012.

We envisage that arts and recreation services will not be required by all Wilton

Junction residents. Assuming an average penetration rate of 40% and 50% (of

total population), between 140-200 jobs are expected to be generated within this

industry.

Other Services

The ‘Other Services’ sector is also a population driven service industry. It includes

repair and maintenance jobs (automotive and machinery), personal and other

services and the employment of persons by private households.

An employment formation ratio of between 0.012-0.015 jobs per additional

person is ascertained from our state-wide analysis. Including trade captured from

Hume Highway patronage and from other parts of Wollondilly LGA, we estimate

an additional 600-780 jobs related to this sector in direct association with the

development of Wilton Junction.

Electricity, Gas, Water and Waste Service

The electricity, gas, water and waste service industry is also related to population.

Employment generation is expected to occur during the initial phase of

development of Wilton Junction.

External or Other Industries

For industries that mainly service external markets (i.e. those that are not

predominantly population driven), ‘locational’ attributes and comparative

advantage present as the two main considerations for business formation.

Industries that service mainly external markets include ‘Transport, Postal &

Warehousing’, ‘Manufacturing’ and ‘Warehouse Trade’.

In order to derive an employment outcome for Wilton Junction for these types of

industries, we firstly consider an employment exemplar - Somersby, located at

the Central Coast (NSW). Somersby has similar attributes to Wilton Junction. It is

located a similar distance from Sydney and is adjacent to a major highway (the

F3). It hosts a range of industrial and business enterprises in a business park type

Wilton Junction – Housing & Employment Needs

40

WJLGYou can also read