TOWN OF SHREWSBURY - Shrewsbury, MA

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Office of the TELEPHONE: (508) 841-8508

BOARD OF SELECTMEN FAX: (508) 842-0587

Selectmen@shrewsburyma.gov

TOWN OF SHREWSBURY

Board of Selectmen Meeting

Board of Selectmen’s Meeting Room

Richard D. Carney Municipal Office Building

100 Maple Avenue

Shrewsbury, Massachusetts 01545-5398

Tuesday, November 26, 2019 - 6:30 PM

MINUTES

Present: Mr. Maurice DePalo, Chairman, Ms. Beth Casavant, Vice Chairman, Mr. James Kane, Selectman, Mr.

John Samia, Selectman, Mr. John Lebeaux, Clerk

Also Present: Mr. Kevin Mizikar, Town Manager

Mr. DePalo called the meeting to order at 6:30 pm.

Ms. Casavant moved that the Board vote to enter into executive session under Mass General Law Chapter 30 A

Section 21 Purpose 6 to consider the purchase, exchange, or lease or value of real property at 653-657 Main Street

and 268 North Quinsigamond Ave. seconded by Mr. Samia, on a roll call vote, Ms. Casavant-yes, Mr. Kane-yes, Mr.

Samia-yes, Mr. Lebeaux-yes, Mr. DePalo-yes. Mr. Depalo stated that the Board will now go into executive session

pursuant to Mass General Law Chapter 30 A Section 21 Purpose 6 to consider the purchase, exchange, or lease or

value of real property at 653-657 Main Street and 268 North Quinsigamond Ave, because an open meeting may have

a detrimental effect on the negotiating position of the Board. Further, the Board will reconvene back into open

session. The Board went into Conference Room A for executive session and reconvened back into the Selectmen’s

Room at 7:00 pm for open session.

Preliminaries:

1. Approve bills, payrolls and warrants

On a motion by Mr. Kane, seconded by Mr. Samia, the Board unanimously voted to approve warrants 2019, 2042,

2044, and 2021 as presented.

2. Approve Minutes of November 12, 2019

On a motion by Mr. Samia, seconded by Mr. Kane, the Board unanimously voted to approve the minutes as written.

3. Announcements

Mr. Lebeaux announced that Saturday December 7th from 9 am to noon the Shrewsbury Police Department will be

holding a fill the wagon event to benefit Saint Anne’s Church human services. Mr. DePalo also announced the first

annual Yuletide Market sponsored by the Town Center Association on Saturday December 7th, and the trash delay due

to Thanksgiving.

4. Town Manager’s Report

Mr. Mizikar thanked and acknowledged all that attended the Town Center forum last week, the next forum is December

11th. Mr. Mizikar and Ms. Las also held an annual meeting with DCR and the USDA regarding the Asian Longhorn

Beetle Program. The DPW initiated the unidirectional flushing program by doing valve investigations. The binder

course is down on the Lake Street section being realigned, and will be open in mid-December. Mr. Mizikar also

thanked Sharon Yager, COA Director, on her 24 years of service prior to her retirement today.

Minutes

Shrewsbury Board of Selectmen

November 26, 2019

Page 2 of 5

Meetings/Hearings:

5. 7:05 pm – Public Hearing with Aggregate Industries-Northeast Region Inc., 625 Lake Street (Known as 651

Lake Street), for an amendment to their Storage Tank License from 40,000 gallons of fuel to 54,000 gallons

of liquid asphalt, 40,000 gallons of specification used fuel oil, and 700 pounds of propane

Stephanie Herbster, Land & Enviornment Manager and Francis DeFrancisco Plant Manager, appeared before the

Board. Ms. Herbster stated that the (2) 20,000 spec oil tanks sit empty, as they are relying on natural gas, and are

sitting as a reserve backup. There are no physical changes on site. No one in the audience wished to speak. On a

motion by Mr. Kane, seconded by Ms. Casavant, the Board unanimously vote to close the hearing. On a motion by

Ms. Casavant, seconded by Mr. Lebeaux, the Board unanimously voted to approve the license amendment.

6. 7:10 pm – Meeting with Chipotle Mexican Grill of Colorado, LLC, d/b/a Chipotle Mexican Grill, 97 Boston

Turnpike, regarding an Application for Change of Officers/Directors/LLC Managers to their Section 12 All

Alcohol Pouring License

Jon Aieta, Attorney from McDermott Quilty & Miller LLP appeared before the Board. Mr. Aeita stated that there is

no change in the day to day operations, just a change in corporate structure. On a motion by Ms. Casavant, seconded

by Mr. Lebeaux, the Board unanimously voted to approve the application.

7. 7:15 pm – Meeting with Huong Dam, proposed manager of Three Nguyen Worcester, Inc. d/b/a Osaka

Japanese Restaurant, 20 Boston Turnpike, for a Change of Manager to their All Alcohol Pouring License

Huong Dam, proposed manager, appeared before the Board. Ms. Dam stated that they need to do change of manager,

because the manager is no longer in the business. Nothing else is changing. On a motion by Ms. Casavant, seconded

by Mr. Lebeaux, the Board unanimously voted to approve the license application.

New Business:

8. Review and act on winter maintenance of unaccepted subdivision streets to be plowed by developers

pursuant to the Board of Selectmen Policy number 16

On a motion by Mr. Kane, seconded by Ms. Casavant, the Board unanimously voted to approve the winter maintenance

of unaccepted subdivision streets to be plowed by developers pursuant to the Board of Selectmen Policy number 16

9. Review memorandum dated November 21, 2019 from Jeffrey Howland, Director of Public Works, and act

on the list of private ways that snow and ice control services will be provided to pursuant to M.G.L. Chapter

40 Section 6C

Ms. Casavant disclosed that she does live on Clearview Road, a road listed on the list of private streets. There were

also three streets not named in the memo that received a letter from the DPW because their streets are impassable or

hazardous. The DPW will not be plowing those private streets until the road can be repaired to an acceptable standard.

On a motion by Mr. Kane, seconded by Mr. Lebeaux, the Board unanimously voted to approve the list of private streets

on the memo with the exception of the three streets that will be determined the following day.

