Strategic Analysis and Valuation of Wizz Air - CBS Research ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Strategic Analysis and Valuation of Wizz Air Master's Thesis Name: Haris Nogo Student number: 53349 MSc in Economics and Business Administration - Accounting, Strategy and Control Submission date: 15.10.2020 Supervisor: Peter Nordgaard Hansen Number of characters/pages: 144.435/76

1. Executive Summary The purpose of the thesis is to prepare a strategic analysis and valuation of Wizz Air. Wizz Air is the largest low-cost airline in Central and Eastern Europe and has seen enormous growth over the years, which has made Wizz Air one of the ten largest airlines in Europe. The Covid-19 pandemic has however led to a declining demand for air travel, which has affected Wizz Air and other airlines. This makes it an interesting case as the pandemic has led to uncertainty within the airline industry. In the strategic analysis, well-known strategic frameworks have been used, such as PESTLE, Porter's Five Forces, VRIO and SWOT. Based on these models, the strategic analysis revealed that the Covid- 19 pandemic has a major impact on the external factors, such as the closure of borders, recession in countries and changing work habits. All these factors can affect the demand for air travel. The analysis furthermore also revealed that the customers have a high bargaining power as they are not loyal to a particular airline, which is why competition was considered to be fierce among low cost and full fare airlines. Finally, Wizz Air's strong balance sheet was considered to have a competitive advantage in these difficult times, as they have the best liquidity among all airlines in Europe. The financial analysis was based on the historical accounts where it was revealed that Wizz Air has performed really well within the last five years. Based on the strategic and financial analysis, a forecast was prepared. Based on the forecast, the share price was estimated at 29.25 Euros in the DCF model. The share is estimated to be overvalued by 20% in comparison to the share price from October 1st, 2020. The estimated value in the DCF-model was compared with the value estimates from the relative valuation approach, where the multiples indicated a value of between 38.18 and 43.59 Euro per share. Subsequently, a sensitivity analysis was performed, which revealed that Wizz Air's value estimate is very sensitive to even small changes in WACC, terminal growth rate, fuel cost or lease depreciation. The scenarios revealed that if a recovery occurs earlier than in the DCF model, it will lead to a higher share price, while a slower recovery will result in a lower share price. The perspectivation highlighted factors, such as introduction of Monte Carlo simulation in the DCF- model, impact on a change in accounting policies on the value estimate and the value of synergy effects, that could have been incorporated to strengthen the analyses. 1

Table of Contents 1. Executive Summary ........................................................................................................................ 1 2. Introduction .................................................................................................................................... 5 2.1 Research question .................................................................................................................... 6 2.2 Methodology ............................................................................................................................ 6 2.2.1 Limitations ......................................................................................................................... 6 2.2.2 Data collection ................................................................................................................... 8 2.2.3 Structure of the thesis ....................................................................................................... 8 3. Theory ............................................................................................................................................. 9 3.1 Strategic analysis ...................................................................................................................... 9 3.1.1 PESTLE ................................................................................................................................ 9 3.1.2 Porter's Five Forces.......................................................................................................... 10 3.1.3 VRIO ................................................................................................................................. 10 3.1.4 SWOT ............................................................................................................................... 11 3.2 Financial analysis .................................................................................................................... 11 3.2.1 Reformulation .................................................................................................................. 11 3.2.2 Profitability analysis ......................................................................................................... 12 3.2.3 Forecasting ...................................................................................................................... 12 3.2.4 Valuation.......................................................................................................................... 13 4. Wizz Air ......................................................................................................................................... 14 4.1 History of the airline ............................................................................................................... 14 4.2 Wizz Air’s future expectations ................................................................................................ 14 4.3 Strategy................................................................................................................................... 15 4.4 Business Model ....................................................................................................................... 15 4.5 Organizational structure ......................................................................................................... 16 4.6 Shareholder structure............................................................................................................. 16 4.7 Share performance ................................................................................................................. 16 4.8 Peer Group.............................................................................................................................. 18 4.8.1 Ryanair Group .................................................................................................................. 18 4.8.2 EasyJet ............................................................................................................................. 19 5. Strategic analysis .......................................................................................................................... 20 5.1 Business environment ............................................................................................................ 20 5.2 PESTLE..................................................................................................................................... 21 5.2.1 Political ............................................................................................................................ 21 5.2.2 Economical....................................................................................................................... 23 2

5.2.3 Social and cultural factors................................................................................................ 25 5.2.4 Technological factors ....................................................................................................... 28 5.2.5 Legal factors ..................................................................................................................... 28 5.2.6 Environmental factors ..................................................................................................... 29 5.2.7 Summary of the PESTLE analysis ..................................................................................... 30 5.3 Porter’s Five Forces ................................................................................................................ 31 5.3.1 Threat of new entrants .................................................................................................... 31 5.3.2 Threat of substitutes........................................................................................................ 32 5.3.3 Bargaining power of customers ....................................................................................... 33 5.3.4 Bargaining power of suppliers ......................................................................................... 34 5.3.5 Competitive rivalry .......................................................................................................... 37 5.3.6 Summary of Porter’s Five Forces ..................................................................................... 39 5.4 VRIO ........................................................................................................................................ 39 5.4.1 Physical resources............................................................................................................ 40 5.4.2 Financial resources .......................................................................................................... 40 5.4.3 Human resources ............................................................................................................. 42 5.4.4 Intangibles ....................................................................................................................... 42 5.4.5 Summary of the VRIO analysis ......................................................................................... 44 5.5 SWOT ...................................................................................................................................... 44 6. Financial analysis .......................................................................................................................... 46 6.1 Quality of the published accounts .......................................................................................... 46 6.2 Reformulation ......................................................................................................................... 47 6.2.1 Reformulation of income statement ............................................................................... 47 6.2.2 Reformulation of balance sheet ...................................................................................... 49 6.3 Profitability analysis ................................................................................................................ 50 6.3.1 WACC ............................................................................................................................... 51 6.3.2 Capital structure .............................................................................................................. 51 6.3.3 Required rate of return on equity ................................................................................... 52 6.3.4 Required rate of return on debt ...................................................................................... 54 6.3.5 Calculation of WACC ........................................................................................................ 55 6.3.6 EVA .................................................................................................................................. 55 6.3.7 Summary .......................................................................................................................... 56 7. Forecasting ................................................................................................................................... 57 7.1 Budget period ......................................................................................................................... 57 7.2 Forecast .................................................................................................................................. 58 7.2.1 Passenger growth in terminal period .............................................................................. 62 8. Valuation ...................................................................................................................................... 63 8.1 DCF-model .............................................................................................................................. 64 8.2 Relative valuation approach ................................................................................................... 64 3

