Strategic Economic Directions - BROADCASTING CONTENT CREATION ESPORTS DIGITAL MEDIA for the Isle of Man in - Isle of Media

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Strategic Economic Directions

for the Isle of Man in

BROADCASTING ∙ CONTENT CREATION ∙ ESPORTS ∙ DIGITAL MEDIA

CAPITAL ∙ CREATIVITY ∙ CONNECTIVITY

PRESENTED BY PRESENTED ON

Dr Richard K Arning, February 2019

Isle of Media Proprietary

Government commits to the Digital Media sector growth

Minister for Enterprise Laurence Skelly on Manx Radio Sept 2017 Treasury Minister Alfred Cannan in ‘The Budget Speech Feb 2018’

“Media and the Creative Industries is quite an interesting proposition “There is also far more to digital business than the booming eGaming

going forward because we think we are very well positioned not just in sector.

TT but great legacy in film for example. We think we can create a new

We are beginning to see exciting opportunities in the digital media, and

industry here with post production and animation and the various other

unlike much of the film industry that we previously enjoyed, the

indigenous media jobs.

employment opportunities could be year-round and sustained on-

And you know the Film Festival which was just the other weekend. island.

Great to see young Manxmen when they shoot film. That’s someone

I will today signal our commitment to the potential in this sector and

who’s been dedicated and we want to have that creative, sustainable

look forward to discussing with the Department for Enterprise”

industry right here on the Isle of Man.”

Isle of Media Proprietary and Confidential 2

Executive Summary

Disruption in TV and exponential growth in video Growth Opportunities for the Isle of Man

Linear Television is a highly profitable, cash-generative, mature • Unique offshore value proposition without competition in Europe

industry. The rise of ‘non-linear TV’ or ‘Video On Demand’ (VOD) or • Building on the Island’s TV/video industry and the heritage in film,

‘Over-The-Top’ (OTT) is driven by changing viewing habits, massive attracting job generating ventures - instead of risky film financing

investments into ‘original content’, leveraging global reach by • Skills synergies with eGaming, video gaming, animation and ICT

streaming, advances into broadband infrastructures and regulatory • Video as the most data-intense form of data can leverage on the

enforced opening of previously geo-blocked/licensed markets. New Island’s ICT infrastructure including the new teleport

forms of content and end user devices have entered the markets, like • Potential regulatory advantages to be explored as VOD/OTT

social media television for millennials, VR and eSports. The ultra-fast regulation (e.g. for the likes of Netflix) is in its infancy

changing value chain is creating numerous opportunities, new jobs and • Leverage on the positive branding of the TV, film and video and

showcase the Isle of Man internationally including the Film Festival

new companies in content production, tech, monetisation, consulting

and advertisement. The Isle of Man can capture this fundamental Recommendations

opportunity for new entrants in the Digital Media Space • Embrace current disruptive opportunities of a Digital Media boom

• Focus on high growth areas of OTT, video tech, eSports etc.,

Financing & Taxation

building on the synergies with eGaming and FinTech and position

‘Tax Rebates’, which are effectively grants, are a race to the bottom for the Island as a finance & service hub for this new sector

the competing jurisdictions in production of film / high-end-TV (drama, • Cluster content around motorsports, nature, animation & eSports

documentary, comedy), animation, kids-TV and video-gaming. Other • Offer financial support for sustainable media companies

TV genres are not subsidized, neither do businesses engaged in tech, • Provide sustainable marketing funding to grow to critical cluster size

distribution, broadcasting or OTT benefit. They are taxed with standard • Research co-production treaties and jurisdictional coopetition

corporate tax rates. This creates opportunities for the Isle of Man to • Create alliances with stakeholders in the North-West and region

attract fast growth, highly-profitable Media ventures rather than film • Explore private investments tools in Digital Media

