Time Dependencies Between Equity Options Implied Volatility Surfaces and Stock Loans

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Degree Project in Financial Mathematics

Second Cycle, 30 Credits

Time Dependencies Between Equity

Options Implied Volatility Surfaces

and Stock Loans

A Forecast Analysis with Recurrent Neural Networks and

Multivariate Time Series

SIMON WAHLBERG

Stockholm, Sweden 2022

ABSTRACT

Abstract

Synthetic short positions constructed by equity options and stock loan short sells are

linked by arbitrage. This thesis analyses the link by considering the implied volatility

surface (IVS) at 80%, 100%, and 120% moneyness, and stock loan variables such as

benchmark rate (rt ), utilization, short interest, and transaction trends to inspect time-

dependent structures between the two assets. By applying multiple multivariate time-

series analyses in terms of vector autoregression (VAR) and the recurrent neural networks

long short-term memory (LSTM) and gated recurrent units (GRU) with a sliding window

methodology. This thesis discovers linear and complex relationships between the IVS

and stock loan data. The three-day-ahead out-of-sample LSTM forecast of IV at 80%

moneyness improved by including lagged values of rt and yielded 19.6% MAPE and

forecasted correct direction 81.1% of samples. The corresponding 100% moneyness GRU

forecast was also improved by including stock loan data, at 10.8% MAPE and correct

directions for 60.0% of samples. The 120% moneyness VAR forecast did not improve

with stock loan data at 26.5% MAPE and correct directions for 66.2% samples. The

one-month-ahead rt VAR forecast improved by including a lagged IVS, at 25.5% MAPE

and 63.6% correct directions. The presented data was optimal for each target variable,

showing that the application of LSTM and GRU was justified. These results indicate

that considering stock loan data when forecasting IVS for 80% and 100% moneyness is

advised to gain exploitable insights for short-term positions. They are further validated

since the different models yielded parallel inferences. Similar analysis with other equity

is advised to gain insights into the relationship and improve such forecasts.

Keywords

Recurrent neural networks, RNN, long short-term memory, LSTM, gated recurrent units,

GRU, vector autoregression, VAR, implied volatility surface, stock loan, equity options,

multivariate time-series analysis, financial mathematics.

ii

SAMMANFATTNING

Sammanfattning

Syntetiska kortpositioner konstruerade av aktieoptioner och blankning med aktielån är

kopplade med arbitrage. Denna tes analyserar kopplingen genom att överväga den

implicerade volatilitetsytan vid 80%, 100% och 120% moneyness och aktielånvariabler

såsom referensränta (rt ), låneutnyttjande, låneintresse, och transaktionstrender för att

granska tidsberoende strukturer mellan de två tillgångarna. Genom att tillämpa multi-

pel multidimensionell tidsserieanalys såsom vektorautoregression (VAR) och de rekursiva

neurala nätverken long short-term memory (LSTM) och gated recurrent units (GRU).

Tesen upptäcker linjära och komplexa samband mellan implicerade volatilitetsytor och

aktielånedata. Tre dagars LSTM-prognos av implicerade volatiliteten vid 80% money-

ness förbättrades genom att inkludera fördröjda värden av rt och gav 19, 6% MAPE

och prognostiserade korrekt riktning för 81, 1% av prover. Motsvarande 100% money-

ness GRU-prognos förbättrades också genom att inkludera aktielånedata, resulterande

i 10, 8% MAPE och korrekt riktning för 60, 0% av prover. VAR-prognosen för 120%

moneyness förbättrades inte med alternativa data på 26, 5% MAPE och korrekt rik-

tning för 66, 2% av prover. En månads VAR-prognos för rt förbättrades genom att

inkludera en fördröjd implicerad volatilitetsyta, resulterande i 25, 5% MAPE och 63, 6%

korrekta riktningar. Presenterad statistik var optimala för dessa variabler, vilket visar

att tillämpningen av LSTM och GRU var motiverad. Därav rekommenderas det att

inkludera aktielånedata för prognostisering av implicerade volatilitetsytor för 80% och

100% moneyness, speciellt för kortsiktiga positioner. Resultaten valideras ytterligare

eftersom de olika modellerna gav dylika slutsatser. Liknande analys med andra aktier

är rekommenderat för att få insikter i förhållandet och förbättra sådana prognoser.

Nyckelord

Rekursiva neurala nätverk, LSTM, GRU, VAR, implicerade volatilitetsytor, aktielån,

aktieoptioner, multidimensionell tidsserieanalys, finansiell matematik.

iii

ACKNOWLEDGEMENTS

Acknowledgements

I want to thank SEB Equities, especially Jonas Andersson and Jonne Viitanen for

your support with data gathering, insights on financial markets, and machine learn-

ing throughout this thesis.

I would also like to thank Boualem Djehiche for your helpful and knowledgeable in-

puts. Also Camilla Landén who further improved this thesis by conducting adequate

and informative seminars.

iv

CONTENTS

Contents

1 Introduction 1

1.1 European Equity Options . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Stock Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.3 The Link . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.4 Research Questions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

1.5 Summary of Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

1.6 Outline . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2 Mathematical Background 8

2.1 Black & Scholes Market Model . . . . . . . . . . . . . . . . . . . . . . . . 8

2.2 Accuracy Measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.3 VAR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.4 LSTM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2.5 GRU . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.6 Dummy Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3 Method 17

3.1 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

3.2 Stock Category . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3.3 Data Normalization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3.4 Granger Causality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3.5 Johansen’s Cointegration Test . . . . . . . . . . . . . . . . . . . . . . . . . 20

3.6 Augmented Dickey-Fuller . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

3.7 Lag Optimization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

3.8 Forecast Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

3.9 Feature Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

3.10 Hyperparameter Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

v

CONTENTS

4 Results 24

4.1 Feature Selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

4.2 Forecast Errors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.3 Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

4.4 Variable Influence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

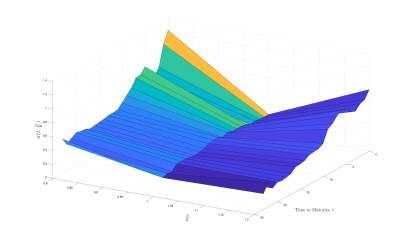

4.5 Implied Volatility Surface . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

5 Discussion 31

5.1 Model Evaluation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

5.2 The Relationship Seen From RMSE . . . . . . . . . . . . . . . . . . . . . 33

5.3 Arbitrage and Linear Dependence . . . . . . . . . . . . . . . . . . . . . . . 35

5.4 Using the Forecasted IVS . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

5.5 Future Work . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

6 Conclusion 39

References 41

A Put-Call Parity 43

B Graphs and Tables 44

vi

LIST OF FIGURES

List of Figures

1.1 Payoff functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

2.1 IVS example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.2 LSTM architecture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

2.3 GRU architecture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.1 Autocorrelation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