8.3 Summary of value estimates .................................................................................................. 66 8.4 Sensitivity analysis .................................................................................................................. 67 8.4.1 Change in WACC and terminal growth rate ..................................................................... 67 8.4.2 Increase in passenger growth .......................................................................................... 68 8.4.3 Increase in fuel cost ......................................................................................................... 69 8.4.4 Summary .......................................................................................................................... 70 9. Scenario analysis........................................................................................................................... 71 9.1 Scenarios................................................................................................................................. 71 9.1.1 Pessimistic scenario ......................................................................................................... 71 9.1.2 Optimistic scenario .......................................................................................................... 72 9.2 Impact on share price ............................................................................................................. 73 10. Conclusion .................................................................................................................................. 74 11. Perspectivation ........................................................................................................................... 76 12. Bibliography ................................................................................................................................ 77 13. Appendix ..................................................................................................................................... 83 4

2. Introduction The airline industry in Europe has seen many bankruptcies in recent years, where airlines such as Air Berlin, Monarch and Wow Air had to discontinue operations (Reuters, 2020A). However, there have also been some acquisitions and mergers at the same time, where the largest airlines in Europe have acquired smaller airlines. Ryanair's CEO, Michael O'Leary estimates that the airline market will be even more consolidated in the next five years, and that the top five airlines in Europe will have a 80% market share, while he also at the same time predicts that Wizz Air will be acquired by Lufthansa (Turvill, 2019). During the Covid-19 pandemic, the airline industry has been very challenged due to closed borders, closed airports and entry restrictions to different countries, that has made it difficult to operate scheduled flights. Therefore, some airlines had to permanently suspend their operations and ground their entire fleet, while other airlines have set up an emergency traffic program to bring stranded passengers home and secure an air bridge to the most important destinations and for transport of protective equipment to combat the Covid-19 pandemic. During the Covid-19 pandemic, Wizz Air had to cancel several thousand flights, lay off 1,000 employees and ground almost all of their aircrafts (Finlay, 2020A). As a result of the Covid-19 pandemic, the investment bank HSBC estimates that a consolidation among European airlines will take place faster than initially assumed (Cirium, 2020). Wizz Air's CEO, József Váradi, has the same opinion and believes that the airline industry will be consolidated within 6 to 12 months (Maceda, 2020). With prospects of consolidation and acquisitions among European airlines, and the possibility of bankruptcies as a result of the uncertainty within the airline industry, the purpose of this thesis is to perform a valuation of Wizz Air in the case of a possible acquisition interest from another European airline, such as Lufthansa, which has previously indicated interest in acquiring Wizz Air (ch-aviation, 2014). In addition to this, a renewed interest from Lufthansa in acquiring Wizz Air may be on the way (Bomberg, 2019). 5

2.1 Research question With the prospects of a consolidation in the airline industry in Europe and a possible acquisition interest of Wizz Air from another airline, this leads to the following research question in the thesis. What is the fair value of Wizz Air and how will different air travel demand recovery scenarios affect the share price? In order to answer the research question, a selection of strategic and financial frameworks will be applied in the analysis. The strategic analysis will provide an insight into which internal and external conditions that affect the airline industry. The financial analysis will examine Wizz Air's profitability through a review of its historical financial performance. Based on the conclusions that have emerged from the strategic and financial analysis, a forecast will be prepared, which will ultimately lead to a valuation of Wizz Air. The estimated value will be compared with other value estimates and a sensitivity analysis will be prepared to examine how sensitive the estimated value is to changes in input factors. Finally, different scenarios will be presented, which will lead to a discussion of the effect that different recovery scenarios will have on the share price. 2.2 Methodology The following section will describe the limitations of the thesis, the data collection as well as the structure of the thesis will be outlined. 2.2.1 Limitations In the thesis, several different assumptions have been taken, which has led to the following limitations. This thesis is only based on publicly available data and secondary literature. Therefore, all other analysts also have access to the same information. The cut-off date for the thesis is set for October 1st, 2020. This means that all relevant information after this date will not be included in the thesis. 6