Isle of Media Proprietary and Confidential 3

Vision: Europe’s unique Offshore Media Cluster

KPI People: Increase of the economically active population

• Jobs in the sector

• Sector related entrepreneurs, investors, actors, … living in the IOM

• Graduates with media degrees

Investment • New media companies

People

Brand KPI Investment: Media business

• Sector GDP/GNP

• Investment into infrastructure like studios, teleport

• Private investments into media ventures

KPI Brand: From awareness to interest

• Marketing reach

• Deal flow: Active leads, prospect visits, pitchdecks/BPs

• Cluster coverage in press and social media

• Isle of Man featuring in media products

Isle of Media Proprietary and Confidential 4

Contents

1 Markets

a. Trends

b. Global TV and Video Markets

c. Global Film Markets

d. Global eSports Markets

e. Competition of Jurisdictions & Clusters

f. Brexit

2 Isle of Man Ecosystem

a. Financial Assistance & Taxation

b. The Isle of Man Cluster

c. SWOT Analysis

3 Strategic Recommendations

a. Embrace Change & Boom: 1001 Opportunities

b. How to organise: Isle of Media as Public Private Partnership

c. Where to concentrate on: Three Areas

d. Marketing Plan

Isle of Media Proprietary 5

1. Markets Isle of Media Proprietary

a. Trends: Disruptive new players in boom sector

New Business Models

Social Shift

#TheNewBlack ‘TV is the New Film’ for #HybridNetworks e.g. bundles with eCommerce or broadband

actors and producers in high end drama; #PeakContent flooding the screens fueled by VC and equity

binge watching; ‘TV Oscars’ coming

#OrginalContent as USP for platforms and broadcasters

#Millenials User generated content; short

#ShortformContent viral videos and memes

formats; mobile viewing; vertical formats

#BrandedContent Retailer: live events or personal shopping

#eSports going big and TV

#NicheInterests reaching economy of scale by global OTT

#SocialMedia platforms like Youtube,

Facebook, Twitter offering live events or #Middleman (distributors, studios) taken out by platforms

even classic broadcast channels streaming

packages

#CordCutting #VOD replacing PayTV;

service bundling by users; skinny bundles Tech

#GigabitSociety (FTTH) overcoming #UHD #4k #HDR becoming mainstream in sport, shopping,

bandwidth bottleneck, enabling VOD for fashion, high-end-documentary… #8k looms

everybody and 4k/HDR

#VR #AR #360 as complementary content and experience

#Cloud for DVR, playout services and video archives

Isle of Media Proprietary and Confidential 7

b. Global TV and Video Markets

Revenues Rise in TV industry Longer TV viewing

PwC Global Entertainment and Media Outlook ’16-‘20)

Growth in transmission service revenues

Rise of OTT

Isle of Media Proprietary and Confidential 8

c. Global Film Markets

Box Office Ticket Sales flat / declining UK Indie Film Crisis (from Screendaily)

• Long-term stagnation in the number of global tickets sold. • ‘The State Of The UK Independent Film Sector’ study recently

Admissions totaled 1.32 billion last year, flat compared with 2015, completed for UK producers’ association PACT was that 78% of the

and down from 1.4 billion a decade ago UK producers contacted for the report have had to defer some or all

• Challenge to lure younger audiences who have more entertainment of their fees since 2007. Given they were unlikely to have had much

options in the home of a share of the ‘backend’ from the profits of their films, this means

that, in certain circumstances, they are working for virtually nothing

Box Office Revenues flat, China disappointing • The international market value for independent UK films has

• Leveling off at the global box office underscored sluggish movie suffered a decline of an estimated 50% since 2007. The report puts

ticket sales in countries outside the United States and Canada. this down to digital disruption, increased competition for audiences

Foreign box office totaled $27.2 billion in 2016, down from $27.3 and the squeeze caused by the global financial crisis of 2007. It

billion in 2015 concludes the present financial model is “broken”

• China fell 1% to $6.6 billion in 2016, in U.S. dollars • With 25% UK tax relief the sector struggles to compete with other

English-speaking countries like Canada and Australia

Monetisation by linear and non-linear TV

• Most UK sales agents acknowledge the international market value

• The importance of box office revenues is diminishing for film (down for UK films has dropped and point out they too are suffering as a

to ca. 10%). Some films directly start online result. “The answer to falling international revenues isn’t simply to

replace them with something else, it is to address those

→ But more important for an Isle of Man Digital Media strategy international markets and get better at selling to them,” suggests

than the global block buster driven cinema business is the small- Charlie Bloye, chief executive of Film Export UK

medium budget and UK (Indie Film) situation

→ Still Indie Film fuels the skill pipeline and has avantgarde value

Isle of Media Proprietary and Confidential 9

d. Global eSports Markets

Other businesses :