4.1 IV out-of-sample forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

4.2 rt out-of-sample forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

4.3 IVS forecast . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

B.1 Granger causality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

B.2 Feature selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

B.3 GRU forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

B.4 LSTM forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

B.5 VAR forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

vii

LIST OF TABLES

List of Tables

3.1 Raw data set . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3.2 Normalized data set . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3.3 Granger causality, three stocks . . . . . . . . . . . . . . . . . . . . . . . . 21

3.4 Johansen’s cointegration test . . . . . . . . . . . . . . . . . . . . . . . . . 21

3.5 Lag evaluation for VAR . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

4.1 Feature selection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4.2 Forecast errors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

4.3 IVS: Granger and feature selection . . . . . . . . . . . . . . . . . . . . . . 29

4.4 rt : Granger and feature selection . . . . . . . . . . . . . . . . . . . . . . . 30

B.1 Chosen hyperparameters . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

B.2 Augmented Dickey-Fuller test . . . . . . . . . . . . . . . . . . . . . . . . . 50

B.3 Complete list of forecast errors . . . . . . . . . . . . . . . . . . . . . . . . 51

viii

CHAPTER 1. INTRODUCTION

Chapter 1

Introduction

Recurrent neural networks (RNN), such as long short-term memory (LSTM) and gated

recurrent units (GRU) have been successfully applied to financial markets in forecast-

ing and contextualizing complex structures (Bernales and Guidolin, 2014), (Fischer and

Krauss, 2018), (Hamayel and Owda, 2021). Option pricing and its different methodolo-

gies have been thoroughly studied, including forecasting these. One important variable

is namely the implied volatility surface (IVS) and its evidential impact on option pricing

in the Black and Scholes market model (Goncalves and Guidolin, 2006), (Audrino and

Colangelo, 2010). Some researchers have included alternative data, such as news feeds in

their implied volatility (IV) forecast and have resulted in more accurate forecasts (Xiong,

Nichols, and Shen, 2015), (Gu et al., 2020). This thesis will continue the exploration

of alternative data in the form of stock loan quantities, and cover both implications.

This will be done through applications of multivariate time-series analysis, specifically

modeled with vector autoregression (VAR), to gain statistically relevant insights into

this relationship. Further application of LSTM and GRU will be conducted in an at-

tempt to improve the VAR forecasts and analyze if similar inferences can be drawn from

these. Equity options and their related stock loan alternatives are bound by arbitrage

(Cocquemas, 2017), which can be shown by constructing alternative portfolios, with

similar or even equal payoffs. This could imply the relationship in question, which will

be quantitatively analyzed throughout this thesis.

1.1 European Equity Options

A European equity call or put option is the right to buy or sell certain underlying equity

on a specified date on a long position. Conversely, for the short holder, it is the obligation

11.1. EUROPEAN EQUITY OPTIONS CHAPTER 1. INTRODUCTION

to sell or buy the underlying equity on the specified date. A European option may only

be exercised on the maturity date. The famous Black and Scholes market model is

assumed for this thesis. The put-call parity holds if and only if the implied volatilities

σCall (t, St /K) = σP ut (t, St /K), (1.1)

which is proven in Appendix A, this is however only true in theory, these may differ

empirically. Equation 1.1 confirms a one-to-one ratio between the IVS for a call and

put option. The standard Black and Scholes model is thus extended to handle an IVS,

depending on time and strike. This is important for this thesis since IV data is extracted

from three strikes, out of the money (OTM), at the money (ATM), and in the money

(ITM), specifically for 80%, 100%, and 120% moneyness. Furthermore, the options con-

sidered have closest time to maturity, that is, if an option reaches maturity it is replaced

by the next closest to maturity option, and so forth.

A rudimentary example of short selling is possible to construct from both calls and

puts. Namely, the long holder of a put is not obliged to possess the underlying stock,

but may still sell it at a future date at a fixed price. Likewise, for the short holder of a

call, the difference is the obligation to sell the stock at maturity. In terms of arbitrage

theory, there is of course a premium to be paid by the long holder, which in this market

setting is determined by Black and Scholes partial differential equation (PDE) and its

governing Itô diffusion’s, presented in subsection 2.1. IV is an important variable in op-

tion pricing, the parameter is the market’s expectation of the volatility for the underlying

stock until maturity (Björk, 2009). An increase in σ(t, St /K) and all other parameters

equal will imply a premium increase, conversely, if σ(t, St /K) decreases, the premium

will decrease. Being able to forecast IV more accurately is, trivially, compelling for any

market participant.

Goncalves and Guidolin (2006) considered an IVS, specifically the one generated by daily

closing prices from the S&P 500 index options. Their framework consists of the empiri-

cally proven assumption that the surface is time and strike varying (Christoffersen and

Jacobs, 2004), (Dumas, Fleming, and Whaley, 1998), with predictable patterns. Their

approach consists of applying vector autoregression, resulting in more accurate forecasts

and significant returns. This thesis will partly build on their framework, however with

58 single equity options on the Swedish market instead of an index. It will also include

applications of RNN in an attempt to further improve the predictive capabilities. Au-

21.2. STOCK LOANS CHAPTER 1. INTRODUCTION

drino and Colangelo (2010) further improved Goncalves and Guidolins work by applying

semi-parametric forecasts using regression trees and a boosting algorithm. Their results

indicate better forecast accuracy, robustness to information loss, and time series discon-

tinuities, also advising that a machine learning approach can be fruitful. Bernales and

Guidolin (2014) finds similar predictability patterns as Goncalves and Guidolin in eq-

uity options, they propose a VARX model to predict the implied volatility surface which

yields abnormal returns, however not resulting in arbitrage opportunities since they are

lowered by transaction costs (Bernales and Guidolin, 2014). They propose further inves-

tigation to analyze possible relationships between equity options and their underlying

equities. Medvedev and Wang (2022) compared traditional models, such as VAR with

LSTM and convolutional LSTM in forecasting S&P 500 index option IVS. Finding that

the two RNNs outperformed the traditional models, the convolutional LSTM was the

most accurate. They mention that hyperparameter tuning such as grid search (which is

applied in this thesis) could make LSTM competitive against convolutional LSTM. It is

noteworthy that they did not use alternative data, only options data. Similar studies

include the application of machine learning algorithms, such as naive Bayes and adap-

tive boosting to predict the direction of the fear index (VIX) compared to standard

economical models (S. D. Vrontos, Galakis, and I. D. Vrontos, 2021). They found that

the application of machine learning yielded better forecasts.

1.2 Stock Loans

Stock lending is a subset of security loans, including two parts, lender and borrower.

An elemental case is that the borrower borrows stocks from the lender, and are then

instantly sold (short sell). The lender usually receives an equivalent value of collateral

from the borrower to compensate for the counterparty risk, in case the borrower de-

faults, the lender keeps the collateral. In exchange for borrowing stocks, the borrower is

obliged to pay an interest rate, proportional to the underlying stocks value, denoted rt .

