Melville Douglas Focused Monthly Commentary

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Melville Douglas

Focused

Monthly Commentary

/ February 2021

Valuation concerns resurface

The new year began with a succession of new highs for global

stock markets. The impetus was the Democratic Party’s surprise

wins in the Georgia senatorial run-off elections that enabled

control of the Senate. The Biden Administration now has more

scope to push through heftier fiscal spending programs. The

rollout of COVID vaccination programs across the globe further

Bernard Drotschie

stoked “look-through-the-crisis” confidence. However, as the

/ Chief Investment Officer

month progressed, this initial optimism dissipated on concerns

about more infectious (and potentially vaccine resistant) COVID

viral strains. Not even stronger than expected economic data,

a very strong outcome from the Q4 2020 earnings season or

assurance from Janet Yellen (the newly appointed US Treasury

Secretary) and Federal Reserve Chair Jerome Powell that more

stimulus was on the way to safeguard the economy from “a

longer, more painful recession now – and long-term scarring

of the economy later”, could stem some short term weakness.

With the deployment of vaccines and inoculations gathering

momentum and policy makers steadfast in pulling the global

economy out of the pandemic hole, investors can look forward

to a much stronger growth environment in the second half of

the year, but the reality is that not all asset prices will benefit

equally, as much of the good news is already reflected in many

valuations.

PRICE-TO-EARNINGS (NEXT 12 MONTHS)

US

World

Europe

EM

Japan

Source: FactSet

More fiscal support on the way.

Investors will take comfort from Joe Biden’s inauguration as the 46th president of the United States. With a Democratic

sweep now a reality after the Georgia Senate run off, President Biden has the majority (albeit at a very slim margin)

support in Congress and his new administration is pushing for a further $1.9 trillion fiscal stimulus package (over and

above the $900bn approved in December). Whilst the actual figure and timing remain up for debate, the economy is

set to receive more assistance, albeit to the detriment of rapidly rising debt levels. These amounts are significant even

for a $20trn economy. The funds have been earmarked to support those that have been worst hit by the pandemic and

to rebuild the economy with a focus on infrastructure investment.

The US government’s debt has ballooned to well over 100% of GDP as a result of the crisis and this will at some point

have to be addressed by policy makers, but evidently not in the near term given that the overarching objective is to

first pull the economy out of the claws of the pandemic. The good news for now at least is that the cost of financing the

increased debt for western world countries has become almost insignificant given the historically low interest rates.

Roll over risk (re-financing risk) has become a non-event for governments given that their central banks stand ready to

provide the necessary support. Further out there will have to be higher taxes to reduce debt but again the immediate

focus is to deal with the severe economic effects of COVID-19 rather than halt any lasting recovery before it has begun.

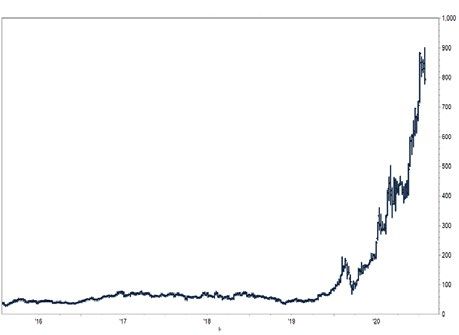

Signs of exuberance surfacing

Focus has rightfully shifted to lofty and in some cases

outright “bubble” like valuations (generally described

as price rises not justified by fundamentals) in certain

sectors such as solar power and electric vehicles; think

Tesla Motors whose share price has increased by a factor

of eight during the past year. The increased involvement

of US retail investors in pushing valuations higher has

also started to raise alarm bells as cheap financing and

easy access to online trading and derivative platforms

has resulted in increasing speculative behaviour,

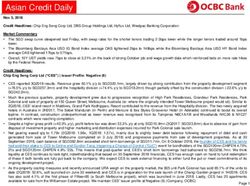

Call option Buys minus Sells by smaller investors,

something which can easily unravel should share

mn contracts (lhs)

prices sharply decline or when (ultimately) liquidity is

Nasdaq, rhs

withdrawn from financial markets.

Source: JPMorgan

Increased involvement of US retail investors in pushing

valuations higher has started to raise alarm bells.