While Wizz Air operates in several different regions, the focus in the thesis is on the European airline industry in the strategic analysis, as Wizz Air's presence is largest in this region. The annual accounts from 2020 have been prepared in accordance with IFRS 16, but since the previous accounts from 2016-2019 have been prepared in accordance with IASB 17, it has been decided to reformulate the annual accounts from 2020 from IFRS 16 to IASB 17 to create consistency in the historical accounts. Wizz Air's accounts are published in Euro, while the share is traded in British pounds. Therefore, in this thesis, it has been decided to use exchange rates for the selected days instead of having a constant exchange rate throughout the thesis. This means that the following exchange rates are used in the thesis. • 31.03.2016: 1.262 GBP/EUR • 31.03.2017: 1.1785 GBP/EUR • 31.03.2018: 1.1376 GBP/EUR • 31.03.2019: 1.137 GBP/EUR • 31.03.2020: 1.1247 GBP/EUR • 01.10.2020: 1.1029 GBP/EUR This will lead to the estimated share price being calculated in Euros instead of in British Pounds. The DCF model is only used in the thesis of the present value approaches that exist. Other present value models would lead to the same value and therefore it is not considered necessary to include additional present value models in the estimation of the value of Wizz Air. The different recovery scenarios will be based on a pessimistic and optimistic scenario in relation to when a recovery will take place. Therefore, only the variable passenger growth changes in the two scenarios, while all other variables remain the same as in the DCF model. 7

2.2.2 Data collection In this thesis, both primary and secondary literature have been used. All data is publicly available. The primary literature consists of annual reports, articles, reports, etc. The secondary data consists of textbooks. Data used in calculations is retrieved from Damodaran, Yahoo Finance, Infront Analytics and OECD. 2.2.3 Structure of the thesis The structure of the thesis follows a top down approach and is shown in figure 1. Figure 1: Structure of the thesis Executive Summary, introduction & theory Wizz Air Strategic analysis Financial analysis Forecasting Valuation Scenario analysis Conclusion & perspectivation Source: Own creation 8

3. Theory This thesis is primarily aimed at professional and semi-professional investors, as well as other people with a background in accounting or finance and who are interested in gaining knowledge about the theoretical value of Wizz Air. Therefore, it has been assumed that those who read this thesis have a strong insight into the literature within the concepts of business valuation and therefore the theories used to analyse and evaluate Wizz Air are only outlined in short terms. 3.1 Strategic analysis The strategic analysis is the first part of a valuation and it aims to examine whether current and historical performance will continue in the future. Historical performance tends to repeat itself, but it’s is not always the case. Some companies may have abnormal profits or growth because they have monopoly status or because the company has just launched a product that has proven to be successful. Other companies may be in a turnaround process to improve profits (Petersen, Plenborg, & Kinserdal, 2017, p. 268-269). Therefore, in the strategic analysis, well-known theories from the literature will be used to analyse the economic cycle of the industry, as well as the non-financial value drivers that may affect Wizz Air’s future profit and risk. 3.1.1 PESTLE The first model from the literature that will be used in the strategic analysis is the PEST model, which aims to identify macro factors that can affect Wizz Air’s cash flow and risk. PEST stands for political, economic, social and technical factors. In a macro analysis, these factors are investigated. However, it is important to emphasize that the list is not exhaustive and there may be more factors than just the four that can affect the company’s cash flow and risk (Petersen, Plenborg, & Kinserdal, 2017, p. 270). Therefore, several versions of the PEST model have been prepared subsequently, where additional factors have been added. One of the models is the PESTEL or PESTLE model, which takes into account environmental and legal factors. In addition, there is also the STEEPLE model, where corporate social responsibility is included as a factor and the STEEPLED model, which includes the demographic factor (Sammut-Bonnici & Galea, 2015, p. 1). For the valuation of Wizz Air, it has been decided to use the PESTLE model, which is the extended model of the PEST model, because it is assessed that environmental and legal factors may affect the airline industry. Although the PESTLE 9

model takes into account six different macro factors that can affect Wizz Air's cash flow and risk, the model still has some limitations. This is due to the fact, that there might be a probability that the model doesn´t capture all the factors that might affect the airline industry. 3.1.2 Porter's Five Forces The second model that will be used in the strategic analysis is Porter's Five Forces, which examines industry-specific factors and risk that may affect a company's margin. By using the five forces, it is possible to analyse how attractive an industry is and whether it is possible to achieve returns that are the same or greater than the cost of capital. There are various parameters that affect how attractive an industry is and if there is a lot of competition in an industry, this might reduce the possibility of earning abnormal returns (Petersen, Plenborg, & Kinserdal, 2017, p. 271). The five forces in the model are potential entrants, rivalry, substituting products, bargaining power of buyers and bargaining power of suppliers (Petersen, Plenborg, & Kinserdal, 2017, p. 272-273). These five forces will be used to analyse the competitive situation in the airline industry as well as the possibility of achieving acceptable returns. There are, however, also drawbacks to Porter's Five Forces and one of them is, that there are many alliances between airlines in the airline industry and Porter's Five Forces does not take this into account. 3.1.3 VRIO The third model that will be used in the strategic analysis is the VRIO model, which analyses the unique resources and capabilities that a company possesses. This model was introduced in 1991 by Barnley and is useful to use when assessing which resources that provide the company with competitive advantages. Companies may be in a possession of physical resources, human resources, financial resources or intangibles. These resources are then assessed in the VRIO analysis, where the resources are assessed in relation to elements such as value, rarity, imitability and organization (Petersen, Plenborg, & Kinserdal, 2017, p. 275). The first letter of the four elements forms the name VRIO and therefore the model has been given its name. The challenge with the VRIO model is to determine the most important resources. Companies have many resources and not all are equally important. Therefore, the most important resources at Wizz Air will be compared with their peer group to better assess the strength of the resources. 10

