U.S. Equity Sector Allocation - July 24, 2023 - Baird Wealth

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

U.S. Equity Sector Allocation

July 24, 2023

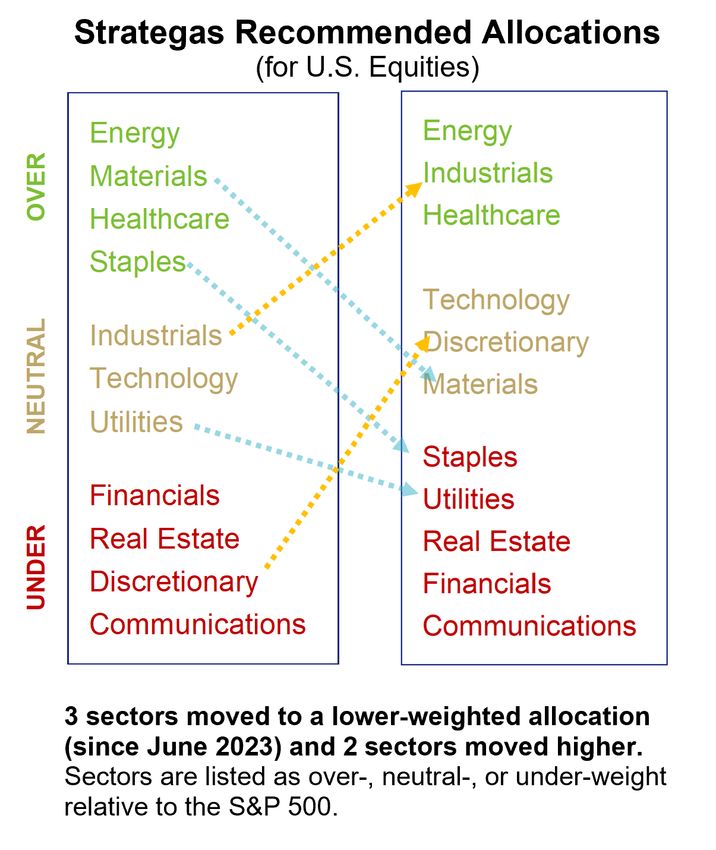

FIVE CHANGES TO OUR SECTOR-WEIGHTING ALLOCATIONS

The stock market is up. Cyclicals appear to have thrown a shoulder behind the rally in the past month and

a half. The market is in a strong patch, as are some segments of the economy. Is it more than that? Can it

last? We continue to harbor doubts. But what is clear is that the temptation to enter (or re-enter) the stock

market has become too great for most investors. Even the economists are less bearish. Last fall, 100% of

economists surveyed by Bloomberg forecast that the U.S. would be in recession within 12 months. Nine

months later, there’s no recession and the surveyed rate has fallen to 58%. To be fair, without the Federal

Reserve backstopping several failing regional banks in March, the U.S. was probably fewer than 48 hours

away from an economic event. Despite a majority of economists still believing a recession is around the

corner, few firms have addressed recession (or higher inflation for that matter) in their outlook for profits. In

fact, the consensus has S&P earnings bottoming in 2Q23—in other words, the earnings that are being

reported now. Investors are behaving as if an earnings recovery is already underway.

We sat down last week with a clean sheet of paper to work

through our views on each of the equity market’s 11

sectors. We made 5 changes to our allocations. Materials,

Staples, and Utilities moved down the weighting scale and

Industrials and Discretionary moved up. Though we

remain doubtful that the current strong patch represents a

durable move higher, the following factors contributed to

our change in allocation: Strength from the cyclicals amid

better-than-feared U.S. economic growth, strength in the

labor market juicing the consumer, manufacturing and

infrastructure spending buoying Industrials, and weakness

in defense stalwarts Staples and Utilities. We go into more

detail o in the table on the following page.

