THE RETURN OF THE INFLATION SPECTRE - Creating Progress

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE RETURN OF THE

INFLATION SPECTRE

ECONOMIC BRIEF 10.032021

Creating Progress

www.asacentra.com

1

The Shape of Global

Recovery

The accelerating rollout of COVID-19 vaccines in many advanced economies has set the stage for

rapid recovery in the second half of this year and into 2022. Although growth in digital and digitally

enabled sectors will level out somewhat, high-employment service industries will ride a wave of

pent-up demand. Assuming that vaccination continues to pick up globally, the most likely scenario

for the economy is a rapid recovery in the second half of this year and into 2022. We should see a

partial but sharp reversal of the K-shaped growth patterns that have emerged in pandemic-hit

economies.

While massive government programs have buffered the economic shock of the pandemic, hard-

hit sectors have nonetheless faced significant losses. Between these transitory reductions on the

supply side and the predictable surge in demand, a temporary bout of inflation is possible and

perhaps likely. But that is no cause for great concern. In the second half of 2021 and into 2022, the

K-shaped dynamic of the pandemic economy will give way to a multi-speed recovery, with the

traditional high-contact sectors taking the lead. The two lingering areas of uncertainty for health

and economic outcomes are the pace of the vaccine rollout in the developing world and

international cooperation to accelerate the restoration of cross-border travel. But with forward-

looking leadership, both issues should be fully manageable.1

Just as no one is safe from COVID-19 until everyone is, a healthy post-pandemic global economy is

not possible without a strong rebound everywhere. But, both across and within countries, the

economic recovery risks falling victim to the same short-sightedness that has hampered the global

vaccine rollout.

1. Central Banks

The world’s biggest central banks will happily live with higher inflation and investors now

aggressively betting on a quicker end to monetary stimulus are all but certain to be proved wrong.

After a decade of underestimating inflation, central bankers in the United States, Europe and

Japan have every reason keep money taps open and policymakers are even rewriting their own

rules so they can let price growth overshoot their targets. If anything, central banks are more likely

to nudge up stimulus, particularly in the euro zone, keeping borrowing costs depressed and

ignoring the inflation hawks at least until growth is back to pre-pandemic levels -- and not just

fleetingly. Even if inflation accelerates, a big if given that big central banks are all undershooting

their 2% goal, tightening policy too hastily is seen as a bigger evil than moving too slowly. 2

1

The Shape of Global Recovery by Michael Spence - Project Syndicate (project-syndicate.org)

2

Analysis: Central banks will happily ignore inflation-mongers | Reuters

2

The ECB is currently accelerating its bond

purchases to push back against higher borrowing

costs, reflecting a widening divergence between

the euro-area and U.S. economies. Central banks

across the region bought an average of 20 billion

euros worth of debt a week over the past two

weeks to keep financing conditions for

governments, companies and households

favorable, and Vasiliauskas signaled that investors

should expect such a pace to continue.3

If the economy recovers and fiscal stimulus turbocharges pent-up demand, a lot of bank credit

could suddenly emerge from central bank money. Price growth will then begin to accelerate, and

the European Central Bank will have a very hard time curbing it without having a functioning

inflation brake.

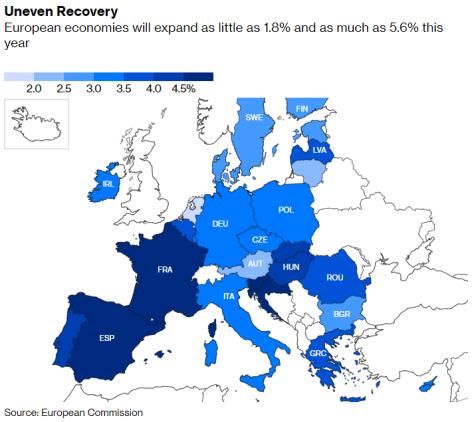

2. Outlook Darkens for Europe’s Virus-Stricken Economy

Economists are cutting growth forecasts for the eurozone economy as a third wave of Covid-19

infections and vaccination delays spur tighter restrictions in several countries including France,

Italy and Germany. ING now expected the eurozone economy to shrink 1.5 per cent in the first

quarter, having previously forecast a 0.8 per cent decline.