3.1.4 SWOT The strategic analysis ends with a SWOT, where the conclusions from PESTLE, Porter's Five Forces and VRIO are summarized in a SWOT matrix. In this matrix, the company's strengths, weaknesses, opportunities and threats are summarized (Petersen, Plenborg, & Kinserdal, 2017, p. 276). The conclusions from PESTLE and Porter's Five Forces are presented in the external factors in the matrix, in which the company's opportunities and threats are summarized. In contrast, the conclusions from the VRIO analysis are presented in the internal factors, where the company's strengths and weaknesses are summarized. 3.2 Financial analysis Following the strategic analysis, a financial analysis of Wizz Air will be prepared, in which the historical accounts will be analysed. The financial analysis will be prepared based on the approach from the book Financial Statement Analysis: Valuation, Credit Analysis, Executive Compensation written by Petersen, Plenborg & Kinserdal (2017). This book is widely used at Copenhagen Business School, where the book is used as the primary literature on several MSc directions in the course Financial Statement Analysis. Therefore, it is not considered necessary to include additional literature to prepare the financial analysis, as this book is based on well-known theories from the field of finance and accounting. 3.2.1 Reformulation The first step in the financial analysis is to reformulate the historical accounts. By reformulating the accounts and turning them into analytical income statements and balance sheets, it is possible to calculate the financial ratios, where the financial ratios are used to assess a company's profitability. The reason why the accounts need to be reformulated and made analytical is because the value creation in a company is primarily created through operational activities (Petersen, Plenborg, & Kinserdal, 2017, p. 107). Therefore, it is important to separate operational activities from financing activates in the reformulation of income statements and balance sheets of Wizz Air. 11

3.2.2 Profitability analysis After making the financial statements analytical, it is possible to prepare a profitability analysis of Wizz Air. Using several different financial ratios, it is possible to assess a company's profitability, growth and risk. The different financial ratios are important indicators of how a company is performing (Petersen, Plenborg, & Kinserdal, 2017, p. 101). The profitability analysis will follow the structure from the Du Pont model, which can be seen in figure 2. Figure 2: Structure of the profitability analysis – Du Pont model Economic Value Added (EVA) Return on Weighted Invested capital average cost of (ROIC) capital (WACC) Turnover rate of Profit margin invested capital Source: Own creation / (Petersen, Plenborg, & Kinserdal, 2017, p. 141) As shown in figure 2, Wizz Air's operating profitability will be assessed through financial ratios, such as ROIC, profit margin and turnover rate of invested capital. 3.2.3 Forecasting After analysing the historical accounts, the next task in the financial analysis is to forecast future earnings of Wizz Air. Forecast is forward looking and reflects expectations for future earnings. Therefore, forecast is also one of the most important parts of the financial analysis, as the key points from the strategic analysis and the analysis of the historical accounts is used to predict possible development in future earnings. The connection between the strategic value drivers and the financial value drivers can be seen in figure 3. 12

Figure 3: Linkage between strategic and financial value drivers Strategic value drivers (the input factors) Financial value driver and financial performance (the out-put factors) Forecasted cash flows, potential and risk Firm value Source: Own creation / (Petersen, Plenborg, & Kinserdal, 2017, p. 253) As shown in figure 3, the strategic value drivers are primary those that create value to a company. The strategic value drivers can be seen as input factors that a company can influence to improve value within a company. These input factors can be measured by their financial performance. It is therefore important to understand how the connection between the strategic and financial value drivers when forecasting future cash flow. 3.2.4 Valuation The valuation will be based on an equity-oriented approach, where the thesis will try to assess the intrinsic value of Wizz Air using financial information (Petersen, Plenborg, & Kinserdal, 2017, p. 25). In this connection, there are several different valuation approaches that can be used. In this thesis, it has been decided to use the present value and relative valuation approach. In the present value approach, the discounted cash flow model will be used to estimate the enterprise value and equity value (Petersen, Plenborg, & Kinserdal, 2017, p. 27). In the relative valuation approach, the multiples EV/IC and EV/EBITDA will be used to estimate the enterprise value, while the multiple P/B will be used to estimate the equity value (Petersen, Plenborg, & Kinserdal, 2017, p. 27). Finally, the two different value estimates from the present value and relative valuation approach will be compared. 13

4. Wizz Air This part of the thesis will present Wizz Air's history, vision, strategy, business model, organizational structure, share performance and peer group. In order to perform an in-depth strategic analysis and valuation of Wizz Air, it is important to know the above elements as they ensure knowledge of how the company has evolved throughout history, where the company's strategic focus lies and what contributes to create future value. 4.1 History of the airline Wizz Air was founded in London in 2013 by József Váradi and a team of six people with experience from the airline industry (Wizz Air, 2019A). József Váradi came from a position as former CEO of the state-owned airline Malév Hungarian Airlines, which went bankrupt in 2012 (Magnusson, 2018). Wizz Air made its debut on its first flight in 2004 from the Polish city of Katowice to Luton airport in London. In 2006, Wizz Air reached their first milestone with 5 million passengers carried. Only two years later, that number increased to 10 million passengers carried. In 2014, Wizz Air was able to celebrate their first decade with the delivery of aircraft number 50 and with 15 million passengers carried since their first flight. In 2015, the company was listed on the London Stock Exchange after a successful initial public offering. A year later, the airline was named the airline with the best value by a leading magazine in the industry. In 2017, Wizz Air expanded their strategic focus by opening a base at Luton airport in London and founded its subsidiary Wizz UK. in 2018 Wizz Air welcomed aircraft number 100 to their fleet, which was also the year when the airline could celebrate 15 years of operation. In 2019 Wizz Air was the greenest airline, while in 2020 it was voted the best low-cost airline in Europe (Wizz Air, 2019A). 4.2 Wizz Air’s future expectations Due to the Covid-19 pandemic, Wizz Air expects to be challenged in the new financial year for 2021 (Wizz Air, 2020A, p. 6). Although the Covid-19 pandemic has challenged the airline industry, Wizz Air is going to open a base outside Europe, in the city of Abu Dhabi from October 2020, where there initially will be 6 routes to destinations within Europe, the Middle East and Africa (anna.aero, 2020). In addition to opening their first base outside of Europe, Wizz Air expects that the seating capacity will increase by 9% in the financial year 2021 compared to 2020, while they also expect new aircrafts 14