Through various social and trading platforms such as Reddit, ordinary retail

investors have recently been targeting and buying certain small cap stocks

such as GameStop which have been shorted (strategy which allows investors

to profit from lower share prices, but can be very expensive when share prices

increase) by long/short hedge funds. This has resulted in significant losses

for the hedge funds involved as they were forced to “cover” their positions,

by buying back shares at higher prices. Because these strategies are usually

funded with debt, hedge funds have no option but to sell their long positions in

equities to cover realised losses and de-leverage. These events coupled with

profit taking by the retail investors resulted in weakness in equity markets

during the last few trading days of the month.

The example above is not unique in nature but does highlight the potential for

more volatility ahead and, at the same time, serves as a good illustration of

some of the unintended consequences of very cheap money, which instead

of being deployed in the real economy to create employment is finding its

way into short term speculative investment bets. For now, regulators will

most likely intervene to restrict this sort of behaviour by market participants,

before the Federal Reserve is forced to respond with tighter monetary policy

(higher interest rates) to prevent this “bubble-like” behaviour from spreading

more widely.

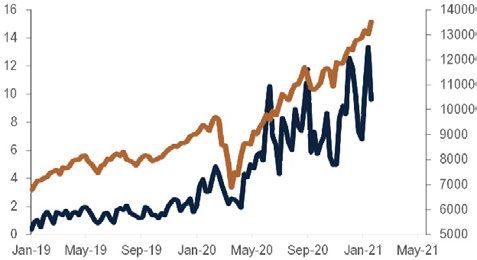

TESLA - SHARE PRICE MSCI EARNINGS YIELD vs US 10Y GOVERNMENT BOND

Tesla’s share price looks extreme. US 10Y Government Bond Yield (lhs)

Source: FactSet MSCI Earnings Yield (rhs)

Positive correlation between equity valuations and the risk-free interest rate.

Source: FactSet

There is no doubt that valuations for risk assets are expensive by historical

standards when viewed in isolation, something we have alluded to previously,

but it is also equally important to understand that this has been a function

of extremely loose monetary policy and a much-improved growth outlook as

the global vaccination program and fiscal support are stepped up a notch.

Risk assets have also benefited from a quicker than expected recovery, with

economic data and company earnings consistently printing well ahead of

consensus estimates. Few would have modelled a +4% year-on-year growth

rate in earnings per share for the S&P500 in Q4 2020. The average (median)

company is on track to hit +10% growth, a 2-year high and the fastest

since Q3 2018 which benefited from the corporate tax cut. More widely, the

International Monetary Fund (IMF) recently raised its 2021 global growth

estimate to 5.5% – a level that would match 2007 as the best in four decades

of data.

The fact is that many companies outside of the hospitality and leisure

industries have adopted a “don’t let a good crisis go to waste” approach

and have successfully been adapting their businesses to a new and more

challenging environment with the assistance of technology. So, while

valuations have adjusted to a lower-for-longer interest rate environment and

with the alternatives of cash and bonds being so unattractive, we have been

following a two-prong approach. The first of which is to continue backing

management teams of companies with secular and structural growth drivers

supported by strong balance sheets, which makes them more defensive

during an economic downcycle and allows them to grow market share.

Secondly, to ensure that the shares that we are invested in provide enough

margin of safety from a valuation perspective for long term investors, even

in the event of a market correction. Interest rates will normalise again and

so too will valuations for risk assets. We can’t be exactly sure when this will

happen given that the US Federal Reserve (FOMC), along with many other

central banks, are adamant that monetary conditions will remain ‘ultra-loose’

for the foreseeable future, but we do expect lower returns and perhaps more

volatility in future and have positioned portfolios accordingly.

Conclusion

The outlook for the global economy remains favourable. Accommodative monetary and fiscal policies, high

savings ratios by households combined with pent up demand and normalisation in mobility as vaccines are

deployed bode well for growth momentum in the second half of the year. Forward looking indicators, the

oil price and industrial metal prices are all pointing to stronger growth and valuations of risk assets have

followed suit, providing investors with attractive returns since markets reached their lows in March 2020.

While fundamentals look set to continue to improve as the global economy re-opens again investors should

temper near term return expectations given elevated valuations. Asset prices have in some cases run

ahead of fundamentals and ideally require a period of consolidation. That doesn’t mean that a correction

is in the offing but does suggest that returns will be lower in the future and that investors need to be more

selective and circumspect when making investment decisions.