The floating part may increase drastically if the underlying asset price increases, which

may be a short squeeze market reaction. When the stocks are returned to the lender,

collateral is returned to the borrower (ISLA, 2010), stock lending can be utilized for

prospecting and hedging purposes. As mentioned in subsection 1.1, a short holder of a

call option is not obliged to possess the underlying stock, if the long holder chooses to

exercise, the short holder is obliged to sell the underlying stocks to the strike price. If

the short holder sees for example, a prospecting opportunity, it may instead be valid to

borrow stocks to sell.

31.2. STOCK LOANS CHAPTER 1. INTRODUCTION

The nature of this asset is quite risky in the prospecting sense, if the stocks value

increases drastically the borrower is inclined to either pay an expensive rate and col-

lateral or buy the stock at a much higher price. This was the case when many market

participants had short positions in GameStop in 2021, this was established by other

market participants who took long positions. Subsequently, large investors also took

long positions due to the market’s virtual bull scenario. Short holders urgently tried to

buy back their short positions, however, since there were many short positions, the price

iteratively increased. Further examples can be found in Volkswagen 2008 and KaloBios

2015.

Short interest is the percentage of stocks that are sold short, which is a natural in-

dication of the market’s bear scenario anticipation. A relative increase in short interest

implies that further market participants anticipate the stock to decline in value. Con-

versely, if the short interest decreases it implies that the market expects bull scenarios.

This statistic was very high in the GameStop example, resulting in a short squeeze.

Utilization is the percentage of loaned stocks relative to lendable stocks, similar to short

interest because it quantifies the market’s short interest. However, it might not be as

indicative on its own due to the dependency on short quantity which may differ vastly

between stocks. Days to cover inform the number of days in which companies short sold

stocks takes until covered, that is, bought back from the market. Many days to cover

indicate an increased risk for short squeezes.

Xia and Zhou (2007) considered the instrument as an American option in the Black

and Scholes market model with a time-varying strike. Chen, Xu, and Zhu (2015) val-

uated stock loans based on a stochastic interest rate framework, applying the model

proposed by Xia and Zhou. It is however misrepresentative of modern stock loans due

to several reasons: It is assumed that a loan is defaultable so that the lender keeps the

principal. If the stock price declines the lender will cancel the loan and keep princi-

pal. In contrast to increased stock price, the lender will get the stocks back and return

principal, hence creating arbitrage opportunities. It is unfortunate since the Black and

Scholes model can be easily applied to this framework. Collateral is instead calculated

each day to cover mark to market movements to generate margin calls, default is not a

real possibility for lenders. Options theory has been further applied to price long-term

stock loans, Kashyap (2016) applies exotic options theory and assumes that a long-

term security loan has optionality due to the availability of shares being modeled as a

41.3. THE LINK CHAPTER 1. INTRODUCTION

Geometric-Brownian-Motion. Specifically, Kashyap applies rainbow and basket binary

barrier American options to construct a pricing framework. Kashyap runs numerical

simulations and confirms that it is a practical and efficient tool. His framework is more

realistic in the modern stock loan setting than the previous articles. However, his model

will not be used in this study, it merely acts as a complementary framework.

1.3 The Link

Cocquemas (2017) examined the possibility of linking the security loan market with the

options market. He constructed a synthetic short position by buying a put and selling a

call, with equal strikes, replicating a stock loan short sell, then extracting IV and implied

lending fee from the trade. These two term structures were shown to be, statistically

significantly positively related by applying panel regression, with and without time fixed

effects. However, he concluded that the loan fee prediction was not especially improved

by IV, just slightly. It is still noteworthy that a relationship is existent between these

variables. This thesis will further investigate this relationship, and only consider Euro-

pean options, however with a dissimilar methodology. Cocquemas only considers ATM

options, whereas this thesis considers OTM -, ATM -, and ITM options. Furthermore,

panel regression will not be applied, instead, VAR, LSTM, and GRU.

Cocquemas study is quite illustrative in the context of linking the two assets by replicat-

ing a short position through options. There are many strategies to yield similar payoff

functions. Consider the very simplified payoff of a short sell, averting the margin costs,

transaction fees, and rate, presented in figure 1.1a. It is essentially equal to the payoff

function of a synthetic short sell. As Cocquemas infer, the two portfolios are linked by

arbitrage, and should therefore obtain similar transactional costs. That is, the premium,

margins, rate, and fees should have a theoretical relationship, at least in the Black and

Scholes market model which, by definition, is arbitrage-free (Björk, 2009) (which any

reasonable market model should be). Generally, call options OTM are cheaper than put

options OTM (this can be seen in the IVS presented in figure 2.1, where the skew is

apparent between 80%- and 120% moneyness). If a portfolio manager is bearish, it is

reasonable to prospect on an OTM put option by selling two OTM call options, which

in this example yields an equal premium. That is, financing the downside by selling the

upside. It does however not yield as much leverage compared to the short- or synthetic

short position. This strategy is known as risk reversal, which hedges some unwanted

fluctuations in the stock price, but somewhat mitigates eventual payoffs, which can be

51.4. RESEARCH QUESTIONS CHAPTER 1. INTRODUCTION

(a) Short sell payoff (b) Payoff function for a (c) Portfolio payoff with a

function, the graph does not synthetic short position, the long put written on K = 80

consider transaction fees, portfolio consists of a long and two short calls written

rates, or margins, only the put and a short call written on K = 120, equal tenor, the

very simplified asset payoff. on equal strike and tenor. calls financed the put.

Figure 1.1: Simplified payoff functions for three portfolios.

seen by inspecting figure 1.1c. With similar arguments as for synthetic short positions,

this might indicate further relations with OTM and ITM IV and stock loan rates.

1.4 Research Questions

This thesis will attempt to answer the following questions.

• Is it possible to infer a predictive, time-dependent relationship between equity

options IVS and their related stock loan rate rt by applying multivariate time-

series analysis and RNNs?

• Is it possible to accurately forecast the implied volatility surface and loan rate

through the application of VAR? Is it further possible to improve these forecasts

by applying LSTM and GRU?

• Will LSTM and GRU give similar inferences as VAR?

1.5 Summary of Findings

This thesis discovers linear and complex relationships between the IVS and stock loan

data. The linear dependencies are prominent for some stocks and improve the VAR

forecast accuracy for both implications, that is, for IVS and loan rate predictions. These

forecasts are further improved by applying LSTM and GRU, the complex relationships

are prominent by applying feature selection where IV for 80% and 100% moneyness

is enhanced by including stock loan data. It is not the case for 120% moneyness IV

and the loan rate, it is shown to be difficult to forecast rt due to much noise. The

61.6. OUTLINE CHAPTER 1. INTRODUCTION

application of LSTM and GRU is shown to be beneficial to gain further insights into

this relationship and also improve forecasts. The inferences drawn from these models are

further validated by comparison of the different models. This thesis contributes to the

research subject by applying new methods for studying this relationship, especially for

80%- and 120% moneyness which has not been previously researched (to the author’s

limited knowledge), to gain forecasting accuracy and link these assets. The forecast

instrument is furthermore shown to be prominent in following trends and directional

movements which can be exploited for short-term positions.