10. Review and act on the reappointment of Mary E. Thompson as Town Accountant for a three year term to

expire December 31, 2022

On a motion by Mr. Lebeaux, seconded by Mr. Kane, the Board unanimously voted to approve the reappointment.Minutes Shrewsbury Board of Selectmen November 26, 2019 Page 3 of 5 11. Review and act on FY21 Fiscal Objectives Mr. Mizikar stated that some changes were made from the prior year. The changes were highlighted in the draft document sent to the Board. Mr. Mizikar stated that based on the actuarial report dated January 1, 2019, with the payment appropriated at ATM in May, the Town anticipates its accrued pension liability will be fully funded this fiscal year, two years in advance of the original goal of FY2022. However the actuary suggests revising mortality tables which would require a new amortization schedule to be set. If adopted these new tables create additional accrued liability for the pension system. There is no action needed to be taken by the Retirement Board this year since we are on schedule to meet what is required for PERAC and to meet the amortization table as originally laid out to be accomplished by FY2022. Mr. Mizikar recommended that the Town be conservative and funds the pension system at $4,315,000 and OPEB trust at $500,000. This would equal the total amount funded for the FY20 budget less one million dollars than in years past. Mr. Mizikar stated that he would work with the Board to determine a plan for the million dollars and that the Town would be conservative with costs moving forward. The allocation of any of the million dollars freed up from pension funding should only be used for one-time expenses and more conservatively could be held for future consideration for appropriation into a reserve or another financial move. Mr. Kane requested that the Manager further explain why the pension is funded earlier than FY2022 and also expressed his concerns that the School Department is moving forward with a no-fee full day kindergarten program which also may pose a budgetary concern. Mr. Samia suggested that the one million less than the proposed amount to fund OPEB be moved into free cash until there is more clarity in FY2022. Ms. Casavant stated that she favors using the million for relief for departments that need it. Mr. Mizikar stated a decision does not need to be made until late in the budget process before Town Meeting. Mr. Mizikar reviewed the remainder of the draft FY21 objectives with the Board and disused the highlighted changes. No action was taken. 12. Review and act on deed restrictions for 653-657 Main Street On a motion by Mr. Kane, seconded by Mr. Lebeaux, the Board voted four to one, Mr. Samia opposed, to set the following deed restrictions on the property of 653-657 Main Street: The premises are conveyed subject to the following restrictions (the “Restrictions”): -The premises may not be subdivided in any manner, including, without limitation, subdivisions permitted by the so-called approval not required process in accordance with M.G.L. c. 41, s. 81P The Restrictions shall run with the land and be binding upon the Grantee, and any future owner of the premises, in perpetuity as restrictions held by a governmental body in accordance with M.G.L. c. 184, s. 26. Grantor, by executing this deed, and Grantee, by accepting this deed, state and acknowledge that the Restrictions are of actual and substantial benefit to the Grantor and are enforceable by the Grantor by proceedings at law or in equity against any person or persons violating or attempting to violate the Restrictions.

Minutes

Shrewsbury Board of Selectmen

November 26, 2019

Page 4 of 5

New Business:

13. Review and vote to support the managers proposed increase for PAYT fees as outlined in a memorandum

dated November 20, 2019

On a motion by Mr. Kane, seconded by Ms. Casavant, the Board unanimously voted to approve the increase as outlined

in the memo.

Possible Executive Session:

14. 6:30 PM: Conference Room A: Executive Session to consider the purchase, exchange, or lease or value of real

property, because an open meeting may have a detrimental effect on the negotiating position of the Board (G.L. c.

30A, S 21 (a)(6), 653-657 Main Street, 268 North Quinsigamond Ave)

6:30 pm: Ms. Casavant moved that the Board vote to enter into executive session under Mass General Law Chapter

30 A Section 21 Purpose 6 to consider the purchase, exchange, or lease or value of real property at 653-657 Main

Street and 2687 North Quinsigamond Ave. seconded by Mr. Samie, on a roll call vote, Ms. Casavant-yes, Mr. Kane-

yes, Mr. Samia-yes, Mr. Lebeaux-yes, Mr. DePalo-yes. Mr. Depalo stated that the Board will now go into executive

session pursuant to Mass General Law Chapter 30 A Section 21 Purpose 6 to consider the purchase, exchange, or

lease or value of real property at 653-657 Main Street and 268 North Quinsigamond Ave, because an open meeting

may have a detrimental effect on the negotiating position of the Board. Further, the Board will reconvene back into

open session. The Board went into Conference Room A for executive session and reconvened back into the

Selectmen’s Room at 7:00 pm for open session.

Correspondence: The Board of Selectmen will review and possibly act on the following:

15. ZBA Decision of October 28, 2019, 3 Industrial Drive, LLC, 487 Grafton Street, for special permit, for property

located at 3A Industrial Drive- so noted

16. ZBA Decision of October 28, 2019, John Power, 246A South Quinsigamond Ave, for special permit, for property

located at 246A South Quinsigamond Ave- so noted

17. ZBA Decision of October 28, 2019, Smart Growth Design, LLC, 625 South Street, for comprehensive permit

extension, for property located at 440 & 526 Hartford Turnpike- so noted

18. ZBA Decision of October 28, 2019, Theodore Canty, 58 Westwood Road, for variance, for property located at 58

Westwood Road - so noted

19. Email, dated October 27, 2019, from Jessica Beliveau, Office of State Representative Hannah Kane, re: Staff

Change in Representative Kane’s Office- so noted

20. Email, dated October 28, 2019, from Anna Darrow, Office of State Representative Hannah Kane, re: Rep Kane &

Sen Moore's Annual Holiday Luncheon- so noted

21. Memo, dated November 8, 2019, from Kristen Las, Assistant Town Manager, re: School Children in Housing

Developments October 2019- so noted

22. Email, dated November 9, 2019, from Kevin Mizikar, Town Manager, to Colleen Hutchins, 3 Millwood Drive, re:

Waste Management- so noted

23. Email, dated November 10, 2019, from Joanne Helstowski, 4 Birch Brush Road, re: Waste Management

Complaint- so noted

24. Email, dated November 13, 2019, from the Community Preservation Shrewsbury Ballot Question Committee, 38

Stoney Hill Road, re: Adopting the Community Preservation Act in Shrewsbury- Mr. DePalo discussed additional

info that would be needed from the CPA group and Mr. Kane asked for more facts to understand what the

mandatory steps are

25. Letter, dated November 12, 2019, from David Brown, Nelson Point, LLC, P.O. Box 427, Harvard, re: Request for

Public Way Acceptance of Point Road and Nelson Point Road- Send to Engineering and Planning for inputMinutes

Shrewsbury Board of Selectmen

November 26, 2019

Page 5 of 5

26. Email, dated November 14, 2019, from James Vuona, Fire Chief, re: Engine 1 Refurbish Completed- so noted

27. Email, dated November 14, 2019, from Kristen Las, Assistant Town Manager, re: Town of Shrewsbury Municipal

Vulnerability Preparedness Grant Application November 2019- so noted

28. Email, dated November 15, from Karen Troy, 22 Minuteman Way, re: Old Mill Road Sidewalks- Send to

Engineering & Highway

29. Email, dated November 18, 2019, from Mary Jane Handy, Massachusetts Department of Revenue, re: Tax Rate

Approval Notification - Shrewsbury – 2020- so noted

30. Email, dated November 20, 2019, from Missy Hollenback, 38 Stoney Hill Road, re: Recycling

Committee/Sustainability Coordinator- Ms. Casavant commented that the Town does have the designation of

Green Community and Mr. Snowdon is the point of contact that works with MassDEP and has received recent

grants and also discussed many recycling initiatives that the Town is working on.