Our allocations are made on the basis of a time horizon of

at least one year. They don’t necessarily reflect the sectors

that could see success in the shorter term if the market

continues to melt higher (irrespective of valuations,

financial conditions or fundamentals). In addition to

Industrials, we think Discretionary and Technology may be

positioned to benefit from a near-term melt up.

Page 2: A summary or Strategas’ recommended allocation (including rationales and risks)

Page 3: A table of key sector metrics

Page 4: Important disclosures

Robert W. Baird & Co. Incorporated Page 1 of 4

Strategas Sector Allocation – Technology – July 24, 2023

Strategas U.S. Recommended Sector Allocation Summary

Rationale Risks

Activity is reaccelerating in some pockets of the economy.

Cost growth in many segments remains higher than

Covid-related supply chain pressures have abated and

nominal activity levels. Elevated risk of a U.S. recession

Industrials weaker US dollar is contributing to improvement in

and the historically low probability the Fed can engineer

fundamentals. New orders may improve in coming months.

Overweight

a soft landing are risks.

Diversity of constituent businesses is a plus

Global recession could disrupt near-term demand. A

Strict stewardship of capital. We view sector as under- breakdown in OPEC+ agreements could stress energy

capitalized. Capex growth rising. Equipment & Services markets. Russia production does not seem affected by

Energy showing resilience. Higher crude prices providing free cash sanctions. Not immune to wage inflation. Concentration

flow generation. risk due to weighting of Exxon and Chevron in the

sector.

Defensive attributes. The sector is in good shape with ACA Would lag in the event of a cyclical upswing. Congress

growth of 35% over the past two years. Congress failed to fix the R&D tax credit as part of the omnibus

Healthcare prevented $750 billion in Medicare cuts going into effect in spending bill. Companies have to amortize expenses

2023. Higher taxes appear unlikely. over 5 years which eats into cash flow.

We anticipate cooling performance after advance off

Concentration remains a risk as AAPL and MSFT make

October lows. AI emerging as a durable long-term target

up nearly half of the sector's market capitalization.

Technology for capex and investment capital. Sector bellwethers are no

Traditionally, Growth struggles in times of high interest

longer the Growth darlings of the past. Consistent

rates and elevated inflation.

weakness in USD will pad fundamentals.

Neutral

Sector is heavily influenced by Amazon and Tesla. A

Wage gains may stick, and with inflation rolling over, may

recession would hamper consumer-spending habits

boost consumer confidence. Avoiding a severe recession

Discretionary could lead to a cyclical bid. Homebuilders have been

and likely result in more restrained activity through

avoiding (or further delaying) a recession could lead to a

strong. Rising rates have been a tailwind for savers.

protracted cyclical bid in the market.

Sector is undercapitalized. Sustained weakness in the U.S. A recession would hamper economic activity. A

dollar is a tailwind (foreign sales). As long as electric vehicle strengthening U.S. dollar would hurt global revenue.

Materials trends remain, commodity prices should benefit from China may not be a panacea should activity pick up as

elevated demand. At secular lows relative to stocks. economy reorients toward domestic consumption.

Sector under pressure from tighter financial conditions

Capital market activity may show some signs of life in

globally and the potential for higher capital requirements

2H23. The banking crisis is contained, and the banks

Financials and regulation. Credit availability is slowing. If not for Fed

recover quickly, leading to outperformance. Bank

intervention, banking crisis would likely have led to

valuations are an attractive entry point.

recession. EPS estimates have further to fall.

Legacy Telecom likely to be a drag (debt + lawsuits). META Durable outperformance from META and GOOGL

and GOOGL are heavyweights. Pressure from higher would buoy sector. Use-case for AI could be realized

Underweight

Communications interest rates and deteriorating economic environment more quickly than expected. Structural trend of digital

could impact ad spending. content and advertising to continue.

Sector tends to underperform in rising rate environment. Hedge against recession risk. Sector retains pricing

With interest rates now above the sector's dividend yield, power as inflation moderates. Record of outperforming

Staples income-seeking investors have an alternative to stocks. in early stages of a slowdown. Consumers still rely on

Difficult to expand margins as inflation starts to moderate. these goods regardless of economic backdrop.