• Event Infrastructure

Operators

• Event Connectivity

• Training Centre

Operators

• Virtual Merchandising

• eGambling, e.g.

lootboxes

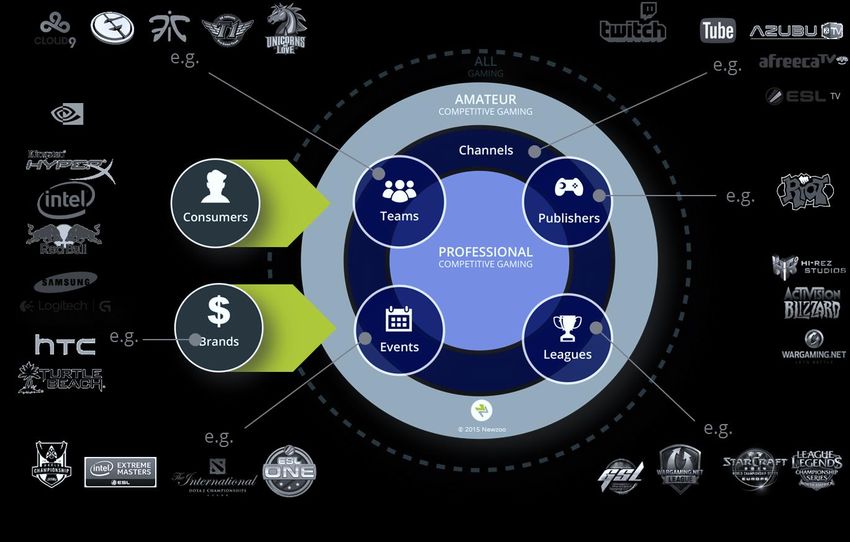

Isle of Media Proprietary and Confidential 10d. Global eSports Markets 60–40–40 CAGR 2015 – 2017 1bn revenue 150 million audience (Deloitte ‘15) 2017 viewers: YouTube Gaming +343%, Twitch +197% Twitch > CNN viewers League of Legends as many viewers as Olympic Opening in ‘15 German coalition contracts awards ‘Sports’ status eSports bigger than Sports in Future? → Massively booming and equity hungry industry with a few, very effectively addressable top decision makers. The UK, which eSports sector is lagging behind Germany and Poland in Europe, is said to become the next big European market Isle of Media Proprietary and Confidential 11

e. Competition by other Jurisdictions & Clusters

Drivers for Cluster Development, examples

• Real Estate:

- Media City UK, Dubai Media City, Media Park Hilversum

• Giant anchor:

- Cologne (60% of TV market, eSports: ESL, Gamescom), Hilversum

Hollywood, Mumbai,

• Attracting Enabler:

- Belfast Studios, Berlin Babelsberg, Pinewood Studios, Malta

• Pooling Initiative:

- RockCity Sweden, @22 Barcelona, Screen.brussels Berlin, Malta, New York, Tokyo,

• Creative Region (Urbanisation Economics) or area: Media City UK, London, Paris

- Paris, Amsterdam, Singapore, London Soho, Hamburg St. Pauli London

• Outdoor Location:

- Isle of Skye, Budapest, Malta

• Tax Incentives:

- Vancouver, Quingdao, Fiji, Sydney

• Low Cost Wages:

New York, Hamburg,

- Budapest, South Africa, Croatia Silicon Valley,

London

• Low Tax ← No cluster competition in Europe for IOM Dublin

- Dubai

Isle of Media Proprietary 12e. Competition by other Jurisdictions & Clusters

The New Studio arms race, a random overview: Tax Rebates & Offshore Competition

• Manchester/Salford: £1bn to double size for more TV studios as • UK Film production (theatrical release): max cash credit 20/16

well as shops, offices, a 330-bed hotel and 1,400 new homes percent of UK expenses (depending if budget above/below £20m)