On a motion by Mr. Kane, seconded by Mr. Lebeaux, the Board unanimously voted to adjourn at 8:05 pm.

Respectfully Submitted,

Valerie B. Clemmey

Administrative Assistant to the Board of Selectmen

Referenced Materials

11/21/2019 Memo from J. Howland, re: Private Streets Winter Maintenance

FY21 Draft Financial Objectives

11/20/2019 PAYT MemoMemo

Department of Public Works

Date: November 21, 2019

To: Kevin Mizikar

Nancy Jones

Nick Repekta

From: Jeffrey Howland, PE; Director of Public Wor1)

RE: Plowing Private Streets

Attached herewith is a list of private streets of which are private in the

Town.

S

The Board of Selectmen would need to vote approval of plowing and

de-icing these streets for the upcoming winter.

The Town in the past has plowed most private streets unless they are

impassable or hazardous. In July, Highway Division Manager Nick Repekta

inspected all the private streets on the list and mailed a letter dated July 26,

rng to each of the property owners that abutted the unacceptable streets.

There were a total of 9 streets on the initial list that were deemed

unacceptable.

The Highway Division conducted a follow-up inspection on the g

unacceptable streets in early November and found only 3 streets remained on

the list and letters were sent out to both the streets that were removed from

the list (letter dated November 6, 2019) and to the streets that remained on

the list Getter dated November 5, 2019). Nick remains in discussion with each

of the three remaining street abutters so that they can also be removed from

the list

There are several private streets that Town does not plow as a result of

previous agreements (Planning Board Decisions, etc.). We assume no

responsibility for any repairs on the streets caused by the Town of Shrewsbury

or its contractors during plowing and sanding operations.

11/21/19TOWN OF SHREWSBURY

PRIVATE STREET

PLOW LIST 201812019

ASSESSOR

TAX MAP

STREET NUMBER

Acorn Street PRIVATE 39

Aithea Path PRIVATE 31

Anglin Lane PRIVATE 57

Avon Drive PVT DR 32

Bagley Avenue PRIVATE 31

Baker Avenue PRIVATE 32

Barrows Road PRIVATE 16

Bay Road PRIVATE 51

Beacon Street PlO PRIVATE 33

Beaver Drive PRIVATE 16

Becket Street PRIVATE 13

Bellingham Way PRIVATE 57

Benton Street PRIVATE 39

Beverly Road PRIVATE 32

Blackstone Street PRIVATE 52

Bosworth Road PRIVATE 7

Broadway PRIVATE 27

Brooklawn Parkway PRIVATE 14

Cedar Road PRIVATE 45

Chamberlain Road PRIVATE 13

Charles Street PRIVATE 32

Church Road PRIVATE 22

Clear View Road PYF DR 17

Colton Lane PlO prr 16, 21

Crosby Street PlO PRIVATE 13

Cutler Street PRIVATE 25

Douglas Circle PRIVATE 33

East Lake Road PRIVATE 38

Eaton Avenue PRIVATE 13

EkCouft PRIVATE 57

Everett Avenue PlO PVT 32

Fifth Avenue R.O.W. PRIVATE 31

First Street PRIVATE 31

Forest Avenue PRIVATE 57

Fyrbeck Avenue PRIVATE 25

Gifford Drive PRIVATE 16

Grace Avenue PRIVATE 45

Greylock Avenue PRIVATE 32

Grove Ridge Path PRIVATE 31

Harlow Road PRIVATE 22

Harold Lane PRIVATE 51Hayden Lane PRIVATE 53 Hazel Avenue PRIVATE 7 Higgins Street PRIVATE 13 Highland Street PRIVATE 52 Huntington Road PRIVATE 57 Ira Avenue PRIVATE 13 Irving Drive PRIVATE 51 Jackson Street PRIVATE 39 Jacob Street PRIVATE 13 John Street PRIVATE 45 Kenmore Street PRIVATE 13 Keswick Street PRIVATE 29 Kings Point Drive PRIVATE 45 Kingston Street PRIVATE 39 Kirk Street PRIVATE 13 Lakeside Path PRIVATE 31 Lakewood Drive PlO PYF 39 Lear Street North PRIVATE 19 Lear Street South PRIVATE 19 Lebeaux Drive PRIVATE 36 Leblanc Road PRIVATE 32 Maplehurst Street PRIVATE 13 Mahe Street PVT DR 40 Marlboro Street PRIVATE 33 Miles Avenue PRIVATE 31 Monroe Street PlO PVT 27 Morrill Avenue PRIVATE 32 Naples Street PRIVATE 39 Nelson Point Road PRIVATE 52 Newton Street PRIVATE 27 Norcross Point PRIVATE 57 Norton Way PRIVATE 51 Norwood Avenue PRIVATE 23 Oak Island PRIVATE 57 Oakland Avenue PRIVATE 19 Olive Avenue PRIVATE 52 Olympia Avenue PlO PVT 31, 32 Oregon Avenue PlO P’fl 31, 32 Oval Drive PRIVATE 14 Overlook Avenue PRIVATE 46 Park Street West PRIVATE 22 Park View Lane PVF DR 22 Pearl Street PVt DR 25 Peninsula Drive PRIVATE 57 Phillips Avenue PRIVATE 31 Phillips Court PRIVATE 31 Pine Avenue PRIVATE 31 Pinedale Road PRIVATE 38

Pineland Avenue PRIVATE 39

Pleasant View Street PRIVATE 7

Pond Avenue PRIVATE 13

Redland Street P/C PVT 39

Rhinecliff Street PRIVATE 13

Rice Avenue /

PRIVATE 13

Roberts Street PRIVATE 38

Robertson Drive PRIVATE 51

Sadler Avenue PRIVATE 32

Salisbury Street PRIVATE 57

Selina Street PRIVATE 32

Shirley Lane PRIVATE 19

Sleepy Hollow PRIVATE 38

Smith Lane PRIVATE 51

Smith Road PRIVATE 51

South Brook Street PRIVATE 46

Stoneland Road PRIVATE 45

Stoneland Road Way PRIVATE 45

Stringer Dam Road PRIVATE 51

Summer Street extension PRIVATE 28

Sunderland Lane PVT DR 57

Sunset Lane PRIVATE 51

Tamarack Lane PRIVATE 19

Temple Court PRIVATE 19

Verona Avenue PRIVATE 13

Viking Terrace PRIVATE 57

Vista Place PRIVATE 17

Walnut Drive PRIVATE 23

Walnut Hill Lane PRIVATE 24

Wendell Street PRIVATE 39

Whitney Street PlO PVI 32

Worthington Avenue P/C PVT 39Office of the

HIGHWAY DWTSION TELEPHONE: (508) 841-8502

FAX: (508) 841-8607

nrepektashrewsburyma.gov

TOWN OF SHREWSBURY

Richard D. Carney Municipal Office Building

100 Maple Avenue

Shrewsbury, Massachusetts 01545-5398

July 26, 2019

Dear Resident,

The Town of Shrewsbury DPW Highway Division has determined that the current

condition of your private road needs repairs so as not to cause damage to Town-owned or

Contractor snow removal equipment this upcoming winter season.

