THE CAMBRIDGE WEEKLY 24 May 2021 - Perspective ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

THE CAMBRIDGE WEEKLY

24 May 2021

Lothar Mentel

Lead Investment Adviser to Cambridge

DISCLAIMER

This material has been written on behalf of Cambridge Investments Ltd and is for

information purposes only and must not be considered as financial advice.

We always recommend that you seek financial advice before making any financial

decisions. The value of your investments can go down as well as up and you may

get back less than you originally invested.

Please note: All calls to and from our landlines and mobiles are recorded to meet

regulatory requirements.

24th May 2021

Source: Chris Adams, 19 May 2021

Market resilience in face of Bitcoin crash

Beyond the directly virus-related stories, last week’s news was dominated by cryptocurrency shenanigans

and the return of outright war in the Middle East. Cryptos are the “Reality TV” version of markets – hugely

fascinating, but not having much to do with reality – and largely purchased by believers and speculators,

rather than investors.

Reality of a different sort, the flaring up of hostilities in the Middle East, is immensely sad. The human

tragedy is apparent, but is yet to have wider contagion. While we discuss it greatly, its impact on markets

is currently small. It does pose some problems for Western governments, particularly for the US

administration, hampering its ability to influence other emerging nations throughout the world. China’s

influence continues to expand and is further aided by the Middle East problems, especially in Africa where

an Islamist surge is creating havoc. Much as the Israel-Palestine problems are awful, the Ethiopia-Eritrea

situation is just as, if not more deadly, damaging and urgent.

For markets, last week’s economic news cycle was far more upbeat. The European nations’ “flash”

purchasing manager survey results of business sentiment released on Friday highlighted growing optimism.

Europe is catching up, possibly heading the way of the US in achieving rapid growth. Our separate article

takes a closer look at this uptrend, but also what may hold it back.

Meanwhile, the US may have passed its peak of optimism. Weekly jobs data is still indicating an improving

employment market, but the pace of improvement has slowed. Many will take comfort from this, given

www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk

Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE

24th May 2021 employers have recently found it challenging to find employees amid the scramble to reopen. A more considered moderate environment is probably healthy. As a consequence, the recent narrative of inflation also reached a peak and markets were nervy. Last week those nerves were calmed. The minutes of the US Federal Reserve Open Market Committee (FOMC) meeting told us that the pressure is mounting from some members that the time is coming for the Fed to discuss whether it needs to alter its stance, and begin to pare back bond purchases. That is not a surprising thing to say (what’s the point of a meeting where members don’t share different opinions?) and does not appear too in dicative of a growing hawkishness – which is probably why markets glossed over what many commentators insisted on describing as a “hawkish” set of minutes. Certainly, it is not indicative of a repeat of the 2013 announcement that sparked the bond market “Taper Tantrum”. Bonds wobbled around a bit, but long yields ended up lower, not higher, on the week. Indeed, investors have taken heart. The Fed is moderate in its quest for higher growth, and will not allow inflation expectations to spiral upwards on short-term price-push observations, as certain post-pandemic supply bottlenecks meet supernormal, ‘de-mob happy’ consumer demand. In contrast to the crypto crash, the relative steadiness of general risk asset markets that ensured stock markets closed higher on the week, appears an encouraging sign that markets are not considered as extended by investors as feared. The cooling of the speculative end of market can therefore be interpreted as a sign of stability, and relative ease with prevailing valuations. Commodity prices falling back – without any obvious signs for a change in demand – is one of those speculative movements that actually carry positive relevance for the real economy. Market valuations continue to demonstrate that perhaps those ‘optimistic’ analyst expectations were still not optimistic enough. The economic dataflow underpins this notion further, as it tells us of a formidable recovery of activity that is strongly supported by unspent monetary and fiscal support. To sum up, we have been happy to see some of the speculative froth come off over the course of May, without bond yields being overly affected. To us, this is an encouraging sign that investors are refocusing on the real sources of long-term returns, namely economic activity levels, rather than the flow of ‘hot’ money. However, it would be naïve to assume that this relative levelheadedness, after an extended period of absolutely unprecedented levels of monetary and fiscal stimulus, means we are already on safe ground. The risk that markets overinterpret future central bank communications as the beginnings of a policy error, or declare a temporary fall in the upwards trajectory of the economy as a looming downturn, will be with us for the foreseeable future. In other words, last week has shown there is perhaps a bit less reason to be overly concerned about the risk of extended market valuations, but equally, complacency would be just as ill-advised. www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE

24th May 2021

Europe’s beacon of hope shines light on old problems

After a long quiet spell, Europe is capturing investor interest once again, with the green shoots of a recovery

now coming through. After a desperately slow start, vaccination programmes on the continent have

stepped up greatly, with ever more jabs set to be delivered in the coming weeks. That, combined with

warmer weather and a slowing spread of the virus, is thawing the freeze on economic activity as businesses

start to reopen. Indeed, the signs suggest the recovery is already underway – high-frequency data from the

Eurozone is showing a sizable uptick in travel, business activity and job postings – even while growth data

suggests the Eurozone economy fared better than feared in the early parts of the year. Barring another

turn for the worse, it looks like Europe is headed out of its punishing double-dip recession.