1.6 Outline

Chapter 2 presents the mathematical background and some previously researched appli-

cations, and chapter 3 presents the methodology following the mathematical background.

Chapter 4 presents results such as forecast errors, feature importance, and forecast plots

for the IVS and rt . An analysis and discussion is presented in chapter 5 which is sum-

marized in chapter 6.

7CHAPTER 2. MATHEMATICAL BACKGROUND

Chapter 2

Mathematical Background

2.1 Black & Scholes Market Model

The continuous, arbitrage-free (Björk, 2009) market model developed by Fischer Black,

Myron Scholes, and Robert C. Merton follows from the two asset Itô diffusion

dSt = rSt dt + σSt dWtQ ,

(2.1)

dBt = rBt dt,

where St is the spot price for a risky asset and Bt a risk-free asset. Further assuming

a constant, risk-free interest rate r, and where dWtQ is a Wiener process under the

risk-neutral (martingale) measure Q. σ refers to the implied volatility and is assumed

constant in standard Black and Scholes. The price of a European option at time t is

derived from the Black-Scholes equation

∂V (t, x) 1 2 2 ∂ 2 V (t, x) ∂V (t, x)

+ σ x 2

+ rx − rV (t, x) = 0,

∂t 2 ∂x ∂x (2.2)

V (T, x) = Φ(x),

where Φ(x) is the value process and V (T, x) the price at maturity. σ is determined by

observing the price of an option and invert these equations. However, σ has been shown

to be non-constant (Christoffersen and Jacobs, 2004), (Dumas, Fleming, and Whaley,

1998), and varies with observed parameters, it is customary to plot it as a function of

t and St /K which is presented in figure 2.1, considering a call option. At maturity, IV

tends to increase, it also illustrates the IV smile, that is, IV is lowest for ATM options

and increases in both directions. However, it is more reminiscent of a skew, where IV

82.2. ACCURACY MEASURES CHAPTER 2. MATHEMATICAL BACKGROUND

Figure 2.1: Smoothed IVS for an option with one month to maturity.

at 80% moneyness is larger than at 120% moneyness. It is further apparent that the

volatility increases as maturity approaches. This thesis will present another method of

approximating σ(t, St /K), namely by multivariate time-series analysis by applying VAR,

LSTM, and GRU.

2.2 Accuracy Measures

Mean square error is defined as

n

1X

MSE = (yi − ŷi )2 (2.3)

n

i=1

where ŷi is the predicted variable. Root mean squared error is simply

√

RMSE = MSE. (2.4)

92.3. VAR CHAPTER 2. MATHEMATICAL BACKGROUND

Another accuracy measure to be used is the percentage of correct directional forecast,

n

1X

PCDF = 1i,PCDF

n

i=1

1 if yi+1yi−yi < −c and ŷi+1yi−yi < −c

(2.5)

1 if yi+1 −yi > c and ŷi+1 −yi > c

1i,PCDF = yi

yi+1 −yi

yi

ŷi+1 −yi

1 if | yi | ≤ c and | yi | ≤ c

0 else,

where c = 0.1%. Also, mean absolute percentage error

n

100 X yi − ŷi

MAPE = | |. (2.6)

n yi

i=1

2.3 VAR

VAR is a multivariate time-series model, assuming a linear relationship between the

endogenous variables y t and their predecessors up to a certain lag p. A VAR(p) model

is defined as

p

X

y t = φ0 + Φi y t−i + εt , (2.7)

i=1

where φ0 is the m-variate intercept, Φi is the m × m variate coefficient matrix for lag

i, and εt ∼ N (0, Σε ) is m-variate white noise, it is assumed that cov(εt , εs ) = 0 for t ̸=

s. By implementing the following compact form of equation 2.7,

Y = ϕZ + ϵ (2.8)

where Y := (y1 , . . . , y T ), ϕ := (φ0 , Φ1 , . . . , Φp ), Z t := (1, y t , . . . , y t−p+1 )T ,

Z := (Z 0 , . . . , Z T −1 ), ϵ = (ε1 , . . . , εT ), it can be proven that the least square estimator

of ϕ is

ϕ̂ = ϕ + ϵZ T (ZZ T )−1 (2.9)

(Lütkepohl, 2005). It is further assumed that the processes y t are stationary, that is

E[y t ] = µ ∀t ,

(2.10)

E[(y t − µ)(y t−h − µ)T ] = Γy (h) = Γy (−h)T ∀t , h = 0, 1, 2 . . . .

102.3. VAR CHAPTER 2. MATHEMATICAL BACKGROUND

Where the first condition means that y t has a finite and equal mean vector for all times,

and the second that autocovariance does not depend on t but only on the difference in

periods h. The time-series data for volatility, rates, and trade prices are however usually

not stationary. To test this, an augmented Dickey-Fuller test is necessary, which is a

unit root test, conducted for each series (y)it∈(p,T ) , i = 1, 2, . . . , m, where

yti = α + βt + γyt−1

i i

+ γ1 ∆yt−1 + · · · + γp ∆yt−p + εit . (2.11)

The model imposes that the disturbances are white noise if α = 0 and β = 0. The

statistic is defined as

T (γ̂ − 1)

DFγ = , (2.12)

1 − γ̂1 . . . γ̂p

where γ̂ is the OLS estimator of γ and T is the time series sample size. If DFγ is less

than a critical value with regards to the t-distribution then the null hypothesis of γ = 0

is rejected, that is, no unit root is present and the time-series can be regarded as sta-

tionary (Greene, 2012). If not, first-order differences are applied to the series, this is

iterated until DFγ is less than the critical value.

Granger causality is a test to assess bivariate relationships between time series, specifi-

j

cally to explore if yt−τ cause yti for i ̸= j and τ = 1, 2, . . . , p. In probabilistic terms,

j

P(yti ∈ A|I(t − 1)) ̸= P(yti ∈ A|yt−τ ∈

/ I(t − 1)), (2.13)

that is, the probability of ytj being in set A given information of everything that has

happened until that point is not equal to the probability of ytj being in set A given

j

information of everything that has happened excluding information generated by yt−τ .

j

If equation 2.13 holds, it is said that yt−τ Granger causes yti (Greene, 2012). Numerically,

the statistic boils down to the VAR(p) models

p p

(1) (1) (2)

X X

yt = Φ11,i yt−i + Φ12,i yt−i + ε1,t ,

i=1 i=1

p p (2.14)

(2) (1) (2)

X X

yt = Φ21,i yt−i + Φ22,i yt−i + ε2,t ,

i=1 i=1

if the variance of ε1,t or ε2,t is reduced by including lagged values of y (2) or y (1) respec-

tively, then y (2) Granger causes y (1) and conversely, with confidence level α (Geweke,

1982).

112.4. LSTM CHAPTER 2. MATHEMATICAL BACKGROUND

Johansen’s cointegration test is a method to further assess relationships between multiple

time series, in contrast to the Granger test. For a detailed explanation of the method,

see Lütkepohl (2005).