The Highway Division will re-inspect your street, approximately October 31, 2019, to see

the necessary repairs have been made and at that time will determine if snow removal on

your private road will continue as it has in the past.

If you need help identifying the work needed to be done, please contact the Highway

Department at (508) 841-8502.

Thank you for your attention to this matter. If you have any further questions, please feel

free to contact me.

Very Truly Yours,

Nick Repekta

Highway Division Managera

Office of the

HTGHWAYDWISION I

TELEPHONE: (508)841-8605

*

FAX(5O8)8414607

nrepckta(shrewsbutyniagov

TOWN OF SHREWSBURY

Richard D. Carney Municipal Office Building

100 Maple Avenue

Shrewsbury, Massachusetts 01545-5398

November 5, 2019

Dear Private Street resident,

Upon recent inspection of your private street, the Town of Shrewsbury DPW Highway

Division has determined that an acceptable standard of your private street has not been

met per the letter sent on July 26,2019. The Highway Division respectfully requests that

within the next 30 days, some repairs to your street to achieve an acceptable standard take

place or plowing and de-icing services provided by the Highway Division will not take

place for this upcoming winter season. If you have any questions, please feel free to

contact me.

Very truly yours,

Nick Repekta

Highway Division Managera

Officeofihe

HIGHWAY DIVISION TELEPHONE: (508) 841-8605

FAX: (508)8414607

nrepektashrewsburyma.gov

TOWN OF SHREWSBURY

Richard D. Carney Municipal Office Building

100 Maple Avenue

Shrewsbury, Massachusetts 01545-5398

November 6, 2019

Dear Resident,

The Town of Shrewsbury DPW Highway Division has recently inspected the current

condition of your private road as a follow up to the letter dated July 26, 2019. It has been

determined that an acceptable standard has been met and snow and ice removal will

continue as it has in the past. -

Thank you for your cooperation with this matter.

Very truly yours,

Nick Repekta

Highway Division ManagerTOWN OF SHREWSBURY

FINANCIAL OBJECTIVES 2021

November 26, 2019Table of Contents INTRODUCTION ................................................................................................................ 2 A – RETIREMENT SYSTEM & OPEB FUNDING .............................................................. 3 A.1 – Objective: Retirement System Funding: FY20 Budget .......................................... 3 A.2 – Reserve: Retirement System Funds Planning ....................................................... 3 A.3 – Reserve: OPEB Funding through Landfill Ash Revenue ....................................... 3 A.4 – Reserve: OPEB Funding through Marijuana Excise Tax ...................................... 4 B – FUNDING REQUIREMENTS FOR THE NEW BEAL ELEMENTARY SCHOOL ...... 4 Town of Shrewsbury – Financial Objectives Fiscal Year 2021 1

INTRODUCTION Annually at the outset of the budget planning process, the Board of Selectmen provides specific direction to the Town Manager by setting Financial Objectives for the upcoming budget year. These objectives clarify and enhance other policies of the Board providing the Town Manager with timely guidance on high priority matters that are to be incorporated into the development of the budget. These objectives are set in concert with the Financial Policies of the Town, and often are much more narrowly focused and provide a greater level of detail on the interests of the Board of Selectmen. If you have any questions, please contact Town Manager Kevin J. Mizikar at 508-841-8508 or kmizikar@shrewsburyma.gov. Town of Shrewsbury – Financial Objectives Fiscal Year 2021 2

A – RETIREMENT & OTHER POST EMPLOYMENT BENEFITS FUNDING Background: The Town of Shrewsbury has prudently enacted a multi-year plan to fund its retiree pension obligations. The dedication to this plan, coupled with recent gains on investments, has placed the Town in a position to fully fund its obligation in fiscal year 2020 (FY20). An actuarial analysis of the Shrewsbury Retirement System as of January 1, 2019 shows the system is 95.8% funded with a remaining obligation of $5,603,844, which will be funded in FY20. A recommendation by the Retirement System’s actuary suggests revising the mortality tables used by the Town to calculate future costs. This will require a new amortization table and funding levels above the normal cost for the next two to five years. However, there will be opportunity to reduce the total funding dedicated to the pension system below the FY20 level of $5,315,693. The Town has made $4,244,916 in contributions to Other Post Employment Benefit (OPEB) liabilities. The most recent actuarial analysis as of June 30, 2018 calculates the Town’s unfunded liability at $52,650,000. The Board of Selectmen committed to enhancing funding for OPEB liabilities once its pension obligations are fulfilled. A.1 – Objective: Retirement System Funding: FY21 Budget Fund the pension system at a $4,315,000. Fund Other Post Employment Benefit trust at $500,000. A.2 – Objective: Retirement System Funds Planning Work with the Retirement Board to establish a manageable funding schedule for FY22 and beyond that accounts for the latest recommended accrued liabilities of the pension system while reducing funding. Should revised mortality table be adopted, satisfy the new accrued liabilities no later than FY24. The $1,000,000 in reduced from the pension system funding when comparing FY20 to FY21 shall be use conservatively for one-time expenses in FY21 to allow the development of a longer term plan. $141,084 of the $1,000,000 shall be used to fund OPEB liabilities. A.3 – Objective: OPEB Funding through Landfill Ash Revenue Background: The Town receives revenue annually through a contract with Wheelabrator for the operation of the Shrewsbury landfill. This revenue is derived from Wheelabrator depositing ash from its waste-energy incinerators into the Shrewsbury landfill. Payments are made based upon an agreed to amount per cubic yard of deposited material. In FY19 the total revenue from this contract was $2,009,241. The Town is free to use these revenues for any lawful municipal purpose. Currently these revenues are used to fund various aspects of the operating budget. The operations that this revenue sources funds are anticipated to continue in perpetuity. Town of Shrewsbury – Financial Objectives Fiscal Year 2021 3