to be delivered, increasing the fleet to 131 aircrafts in 2021. However, Wizz Air does not expect a positive development in the profit margin in the new financial year for 2021. In continuation of this, Wizz Air is currently unable to comment on what they expect the net profit to be in the new financial year due to uncertainty within in the airline industry as a result of the Covid-19 pandemic (Wizz Air, 2020A, p. 12). 4.3 Strategy Since its inception, Wizz Air's strategic focus has remained the same (Wizz Air, 2020A, p. 5). Wizz Air's strategic focus is on emerging markets in Central and Eastern Europe, but they are as well focused on strengthening their position in Western Europe, since they have opened a new base in London. Wizz Air’s goal is to keep costs as low as possible, in order to offer the best fares. They try to fulfil this goal by ordering new aircrafts, that are much more efficient and where the seating capacity is increased. This will make it possible to transport more passengers at the lowest possible cost (Wizz Air, 2019B, p. 7). With an order of 268 new aircrafts, the focus is also on reducing emissions and offering customers as many routes as possible without compromising on safety and other measures. In addition, their new strategic focus is also to expand their business operations to the United Arab Emirates, where they are in the process of establishing a new airline (Wizz Air, 2020A, p. 5). 4.4 Business Model Wizz Air's business model is built on an ultra-low-cost principle. The reason why Wizz Air can offer the best fares is because they have taken steps to reduce costs and simplify their business model. First and foremost, they offer direct bookings through their website or their app and therefore they avoid expensive intermediaries, such as travel agencies or other distribution channels that sell tickets on behalf of the airlines. In addition, Wizz Air also does not have more classes on board their aircraft, as they only have a single class. This creates equal value for all passengers (Wizz Air, 2020A, p. 4). Wizz Air has a unified fleet of Airbus aircraft, operating with a mix of Airbus A320 and A321 aircraft (Wizz Air, 2020B). In addition, Wizz Air flies to both primary and secondary airports and the choice of airport is of great importance for maintaining a low-cost base (Wizz Air, 2020A, p. 4). Wizz Air does, therefore not fly to airports that have high fees or were the demand is fluctuating, such as 15

Zagreb Airport in Croatia, which has far too high costs for Wizz Air to be interested in opening flights from the Croatian capital (EX-YU Aviation News, 2018). 4.5 Organizational structure Wizz Air's parent company is Wizz Air Holdings plc, which is formally located in Jersey (Wizz Air, 2020C). This company owns a number of subsidiaries. The largest subsidiary owned by the parent company is Wizz Air Hungary with a 100% ownership interest. This subsidiary is the main airline operator and the company that operates all the flights except those departing from London-Luton Airport. The flights departing from London-Luton Airport are operated by Wizz Air UK, which is also 100% owned by the parent company. In addition to this, Wizz Air is in the process of establishing a new airline in Abu Dhabi, United Arab Emirates. This airline will be owned by Wizz Air Abu Dhabi, of which Wizz Air Holdings plc will have a 49% stake. Besides this, the parent company also has 2 crew companies, one located in Bosnia-Herzegovina and the other in Moldova. These are also 100% owned by the parent company. Finally, the company also has a pilot academy in Poland, which is 100% owned by the parent company and a few companies located in the Netherlands, Poland, Ukraine and Hungary, but these are currently dormant (Wizz Air, 2020A, p. 132). 4.6 Shareholder structure Wizz Air Holdings PLC has 85.44 million outstanding shares (Financial Times, 2020A). As a legal requirement, Wizz Air is obligated to publish key shareholders with a shareholding of more than 3% of the company's ordinary shares. As of March 31, 2020, the largest shareholder was indigo Hungary LP with a shareholding of 13.5% or 11,515,509 shares. The second largest shareholder was Fidelity Management & Research Company with a shareholding of 6.7% or 5,708,444 shares. The third largest shareholder was Fidelity International with a shareholding of 6% or 5,123,163 shares. The seven largest shareholders had a shareholding of 42.2% or 36,045,653 shares (Wizz Air, 2020A, p. 33). 4.7 Share performance Wizz Air has been listed on the London Stock Exchange since February 25th, 2015 following a successful IPO where the share price was set at 1.150 Pence Sterling (London Stock Exchange, 2015). 16

Wizz Air has a market capitalization £ 3.38 bn and is a part of the FTSE 250 index, which consists of the 101st to 350th largest companies listed on the London Stock Exchange (Hargreaves Lansdown, 2020A). The opening price of the share was 1.250 Pence Sterling and already on its first trading day the share rose. Since then, the share has generally been rising, as can be seen in figure 4. In the first year of the stock price's maturity, the stock price reached its highest level for 2015 on October 5th, when the stock price closed at 2.058 Pence Sterling per share. After that, there has generally been a downward trend until June 27th, 2016, when the share price closed at 1.415 Pence Sterling per share. After that, the share price has again been rising with few fluctuations until 2017, after which the share price saw a big increase and closed at 3.797 Pence Sterling for a share on July 18th, 2018. After that there has been a decline and the share price closed at a price of 2.363 Pence Sterling on October 10th, 2018. This is probably due to the uncertainty of Brexit and its consequences for companies as the United Kingdom is no longer a part of the European Union. This may also affect Wizz Air, because Wizz Air has a subsidiary in the United Kingdom named Wizz UK with a base at Luton airport in London. After that period, there has been an increasing trend in the share price over the next years and Wizz Air closed at a price of 4.496 Pence Sterling on February 12th, 2020. This is the highest price at which the stock has been traded at in its history. As a result of the Covid-19 outbreak around the world and the declaration of the Covid-19 pandemic worldwide, the pandemic has also affected the stock markets. In a market with great uncertainty and volatility, the share price saw a decline and closed at a price of 2.006 Pence Sterling for a share on March 19th, 2020. Following the big drop, the stock price rose again and was traded at a price of 3.174 Pence Sterling as of October 1st, 2020. Figure 4: Development in the share price Source: (Hargreaves Lansdown, 2020B) 17