2.4 LSTM

LSTM was discovered by Hochreiter and Schmidhuber which is a permutation of RNN.

Vanilla RNN suffers from exploding and vanishing gradients, making them difficult to

train. Instead, the LSTM algorithm has a constant error carousel to normalize gradients

by using shortcut connections (Ushiku, 2021). This enables long-term dependencies

which could not be considered before, more than 1000 discrete time steps to be specific

(Hochreiter and Schmidhuber, 1997). That is, being able to store relevant data for

substantially longer periods than RNN to contextualize input data. Each cell has several

gates, a forget gate, which is described as

" #

xt

ft = ς(Wf + bf ), (2.15)

ht−1

1

at time t. Where ς(x) = 1+e−x

is the sigmoid function, Wf a weight matrix, xt is the

current input vector with dimension d, ht−1 is the previous short term memory and bf

a bias vector. An input gate

" #

xt

int = ς(Win + bin ), (2.16)

ht−1

with similar notations as before. To decide what new information should be stored, int

is multiplied with new possible values

" #

xt

c̃t = tanh (Wc + bc ). (2.17)

ht−1

ex −e−x

Where tanh(x) = ex +e−x

is the hyperbolic tangent function. Then, the next cell state is

determined as

ct = ft ⊙ ct−1 + int ⊙ c̃t . (2.18)

122.4. LSTM CHAPTER 2. MATHEMATICAL BACKGROUND

Where ⊙ denotes the Hadamard product. Finally, an output gate

" #

xt

ot = ς(Wo + bo ) (2.19)

ht−1

is considered, which produces the next short-term memory as

ht = ot ⊙ tanh(ct ). (2.20)

The architecture of the algorithm is presented in figure 2.2.

This algorithm was applied to financial data such as stock prices and volatility by Fischer

and Krauss (2018). Specifically, they compared daily returns for S&P 500 stocks based on

LSTM, logistic regression, random forest classification, and standard deep nests. Their

study showed that a single input LSTM network with a sliding window methodology

can find patterns and contextualize data which is usually a manual constriction when

modeling financial time series data. It is also capable of extracting meaningful features

from noisy financial data. Their study shows statistically, and economically significant

returns, 0.46 % before transaction costs. Their LSTM network outperforms the bench-

mark algorithms (Fischer and Krauss, 2018), this return is based on a trading strategy

to rank stocks based on the classification of expected performance outcomes. However,

it is noteworthy that LSTM outperformed the general market from 1992 to 2009, from

2010 the market seems to have been accustomed to the application, hence the return

was worse than prior but still significant.

Lin et al. (2021) studied the accuracy improvement by applying Complete Ensemble

Empirical Mode Decomposition with Adaptive Noise (CEEMDAN) to LSTM. Ordi-

nary EMD is used to reduce noise in data, Lin et al. used it on financial time-series

data, specifically S&P500 and CSI300 prices. They compare this algorithm to support

vector machines, Elman networks, and wavelet neural networks. It is concluded that

CEEMDAN-LSTM outperforms the compared algorithms and yields accurate out-of-

sample forecasts. This thesis will however not use EMD or CEEMDAN, but rather

acknowledge the possible fruitfulness of applying these to the presented RNNs.

Research conducted by Xiong, Nichols, and Shen (2015) considered S&P 500 volatil-

ity forecasting in terms of alternative data. Specifically with regards to Google domestic

trends, in the context of word searches somewhat related to the index. Compared to

132.5. GRU CHAPTER 2. MATHEMATICAL BACKGROUND

linear Ridge/Lasso and autoregressive GARCH, LSTM showed significantly better ac-

curacy in terms of RMSE and MAPE. Their results are promising in the sense that deep

learning networks, such as LSTM with alternative data, can more accurately predict

market behavior.

Figure 2.2: Architecture of an LSTM at a discrete time step t with input vector xt , short

term memory ht , cell state ct , forget gate ft , information gate int , possible cell state

c̃t , output gate ot , and Wf , Win , Wc , Wo weights for the corresponding gates. Where

furthermore ς is the sigmoid function, tanh the hyperbolic tangent function and ⊙ the

Hadamard product.

2.5 GRU

GRU is a less complex version of the LSTM algorithm with only two gates (Cho et al.,

2014). Similar to LSTM, it solves the problem of exploding or vanishing gradients by

introducing sigmoid functions to normalize the data processing through gates. First

represented as a reset gate

ret = ς(Wre xt + Ure ht−1 + bre ), (2.21)

142.5. GRU CHAPTER 2. MATHEMATICAL BACKGROUND

ret with similar notations as before (see subsection 2.4), where Wre and Ure are weight

matrices. Secondly as an update gate

upt = ς(Wup xt + Uup ht−1 + bup ). (2.22)

Thereafter, new possible memory contents are introduced

h̃t = tanh(Wh xt + Uh (ret ⊙ ht−1 ) + bh ), (2.23)

and updates the proposed memory unit as

ht = (1 − upt ) ⊙ ht−1 + upt ⊙ h̃t . (2.24)

A trivial limit implies

lim ht → ht−1 , (2.25)

upt →0

the hidden state completely forgets the current input and only remembers the previous

memory state. Conversely, if

lim ht → h̃t (2.26)

upt →1

the hidden state ignores the previous input and only remembers the proposed memory

unit. The network is thus qualified to forget and remember relevant input based on

the learned weights. Noticeable in figure 2.3, and comparatively with figure 2.2, is the

decreased complexity, with only two gates, ret and upt , without a cell state ct .

Similar to Xiong, Nichols, and Shen (2015), Gu et al. (2020), applied GRU on real-

ized volatility data, with alternative data, specifically news feeds. They found that a

GRU, with a single input parameter, and its extension, GRU-AI, with multiple features

and single input, gave more accurate predictive results than the linear time-series models

HAR-RV, and HAR-RV-AI respectively. The model was set up with a sliding window

scheme and evaluated based on four loss functions. Noteworthy is that GRU-AI outper-

formed GRU in terms of those statistics, but only slightly. They further implied that,

trivially, it is easier to infer variable weights and relationships between these in the linear

models, which is applicable to this thesis as well.

Hamayel and Owda (2021), applied LSTM and GRU to predict cryptocurrency prices,

their raw data only covered prices at open, high, low, and close. They found that GRU

performed more accurately than LSTM, but only slightly, both algorithms proved ef-

152.6. DUMMY MODEL CHAPTER 2. MATHEMATICAL BACKGROUND

Figure 2.3: Architecture of a GRU algorithm at a discrete time step t with input vector

xt , memory state ht , reset gate ret , update gate upt , possible memory state h̃t and

weights W , U = [Wre , Wup , Wh ], [Ure , Uup , Uh ]. Where furthermore ⊙ is the Hadamard

product, ς and tanh is the sigmoid and hyperbolic tangent function respectively.

ficient prediction tools. They mention alternative data as a future research extension,

specifically news feeds. Moreover, spot prices are not the subject of this project, how-

ever, it is relevant to mention that both algorithms work well with financial data which

is notoriously noisy and more often than not with high autocorrelation. Thus indicat-

ing that it is highly relevant to apply both algorithms to inspect eventual predictive

differences and variable impact on accuracy metrics.