Unfortunately, there is a limited amount of space remaining at the Shrewsbury Landfill. Based upon a detailed review of the current agreement and meetings with Wheelabrator’s operations manager, the Town can expect to receive approximately $1,500,000 in FY21 and then $1,600,000 per year through FY28. This is a reduction from previous estimates of $1,800,000 per year. The landfill will reach its current permitted capacity in FY28. Therefore, the Town must find a way to offset its reliance on this revenue source to prevent a structural budget deficit. Objective: Once a long term reallocation plan for the pension funding is adopted, dedicate all forecasted revenues from the agreement with Wheelabrator to funding OPEB liabilities. The Wheelabrator revenue used to fund the operating budget will be replaced with revenues currently funding the Retirement System. A.4 – Objective: OPEB Funding through Marijuana Excise Tax Background: The Town is in a relatively unique situation where it will benefit from a new revenue source likely in FY21. These funds will be realized through the collection of a 3.0% excise tax on the retail sales of recreational marijuana. The total revenue that the Town will receive through this source is unknown. However, various independent marijuana establishments have estimated the Shrewsbury market to have $10,000,000 to $15,000,000 in sales resulting in $300,000 to $450,000 in taxes. Objective: Do not anticipate marijuana revenue for FY21 given that no retail establishments are fully licensed or permitted to open. Consider the use of marijuana revenues in future years for OPEB purposes once a funding philosophy is established. B – FUNDING REQUIREMENTS FOR THE NEW BEAL ELEMENTARY SCHOOL Background: Construction has begun on the new Beal Elementary School at 214 Lake Street. The building is scheduled to open in the fall of 2021, in FY22. This school is being constructed in part to provide additional educational space to meet the growing school student population, reduce overcrowding in other school facilities and provide full day educational programs for Kindergarten through Grade 12. This will require additional educational professionals, educational support professionals and there will be an increase in related expenses. Objective: Working closely with the School Department, develop a comprehensive expense plan for the operation of this new facility and related changes across the Shrewsbury Public Schools. This plan should be developed by the early summer of 2020 and be used to inform the FY22 budget process. Town of Shrewsbury – Financial Objectives Fiscal Year 2021 4

Adopted this 26th day of November, 2019.

Board of Selectmen:

_______________________________

Maurice M. DePalo

_______________________________

Beth N. Casavant

_______________________________

John I. Lebeaux

_______________________________

James F. Kane

_______________________________

John R. Samia

Town of Shrewsbury – Financial Objectives Fiscal Year 2021 5Office of the TELEPHONE: (508) 841-8508

TOWN MANAGER FAX: (508) 842-0587

kmizikar@shrewsburyma.gov

TOWN OF SHREWSBURY

Richard D. Carney Municipal Office Building

100 Maple Avenue

Shrewsbury, Massachusetts 01545-5338

MEMORANDUM

November 20, 2019

To: Board of Selectmen

From: Kevin J. Mizikar, Town Manager

Re: Pay-As-You-Throw Rate Increase

I am seeking the support of the Board of Selectmen in my decision to increase the rate structure of the

Pay-As-You Throw program as follows, with an effective date of July 1, 2020:

% Proposed Proposed Current Current Variance Variance

Increase $/item $/roll $/item $/roll $/item $/roll

Small Bag 47.00% $1.10 $5.50 $0.75 $3.75 $0.35 $1.75

Large Bag 50.00% $2.25 $11.25 $1.50 $7.50 $0.75 $3.75

Recycling Bins 36.36% $15.00 - $11.00 - $4.00 -

Bulk waste 20.00% $12.00 - $10.00 - $2.00 -

Reference material supporting this request can be found in the attached PAY-T Fee Analysis

dated October 3, 2019. This increase is necessary to meet the rising costs of the recycling market

which requires the Town to now pay processing and disposal of recyclable materials and the

apparent cost of the recent consumer price index (CPI), and will result in the end goal of funding

the enterprise account through 50% of the tax levy and 50% of program fees.

This is the first instance that the rates will be increased since the implementation of the Pay-As-

You-Throw Program in 2008.

Enclosure: PAYT Draft Analysis dated October 3, 2019TOWN OF SHREWSBURY

PAY-T FEE ANALYSIS & RECOMMENDATION

October 3, 2019(This Page Intentionally Left Blank) Town of Shrewsbury – PAY-T Fee Analysis 1

Table of Contents

EXECUTIVE SUMMARY................................................................................................................ 4

BACKGROUND .............................................................................................................................. 5

STAKEHOLDER ANALYSIS .......................................................................................................... 8

INTENDED USE OF THE ANALYSIS ............................................................................................ 9

EVALUATION FOCUS...................................................................................................................10

METHODS .....................................................................................................................................10

NEEDS ASSESSMENT...............................................................................................................10

OUT-YEAR EXPENDITURES & REVENUES ...........................................................................10

COMPARABLE COMMUNITIES ............................................................................................... 11

COMPARABLE PRIVATE RESIDENTIAL SERVICE ................................................................ 12

EVALUATION LIMITATIONS .................................................................................................. 12

PROPOSED MEASUREMENTS ................................................................................................ 12

ANALYSIS AND INTERPRETATION ........................................................................................... 13

SUMMARY ................................................................................................................................. 13

ADDITIONAL PAY-T FEE REVIEW.......................................................................................... 16

REVENUE ANALYSIS ............................................................................................................... 17

INDIRECT COSTS ..................................................................................................................19

TOTAL EXPENDITURES & TAX LEVY ................................................................................. 21

ENTERPRISE REVENUES ....................................................................................................21

PAY-T FEE ANALYSIS .............................................................................................................. 23

FINDINGS & IMPACT ANALYSIS............................................................................................ 26

IMPLEMENTATION & COMMUNICATION ............................................................................... 27

KEY ROLL-OUT OBJECTIVES................................................................................................. 27

APPENDIX.................................................................................................................................... 30

Town of Shrewsbury – PAY-T Fee Analysis 2(This Page Intentionally Left Blank) Town of Shrewsbury – PAY-T Fee Analysis 3

EXECUTIVE SUMMARY

The following evaluation and recommendation was developed and prepared for the Town

of Shrewsbury to both review the Pay-As-You-Throw (PAY-T) operations within the Solid

Waste Enterprise and to assess the fee structure’s viability to date resulting in a

recommendation for PAY-T fees (bags, bins, bulk waste) for FY 21 – FY 25.

Now in the 11th year of operation and with the recycling market changes the Town has the

opportunity to gain new perspective on the program’s success in its endeavors. Through

a mixed methodical approaching implementing both quantitative and qualitative

approaches and a cross-community comparison; this report reviews and evaluates the

Town’s Solid Waste and Recycling Enterprise and addresses the following:

1. PAY-T Fee recommendation for FY 21 – FY 25 as detailed below:

Proposed Proposed Current Current Variance Variance

$/bag $/roll $/bag $/roll $/bag $/roll

Small $1.10 $5.50 $0.75 $3.75 $0.35 $1.75

Large $2.25 $11.25 $1.50 $7.50 $0.75 $3.75

Recycling Bins $15.00 - $11.00 - $4.00 -

Bulk waste $12.00 - $10.00 - $2.00 -

2. Comprehensive 5-year Operating Cost Projection (Direct and Indirect)

3. Recommendations of program improvements based on a cross comparison of

comparable communities PAY-T programs.

When averaged, the household impact for PAY-T bags would be an increase of $0.7885

per week or $41.00 per year. Using the average household consumption figures a

household currently can expect to pay $83.46 in PAY-T bags. The proposed bag fees

would increase this annual amount to $124.46/year.

The evaluation/report establishes a critical initial step in the review of the Solid Waste

and Recycling Enterprise and it is recommended that a similar review be conducted in

concert with the Solid Waste Contracts every five years to ensure sufficient program

funding.