4.8 Peer Group Wizz Air flies to several destinations within Europe, as well as to some destinations in Central Asia, North Africa and the Middle East (Wizz Air, 2020D). Although Wizz Air has expanded in Western Europe in the recent years, their strategic focus is still on growing markets in Central and Eastern Europe (Wizz Air, 2019B, p. 7). Therefore, in the selection of the peer group, the focus will be on comparative airlines operating in Central and Eastern Europe. Wizz Air was the leading low-cost airline in Central and Eastern Europe in the period from April 2019 to March 2020 with a market share of 39.6% in the low-cost sector. The closest competitors were Ryanair Group, which had a market share of 31.9%, followed by EasyJet, which had a market share of 6.1% (Wizz Air, 2020A, p. 8). If all airlines were involved instead, then Wizz Air would still have the largest market share with 17.5%. Wizz Air is followed by Ryanair Group with a market share of 14.1% and Lot Polish Airlines with a market share of 6.2% (Wizz Air, 2020A, p. 8). As can be seen from the market shares in Central and Eastern Europe, then Ryanair Group, EasyJet and LOT Polish Airlines are the closest competitors to Wizz Air. While Ryanair Group and EasyJet use the same business model and operate in the low-cost sector, LOT Polish Airlines is a full fare airline with a hub strategy. Therefore, in the choice of peer group, it has been decided to only include Ryanair Group and EasyJet, as these airlines are most reminiscent to Wizz Air. 4.8.1 Ryanair Group Ryanair Group was the largest airline in Europe and carried 152.4 million passengers in 2019 (Appendix 1). Ryanair began with their first flights back in 1985, operating on the route between Waterford in Ireland to Gatwick Airport in London with a plane that could only seat 15 people (Ryanair, 2020A). Since then, the airline has expanded significantly and the current strategy they use today dates back to the early 90s, when Ryanair started to copy the same low-cost model from Southwest Airlines, which was the first airline to introduce the low-cost concept in the United States. In the following years, the airline expanded with more routes and bought used Boeing aircrafts. The company was listed in 1997 after a successful IPO. In the period from 1997 to 2019, Ryanair significantly increased its operations, introducing more than 2.100 new routes and opening 86 bases around Europe. Ryanair has also founded 2 start-up airlines in Poland and in the United Kingdom, 18

as well as acquired the Austrian airline Laudamotion and the Maltese airline Malta Air. These airlines are now a part of a low-cost airline group that Ryanair established in the period from 2019 to 2020. Ryanair fly to over 200 destinations and has a fleet consisting of 455 Boeing 737-800 aircraft and 20 Airbus 320, which are distributed among Ryanair and their subsidiaries. By 2024, this number is expected to increase as Ryanair expects to have a fleet of 585 aircraft (Ryanair, 2019, p. 96). 4.8.2 EasyJet EasyJet was the fifth largest airline in Europe and carried 96.1 million passengers in 2019 (Appendix 1). EasyJet was founded in 1995 by 28-year-old Sir Stelios Haji-Ioannou. The first scheduled route went from Luton Airport in London to Glasgow followed by a route to Edinburg. In the following year, EasyJet received their first owned aircraft and scheduled operations from Luton to Barcelona, Nice and Amsterdam. After that things went fast and the airline opened their second base in Liverpool in 1997 and acquired a 40% stake in a Swiss charter airline in 1998, which was later renamed EasyJet Switzerland. In 1999, the airline was listed on the London Stock Exchange following a successful IPO (EasyJet, 2020A). Following the listing in 1999, EasyJet has seen great growth, due to the opening of new bases around Europe. In addition, EasyJet has over the years also acquired other airlines and established a new airline based at the airport in Vienna, which is named EasyJet Europe. Acquisitions by other airlines and the establishment of subsidiaries have contributed to the increased number of bases and aircrafts in the fleet over the years (Diagilev, 2020). 19

5. Strategic analysis In order to be able to prepare pro forma statements, the first task is to carry out a strategic analysis of Wizz Air. The purpose of the strategic analysis is to identify strategic value drivers that affect Wizz Air's future cash flow, potential and risk. The strategic analysis will follow a top-down approach, where Wizz Air's business environment will be examined first. The external environment will then be analysed through PESTLE and Porter's Five Forces. The PESTLE model will contribute in identifying the most relevant macro factors that affect Wizz Air cash flow and risk, while Porter's Five Forces will contribute in identifying the most relevant industry factors that affect Wizz Air's margins. The internal environment will then be analysed through the VRIO model, where Wizz Air's unique resources and capabilities will be found. Finally, the conclusions from the strategic analysis will then be summarized in a SWOT matrix, where Wizz Air's opportunities, threats, strengths and weaknesses will be presented. 5.1 Business environment Wizz Air’s business environment will be examined to assess whether the product is simple or complex and whether the market is simple or dynamic. In relation to the product, then most airlines offer transportation of passengers and goods, while cargo airlines only offer transportation of goods. In terms of complexity, it must be assumed that the product is relatively simple in the airline industry, since the product is transport of passengers from one airport to another. Figure 5: The dynamic of the market and the complexity of the product Market/Product Simple Complex Stable Simple analysis Thorough analysis Simple forecasting Scenario analysis Dynamic Thorough analysis Thorough analysis Scenario analysis Scenario analysis Source: Own creation / (Petersen, Plenborg, & Kinserdal, 2017, p. 270) The market in the airline industry is characterized by being cyclical, as it has been statistically proven several times that demand for travel is correlated with economic growth (Lenoir, 2014). Therefore, 20