• Pinewood: £250m expansion by adding 100,000 sq m of new • UK TV producers, broadcasters, distributors: No tax credits

facilities, including twelve large stages with supporting workshops, • UK S/EIS tax reliefs for investors

production offices and infrastructure • Ireland: Capped tax reliefs for film investors plus 32% cash credit on

the lower of eligible expenses, 80% total costs, €70m

• Edinburgh/Straiton: New ‘Pentland Studios’, £250m for 1,600 jobs

• Canada: foreign producers tax credits from 32% to 70% of eligible

by purpose-built studio complex, six sound stages up to 70ft tall at

labour, plus tax incentives on local spend from 20% to 30%. Extra

the 106-acre site, 2 Hollywood-style backlots, a 180-room hotel, a

regional tax incentives for visual effects and animation

50,000sq ft creative industries hub, 50,000 sq ft of workshop

• Channel Islands: Rather inactive ‘Creative Industries Guernsey’,

space and a film academy

failure to create something similar in Jersey. No Media Fund

• London: Plans to build London’s largest studio in Dagenham • Malta: Film shooting location strategy plus attracting Media Funds.

• Liverpool: New ‘Pinewood of the North’ £35m for 350 jobs Up to 27% cash rebate, for co-productions up to 32%. Newly

• Belfast: Adding ‘New Harbour Studios’ with £20m for 120,000 sq launched fund for feature films up to 120,000€. Studios, film and TV

ft of studios, workshops and offices on 8 acres industry existing. Some smaller funds for creative industry. 35%

• Dublin: €20m for ‘New Bay Studios’ on 20 acres corp.tax but tax refunds to non-resident-shareholders result inf. Brexit

Background Information Scenarios

• The EU Audio Visual Media Services Directive (AVMSD) • EU funds for content and ventures might not/only partially be

regulates mass media whether television broadcasting or on- replaced in the UK but are negligible (£40m in 14/15) compared to

demand billions of commercial funding. Impact is on small indie artists only

• The AVMSD applies the ‘Country of Origin* Principle’ which • Unlike the current UK situation with the EU’s AVMSD applied or

means that broadcasters just need one regulatory approval of the the similar EEA arrangement (e.g. Norway), the other role models

most relevant EU member state (‘Passporting’) for a post Brexit Britain are: the Customs Union model (e.g.

Turkey), the Free Trade Agreement (e.g. Canada) and the WTO

• The Isle of Man as being outside the EU cannot provide the

model, all applying the ‘Country of Destination Principle’. Without

necessary EU member state regulatory approval for an EU

the EU ‘Passporting Rights’ from the AVMSD the UK might lose

satellite channel operated from the Island. This is different for an

several channels currently operating from the UK. Especially

Isle of Man based web TV channel, streaming into EU territory

Ireland and the Netherlands might benefit. But also the Isle of Man

• Regulatory restrictions e.g. for advertising result largely from would have no regulatory disadvantage any more compared to UK

national regulation than the less specific AVMSD, creating a

• As a positive Brexit outcome the UK, being lifted from EU state-aid

regulatory competition of jurisdictions

restrictions to subsidise content with local connection only, could

• EU funding is currently provided for UK content and ventures further boost its content industry already fuelled by US investments

• EU broadcasting and film talent can work currently in the UK → The outcome of state level Brexit negotiations as well as the

market reactions are not known.

Isle of Media Proprietary *Criteria Ranking; Location of Headquarter. Editorial Decisions, Staff, Satellite Uplink, Satellite Capacity… 142. Isle of Man Ecosystem Isle of Media Proprietary

a. Financial Assistance & Taxation

Taxation Grants Tax Rebates / Sovereign Equity Private Equity

Cash Backs

Corporate Tax 0% Up to 40% grant Isle of Man supports Multi-million support Angel Networks:

managed by content production scheme in equity • Bridge

Capital Gains Tax 0%

Department for ventures financially financing and loans • Ellanstone

Enterprise with grants and the • Icarus Media

No Inheritance Tax

Digital Creation • NorthInvest

No Insurance Tax

Scheme • Manninvest

No Stamp Duty

Income tax: Funding for: Instead of cash-backs Available private • Family Offices

0-20% with a 5-year • Global Marketing e.g. for one-off Co-Investments • HNWIs

election of a £175k cap • Infrastructure productions the Island • Funds

‘Key Employee • Equipment offers grants. Loans & • Corp. Investors

Concession’: • First year expenses equity for relocating • S/EIS

3-year tax concession • Training and local sustainable • Int. Stock Exchange

for non-Manx income media companies

Isle of Media Proprietary and Confidential 16b. The Isle of Man Cluster – The Starting Point

Location used / featured Financing of Film Shootings Production & Distribution Businesses