Yield competition is impacting the shares. The sector's

A recession could give a bid to the sector. A sharp

dividend yield is facing competition from bonds. Sector

Utilities faces fundamental struggles like volatile natural gas prices

decline in yields could enhance the yield-attractiveness

of the sector.

and rising leverage.

A fall in yields could make interest and dividend income

Ambiguity re: commercial real estate valuations and broad

from Real Estate attractive. Cloud infrastructure needs

sector underperformance. Return to office jagged and

Real Estate commercial property valuations impacted. Similarly poor

to be built and housed. Elevated mortgage rates could

be a tailwind for apartment REITs. Sentiment is

long-term trends in global real estate.

extremely negative.

Robert W. Baird & Co. Incorporated Page 2 of 4Strategas Sector Allocation – Technology – July 24, 2023

SECTOR METRICS

Metric TECH HC CD COMM FIN IND CS UTL RE MAT ENE

S&P Sector Weight 28.1% 13.5% 10.5% 8.2% 12.7% 8.5% 6.7% 2.6% 2.5% 2.5% 4.2%

2-Year Beta Rel. S&P 500 1.26 0.66 1.31 1.06 0.97 0.92 0.60 0.62 0.96 0.97 0.67

Foreign Revenue Exposure 58.9% 36.3% 34.7% 43.0% 21.4% 32.5% 44.0% 1.9% 16.0% 55.1% 38.2%

2023 EPS Growth 1.2% -12.7% 26.8% 17.5% 9.4% 14.5% 2.6% 6.6% 1.0% -19.6% -31.1%

2023 Sales Growth 1.4% 4.2% 6.5% 3.4% 8.2% 4.1% 3.9% 2.9% 5.7% -5.7% -16.1%

NTM P/E 27.6x 17.9x 26.6x 17.0x 14.0x 19.0x 20.2x 17.7x 17.4x 18.1x 11.6x

TTM P/E 36.8x 21.3x 37.2x 22.8x 18.1x 22.2x 24.9x 23.1x 35.0x 16.0x 7.2x

EV/EBITDA 23.7x 14.3x 17.3x 11.3x 19.0x 14.9x 16.2x 13.8x 20.8x 10.5x 5.1x

P/Sales 7.1x 1.8x 2.2x 2.9x 2.4x 2.1x 1.4x 2.3x 6.6x 1.9x 1.1x

P/Book 10.9x 4.8x 9.8x 3.5x 1.8x 5.6x 6.4x 2.1x 3.0x 2.9x 2.2x

Cash as % of Debt 65.5% 34.9% 33.8% 29.6% 63.2% 26.6% 17.8% 2.6% 6.0% 23.9% 33.6%

Debt as % of Total Assets 26.2% 30.5% 38.7% 29.5% 18.7% 32.4% 32.2% 42.3% 44.5% 28.1% 21.1%

Debt as % of Equity 63.4% 83.4% 182.4% 76.5% 40.6% 125.3% 112.3% 162.3% 107.7% 67.1% 43.6%

EBIT/Interest Expense 17.1 11.2 7.3 7.1 10.7 7.3 10.4 2.5 3.1 9.8 21.4

Dividend Yield 0.8% 1.6% 0.9% 0.8% 1.8% 1.5% 2.5% 3.1% 3.1% 2.0% 3.7%

% of Stocks Above 200-Day 89.2% 65.6% 81.1% 69.6% 58.3% 86.7% 59.5% 66.7% 71.0% 55.2% 65.2%

Rolling 6-Month % Change 36.2% 1.7% 23.8% 21.9% -0.3% 10.6% 4.4% -1.2% -1.9% 1.0% -7.2%

1-Month SPDR Sector Flows ($Mil) $7.7 -$663.2 -$365.1 $838.0 $1,265.8 $663.9 -$233.6 -$371.9 $133.3 $451.7 -$131