the demand for air travel and airline’s earnings will generally be higher when countries have economic growth, as citizens have more money on their hands and a greater desire to travel. The opposite is the case when a country is in a recession, then the demand will also be less and likewise will the airline’s earnings, as citizens now have less money on their hands and a lesser desire to travel. The market is therefore considered to be dynamic. When the product is simple and the market is dynamic, then, according to figure 5, it requires a thorough analysis and scenario analysis. Through a thorough analysis of current and future conditions that may affect Wizz Air, the company's future earnings will be forecasted by a scenario analysis, where several different scenarios will be presented. 5.2 PESTLE In this section, Wizz Air's macro-environment will be analysed through six different factors that may influence Wizz Air's value creation. 5.2.1 Political Wizz Air is very influenced by political conditions in countries where Wizz Air either operates to or have established a base. Wizz Air offers flights to several destination within Europe, Central Asia, North Africa and the Middle East (Wizz Air, 2020D). Among these continents that Wizz Air operates on, there are countries that have experienced political unrest in the recent years. This applies to Ukraine, who has been in a conflict with Russia regarding the Crimean Peninsula. The political conflict between Ukraine and Russia affected Wizz Air. Due to the political unrest, Wizz Air closed its base in Donetsk, Ukraine in April 2014 and Wizz Air's subsidiary, Wizz Air Ukraine ceased operations in 2015 (Wizz Air, 2016, p. 7). Similar conflicts to those in Ukraine may affect Wizz Air's route network in the future. Among them, the political conflict between Armenia and Azerbaijan could possibly affect Wizz Air's routes to these two countries. Since July 12th, 2020, a protracted conflict between Armenia and Azerbaijan has escalated again with several soldiers losing their lives (Reuters, 2020B). As a consequence of the political unrest between Armenia and Azerbaijan, the routes in the neighbouring countries in the Caucasus region, such as Georgia and Russia might be affected as well, if the political unrest is further exacerbated. 21

Another political factor that can affect Wizz Air is Air Traffic Control (ATC) strikes. Wizz Air, like many other airlines, flies over several countries. A flight from one airport to another can lead to an overflight through the ATC of several countries. The purpose of ATC’s is to prevent collisions between aircrafts. In Hungary, where Wizz Air is headquartered, HungaroControl provides air navigation services in the airspace over Hungary and Kosovo (HungaroControl, 2020). To ensure a stable route service without delays or cancellations, Wizz Air and other airlines depend on the countries' ATC to be reliable and well-functioning. However, this is not always the case in Europe, where ATC’s regularly goes on strike (Janzen, 2020). This means that flights are delayed, cancelled or have to be diverted through the airspace of other countries. The consequences of ATC strikes are high. The economic costs associated with ATC strikes do not only affect airlines, but also tourism. A survey conducted by PricewaterhouseCoopers shows that the economic cost was € 10.4 bn in the period between 2010 and 2015, where 6% of airlines' revenue were lost as a result of ATC strikes. Similarly, productivity was lost by 35%, while 59% was due to reduced tourism spending (PwC, 2016A). Although ATC strikes have many economic consequences, it is a political problem. Wizz Air's CEO, József Váradi, believes that the problems are due to lack of international cooperation and strikes (Spero, 2019). The same frustrations are shared by several other airlines, where Wizz Air together with IAG, Ryanair and EasyJet, has sent a complaint about the many strikes over French airspace to the EU Commission and demands political action to solve the problem (Ryanair, 2018). Future losses in revenue and productivity could affect Wizz Air if problems with ATC strikes does not get resolved politically within the EU. A third political factor that has been noticed during the Covid-19 pandemic is border restrictions, which have been introduced by governments in Europe. Due to border restrictions, the demand for air travel has dropped significantly. IATA estimates that air traffic in Europe will see a decrease of around 60% in the number of passengers in 2020 compared to the 2019 level, while IATA also estimates that the same level as in 2019 will not return until 2024 (IATA, 2020A). However, it is difficult to assess how the development will be in terms of number of passengers, as it will depend on whether border restrictions are going to continue or not. This political factor is therefore of great importance for the future growth of the number of passengers. 22