That prospect is making capital markets excited. For most of the year, a dreary economic outlook (and

drearier virus crisis) meant investors held some scepticism on European equities, even if this year they have

traded level with their US counterparts. Low growth expectations, coupled with continued European

Central Bank (ECB) buying were an anchor on government bond yields, which stayed down at historically

low levels, even as the US saw a pick-up. But with hope now on the horizon, bond yields are on the up.

Germany’s ten-year debt yields temporarily rose to their highest level since 2019 – almost touching the 0%

mark at one point – while yields in all the other major European Union (EU) economies are in positive

territory.

Bonds are being pushed by rising inflation expectations, with Eurozone five-year forward inflation swaps (a

measure of long-term price expectations) at their highest levels since late 2018. Crucially, rising yields do

www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk

Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE24th May 2021 not seem to be overly worrying the ECB. This marks a big change from just a couple of months ago, when a move up in Eurozone yields led it into damage control. Policymakers warned against tightening of financial conditions, and announced emergency bond purchases would be at a “significantly higher pace than during the first months of this year”. Now it appears those words did the trick – purchases were ongoing but not necessarily in greater amounts. That the ECB seems rather nonchalant this time round is significant. It suggests officials think the recovery is real, and the Eurozone economy is strong enough to withstand a move higher in bond yields. This is understandable, given where the market moves are coming from. In February, soaring US growth expectations pushed bond yields up all around the world – even though regions including the EU were still languishing. This time, expansion hopes fanning inflation expectations are coming from Europe itself. The US comparison is interesting from a market perspective. The world’s largest economy has undoubtedly been the strongest this year, with a rapid vaccine rollout and significant fiscal stimulus exciting global investors. But the latest data shows a plateau in that rampant growth. And, while activity is stabilising at a decent level, the hype around American assets has been so great this year that there is not much room to budge higher. Europe, on the other hand, has occupied the other end of the spectrum – severe restrictions and the very public vaccine fiasco painted a rather dark picture. But now things are ramping up, markets are shifting focus. That shift has obvious benefits for European assets, but also shines a light on issues that were best left forgotten. Hand-wringing over the European recovery fund – a hard-fought fiscal package for all EU members – had investors sweating earlier in the year. And, even though the political problems there have dialled back, there is yet again more focus on EU’s perennial problem child: Italy. The EU’s third-largest economy has a host of longstanding problems that have been brushed under the rug by the pandemic. Its banking sector has struggled under a raft of non-performing loans since the financial crisis (even if some progress has been made), while its old fashioned and complex legal system has long been a barrier for investment. These structural problems are one of the main factors behind Italy experiencing more than a decade of low growth and disinflation – something that only compounds its debt issues. The situation may be worsened by Brussels’ strict budgetary rules, though any spending is only likely to bear lasting fruit if accompanied by structural reforms. The malaise has been a repeated site of political tension, with populists gaining popularity in Italy and getting into regular spats with eurocrats. The script is always the same: tensions flare between Rome and Brussels; fears of a Eurozone breakup rise; officials find some way of kicking the can down the road; and repeat. Markets were happy earlier in the year when technocrat and former ECB governor Mario Draghi assumed Italy’s premiership after the fall of a fractious government featuring the far-right Lega Nord party. Draghi commands financial expertise and significant respect in Brussels, so markets hoped his technocratic unity government could find a way out of trouble. Reality is always more difficult. While Draghi is popular among international investors, he still has a deficit with the Italian population, simply because he was not elected to office. Moreover, even if he manages to last until Italy’s next scheduled election in 2023, it would be a tall order to solve the country’s structural problems by then. According to latest reports, Italy’s President, Sergio Mattarella, said last week that he plans to retire next year. Lega Nord leader and former deputy prime minister Matteo Salvini was quick to suggest Draghi as the president’s www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE

24th May 2021

successor. If that happens, Draghi will have to relinquish the premiership, likely triggering an election that

Salvini stands a good chance of winning. Nothing has been decided and opinions on the actual outcome

diverge, but already this is a scenario that is keeping observers occupied.

Any political uncertainty would certainly be a headache for capital markets – potentially dampening the

outlook for the wider Eurozone as it dampens hopes for structural reform. With that issue on the horizon,

investors might start to wonder what the Eurozone looks like once the ECB starts buying fewer securities

– which for now have kept Italy’s yield spread versus the German bund very tight, and therefore far less

burdensome than it had been at certain points in the past. For now, we can at least take comfort that these

problems are coming from a place of strength.