As this plan presupposes a participatory collaboration among all stakeholders involved,

it is imperative that any rate adjustments or program changes continue in a transparent

and communicative process.

As with the development of any comprehensive evaluation and/or report, this study

would not be made possible without the extended efforts by all those involved. At this

time, I want to thank each and every one who assisted throughout this project.

If you have any questions, please contact Management Analyst, David C. Snowdon at

508-841-8508 or dsnowdon@shrewsburyma.gov.

Respectfully Submitted,

David C. Snowdon

Town of Shrewsbury

Assistant – PAY-T

to the Town Fee Analysis

Manager, Management Analyst 4BACKGROUND

Shrewsbury’s PAYT program went into effect in August 4th, 2008. In the PAY-T program,

residents are charged for the collection of municipal solid waste based on the amount they

throw away. With the goal to create an economic incentive to recycle more, generate less

waste, and reduce Solid Waste costs to both the town and its citizens.

Pay-as-you-throw, “The solution to the trash problem” 1

For roughly 56% of the communities across the Commonwealth, the typical municipally

led solid waste program draws revenue from two main sources: a portion of property

taxes, or a fixed bill amount that does not vary in respect to the amount of waste removed.

This approach creates a disconnect between the cost of service and the constituent,

ultimately hindering any incentive to reduce waste disposal. The remaining 154

communities such as Shrewsbury have implemented variations of the PAY-T program for

this purpose.

Ten years prior to the Town of Shrewsbury’s adoption of a PAY-T program, The EPA had

been promoting similar initiatives. By 2004, 110 out of 351 municipalities in

Massachusetts had implemented PAY-T programs. Shrewsbury’s neighbor, Worcester,

through its PAY-T program had decreased its waste management costs by $1.2 million

and increased its recycling rate from 3% to 36% immediately following the program’s

introduction in 1993. 2

In fiscal years 2006 and 2007, the town of Shrewsbury’s recycling was only 20% of the

total waste collected, which was significantly lower than the EPA’s 40% diversion goal. 3

Additionally, the low recycling rates were incurring higher solid waste expenses for the

town. The Town of Shrewsbury’s trash hauler in 2007 provided recycling at no additional

charge, and residents who were not recycling were in violation of the town’s bylaw. 4

The PAY-T program was designed to reduce budget expenses by incentivizing residents

to recycle more; and the Town’s revenue generated from the sale of PAY-T bags would pay

for services and offset the Tax Levy impact. 5 Until very recently, simply increasing

recycling would reduce the tonnage of trash at the curb, resulting in less spending for

1 WasteZero. “Pay-as-you-throw, The Solution to the Trash Problem”. http://wastezero.com/our-solutions/pay-as-

you-throw/

2 Canterbury, J. & Eisnefeld, S. “The Rise and Rise of Pay-as-you-Throw”. (MSW Management), Dec., 15, 2005.

3 Ibid., & Town of Shrewsbury. “2007 Annual Report”. https://shrewsburyma.gov/ArchiveCenter/ViewFile/Item/48

4 Town of Shrewsbury. “2007 Annual Report”. https://shrewsburyma.gov/ArchiveCenter/ViewFile/Item/48

5 Town of Shrewsbury. “2008 Annual Report”. https://shrewsburyma.gov/ArchiveCenter/ViewFile/Item/49

Town of Shrewsbury – PAY-T Fee Analysis 5waste disposal. While this model inherently is still valid, it is imperative that the correct

curbside recyclable materials are collected as the Town now is required to pay for the

processing of recyclable materials. Recycling smart results in the best benefits to the

Town, the community, and the recycling market.

Over the first three years, the Town witnessed an 11.5% increase in recycling tonnages to

a total of 33.74% of the Town’s total collected curbside tonnage. From 2012 forward

recycling has slowly trended downward to approximately 29.67% of the total collected

curbside tonnage. This variance may best be explained by the transitioning from “wish

recycling” that may have been more evident in the first years of the PAY-T program to a

cleaner more marketable recycling stream. An August 2019 audit of the Town’s recycling

materials revealed a 1.55% and 2.00% contamination rate for the Co-mingled and Fiber

stream respectively. 6 While there is certainly room for improvement, the Town should be

encourages and proud of these levels.

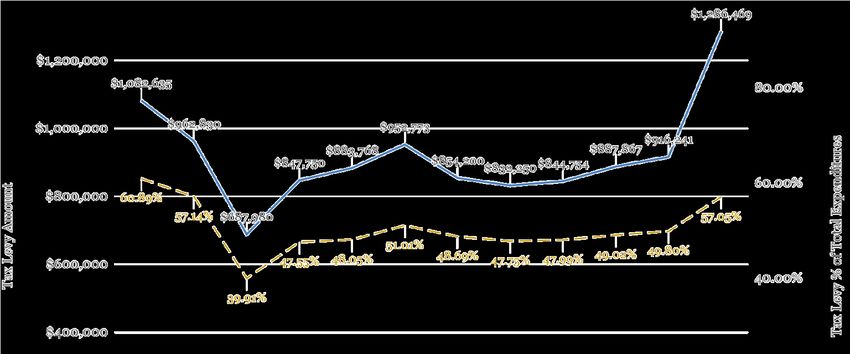

Prior to the implementation of the PAY-T program, the Solid Waste Enterprise Tax Levy

requirement in 2008 was $1,691,639. Since its inception, Shrewsbury’s PAY-T program

has endeavored to increase town wide recycling rates while reducing the Town’s financial

Tax Levy burden to roughly 50% of the enterprise’s total annual budgeted. From FY 09

to FY 19 the average budgeted tax levy and median budgeted tax levy are calculated at

$886,641 and $883,768 or 49.80% and 48.69% of the total budgeted expenditures

respectively.

Starting July 1, 2019, the Town began both its new Solid Waste and Collection contract

with Waste Management, and recycling disposal contract with Casella recycling.

Additionally, global changes in the recycling market introduced new recycling disposal

costs for the Town’s Solid Waste Enterprise. Thus, the PAY-T FY 20 budgeted Tax Levy

requirement is calculated at $1,286,469 or 57.05% of the enterprise budgeted

expenditures. A visual representation of the dollar change and percent change in the Tax

Levy Impact can be seen in Figure 1, Solid Waste and Recycling Enterprise Tax Levy

Impact, on page 7.

6

Casella Recycling, Town of Shrewsbury Residue Audit, August 5 – 16.

Town of Shrewsbury – PAY-T Fee Analysis 6Figure 1: Solid Waste & Recycling Enterprise – Tax Levy Impact* * Budgeted Tax Levies include Solid Waste Management Retained earnings except for FY 09 and FY 2010. ** In 2011, Solid Waste Retained Earnings were $200,000. Town of Shrewsbury – PAY-T Fee Analysis 7

STAKEHOLDER ANALYSIS

Background:

INFLUENCE

The intent of this section is to foster transparency about

the purposes of the analysis/evaluation and the access to

evaluation results. This section identifies the primary

intended users and purposes and intended uses of the

evaluation. To capture the involvement and needs of each

group associated with the Solid Waste Enterprise and the

PAY-T program, the stakeholders have been identified by

their roles along the following matrix.