(no financial support by Government)

• Isle of Man featured in TV or films • Investments into films for • Real Business:

theatrical release at the Sustainable jobs & revenues

• Good for marketing the Island

box office are speculative

• Growing incumbent sector

• Examples from TV:

• Markets the Island directly by photo-

• Up to 100% spend on Island

• Isle of Man in Mare TV, NDR (G) shooting or by bringing over film stars

• The Queen’s Isles, Arte (G, F) • Isle of Man USP with zero corporate tax,

• Very active cultural scene of filmmakers

• Cyclefest, Bikechannel (UK) no capital gains tax, low income tax

especially with Isle of Man Film Festival

• Julia Walks, BBC

• Available financial support by existing DfE

• BBC Crimewatch • Sound film and acting oriented education

schemes

• British Cycling Championships, offerings and local talent base

Eurosport (UK) • Sector promoted by Isle of Media

→ Not jobs creation related

→ Previously offered equity financing of • Island promoted by locate.im

Paid Marketing by DfE film productions cannot compete with → Jobs creation & investment focussed

‘cash-back film jurisdictions’ like UK, → De-risking public investments

• TT and Classic TT Ireland, Canada

• TV advertisements → Large audience reach for marketing the

• Videos on Social Media Island as a place for tourism, living and

→ Too small to compete e.g. with Scotland or business

Channel Islands

Isle of Media Proprietary 17b. The Isle of Man Cluster – Building the Supply Chain

The Tech Side

• Television, Displays, Set-Top-Boxes

• Satellite, Cable, Terrestrial, Antennas

• Telcos, Data Centres, CDNs, MSOs

Transmission

• Encryption, Encoding, Ingest, Sync

Playout • Measurement, Metadata

• Profiling, Targeted Ads

Channels & Platforms

• Recommendation Engines

Distribution Advertising • App Developments and App Platforms

Post Production • Video Middleware

• Video & Image Processing

Production • Capturing: Cameras, Recording…

• Production Studios, Broadcast Studios

Isle of Media Proprietary 18b. The Isle of Man Cluster – A Growing Supply Chain

IOM Enterprises

Related Sectors

• SES

Radio

• Continent8, Domicilium, Manx Telecom,

3FM, Energy FM, Manx Radio

Netcetera, Sure, Wi-Manx

Web Design (selected) • (Offer of Sohonet to invest in PoP and connect to

400 Media ventures for virtual collaboration)

IOM Advertising & PR, Transmission

572 Digital, BOLD,

• (SES MX1)

Mannin Group, Playout • UniqueX, (LaunchTV)

MM&C,

Gef • Arts Council, BBC IOM, BigClive, CultureVannin,

Channels & Platforms ITV IOM, lovelygreens, mt.tv, ralfydotcom

Newspapers

Tindle • Duke / Motorsport Network, Greenlight International,

Distribution Advertising Heroes & Friends, Mediatech Advertising

• Actiphons, Bloom Creative, Blue Olive, Cooil Creatives,

Post Production Cool Edit Prod., DAM Prod., Dark Avenue Film, Duke

Marketing, EDITIOM, (Flix), FormatZone, Glass Line

Media, Global Motorsports Ventures, GreenlightTV,

Halycone Studios, IOM Props and Film Services,

LovelyGreens, Mannimation, Parker & Snell,

Production (Waterbear), Visual Picnic, Your Movie Crew

• CG Aerial , Engine House, Island Media Studios,

HawkEye, Manx Radio Sound Stage, The Dome

Motorsports Nature Animation eSports

Isle of Media Proprietary 19c. SWOT Analysis Isle of Man Cluster

Strengths Weaknesses

• Low corporate and personal taxation; country lifestyle & safety • No ‘tax credits’ for film/TV production or game design

• Nucleus and organically growing media sector existing to build upon • Access to equity (> 500k ) difficult, missing VCs, angels not used to media

• Positive momentum of new ventures setting up and increase of deal flow • Regulator tending to overregulation

• Senior level expertise in joint team and wider expert network of Isle of Media • No major broadcaster, studio, or digital company as catalyst like in Salford

• Strong synergies with existing Island’s skillset in animation, game and gamble • Small size of Isle of Man media sector and related brand in its infancy

design, marketing. Natural centres of gravity in motorsports and biosphere • Extreme low unemployment (< 1%); recruitment from outside necessary