Don’t blame it on the property

With a heavy heart – and a heavier bill – Aviva told investors last week that after a tumultuous year for the

fund, the firm will shut its main UK Property Fund as well as its two feeder funds on 19 th July and return

cash to investors “in a fair and orderly manner”. The current liquidity of about 40% of the fund will be

returned (equivalent to about 40% of current value) but the rest will dribble back as asset sales are

completed, which may take up to two years.

Like many other investment firms, Aviva suspended trading in its open-ended property fund last March –

just as the pandemic began and capital markets were in nosedive. Equity markets have long since recovered,

generating impressive returns over the rest of 2020, but the gates never opened on Aviva’s property

investments. Now they never will, with the group concerned that maintaining value – while keeping enough

liquidity to fulfil redemptions – would be impossible.

As reasons for the closure, Aviva effectively cited the continued “material uncertainty” around its assets

that had caused the initial suspension. An internal review found that generating positive returns while

maintaining a suitable cash level for investors was not viable amid the fallout of the pandemic.

After a year of the deepest global recession on record, this might sound reasonable. But it sounds much

less reasonable when you consider that now, and for some time, the global real estate market has been

doing quite well. Like everything in the early pandemic, both commercial and residential property prices

looked in trouble last March. But more recently, prices, trading volumes and interest have fared fairly well

in almost all areas.

We have noted before how this has played out for residential markets across the world. For current and

prospective homeowners, lockdown has bolstered current savings, employment is reasonably assured (with

interest rates rises not expected to exceed pay growth), making houses just about affordable.

In the UK, an extended Stamp Duty holiday has pushed buyers into the market, initially in those previously

underbought areas outside of the main cities. Office for National Statistics (ONS) data published on

Tuesday showed house prices rose in March by more than 10% in annual terms – the biggest monthly

increase since August 2007. Prices of detached houses rose 11.7% in the year to March. Last week, with

the delights of socialising returning, Tim Bannister, Rightmove's director of property data, told us there is

"good news for city centres across Great Britain, with a number of agents now telling me they've seen a

marked uptick in demand from first-time buyers”. Rightmove said buyer demand for flats in April stood