INTEREST LEVEL

Meet Needs: Massachusetts Department of Environmental

Protection – The Recycling Dividends Program (RDP) is part of the MassDEP

Sustainable Materials Recovery Program (SMRP) which provides qualifying

municipalities who have implemented programs proven to maximize waste reduction,

re-use and recycling of which the Town of Shrewsbury has been granted. 7 Any changes

and improvements to Shrewsbury’s PAY-T program are also of direct concern of

MassDEP.

Key Players: Board of Selectmen, Finance Committee, Department of Public

Works, Town Manager’s Office – It is imperative these individuals be involved early

in the evaluation process to develop the values and questions most necessary for the

Town and the residents. These individuals are directly responsible for the general

welfare of the community and they possess direct influence on the current

implementation of the PAY-T program. For the above mentioned departments roles

will include the following:

a. For the above mentioned departments roles will include the following:

i. Facilitate in data collection

ii. Ensure/Increase credibility of analysis and interpretation on behalf

of Town residents

iii. Disseminate evaluation recommendations/information

iv. Aid implementation of recommendations

Key Informed: WasteZero, Manufacturer of PAY-T bags, Waste Management,

contracted hauler, Wheelabrator, contracted solid waste disposal, and retailers of

PAY-T bags and stickers – WasteZero and several of the retailer stores have been

working with the Town of Shrewsbury since the inception of the PAY-T program in

2008. Any changes to the program will directly impact their service provision.

WasteZero currently holds the contract with the Town of Shrewsbury to supply the

necessary volume of PAY-T bags which are then sold through retailers in town.

Both Waste Management, the contracted hauler, and Wheelabrator, trash disposal

services, provide daily waste management services. Wheelabrator has a yearly limit

on the allotted cubic yardage of ash stored at the town’s landfill. Any reduction in

7MassDEP. “Sustainable Materials Recovery Program (SMRP) Municipal Grants”.

https://www.mass.gov/how-to/sustainable-materials-recovery-program-smrp-municipal-grants

Town of Shrewsbury – PAY-T Fee Analysis 8Shrewsbury waste allows Wheelabrator to bring in ash from other communities to be

stored at the landfill. Therefore, any changes and future implementation of the PAY-

T would be of direct concern as it would impact their contracts and solid waste

management services.

b. Roles will include:

i. Inventory of current PAY-T quantities in production and at retailers

ii. Provide insight into PAY-T program options

iii. Address any concerns with bag quality

iv. Assist in implementation of PAY-T Bag fee changes

Key Informed & Involved: Town Meeting members, Town Residents – To

understand all the contextual factors and aspects of Shrewsbury’s PAY-T program it is

important actively involve and engage the direct users of the program. The Town

Meeting members are elected residents who are to act in the best interest of the

residents they represent. Gathering and understanding the views of the Shrewsbury

residents and their Town meeting representatives is imperative for any successful

program changes.

c. Roles will include:

i. Provide insight into current program operations

ii. Provide insight on proposed fee adjustments

INTENDED USE OF THE ANALYSIS

The variety of stakeholders involved will be able to use the evaluation results to focus and

improve the operations of Shrewsbury’s PAY-T program going forward. An evaluation of

the program's effectiveness in meeting its goals will be most useful to the Town

Administration, the Board of Selectmen, and the Finance Committee who design, review

financials, and implement the various aspect of the PAY-T program.

The recommendations and results can be a useful resource for Massachusetts Department

of Environmental Protection (MassDEP) as they will provide contextual insight into how

effectively the PAY-T programs are working to achieve its goals within specific

municipalities. The evaluation results will also be shared with comparable communities

to provide useful insight for their specific programs.

Ultimately, the intent of evaluation is to gauge the effectiveness and efficiency of

Shrewsbury’s PAY-T program while providing opportunities for improvement within the

town and the statewide program. A primary goal of the evaluation, is to uncover strengths

in programs that engender greater recycling rates at a reduced cost to municipalities.

Individuals and residents, may possess the desire to recycle through ingrained social

values; however, when the rubber meets the road proper incentives must be in place to

further encourage such social values.

Town of Shrewsbury – PAY-T Fee Analysis 9EVALUATION FOCUS

The proposed evaluation plan’s focus and design has been selected for its feasibility in

implementation and its efficiency to discern the program’s strengths and weaknesses.

Accordingly, this plan proposes the use of both quantitative and qualitative design and

methodologies which will provide meaningful data and further inform evaluation

questions and procedures. The following evaluation questions have been chosen for their

ability to ascertain core program values.

Evaluation Questions:

1. Operational Costs on a per PAY-T bag basis

2. PAY-T Bag Fee recommendation for FY 21 – FY 25

3. Comprehensive 5-year Operating Cost Projection (Direct and Indirect)

4. Recommendations of program improvements based on a cross comparison of

communities with and without PAY-T

METHODS

This section details the necessary performance measures, data sources, and the methods

selection to properly address the evaluation questions. Throughout the analyses that

follow, detailed assumptions are provided to ensure clarity and transparency.

NEEDS ASSESSMENT

The pretest, or initial observation evaluated the community’s annual solid waste tonnage

as a means to understand the full cost of collecting, disposing, and providing services

related to the Solid Waste and Recycling Enterprise on a per PAY-T bag basis.

Enterprise Revenue, actual received, for SMALL and LARGE bags, Bulk waste stickers,

and Recycling Containers, ranging from FY10 – FY 19 were gathered through the Town’s

accounting in Munis.

Disposal Tonnages per year are gathered through Wheelabrator invoices and reported

annually both in a Town PAY-T Report and to MassDEP per the Recycling Dividends

Program requirements.

OUT-YEAR EXPENDITURES & REVENUES

Known out-year expenditures were gathered from current agreements for service:

1. Waste Management - Collection of Solid Waste & Recycling Materials, FY 20 - FY 25

2. Casella Recycling – Recycling Services Agreement, FY 20 - FY 25

3. Wheelabrator Technologies – Solid Waste Disposal, Thru – FY 28

4. WasteZero – Manufacturing of PAY-T Bags, FY 20 – FY 22

Additionally, adjustments for inflation based on recent cost trends for services not under

agreement but annually expended were utilized in the projection of out-year

expenditures.

Town of Shrewsbury – PAY-T Fee Analysis 10COMPARABLE COMMUNITIES

The comparable communities were selected using purposeful/ theoretical sampling based

on population size, population, trash households, Equalized Value, and PAY-T start date. 8

Following an initial analyzation of Massachusetts Department of Revenue and

Massachusetts Energy and Environmental Affairs data the following criteria have been

chosen for the comparable communities.