Market Performance % / as at 31 January 2021 EQUITIES JANUARY YTD 12 MONTHS Global FTSE All World TR Net (Sterling) -0.90% -0.90% 12.15% FTSE All World TR Net (US Dollar) -0.45% -0.45% 16.83% UK FTSE All-Share TR -0.81% -0.81% -7.55% US S&P 500 TR -1.01% -1.01% 17.25% Europe Dow Jones Euro STOXX TR -1.37% -1.37% 0.61% FIXED INCOME JANUARY YTD 12 MONTHS Bloomberg Barclays Series - E UK Govt 1-10 Yr Bond Index -0.44% -0.44% 1.73% Bloomberg Barclays Series - E US Govt 1-10 Yr Bond Index -0.24% -0.24% 4.03% JP Morgan Global Government Bond (Sterling) -1.80% -1.80% 2.06% JP Morgan Global Government Bond (US Dollar) -1.35% -1.35% 6.32% Iboxx Sterling Corporates Total Return Index -1.07% -1.07% 4.50% Iboxx US Dollar Corporates Total Return Index -1.07% -1.07% 6.06% CURRENCY vs. STERLING JANUARY YTD 12 MONTHS US Dollar -0.37% -0.37% -3.71% Euro -1.16% -1.16% 5.40% Yen -1.73% -1.73% -0.30% CURRENCY vs. US DOLLAR JANUARY YTD 12 MONTHS Euro -0.76% -0.76% 9.46% Yen -1.34% -1.34% 3.55% Source: FTSE International Limited (“FTSE”) © FTSE 2013. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under licence. All rights in the FTSE indices and / or FTSE ratings vest in FTSE and / or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and / or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent.

Asset Classes Equities

Equities Overweight Consumer Discretionary Overweight

Fixed Income Underweight Consumer Staples Neutral

Cash Plus Overweight Energy Underweight

Financials Neutral

Healthcare Overweight

Fixed Income Industrials Neutral

G7 Government Underweight Information Technology Overweight

Index-Linked (US Government) Overweight Materials Neutral

Investment Grade - Supranational Overweight Communications Services Neutral

Investment Grade - Corporate Slight Overweight Utilities Neutral

High Yield - Corporate Overweight Real Estate Underweight

Currencies / Interest Rates

RECOMMENDATION - INTEREST RATES

Current Direction

US Dollar Overweight 0.25%

Sterling Neutral 0.10%

Euro Underweight 0.00%

Melville Douglas

Melville Douglas is a subsidiary of Standard Bank Group Limited. Melville Douglas Investment Management (Pty) Ltd. (Reg. No. 1962/000738/06) is an authorised Financial Services

Provider. (FSP number 595)

Disclaimer

This document has been issued by Standard Bank Jersey Limited. Standard Bank House. PO Box 583. 47-49 La Motte Street. St Helier. Jersey. JE4 8XR. Tel +44 1534 881188. Fax +44 1534

881399. e-mail:sbsam@standardbank.com. For information on any of our services including terms and conditions please visit our website. www.standardbank.com/wealthandinvestment

Melville Douglas is a registered business name of Standard Bank Jersey Limited which is regulated by the Jersey Financial Services Commission. Registered in Jersey No. 12999. Standard

Bank Jersey Limited is a wholly owned subsidiary of Standard Bank Offshore Group Limited. a company incorporated in Jersey. Standard Bank Offshore Group Limited is a wholly owned

subsidiary of Standard Bank Group Limited which has its registered office at 9th Floor. Standard Bank Centre. 5 Simmonds Street. Johannesburg 2001. Republic of South Africa.

Prospective clients residing in the UK should be aware that the protections provided to clients by the UK regulatory system established under Financial Services and Markets Act 2000

(“FSMA”) do not apply to any services or products provided by any entity within the Standard Bank Offshore Group. In particular. clients will not be entitled to compensation from the

Financial Services Compensation Scheme. nor will they be entitled to the benefits provided by the Financial Ombudsman Service or other protections to clients under FSMA.

This document does not constitute an invitation or inducement to engage in investment activity and is presented for information purposes only. Investment in the portfolio should only be

undertaken following the receipt of advice from an appropriately qualified investment professional.

The value of investments may fall as well as rise and investors may get back less cash than originally invested. Prices. values or income may fall against the investors’ interests and the

performance figures quoted refer to the past. and past performance is not a reliable indicator of future results.

February 2021 | 2021-031You can also read