2.6 Dummy Model

The dummy model is an assumption of constant value from the forecast date. That is

j

yt+1:t+n = ytj , (2.27)

and will serve as a comparison relative to the other three models.

16CHAPTER 3. METHOD

Chapter 3

Method

3.1 Data

The IVS and stock loan data are provided by Bloomberg and Markit respectively, with

data ranging from 2015 to late 2021, specifically defined by t = {0, 1, . . . , n}. The mar-

ket implications created by the Corona pandemic are thus included, which extensively

impacted financial markets and have to be considered when modeling. The data set

includes approximately 58 stocks, abbreviated Sk , on the Swedish market, ranging from

large-cap to small-cap which is an important factor for the liquidity of stock loans and

options to consider in terms of data availability. The IVS σ(t, St /K) for this project is

discretized at 80%, 100%, and 120% moneyness, additionally by only extracting clos-

ing volatility for each day t. The structure can thus be seen as multiple multivariate

time-series, for example

σ(0, 80%) σ(0, 100%) σ(0, 120%) r0

σ(1, 80%) σ(1, 100%) σ(1, 120%) r1

.. .. .. .. (3.1)

. . . .

σ(n, 80%) σ(n, 100%) σ(n, 120%) rn

for each stock Sk={1,2,...,58} . Some of these stocks are missing data for certain days, this

is handled by forward filling, specifically if ytj miss data,

ytj = yt−1

j

. (3.2)

Note that equation 3.1 is a reduced example, the data matrix actually includes all

variables presented in table 3.1.

173.2. STOCK CATEGORY CHAPTER 3. METHOD

Table 3.1: Variables in the data set and their corresponding spaces.

Short loan quantity ∈ N

Available loan quantity ∈ N

Shares outstanding ∈ N

Stock loan transactions ∈ N

Benchmark rate (stock loan rate) ∈ R+

Days to cover ∈ R+

Closing stock price (St ) ∈ R+

σ(t, 80 : 120%) ∈ R+

3.2 Stock Category

The loan rate rt is assumed to have a categorical mandate, in terms of finding stocks

with similar stock loan data and behavior. The definition

GC, if rt < 35bp,

SGroup = Warm, if 35bp ≤ rt < 300bp,

if 300bp ≤ rt ,

Special,

specifies these, where GC abbreviates General Collateral, and bp for basis points. This

says that GC stocks are generally quite cheap to borrow, whereas warm and special

stocks are more expensive due to a higher lending rate. The definition is dynamic, hence

re-evaluated at each time step. It is thus necessary to further specify the stability of the

stocks based on these categories, if a stock is

• GC for more than 90% of the time, it is regarded as GC stable,

• warm for more than 50 % of time, it is regarded as Warm stable,

• special for more than 50 % of time, it is regarded as Special stable.

It is quite rare for a stock to be warm or special stable compared to GC stable in this

data set. This is considered when evaluating LSTM and GRU where three GC stable

stocks will serve as out-of-sample accuracy measures.

3.3 Data Normalization

To reduce training time for the LSTM and GRU models it is necessary to normalize the

data set. Well-used methods such as standardization, or mean and variance scaling are

183.4. GRANGER CAUSALITY CHAPTER 3. METHOD

not applied to the data set, instead, some financial concepts. Specifically, new variables

are defined by self-contained permutations from the raw data set. These are

Short loan quantity

Short interest [%] = ,

Shares outstanding

Short loan quantity

Utilization [%] = ,

Available loan quantity

(3.3)

Stock loan transactions

Transaction trend [%] = ,

Average stock loan transactions 30 days prior

St − St−1

Daily return [%] = .

St−1

The transaction trend will imply a 30-row cut of each stock data set. The normalized

data set used in this thesis is presented in table 3.2. The target variables in question,

Table 3.2: The normalized data set used for the remainder of this thesis.

Short interest

Utilization

Transaction trend

rt

Days to cover

Daily return

σ(t, 80 : 120%)

SGroup

σ(t, 80 : 120%) and rt posses quite high autocorrelation. This is however dependent on

the chosen stock, an example is presented in figure 3.1.

3.4 Granger Causality

In table 3.3, p-values for the bivariate relationship is presented with respect to equation

2.13, with max{τ } = 12. Given a significance level of 0.05, it is possible to either reject

the null hypothesis or not be able to reject it. This test is possible to conduct for

each stock, table 3.3, merely presents three stocks, however, differentiated based on the

categories specified in subsection 3.2. For this data set, about 47 stocks are considered

GC stable, 2 are warm stable, and 2 are special stable. There is some fluctuation inside

193.5. JOHANSEN’S COINTEGRATION TEST CHAPTER 3. METHOD

(a) σ(t, 80%). (b) σ(t, 100%).

(c) σ(t, 120%). (d) rt .

Figure 3.1: Target variable autocorrelation for a GC stable stock. Spikes above the

faded area indicate significant autocorrelation.

the GC category in terms of p-values, which is presented in figure B.1. It is however

possible to conclude that many stocks have a significant Granger causality considering

alternative data. Hence, it is valid to build a VAR model with bivariate relationships

between these variables for some stocks.

3.5 Johansen’s Cointegration Test

It is possible to run the test on each stock and variable, however, only the result for

three category stable stocks with some variables are presented. Whom are: Benchmark

rate, σ(t, 80%), σ(t, 100%), and σ(t, 120%), see table 3.4. It may be inferred that every

time series, except σ(t, 100%) for the warm and GC stable stock, are cointegrated based

on these results, given a significance level of 0.05.

203.6. AUGMENTED DICKEY-FULLER CHAPTER 3. METHOD

Table 3.3: Granger causality for a special, warm, and GC stable stock.

SCategory Target variable rt−τ σ(t − τ, 80%) σ(t − τ, 100%) σ(t − τ, 120%)

Special rt 1.00 0.00 0.00 0.05

σ(t, 80%) 0.00 1.00 0.00 0.00

σ(t, 100%) 0.00 0.00 1.00 0.00

σ(t, 120%) 0.00 0.00 0.00 1.00

Warm rt 1.00 0.25 0.60 0.45

σ(t, 80%) 0.71 1.00 0.00 0.00

σ(t, 100%) 0.15 0.00 1.00 0.00

σ(t, 120%) 0.18 0.03 0.00 1.00

GC rt 1.00 0.28 0.01 0.10

σ(t, 80%) 0.01 1.00 0.00 0.04

σ(t, 100%) 0.18 0.17 1.00 0.00

σ(t, 120%) 0.66 0.00 0.00 1.00

Table 3.4: Johansen’s cointegration test statistic on three category-stable stocks, con-

sidered variables are presented in the left-most column. If the test statistic is below the

given significance level, the time series may be considered cointegrated. This is the case

unless a statistic is indicated by *.