Holger Schmieding, chief economist at Berenberg, said each

month in lockdown would shave 0.3 percentage points off

eurozone growth. He has cut his growth forecast for this year

from 4.4 to 4.1 per cent, assuming a one-month delay to

reopening. Barclays economists said they now expected

European mobility restrictions to only be lifted toward the end

of the second quarter, “which will weaken domestic demand,

and consequently imports”. They kept their growth forecast for

this year at 3.9 per cent but cut next year’s from 5.3 to 4.3 per

cent.

Switzerland’s central bank will publish its 2020 currency intervention tally and conduct the first

rate decision of the year, with officials expected to maintain current policy settings with the world’s

lowest interest rate. Counterparts in Hungary, Iceland, the Czech Republic and Morocco are also

expected keep their monetary stance unchanged.

3

ECB Governor Warns Against Sharp Policy Tilt When Crisis Passes - Bloomberg3

Although many economists are downbeat about the short-term outlook for the eurozone, most are

convinced it will rebound strongly once enough people are vaccinated to lift most restrictions later

this year. Others point out that the rebound of global trade will boost export-focused manufacturers

in Germany.4

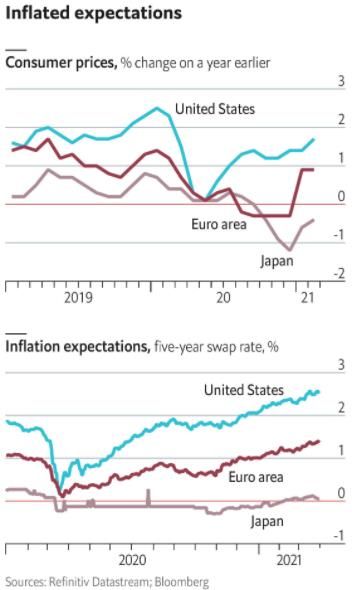

3. Inflation in the Euro Area

Inflation in the eurozone has jumped to its highest level

since the start of the pandemic, but it was driven by one-

off factors that will fade next year, rather than underlying

price pressures, according to the European Central Bank.

European investors will be dreading today’s flash estimate

of euro-area inflation in March, which is expected to be at

its highest in more than a year. Markets fear higher

inflation because it would raise bond

yields and interest rates, which could

in turn destabilise currencies and

asset markets. Yet the rise in inflation, caused by higher energy prices,

disruptions in supply chains and the eventual unleashing of pent-up

demand once covid-19 lockdowns have been eased, is expected to be

temporary. The effects of higher oil prices and supply-chain bottlenecks will

soon fade, but not quite yet. Europe’s recovery will be slower and weaker

than forecast as the continent’s roll-out of covid-19 vaccinations continues to

stutter, falling behind that of America and Britain. The continent is battling

with a particularly vicious third wave of the pandemic that could prolong

tight measures to contain the virus until the early summer. 5

4

Outlook darkens for Europe’s virus-stricken economy | Financial Times (ft.com)

5

https://www.economist.com/4

4. Covid Resilience Ranking

The Ranking’s top four show that snuffing out

or containing Covid early continues to pay off in

quality of life. But, with the exception of

Singapore, these places are lagging on

vaccinations as low caseloads have made the

virus a distant threat. Going forward, that could

put them at a disadvantage as the economies

racing ahead with vaccination start to fully

reopen.6

5. The economic context of North Macedonia

Public finances were also severely affected by the pandemic, with support measures accounting

for about 9% of expected full-year GDP. The overall government deficit was thus estimated at 8.6%

in 2020: to cover the budget financing needs in 2020 and 2021, the government obtained a EUR 176

million credit line from the IMF, and macro-financial assistance from the EU of EUR 160 million, in

addition to issuing a EUR 700 million Eurobond. The deficit is projected at 4.5% this year and 3.2%

in 2022. As a result, debt-to-GDP increased to 50.3% in 2020 (from 40.2% one year earlier), and

should stabilize around this figure in upcoming years (IMF forecast). Meanwhile, inflation remained

stable at 0.8% in 2020, with a rise in internal demand expected to bring it up to 1.3% this year and

1.6% over the course of 2022. Tax evasion remains one of the country’s main problems, with the

informal economy creating unfair competition from unregistered companies (it is estimated that

the informal sector accounts for 18% of employment and between 30% and 40% of income). 7

6

Coronavirus Pandemic: Ranking The Best, Worst Places to Be (bloomberg.com)

7

The economic context of North Macedonia - Economic and Political Overview - Nordea Trade PortalYou can also read