U.S. Wealth Market Outlook - Q3 2021 - BlackRock

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

U.S. Wealth

Market Outlook

Q3 2021

USWAM0821U/S-1755111-1/23

U.S. Wealth Market Outlook

Our views for 2021

What we’re closely watching:

1 2 3

The economic restart The low rate problem The globe, rewired

USWAM0821U/S-1755111-2/23

THE ECONOMIC RESTART

Back on track?

1 Economic activity has accelerated sharply – in contrast to prolonged weakness following the

global financial crisis. But strong growth is unlikely to be sustained once the restart completes.

U.S. GDP growth trend after the Covid shock and global financial crisis

10

n U.S. GDP and consensus median

n Pre-GFC five-year growth trend

n Range of growth trend assumptions

n GDP consensus range

9.9

Real GDP (log units)

9.8

9.7

9.6

2007 2009 2011 2013 2015 2017 2019 2021

Forward looking estimates may not come to pass. Sources: BlackRock Investment Institute and Reuters News, with data from Haver Analytics, July 2021. Notes: The pink line represents the extrapolation of

the five-year growth trend preceding the global financial crisis (GFC). The yellow area represents a range of consensus assumptions for trend growth following the Covidshock. The orange line represents

actual U.S. GDP up to the first quarter of 2021 and the median forecast from the second quarter of 2021 to the last quarter of 2022, based on the latest Reuters poll as of June 10, 2021. We plot the log of

GDP so that the slope of the line indicates the trend growth rate.

USWAM0821U/S-1755111-3/23

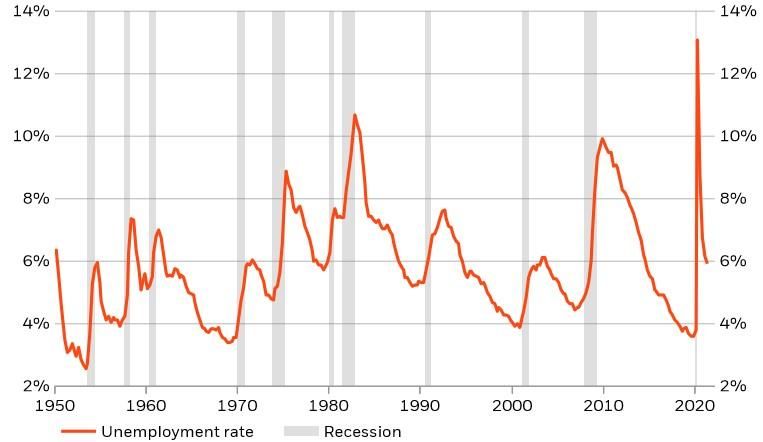

THE ECONOMIC RESTART

Not a typical business cycle

1 The essence of the “restart” is that it does not follow the pattern of a typical economic cycle.

According to traditional measures, the Covid-19 induced “recession” only lasted a few months.

U.S. unemployment rate and recessions

Source: Refinitiv Datastream, BlackRock Investment Institute, as of July 21, 2021

USWAM0821U/S-1755111-4/23

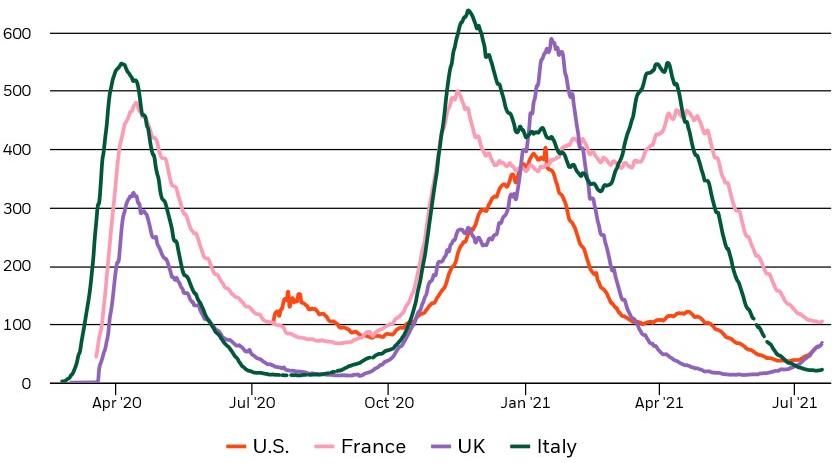

THE ECONOMIC RESTART

Virus dynamics

1 While new case data can be influenced by a myriad of factors, looking at positive test rates or

hospitalization data can give a better picture of the impact of the virus through time.

Hospitalization levels per million

Sources: The COVID tracking project, ECDC, UK government.

Notes: Due to different definition/measurement data levels may not be comparable across countries.