Variable Special stable Warm stable GC stable Significance level (0.05)

rt 208.1 224.2 315.1 40.2

σ(t, 80%) 80.8 94.2 169.3 24.3

σ(t, 100%) 6.7 2.3∗ 0.86∗ 4.1

σ(t, 120%) 27.4 24.8 60.0 12.3

3.6 Augmented Dickey-Fuller

As previously mentioned in subsection 2.3, results from the unit root test (still consid-

ering the three category stable stocks) specified in equation 2.12 are presented in B.2

before and after the first difference. The critical value for a significance level of 0.05 is

-2.87, which DFγ has to be below to regard the time series as stationary. If the null

hypothesis cannot be rejected, a first difference is conducted on the complete data set,

this procedure is repeated until each time series can be regarded as stationary. The

forecasted values are then transformed back to the original scale.

3.7 Lag Optimization

After eventually conducting first-order difference, optimal lag is found based on Akaike-

and Hanna-Quinn information criterion for the VAR model, see Lütkepohl (2005) for

a detailed description of these metrics. The general principle is that AIC and HQI

213.8. FORECAST METHODOLOGY CHAPTER 3. METHOD

close to zero imply more accurate models. That is, a VAR(τ ) model is fitted for each

τ = {1, 2, . . . 12} and evaluated using a training set that includes 80% of the stock

available data. The metrics are presented in table 3.5 for a special, warm, and GC

stable stock respectively. It is easy to see that the optimal lag is seven for the warm

Table 3.5: Optimal lag based on Akaike - and Hanna-Quinn information criterion, small

values indicate more accurate models. The smallest number in each row is indicated by

*. Train size set to 80%, presented figures are based on a special, warm, and GC stable

stock respectively.

Lag AICspecial HQIspecial AICwarm HQIwarm AICGC HQIGC

3 - - - - -59.91 −59.54∗

6 - - −50.20∗ -49.47 −60.13∗ -59.40

7 -18.68 -16.79 −50.20∗ −49.35∗ - -

10 -20.60 −18.17∗ - - - -

12 −20.91∗ -18.00 - - - -

stock. However, since the special and GC stock obtain different lags concerning AIC

and HQI it is necessary to make a conjecture. The lag is thus chosen based on HQI

for special and GC which yields τspecial = 10 and τGC = 3 to reduce input parameters

compared to evaluating with AIC. This lag optimization is only relevant for the VAR

model, another approach involving grid search is applied to determine optimal lag for

GRU and LSTM.

3.8 Forecast Methodology

Conveniently, Keras (Chollet et al., 2015) supports LSTM and GRU layers, a layer

expects an input shape of (samples, time, features). In this project, the second shape

can be interpreted as how many past time steps (τ ) are wanted to make predictions.

Samples can be seen as how many time series of length lag are available, for example,

the number of rows in equation 3.1 divided by lag. The set is subsequently split into a

training and a test sample. Sliding window is further applied to emulate a real setting,

denoting the data set in equation 3.1 by X with t = 0, 1, . . . , n,

inputt = Xt−τ :t ,

(3.4)

outputt = Xt+1:t+days to forecast ,

which is iterated n−(days to forecast) times. Both models have one input layer and a

dense, single output layer.

223.9. FEATURE SELECTION CHAPTER 3. METHOD

3.9 Feature Selection

The variable’s importance is determined by dropping each feature except the target vari-

able and assessing RMSE for each temporal data set. It is repeated iteratively until no

improvements are made. This procedure is done before tuning any other hyperparameter

(except for rt where the lag component is determined based on a broad, single parame-

ter grid search) and repeated for each target variable of importance, that is: rt+1:t+21 ,

σ(t + 1 : t + 3, 80%), σ(t + 1 : t + 3, 100%), and σ(t + 1 : t + 3, 120%). This data

set only includes dates when the market is open, and 21 discrete time steps, therefore,

approximately relates to one month forward in time. Furthermore, they are evaluated

based on average out-of-sample forecast RMSE, calculated over three GC stable stocks.

3.10 Hyperparameter Selection

Grid search is applied on both LSTM and GRU, where the hyperparameters to be

determined are lag (τ ), number of units, and batch size, evaluated with average RMSE

over the three GC stable stocks. See table B.1 in Appendix for chosen values, the network

uses tanh as activation function, 80% train size, and the chosen optimizer is adam.

23CHAPTER 4. RESULTS

Chapter 4

Results

This chapter will present results from feature selection in section 4.1, forecast errors in

4.2, forecast graphs compared to actual values in 4.3, variable influence which summa-

rizes important results in 4.4, and the resulting IVS in 4.5.

4.1 Feature Selection

Figure B.2 indicate a preferable variable selection for the three models. Considering

LSTM and figure B.2a, referring to σ(t, 80%), obtains minimal RMSE by only consider-

ing the volatility surface and the stock loan rate. Figure B.2b, referring to σ(t, 100%),

obtains it by removing days to cover, daily return, σ(t, 80%), and σ(t, 120%). While the

previous target variables seems to enhance accuracy by having more variables, σ(t, 120%)

and rt are conversely worsened by it, which can be seen in figure B.2c and B.2d.

Considering GRU, it is clear that figure B.2e, referring to σ(t, 80%), obtains RMSE

minimum by considering utilization, loan rate, and the volatility surface. Figure B.2f,

referring to σ(t, 100%) obtains it by removing utilization, days to cover, daily return,

dummy variables, and loan rate. Similarly to forecasting σ(t, 120%) and rt with LSTM,

GRU also finds that only considering lagged values of σ(t, 120%) rt yields minimal RMSE.

Finally VAR, where it is apparent that minimal RMSE is reached by removing trans-

action trend and rt considering σ(t, 80%) and figure B.2i. Removing utilization, daily

return and rt for σ(t, 100%) in figure B.2j. σ(t, 120%) in figure B.2k reaches it by only

considering the IVS. Conversely from LSTM and GRU, VAR yields minimal RMSE by

considering the entire data set. Note that the dummy variables are not utilized in the

244.2. FORECAST ERRORS CHAPTER 4. RESULTS

Table 4.1: Selected feature for each target variable in LSTM and GRU-setting respec-

tively. X indicates that a variable is used in the data set for forecasting the specific

target variable. These choices are made based on minimizing RMSE, considering the

algorithm explained in subsection 3.9.

Target Short interest Utilization Transaction trend Days to cover Daily return GC/Warm/Special rt−τ σ(t − τ, 80%) σ(t − τ, 100%) σ(t − τ, 120%)

LSTM σ(t, 80%) X X X X

σ(t, 100%) X X X X X X

σ(t, 120%) X

rt X

GRU σ(t, 80%) X X X X X

σ(t, 100%) X X X X X

σ(t, 120%) X

rt X

VAR σ(t, 80%) X X X X X X X

σ(t, 100%) X X X X X X

σ(t, 120%) X X X

rt X X X X X X X X X

VAR model. These results are summarized in table 4.1. It is noteworthy that no target

variable uses days to cover or daily return, considering LSTM and GRU. These selections

are used throughout the remainder of this analysis.