• Digital Media Education established; available local talent base of creatives • Exit taxation on off-shoring assets; withholding tax levies; lack of tax treaties

• Positive sector brand. British-Irish and globally a boom sector • Higher costs of living, travel, communication; no “Soho-Feeling” on “The Rock”

• New / redesigned incubators like Engine House, Mountain View, Eagle Lab • Understaffed and only part time teams of Isle of Media and DfE

Opportunities Threats

• Become Europe’s only Offshore Digital Media hub including financing for • No long term commitment to the media sector in politics and society

high-growth, high-profit ventures. Driven by industry, supported by IOMG • New Communication Bill with overregulation e.g. of VOD/OTT

• eSports as new, motorsports, nature and animation as existing growth areas • Draft area plan preventing broadcast/telco infrastructure investments

• Video tech, media finance and services • Potential Brexit impact: on immigration rules, TV channel passporting, EU-Co-

• Transform the Island’s ‘brick-and-mortar’ DVD exporters into online offerings Production Treaty

• Leverage on telecommunication infrastructure including local teleport • EU Single Digital Market legislation potentially threatening leading UK creative

• Midterm: liaise with #NorthernPowerhouse and Salford Media City industries by abandoning national licensing

• Work with the related sectors of ICT, eGaming/eSports and Cultural Industries • Eventual future studio overcapacities in UK & Ireland

within the Digital Agency

Isle of Media Proprietary 203. Recommendations Isle of Media Proprietary

a. Embrace Change & Boom: 1001 Opportunities Content Production & Distribution Content remains key! Whether it plays to the strengths of the location or to the tax advantages outside the subsidised genres like drama & kids there are plenty of USPs. Focus on support for production enterprises rather than individual content projects, plus distribution Broadcasters, Platforms, eSports, Adverts Endless opportunities building on eGaming and the existing video industry. The new Isle of Man teleport adds to the Island’s telecoms and data centre infrastructure. On top of attracting new channels and platforms the monetisation of existing video libraries on the Island via OTT can give a boost for incumbent IOM companies Media Tech Sector So far an almost untapped field in the marketing and a rapidly expanding sector. With dedicated events, e.g. IBC Future Zone & Launch Pad, a targeted marketing is possible, subject to available resources Isle of Media Proprietary and Confidential 22

b. How to organise: Public Private Partnership

Strategy Financing

‘Digital Media’, even if focused on video, television & film, bears a Expertise from industry is not just needed to pre-evaluate business

complexity which requires several experts from different backgrounds plans but also to identify and engage the private funds industry and

to derive a holistic sector strategy for the Island. Different monetisation angel investors.

and distribution strategies for different genres, new technologies, cloud

Networking & Association

service strategies and pricing benchmarks, international tax laws and

film and TV funding, …only industry can structure the way forward Isle of Media was also set up as network platform to create a dialogue

between the various stakeholders on joint opportunities and give the

Marketing & PR incumbent industry a voice. The Digital Agency of the Department for

Off-Island marketing is key to success. Road shows, networking on Enterprise provides the opportunity to build closer links to ICT and

trade shows and individually targeted approaches are as important as eGaming. Cooperation has be found with the NorthWest/region

social media is. But it still comes down to personal contact networks

Governance

and the seniority brought to the table. This is why executives and big

Directors of the Board are from the Island’s sector largest media and

corporate brand names are mandatory. Bundling resources from

broadcast companies. An advisory board provides:

government and industry, we operate with a single brand as a PPP

• Independence: largely based off-Island with international expertise

Business Development • Strategic guidance

From marketing to develop a concrete ‘lead’ for a venture to setup • Tactical reach to enlarge client network

business on the Island, this takes persistence and is work intense. • Seniority reference

Financing, tax, facilities, staffing questions… need to be answered, the

Island ‘show-cased’. The PPP provides the legwork for clients but most

importantly it creates the trust of dealing with industry experts

Isle of Media Proprietary and Confidential 23c. Where to concentrate on: Three Areas

Conditions:

• Public financial support schemes & private equity

• Regulatory framework and jurisdictional coopetition

• Infrastructure in telecommunication & studios

• Education & training

Conditions

Campaigns

Campaigns:

Clients • Geographically: From the NorthWest to UK/EU to global – no limits.