USWAM0821U/S-1755111-5/23

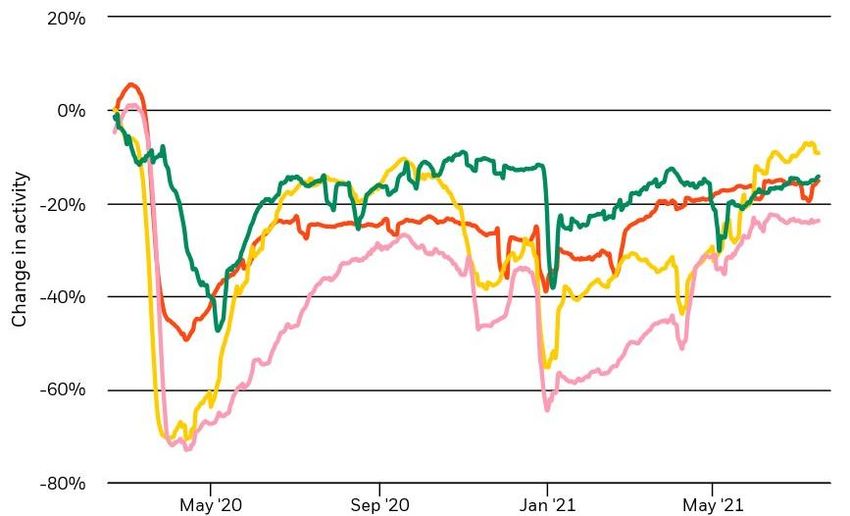

THE ECONOMIC RESTART

Cutting out the noise

1 Early in the pandemic, mobility data may have been a better predictor of economic activity than

lockdown mandates, or even virus cases.

Location based Google data showing the difference in activity from pre-virus baseline

Sources: BlackRock Investment Institute, with data from Google.

Notes: Google location data based on the average of the retail and recreation, workplace and transit categories, 7-day rolling average. Euro area based on average of Germany, France and Italy.

USWAM0821U/S-1755111-6/23

THE LOW RATE PROBLEM

Historically low bond returns

2 With interest rates at historic lows, expect low bond returns for the foreseeable future.

Bond returns mirror interest rates at the start of a decade

Average annual 10-year bond returns since 1930

Represents return decade-to-date (1/1/10 to 12/31/20). Morningstar and U.S. Treasury as of 12/31/20. U.S. Bonds are represented by the BbgBarc U.S. Aggregate Bond Index from 1/3/89 to

12/31/20 and the IA SBBI U.S. IT Bond Index from 1/1/26 to 1/3/89.

Past performance does not guarantee or indicate future results.Index performance is for illustrative purposes only. You cannot invest directly in the index.

USWAM0821U/S-1755111-7/23THE LOW RATE PROBLEM

Loss of a shock absorber

2 During past stock market selloffs, core bonds rallied. But today’s yields are close to zero and

have not much more room to fall.

Can core bonds diversify equities like they used to?

U.S. 10-Year Treasury yield changes during recessions

P ast performance does not guarantee future results.

Source: BlackRock, Bloomberg as of 3/31/21. U.S. recession periods are defined by National Bureau of Economic Research. Graph displays U.S. 10-Year Treasury Yield rate changes during recession

periods. 10-Year Treasury change reflects the biggest move seen from as early as six months before the recession period

USWAM0821U/S-1755111-8/23THE LOW RATE PROBLEM

Inflation can spell negative returns

2 Unlike in previous inflationary periods, interest and savings rates may not keep up

Inflation versus interest and savings rates Largest gap between interest rates and inflation

today since 1980

As of 5/31/21 10-year U.S. Treasury yield minus inflation (CPI), as of 5/31/21

5.0% 12

10

8

6

4

2

1.6% 0

-2

0.1% -4

-6

Jun-64

Jun-67

Jun-79

Jun-82

Jun-85

Jun-00

Jun-03

Jun-06

Jun-18

Jun-21

Jun-70

Jun-73

Jun-76

Jun-88

Jun-91

Jun-94

Jun-97

Jun-09

Jun-12

Jun-15

Inflation 10-year U.S. 3-month

May-2021 Treasury CD

Source: Bureau of Labor Statistics, as of 5/31/21 and Morningstar.

P ast performance does not guarantee or indicate future results. Index performance is for illustrative purposes only. You cannot invest directly in the index.

USWAM0821U/S-1755111-9/23THE GLOBE, REWIRED

Deglobalizing forces

3 Purchasing manager surveys indicate longer delivery times, partly on shipping capacity

shortages.