1-Mo. Flows % of Total SPDR

0.5% -41.6% -22.9% 52.5% 79.3% 41.6% -14.6% -23.3% 8.4% 28.3% -8.2%

Flows

12-Month Average of 1-Mo. Flows -$121.0 $180.1 $47.9 $172.7 $42.7 -$69.1 $133.6 $77.2 -$21.5 -$98.3 -$455.3

Data source: FactSet

Robert W. Baird & Co. Incorporated Page 3 of 4Strategas Sector Allocation – Technology – July 24, 2023 IMPORTANT DISCLOSURES Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index. Allocations are labeled as over-, under-, and neutral weight compared to sector weightings in the S&P 500, an index of the largest U.S. publicly traded companies. The S&P 500 is market-cap weighted, giving larger companies greater influence on sector weights. The weightings in the index can float from day to day as normal trading causes shares within the index to rise or fall in price. It is not possible to invest directly in an index. This communication was prepared by Strategas Securities, LLC (“we” or “us”). Recipients of this communication may not distribute it to others without our express prior consent. This communication is provided for informational purposes only and is not an offer, recommendation, or solicitation to buy or sell any security. This communication does not constitute, nor should it be regarded as, investment research or a research report or securities recommendation and it does not provide information reasonably sufficient upon which to base an investment decision. This is not a complete analysis of every material fact regarding any company, industry, or security. Additional analysis would be required to make an investment decision. This communication is not based on the investment objectives, strategies, goals, financial circumstances, needs or risk tolerance of any particular client and is not presented as suitable to any other particular client; therefore, this communication should be treated as impersonal investment advice. The intended recipients of this communication are presumed to be capable of conducting their own analysis, risk evaluation, and decision-making regarding their investments. For investors subject to MiFID II (European Directive 2014/65/EU and related Delegated Directives): We classify the intended recipients of this communication as “professional clients” or “eligible counterparties” with the meaning of MiFID II and the rules of the UK Financial Conduct Authority. The contents of this report are not provided on an independent basis and are not “investment advice” or “personal recommendations” within the meaning of MiFID II and the rules of the UK Financial Conduct Authority. The information in this communication has been obtained from sources we consider to be reliable, but we cannot guarantee its accuracy. The information is current only as of the date of this communication and we do not undertake to update or revise such information following such date. To the extent that any securities or their issuers are included in this communication, we do not undertake to provide any information about such securities or their issuers in the future. We do not follow, cover or provide any fundamental or technical analyses, investment ratings, price targets, financial models or other guidance on any particular securities or companies. Further, to the extent that any securities or their issuers are included in this communication, each person responsible for the content included in this communication certifies that any views expressed with respect to such securities or their issuers accurately reflect his or her personal views about the same and that no part of his or her compensation was, is, or will be directly or indirectly related to the specific recommendations or views contained in this communication. This communication is provided on a “where is, as is” basis, and we expressly disclaim any liability for any losses or other consequences of any person’s use of or reliance on the information contained in this communication. Strategas Securities, LLC is a registered broker-dealer and FINRA member firm, as well as an SEC-registered investment adviser. It is affiliated with Strategas Asset Management, LLC, an SEC-registered investment adviser. Strategas Securities, LLC is also affiliated with and wholly owned by Robert W. Baird & Co. Incorporated (“Baird”), a broker-dealer and FINRA member firm, although the two firms conduct separate and distinct businesses. A complete listing of all applicable disclosures pertaining to Baird with respect to any individual companies mentioned in this communication can be accessed at http://www.rwbaird.com/research-insights/research/coverage/thirdpartyresearch- disclosures.aspx. You can also call 1-800-792-2473 or write: Robert W. Baird & Co., PWM Research & Analytics, 777 E. Wisconsin Avenue, Milwaukee, WI 53202. Robert W. Baird & Co. Incorporated Page 4 of 4

You can also read