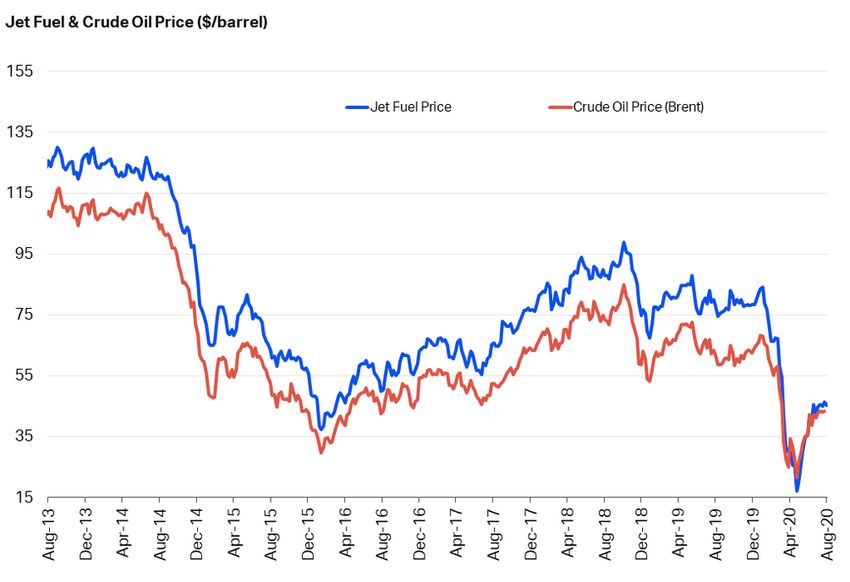

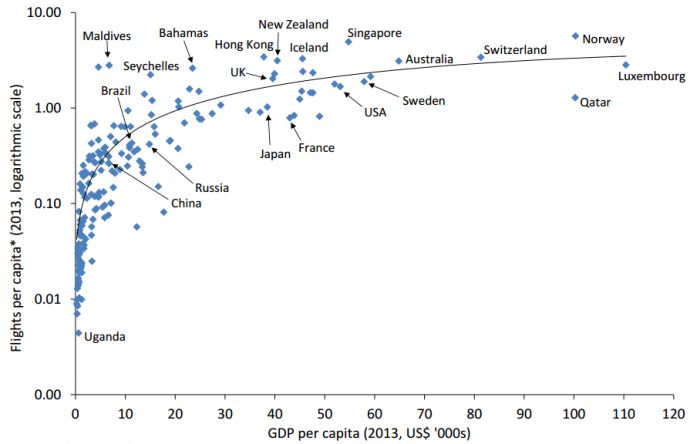

5.2.2 Economical There are many macroeconomic factors that can affect the profitability of Wizz Air and the airline industry. The most used economic performance indicator for a company or industry is the gross domestic product (GDP) per capita (Sammut-Bonnici & Galea, 2015, p. 2-3). For Wizz Air, this is particularly interesting, as it appears from figure 6 that GDP per capita and flights per capita are positive correlated to a large extend. This means that if GDP per capita increases in a country, then the corresponding number of flights per capita will also increase, as the demand for air travel will be higher, because a higher disposable income, most likely will result in more purchased airline tickets. Figure 6: Flights per capita / GDP per capita Source: (Ciesluk, 2019) Another economic factor that can affect Wizz Air is fuel cost, which is also the largest operating expense for Wizz Air. Expenditure on fuel amounted to 876.5 million euros in 2020, or the equivalent of 34.5% of Wizz Air’s total operating expenses (Wizz Air, 2020A, p. 25). Fuel cost is a variable cost, as the fuel cost can change over time. This can be seen in figure 7, where it appears that there have been large fluctuations in both the jet fuel price and the crude oil price in the period from August 2013 to August 2020. At the same time, figure 7 also shows at the same time that the jet fuel price has been higher than the crude oil price from August 2013 to April 2020. From April 2020 to August 2020, the price has been almost identical between jet fuel and crude oil. It is also possible to see 23

from figure 7, that when the jet fuel price increases, the crude oil price also increases and correspondingly when the jet fuel price decreases, then also the crude oil also price decreases. This is why the ratio between jet fuel price and crude oil price is positively correlated. For Wizz Air, large fluctuations in fuel costs can affect Wizz Air's future financial performance. It is, therefore, a common practice for airlines to hedge fuel price and in that way try to avoid large fluctuations in the fuel price. Figure 7: Jet Fuel & Crude Oil Price Source: (IATA, 2020B) A third economic factor that can affect Wizz Air is fluctuations in exchange rates. Wizz Air's financial statements are reported in Euros, but as Wizz Air is an international business, Wizz Air has transactions in more than twenty different currencies. Most payments are however made in US dollars as well as in British pounds, due to their subsidiary in the UK (Wizz Air, 2020A, p. 25). Since Wizz Air makes payments in several different currencies, then Wizz Air is exposed to fluctuations in exchange rates. This could adversely affect Wizz Air's margins in the event of a depreciation of the US dollars or the British pound against the Euro. To reduce this possibility, Wizz Air participates in hedging, which as with fuel cost is a common practice in the airline industry if the airline makes many payments in several different currencies. 24

A fourth economic factor is the impact of Covid-19 on the economy. As a result of the lockdown during the Covid-19 pandemic, many countries have experienced declining GDP, increasing unemployment rates and entered into a recession. The stock markets have been affected and there have been large drops within the markets worldwide, which has resulted in the Dow Jones and FTSE stock indices declining by 23% and 25% respectively in the first quarter of 2020 (BBC, 2020). In addition, unemployment has also increased, as a result of the Covid-19, where countries such as Japan, Germany, the United Kingdom, Canada, France, Italy and the United States have seen an increase in unemployment rates of between 0.6% and 6.7% in 2020 compared to 2019 (Jones, Palumbo, & Brown, 2020). Furthermore, many countries have declared their economy to be in a recession, with the United Kingdom in particular being hit hardest by a 20.4% decline in GDP in the second quarter of 2020 compared to the first quarter of 2020 (Gray & Corcoran, 2020). Hence, increasing unemployment rates, declining GDP and recession in countries where Wizz Air offers flights, may affect the demand for air travel. 5.2.3 Social and cultural factors The majority of Wizz Air's revenue comes from flight operations within the EU, while the remaining part of the revenue comes from countries outside the EU and Europe. In 2020, Wizz Air's revenue from the EU accounted for 2,374.0 million euros, while other (non-EU) revenue was 387.3 million euros (Wizz Air, 2020A, p. 125). Therefore, the demographic development in the EU is therefore an important factor to look at as 86% of Wizz Air's revenue comes from this region. As figure 8 shows, the total population in EU is projected to increase from a population of 447.7 million in 2020 to a population of 449.7 million in 2025. From 2025 until 2100, the population in EU is estimated to decline from a population of 449.7 million in 2025 to a population of 416.1 million in 2100. Figure 8: The EU’s population projected up to 2100 (in millions) 448 450 447 441 433 424 419 417 416 2020 2025 2040 2050 2060 2070 2080 2090 2100 Source: Own creation / (Eurostat, 2019) 25

You can also read