Special links to South Africa & Norway to be assessed

• Int. Conferences & Hot Spots: Cannes, London, Amsterdam,

Manchester, Cologne, Munich, Zurich, Edinburgh

• Home turf: Celtic Media Festival, Isle of Man Film Festival

• Social Media & Press: Focus on Twitter and interplay with press

Clients:

• Level: Owners, board and C-level

• Genres: Motorsports, Nature, Animation/VFX/games and eSports

• Sector: Address all levels of the supply chain to build a cluster

Isle of Media Proprietary and Confidential 24d. Marketing Plan: Events 2019

Scouting, Research & Strategy Off-Island Events Other

MipTV Cannes IOM AfterWork Network

NorthWest

Celtic Media Festival IOM

Ludicious – Zürich Game Festival

Isle of Man Film Festival

MIPCOM Cannes

IBC Amsterdam or Angacom or TV

TT Media guests

Connect

London Business Club

RTS Centre

Isle of Media Proprietary 25d. Marketing Plan: Print, Social Media, Web, Press Webpage: Information Youtube-Channel: Videos & Promo Press Coverage of: Investments, New Ventures TWITTER: Industry Facts, Events & News LinkedIn & Facebook: Events & News Brochures: Information ‘ Isle of Media Proprietary 26

Invitation for discussion:

This strategy document is intended to stay ‘in working progress’.

Isle of Media invites all stakeholders to comment, correct, criticise and contribute!

We are looking forward to hear from you!

info@isleofmedia.org

Isle of Media Proprietary 27Annex: Isle of Media Limited Isle of Media Proprietary 28

Isle of Media Limited

Board of Directors Objectives

• 1 To act as a ‘Business Development Agency’ to support the

development and growth of the Isle of Man’s ‘Digital Media Sector’

involved in the television and video value chain:

• 1.1 from content and format production for all types of television and

video formats including also film, games, animation, virtual and augmented

reality,

• 1.2 content aggregation,

• 1.3 content management,

Comprising the largest Broadcast Media related IOM companies the appointed • 1.4 commercial, electronic and physical distribution in all forms like for

Directors and CEO are: instance licensing, broadcasting, streaming, Video On Demand, DVD

• Dr. Richard K. Arning, Chairman (Director Satellite Leasing) sales,

• Dave Beynon (Director Green Light) • 1.5 display, financing, incubating, consulting and promotion of video

and television,

• Peter Duke (Managing Director Duke Marketing)

• 1.6 and related activities,

• Michael Wilson, CEO

by the means of for instance but not limited to:

Advisory Board • 1.7 on- and off-Island marketing,

• Dr. Bettina Brinkmann (Consultant, Lausanne) • 1.8 education,

• Clark Bunting (CEO Digital Media Circus, Mount Clemens) • 1.9 consulting,

• Joan Burney Keatings MBE (CEO Cinemagic Film) • 1.10 participation in definition of public sector policy and

• Catriona Logan (Director of Celtic Media Festival, Glasgow) • 1.11 general participative and advisory activities which support the

development of the sector and its revenue, taxation and employment

• Dr. Frank Hoffmann (SVP Experience & Strategy Video, SES, Munich)

capabilities;

• Mark Rowland (Chairman C21, CEO Formatzone, London)

• 2. to act as an ‘Association’ for the representation and benefit of the

• Simon Kelly (Director Dixcart Management, Isle of Man) Company’s membership and the wider Isle of Man economy and society.

• Simon Nicholas (Director, KPMG LLC, Isle of Man)

Isle of Media Proprietary 29Isle of Man Head Office: For general inquiries:

St George’s Court Email info@isleofmedia.org

Department for Enterprise Web www.IsleofMedia.org

Upper Church Street Twitter @IsleofMedia

Douglas IM1 1EX

Isle of Man

Languages:

France Office:

Villa Rose Blanches English + 44 7711 97 67 20

9 Rue des Vosges Deutsch + 44 7624 29 29 93

06400 Cannes Français + 33 6 76 42 46 26

France

ISLE OF MEDIA LIMITED, incorporated in the Isle of Man

Company Number 131277C, Registered Office: Mountain View Innovation Centre, Jurby Road, Ramsey, IM7 2DZ

Isle of Media Proprietary 30You can also read