PMI supplier delivery index, 2008-2021

Through March 2021

-8

Japan 2011

Supplier delivery times (z-score

Fukushima

-6 Longer delivery

n Global n Euro area times

n U.S. n Japan

-4

inverted)

-2

0

2

4

2008 2010 2012 2014 2016 2018 2020

Sources: BlackRock Investment Institute, Markit, with data from Refinitiv Datastream and Haver Analytics, March 2021. Notes: Chart on the left shows an index of delivery times for items used in the production

process, for manufacturing firms. As delivery times lengthen (for example due to capacity constraints) the level of the index falls (note the Y-axis is inverted). Euro area data is for the whole region.

USWAM0821U/S-1755111-10/23THE GLOBE REWIRED

Opposite poles

3 The world looks increasingly fragmented, with the U.S. and China at opposite poles.

Regional share of global GDP, 1990-2024

60%

50%

Share of global GDP

n North America, Europe and Japan

40%

n Asia ex-Japan

30%

20%

10%

1990 1995 2000 2005 2010 2015 2020 2025

Sources: BlackRock Investment Institute, with data from IMF, Refinitiv, October 2020. Notes: The lines how each region’s combined share of global GDP on a purchasing power parity (PPP) basis. The dotted

lines show the forecast period based on IMF projections to 2024.

USWAM0821U/S-1755111-11/23U.S. Wealth Market Outlook

Our views for 2021

The path forward:

Balancing optimism and realism

USWAM0821U/S-1755111-12/23THE PATH FORWARD

Chase individual stocks at your own risk

Not all stocks are created equal, but there’s strength in numbers.

Individual U.S. stocks U.S. stock mutual funds and ETFs

(last 5 years) (last 5 years)

26% 99.9%

74%

lost

money 0.1%

lost

money

# positive # negative % lost money

U.S. stocks 2698 951 26%

U.S. stock mutual funds 1702 2 0.1%

U.S. stock ETFs 276 0 0%

Source: Morningstar as of 6/30/21. Mutual Funds and ETFs are the Morningstar U.S. Equity Category, oldest share class only. US Individual Stocks are the Morningstar US Stock Universe, all securities on

the NYSE and NASDAQ. Analysis does not include obsolete mutual funds, ETFs or stocks as defined by Morningstar. Performance is historical and does not guarantee or indicate future results.

USWAM0821U/S-1755111-13/23THE PATH FORWARD

Waiting to invest can leave you behind

“Compound interest – the eighth wonder of the world.”

$300,000 Hypothetical growth of $100,000 assuming 10% annual yield

$259,374

$260,000

$220,000

$180,000

$161,051

$140,000

$100,000

0 1 2 3 4 5 6 7 8 9 10

Years

Source: BlackRock For illustrative purposes only.

USWAM0821U/S-1755111-14/23THE PATH FORWARD

It’s time in the market, not timing the

market

Missing top-performing days can hurt your return

Hypothetical $100,000 investment in the S&P 500 Index

over the last 20 years (2001-2020)

$425K Don’t miss out

$381K when markets

$344K snap back

$314K

$287K

$268K 22 of the 25

$195K worst days in the

$147K market were

$155K within one month

$92K

of one of the 25

best days

Stayed 1 2 3 4 5 10 15 20 25

Invested

Missing the top-performing days

Source: BlackRock; Bloomberg as of 12/31/20. Stocks are represented by the S&P 500 Index, an unmanaged index that is generally considered representative of the U.S. stock market. Past performance does not guarantee or indicate future results. It is not

possible to invest directly in an index.

USWAM0821U/S-1755111-15/23THE PATH FORWARD

Get cash off the sidelines

Investors are pouring record assets in money market funds – potentially to their detriment

Money market fund assets 3-year U.S. stock performance following a

Last 15 years (2/1/96 – 1/31/21) peak in money market fund assets

Average annual performance

Jan-21

$5,000 $4.3T

$4,500

Jan-09

$4,000 $3.8T 19.2%

$3,500

16.4%

$3,000

Jan-03

Billions

$2,500 $2.3T

$2,000

$1,500

$1,000

$500

$0

1/31/03 - 1/31/06 1/31/09 - 1/31/12

Source: Morningstar as of 1/31/21. U.S. stocks represented by the S&P 500 Index, an unmanaged index that is generally considered representative of the U.S. stock market. Past performance does not

guarantee or indicate future results. Index performance is for illustrative purposes only. You cannot invest directly in the index.

USWAM0821U/S-1755111-16/23THE PATH FORWARD

Go beyond your borders

Global market leadership comes in waves.

1International stock index returns and U.S. stock index returns, 10-year average annual rolling returns, 11/30/86 –12/31/20 with international stock positive index returns represented as negative.

Source: Morningstar as of 12/31/20. U.S. stock index represented by the IA SBBI U.S. Large stock index and international stocks represented by the MSCI EAFE NR USD index. Past performance does not

guarantee or indicate future results. Index performance is for illustrative purposes only. You cannot invest directly in the index. 2Source: BlackRock as of 03/31/21. US equities represented by the S&P 500

Index. International equities represented by the MSCI ACWI ex USA Index. Historical average data between 1/1/2011-03/31/2021. Past performance is no guarantee of future results.