4.2 Forecast Errors

This section will summarize important results from the out-of-sample model evaluation.

Table 4.2 summarizes average RMSE, MAPE, and PCDF, evaluated over three GC sta-

ble stocks at 20% test data.

σ(t + 3, 80%) achieves minimal RMSE, MAPE, and maximum PCDF with LSTM, it

forecasts the correct direction three days ahead at 81.1% of samples, compared to 0.11%,

76.2%, and 68.7% for the Dummy model, GRU, and VAR respectively. Application of

LSTM is thus considered to be optimal in the case of forecasting σ(t + 3, 80%), achieving

an average RMSE and MAPE of 0.196 and 19.6% respectively, compared with the true

sample mean of 0.606.

σ(t + 3, 100%) achieves minimal RMSE, MAPE, and maximum PCDF with GRU, it

forecasts the correct direction three days ahead at 60.0% of samples. Application of

GRU is thus considered to be optimal in the case of forecasting σ(t + 3, 100%), achieving

an average RMSE and MAPE of 0.044 and 10.8% respectively, compared with the true

sample mean of 0.255.

σ(t + 3, 120%) achieves minimal RMSE and MAPE, and maximum PCDF with VAR

at 66.2%. Achieving an average RMSE and MAPE of 0.143 and 30.2% respectively,

compared with the true sample mean of 0.367.

254.3. FORECASTS CHAPTER 4. RESULTS

Table 4.2: Average RMSE, MAPE, and PCDF were evaluated on an out-of-sample

forecast over three GC stable stocks and 0.8 train size. The best statistic for each target

variable is indicated by *.

Target variable Average RMSE Average MAPE Average PCDF

Dummy σ(t + 3, 80%) 0.349 38.3% 0.1%

σ(t + 3, 100%) 0.053 11.2% 1.1%

σ(t + 3, 120%) 0.207 27.8% 0.6%

rt+21 0.0023 28.7% 0.6%

GRU σ(t + 3, 80%) 0.221 23.2% 76.2%

σ(t + 3, 100%) 0.044∗ 10.8%∗ 60.0%∗

σ(t + 3, 120%) 0.143 30.2% 56.6%

rt+21 0.0018 25.9% 65.3%

LSTM σ(t + 3, 80%) 0.196∗ 19.6%∗ 81.1%∗

σ(t + 3, 100%) 0.051 12.5% 57.4%

σ(t + 3, 120%) 0.156 30.1% 65.2%

rt+21 0.0019 40.3% 65.8%∗

VAR σ(t + 3, 80%) 0.275 31.8% 68.7%

σ(t + 3, 100%) 0.052 14.2% 55.1%

σ(t + 3, 120%) 0.138∗ 26.5%∗ 66.2%∗

rt+21 0.0017∗ 25.5%∗ 63.6%

Finally, rt+21 achieves minimal RMSE and MAPE with VAR, and maximum PCDF

with LSTM, but just slightly. VAR is thus considered optimal for this case. Achieving

an average RMSE and MAPE at 0.0017 and 25.5%, comparatively with the true sample

mean of 0.0019. See table B.3 for a complete table of one, two, and three-day forecasts

on IVS and five, seven, and 21-day forecasts on loan rate.

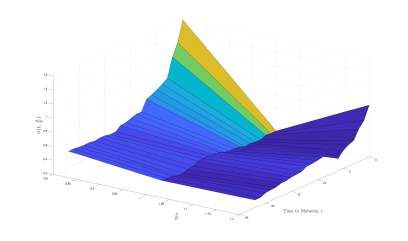

4.3 Forecasts

Having decided an algorithm for each target variable following section 4.2, and further

evaluating RMSE, MAPE, and PCDF for a single GC stable stock, the forecasts gen-

erated from these are presented here. Figure 4.1a shows an out-of-sample, three days

ahead rolling LSTM forecast on σ(t, 80%), it is apparent that the algorithm managed to

contextualize lagged data in terms of similarity with actual values.

Figure 4.1b presents a three-day ahead rolling GRU forecast on σ(t, 100%), it is easy to

notice how noisy this variable is. The GRU algorithm is however quite capable in terms

of visually following similar trends as the true values. Compared to figure 4.1a it is not

264.3. FORECASTS CHAPTER 4. RESULTS

as accurate, which is also expected from table 4.2.

Figure 4.1c presents a three day ahead rolling GRU forecast on σ(t, 120%), more reminis-

cent of figure 4.1a in regards to accuracy and time trend than figure 4.1b. Noteworthy

here is that this forecast only considers lagged values of itself but is still capable of

contextualizing the information.

(a) σ(t, 80%). (b) σ(t, 100%).

(c) σ(t, 120%).

Figure 4.1: Out-of-sample forecast for σ(t, 80 : 120%) on a GC stable stock with LSTM

and GRU. The blue line is the three days ahead forecast with rolling window methodol-

ogy, orange dotted is the actual three days ahead IV.

Figure 4.2a presents a 21 day ahead rolling GRU forecast on rt , it is apparent that there

is more noise in this variable compared to figure 4.1a, 4.1b, and 4.1c. The GRU model

seems less capable of forecasting this variable compared to the aforementioned. Table

4.2 presents that the directional forecast is correct 65.3% of samples, for the LSTM

model it is 65.8%, which is better than a coin toss (50%) and much better than the

dummy model at 0.6%. Furthermore, table B.3 presents errors for five and seven days

ahead, presenting that the direction is correct 73.6% and 69.7% of samples respectively.

Outperforming the dummy- (0.1% and 0.7%) and LSTM model (59.3% and 68.4%) in

all defined regards. The five and seven days ahead rolling forecasts are presented in

274.3. FORECASTS CHAPTER 4. RESULTS

figure 4.2c and 4.2b respectively. Both are visually more accurate than the 21-day ahead

forecast, however still incapable of matching the actual fluctuations of the rate.

It is noteworthy that VAR is quite capable of forecasting these variables (see figure

B.5) however not as good in following trends and large fluctuations when considering

σ(t, 80%). For σ(t, 100%) the model generates similar results as GRU (figure 4.1b), how-

ever with somewhat lagged trends compared to the true values. Similar inferences can

be drawn from the forecast of σ(t, 120%) as for σ(t, 80%). rt remains seemingly difficult

to forecast, almost constant for the 21-day forecast, explaining the relatively low RMSE

and MAPE. Comparatively to GRU which is capable of finding some trends.

The models with best statistics, in all regards, for variables not yet considered in this

section are here presented concisely accordingly with table B.3. GRU: σ(t + 1, 100%),

σ(t + 2, 100%), rt+5 , and rt+7 . LSTM: σ(t + 1, 80%), σ(t + 2, 80%). VAR: σ(t + 3, 120%).

(a) 21 days ahead. (b) Seven days ahead.

(c) Five days ahead.

Figure 4.2: Out of sample forecast for rt on a GC stable stock with GRU. The blue line

is the rolling window forecast, orange dotted is the actual loan rate.

28You can also read