www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk

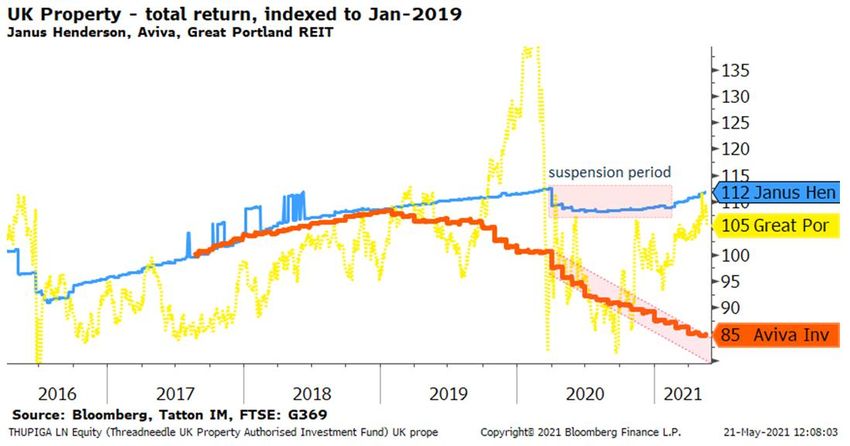

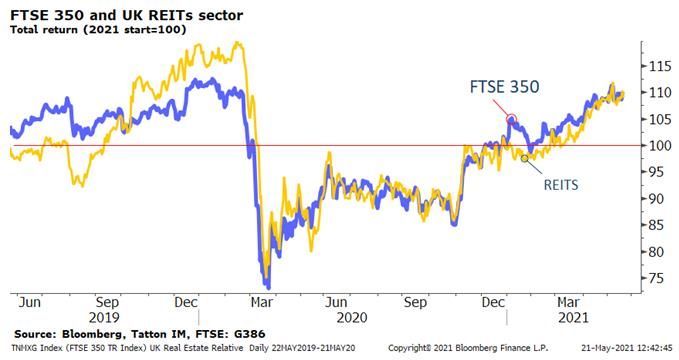

Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE24th May 2021 51% above pre-pandemic levels in February 2020, while ONS March year-on-year data showed an increase of 5.0% for flats and maisonettes. Similar situations hold in the US, Australia and other developed nations, where consumers are putting stimulus cheques to work, and housebuilders are seeing strong demand. One exception is China, where property prices are faring relatively worse. This is almost certainly due to the relative tightness of China’s monetary policy – something we have pointed out several times. This suggests that the extremely accommodative monetary policy we are seeing around the world is driving activity, as expected. In the UK commercial property market, Stamp Duty holidays do not apply. But, according to last month’s survey from the Royal Institute of Chartered Surveyors (RICS), commercial property in Britain is nevertheless undergoing a decent revival. There are longstanding issues in the commercial property market which have been compounded by the pandemic, from the ‘death of the high street’ phenomenon to an increase in working from home – lowering demand for office space. And yet, the RICS survey for the first quarter of the year shows respondents are confident of a recovery. That returning confidence may be reflected in the relative performance of the FTSE350 REITs sector (REITs are publicly listed, close ended real estate investment trusts). The graph below shows the beginnings of outperformance relative to the FTSE350 index since the start of the year. Revaluations of net asset values happened through last year, and REITs are mostly trading at discounts which suggest those are generally not likely to start being pushed up. However, REITs are outperforming the recent rise in the overall FTSE350, which may tell us that investor perceptions of commercial property market values are improving in line with the survey. Our point is not to be a cheerleader for the property market, rather to highlight that Aviva’s property fund troubles cannot be put down to economic or market factors alone. www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE

24th May 2021 There are certainly questions around how different parts of the market will respond as the recovery continues. Industrial and distribution space is doing well. We are not back to normal as far as retail and offices are concerned, but as people flock back into cities, some property developers are confident of what is ahead. For example, despite the empty offices, there is currently a building and refurbishment boom going on in the capital, as well as other major cities around the developed world. New construction starts have jumped by 20% between September 2020 and March 2021 to 3.1 million square feet, Deloitte's London Office Crane Survey showed. Of this work, 56% involves upgrades of existing office stock. "Occupiers' needs are shifting and buildings that meet their ESG principles while taking into account the welfare of their people are top of mind. Grade A, well-connected and eco-friendly office spaces, designed to maximise the benefits of new ways of working, will be the most desirable," said Mike Cracknell, director in real estate at Deloitte. So, although overall property prices may have bottomed, changing demands from tenants means the most important factor in real estate asset performance is having the right space. The problem – as with all open-ended property funds – is the way these funds are structured. Open-ended property funds promise investors the best of both worlds: exposure to the returns of the highly illiquid property market, but with the benefit of daily-traded liquidity. Investments that sound too good to be true usually are, and these funds are no different (which is incidentally also why we do not consider holding such property funds in our investment portfolios). As investors in these funds have found out over the last year, liquidity turns out into a mirage as soon as the going gets tough. Most open-ended property funds are only just re-opening, more than a year after shutting their gates, and several that have opened have had to sacrifice huge chunks of their property portfolios – the bit that actually generates return – to do so. Aegon’s property fund is still struggling to sell its stock to reach adequate cash levels for redemptions. In April 2020, just after most funds had shuttered, reports came out that in aggregate, retail investors were paying nearly £10 million in monthly fees despite not being able to sell their investments. Illiquidity bites open-ended funds especially hard at the bottom of cycles such as this one. End-investors may be trying to withdraw capital, but difficult properties find no buyers, while good ones are snapped up at what looks like almost ridiculous valuations. A fund, even a generally well-managed one, can find itself in the wrong place with no chance of rotating the portfolio. The graph below shows how Aviva found itself in the wrong space, while Janus Henderson seems to have played its hand better. www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE

24th May 2021 In truth, the stability offered by open-ended property funds is really just an inadequate form of risk-pricing. We can see this when comparing their performance against REITs (like the Great Portland REIT in the chart above), the structure of which we would consider much more suitable for portfolio inclusion. Unlike open-ended funds, REITs are companies whose value is based on their property portfolios, but can fluctuate day-to-day as the market moves. Investors may be put off by the volatility REITs go through – especially as property is often perceived to be a non-volatile asset. But again, this volatility is actually just an accurate pricing of the underlying risk, which can move around even when underlying property valuations might not. As the recovery gathers momentum, property prices should benefit. That gives it a reasonable investment perspective, but investors should as always be aware of the risks they are taking. If that means the investment is clearly labelled as volatile, we would argue this is still better than papering over those risks with false promises. www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE

24th May 2021 * The % 1 week relates to the weekly index closing, rather than our Friday p.m. snapshot values ** LTM = last 12 months’ (trailing) earnings; ***NTM = Next 12 months estimated (forward) earnings If anybody wants to be added or removed from the distribution list, please email enquiries@cambridgeinvestments.co.uk www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE

24th May 2021 Please note: Data used within the Personal Finance Compass is sourced from Bloomberg/FactSet and is only valid for the publication date of this document. The value of your investments can go down as well as up and you may get back less than you originally invested. Lothar Mentel www.cambridgeinvestments.co.uk | enquiries@cambridgeinvestments.co.uk Tel : 01223 365 656 | Nine Hills Road, Cambridge CB2 1GE

You can also read