USWAM0821U/S-1755111-17/23THE PATH FORWARD

Go beyond your borders

Rolling 10-year period outperformance, international vs. U.S.

(10-year rolling periods various, U.S. return levels 1970 — 12/2020)

International

US Returns outperforms +2.4% on avgTHE PATH FORWARD

Today’s leaders may not be tomorrow’s

Don’t unwittingly overweight today’s leaders. Consider strategies that seek tomorrow’s potential innovators.

Technology Health care

S&P 500 Select technology Sector S&P 500 Select health care Sector

Top 3 holdings Top 3 holdings

48% 22%

Microsoft J&J

Apple United Health

Visa Pfizer

The other 70 The other 60

holdings holdings

52% 78%

Source: State Street as of 10/26/2020. Allocations are subject to change. This is not meant as a guarantee of any future result or experience. This information should not be relied upon as research,

investment advice or a recommendation regarding the Funds or any security in particular. Specific companies or issuers are mentioned for educational purposes only and should not be deemed as a

recommendation to buy or sell any securities. Any companies mentioned do not necessarily represent current or future holdings of any BlackRock products.

USWAM0821U/S-1755111-19/23THE PATH FORWARD

Sustainability is the new investment

standard

Companies are disclosing Institutions are Investors are asking about

more ESG information investing in ESG sustainable investing

90%

20%

70% 72%

2011 2019

% of S&P companies of institutional investors of Americans surveyed by

reporting ESG disclosures have implemented ESG Morningstar have expressed

has increased1 strategies2 interest in sustainable investing3

1 Source: 2020 GA Institute Annual S&P 500 Sustainability Reporting Analysis;https://www.ga-institute.com/research-reports/flash-reports/2020-sp-500-flash-report.html.

2 Source: 2018 Morgan Stanley Survey: https://www.morganstanley.com/press-releases/morgan-stanley-survey-finds-sustainable-investing-momentum-high-.

3 Source: Morningstar Are Your Clients ESG Investors?, April 22, 2019.

USWAM0821U/S-1755111-20/23THE PATH FORWARD

Sustainability considers both

traditional and ESG analysis

Consider two companies that have …but different environmental, social,

similar financial characteristics... and governance characteristics.

Company A Company B Company A Company B

Consistent Which one looks Fair CEO

✓ profits?

✓

like a better

✓

Pay? X

✓

long-term Robust

Grows

✓ dividends?

✓ investment ✓ data X

✓

after applying security?

High an ESG lens?

Employee

✓ market

share?

✓ ✓

satisfaction? X

✓

Source: BlackRock. For illustrative purposes only.

USWAM0821U/S-1755111-21/23THE PATH FORWARD

Think beyond the traditional 60/40

portfolio

While stock volatility and valuations are elevated, bonds are less equipped to provide protection.

P ast performance is no guarantee of future results. Equity market data – Source: Morningstar, as of 3/31/21. Stock market represented by the S&P 500 Index. Average annual volatilit y based on standard

deviation. Index performance is for illustrative purposes only. It is not possible to invest in an unmanaged index. Rates dat a – Source: U.S. Dept. of the Treasury as of 3/31/21. Data is since 7/25/12 when

the 10-year Treasury hit a 30 year low point.

USWAM0821U/S-1755111-22/23Important notes

This material is prepared by BlackRock and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation

to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of July 2021 and may change as subsequent conditions vary. The

information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-

inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and

omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents.

Investment involves risks. International investing involves additional risks, including risks related to foreign currency, limited liquidity, less government regulation and the

possibility of substantial volatility due to adverse political, economic or other developments. The two main risks related tofixed income investing are interest rate risk and

credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond

will not be able to make principal and interest payments. Index performance is shown for illustrative purposes only. Commodities’ prices may be highly volatile. Prices may

be affected by various economic, financial, social and political factors, which may be unpredictable and may have a significant impact on the prices of precious metals.

Concentrated investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset

classes and the general securities market. A significant portion of the aggregate world gold holdings is owned by governments, central banks and related institutions. One

or more of these institutions could sell in amounts large enough to cause a decline in world gold prices. Should there be an increase in the level of hedge activity of gold

producing companies, it could cause a decline in world gold prices. Should the speculative community take a negative view towards gold, it could cause a decline in world

gold prices. You cannot invest directly in an index.

©2021 BlackRock. All rights reserved. BlackRock is a trademark of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are

the property of their respective owners.

Prepared by BlackRock Investments, LLC. Member FINRA.

USWAM0821U/S-1755111-23/23You can also read