1. Population size: 25,000 – 45,000

2. Trash households served: 9,000 – 15,000

3. Equalized Value: $5,000,000,000 - $8,000,000,000

4. PAY-T start date: 2000 – 2008

In addition to the aforementioned criteria surrounding PAY-T communities which have

historically been used for comparison have been added. A list comprised of thirteen

municipalities, six of which meet the above set of criteria (including Shrewsbury) and

seven of which have been added as historical and geographic comparisons can be found

in Table 1, Comparable Communities, located below.

Table 1: Comparable Communities

Households

Municipality Population EQV** PAY-T Start Date

Served*

Attleboro 44,284 14,094 $4,710,804,300 7/1/2005

Clinton 13,805 4,346 $1,385,425,600 1/1/1989

Dartmouth 33,511 10,040 $5,885,151,300 10/1/2007

Gloucester 29,781 12,500 $6,746,082,000 9/17/1990

Grafton 18,540 4,650 $2,596,289,300 7/1/2009

Marshfield 25,709 9,388 $5,107,817,200 7/9/2007

Natick 33,006 10,525 $7,703,653,670 7/1/2003

Northborough 15,042 4,890 $2,982,076,900 1/1/2002

Shrewsbury 35,608 10,140 $6,091,353,800 8/4/2008

Sutton 9,272 1,150 $1,481,010,900 7/1/2006

Upton 7,725 2,301 $1,214,624,300 1/25/1999

West Boylston 7,894 2,458 $973,854,400 7/1/2009

Worcester 184,815 52,000 $13,336,462,800 11/29/1993

*Data for Trash households Served from PAY-T programs was gathered from Mass EEA

database. 9

**Equalized Values are for FY2020 made available through the Division of Local Services 10

8 Mertens, Donna, M. & Wilson, Amy T. Program Evaluation Theory and Practice. New York: The Guilford Press:

2012. Page 427

9 MassDEP, Existing PAY-T/SMART Programs. https://www.mass.gov/lists/pay-as-you-throw-paytsave-money-

and-reduce-trash-smart

10 Municipal Databank (Data Analytics) including Cherry Sheets, DLS. https://www.mass.gov/service-

details/socioeconomic-data

Town of Shrewsbury – PAY-T Fee Analysis 11COMPARABLE PRIVATE RESIDENTIAL SERVICE

Annual cost to provide residential collection on par with the service provided through the

Town’s PAY-T program was gathered through conversations or online quotations from

the following vendors: Casella Waste Systems, Republic Services, and Waste

Management. Annual collection rates from the vendors have been reported as an

aggregated range.

EVALUATION LIMITATIONS

It is important to be aware of the inherent limitations of each evaluation. Quantitatively,

the analysis is subject to selection bias. The metrics utilized for the comparable

communities should be reviewed and agreed upon by key stakeholders while also

recognizing the difficulty of controlling for all contextual variables.

Following this analysis and review with the key players of the stakeholder matrix, it is

imperative to review the findings with the remaining stakeholders to ensure all the

nuances and complexities of the Town are understood and properly represented.

PROPOSED MEASUREMENTS

It is important to select methods most appropriate in answering the evaluation questions.

The following indicators and performance measures have been selected for their

feasibility in answering the evaluation questions and their availability due to being pre-

determined municipal metrics (either for the Town of Shrewsbury or Comparable

Communities). Municipalities implementing PAY-T/SMART programs are required to

track solid waste expenditures and metrics and these figures are made readily available

through MassDEP.

1. Shrewsbury’s annual Tax Levy Impact

2. Shrewsbury’s Solid Waste Enterprise – Out Year Expenditure Estimate

3. Shrewsbury’s Annual PAY-T program receipts

4. Population growth throughout tenure of program (DOR)

5. PAY-T Bag Pricing (small/large) Mass DEP, existing PAY-T municipalities

6. Mass DOR Cherry sheet databanks (single-family tax bill, assessed value, and

population)

Town of Shrewsbury – PAY-T Fee Analysis 12ANALYSIS AND INTERPRETATION

SUMMARY

To effectively meet out-year expenditures and the changing recycling market we

recommend the setting of PAY-T Fees as the following for FY 21 – FY 25.

% Proposed Proposed Current Current Variance Variance

Increase $/bag $/roll $/bag $/roll $/bag $/roll

Small 47.00% $1.10 $5.50 $0.75 $3.75 $0.35 $1.75

Large 50.00% $2.25 $11.25 $1.50 $7.50 $0.75 $3.75

Recycling Bins 36.36% $15.00 - $11.00 - $4.00 -

Bulk waste 20.00% $12.00 - $10.00 - $2.00 -

When averaged, the household impact for PAY-T bags would be an increase of $0.7885

per week or $41.00 per year. Using the average household consumption figures a

household currently can expect to pay $83.46 in PAY-T bags. The proposed bag fees

would increase this annual amount to $124.46/year. While the recommended PAY-T

Fees are greater than the selected Comparable Community averages of $1.03 and $1.95

they are in line with $1.25 and $2.21 average value of the 59 PAY-T of communities

providing curbside collection across the commonwealth. For the full list of Communities

please see both the PAY-T Community Map and Database provided by MassDEP located

in the Appendix. These differences may be best explained by the nuances and the

designed funding models of each program; for example the use of an annual fee, ranging

from $80-315, in addition to PAY-T bag fees to supplement program costs.

Another valuable point of interest is the proposed fee structure impact compared to

private residential service on an average household level per year. The cost of comparable

private residential collection of refuse and recyclable materials would range from $442 -

$576 per year. The average private service at $515 per year is approximately 4.1 times

greater than the average household PAY-T bag usage at $124.46 per year. Stated

alternately, $515 per year equates to disposal of 22.25 LARGE bags per week.

It should be noted that the out-year expenditures and the revenues set to meet these

requirements attributed Indirect Costs in accordance Massachusetts General Laws

Chapter 44 Section 53 F½ and the budgeting approaches used for the Water, Sewer, and

Stormwater Enterprises in the Fiscal Year 20 budget. These indirect costs equate to an

average of $62,305 per year for the enterprise or approximately $0.09 of the bag increase

for both SMALL and LARGE bags. In most cases, these indirect costs are not new charges,

but existing costs in the enterprise service provision. The goal is to provide a more

transparent and accurate accounting of the costs to provide the service to the Town.

In the future, the Town may want to consider hiring a Sustainability/Recycling

Coordinate whose salary would be allocated as a direct charge to the enterprise. A

dedicated employee could provide heightened services and messaging for the community.

It is feasible to receive grant funding for the initial establishment of such a position

through MassDEP.

The following pages 14 – 27 provide a comprehensive walk through of the analysis and

approaches used to determine the FY 21 – FY 25 PAY-T Bag Fee recommendation.

Town of Shrewsbury – PAY-T Fee Analysis 13You can also read